CWCO - Consolidated Water Is Capturing Market Share In Infrastructure Spending

2023-06-21 18:06:15 ET

Summary

- Despite a large run up in price, CWCO still looks undervalued.

- I see significant growth ahead as infrastructure spending increases.

- CWCO has expertise and technology which make them a competitive bidder on projects.

The Buy Thesis

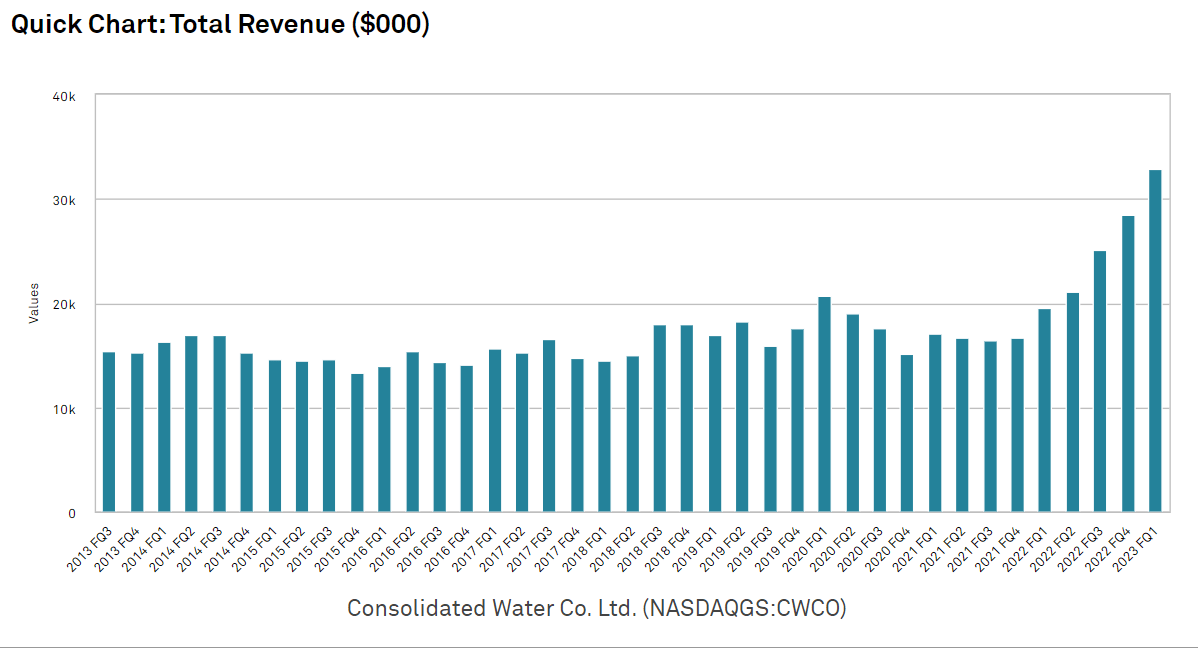

For a small ($320 million enterprise value) company, Consolidated Water ( CWCO ) has a tremendous amount of revenues coming in. As they are among the leaders in water treatment and desalination, I anticipate further waves of new projects as the water shortages worsen in the southwestern U.S. Given the growth outlook, I find CWCO to be significantly undervalued.

This article will discuss the following:

- Recent surge of CWCO contracts

- Impetus for future projects

- CWCO’s positioning to capture those projects

- Valuation

- Risks to CWCO

Recent contracts

Historically, CWCO has derived much of its revenue from the Cayman Islands where they have a longstanding position as the primary provider of fresh water which they do through desalination. This is a stable revenue base which grows year over year with population and tourism. On 5/10/22, CWCO announced an additional $20 million desalination plant they will design, build, and operate in the Cayman Islands.

More recently, however, activity has shifted to the U.S.

- $82 million contract in May of 2022 for a 4-million gallon per day water treatment facility in Arizona

- $49.2 million contract commencing October 2022 to maintain and operate two water treatment facilities in southern California.

- $204 million contract announced 6/6/23 to design, build, operate and maintain a desalination plant in Hawaii. $149.6 million during the 24-month construction followed by $2.7 million annually for the 20 year initial term.

That is a total of $355.2 million incremental revenue signed in the last 13 months. CWCO has historically traded at a discounted multiple because so much of its revenue was from overseas where governments are not always as reliable of payers. The Cayman Islands pay what they owe CWCO, but are frequently late while Mexico backed out on a contract to have CWCO build desalination plants.

U.S. government revenue is the closest thing a company can get to guaranteed revenue and $335.2 million of CWCO’s signings in the last 13 months were in the U.S. That is an enormous amount of new activity for a company with an enterprise value of $320 million, yet I believe it is just the tip of the iceberg.

The revenue growth seen so far is largely a result of increased water usage following the Cayman Islands reopening after the COVID shutdown.

{kind=link}

The announced projects will hit revenues over the next couple years with the operating revenues going out through the next 20 years.

Impetus for future projects

The former abundance of fresh water in the U.S. has kept the total addressable market small, but water needs are expected to expand while the availability of fresh water declines. In a previous CWCO article we more fully went into the water crisis, but the source of the problem is the rapidly dropping water level of Lake Mead.

USlakes.info

As this is the primary water source for Arizona, California and much of the southwestern U.S., its water level approaching a critical level necessitates finding new sources of water. There are three primary ways to solve the crisis:

- Better water treatment facilities

- Recycling infrastructure and policies (Vegas has done a great job with this)

- Desalination to make more fresh water

A wave of infrastructure spending has already commenced, partially funded by the Inflation Reduction Act along with other more directly water related government funding.

The type of project varies greatly by location. In more inland areas such as Arizona and Nevada, conservation and treatment efforts are most effective (such as the Arizona project CWCO is doing) while in more coastal or Island areas, desalination is the best option (such as CWCO’s Hawaii and Cayman Islands projects).

Why CWCO will capture the lion’s share of new projects

Despite its small size, CWCO has a tremendous amount of intellectual property and expertise including proprietary designs for plants and individual parts. This allows CWCO to be a one-stop solution to a location’s water problems which can be seen in the recent Hawaii and Cayman Islands projects. CWCO is designing, developing, operating and maintaining these plants. CWCO even manufactures the parts through its AEREX subsidiary.

Full vertical integration makes CWCO a compelling bidder on new projects.

Over time CWCO has expanded its repertoire

In 2019, CWCO bought 51% of PERC Water which specializes in water treatment and re-use infrastructure. At the time, PERC was a small company but as part of CWCO it now has access to more capital along with other vertical integration synergies. Its revenues have shot up with the California, Hawaii and Arizona projects all coming through PERC.

In August of 2022 CWCO acquired another 10% of PERC and on 1/9/23 they bought the final 39% for $7.8 million. That is a massive amount of new revenue coming in for a relatively small acquisition price.

Desalination expertise

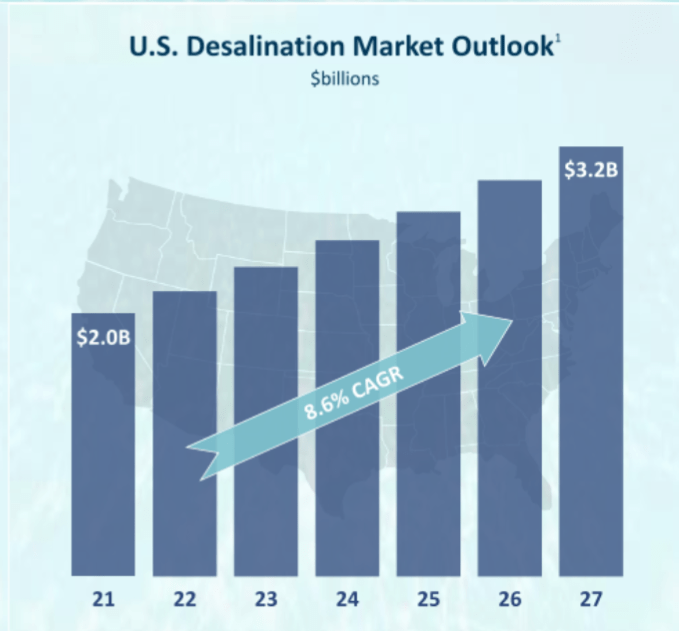

So far, the desalination market in the United States is tiny with annual revenue of just over $2 billion.

{kind=link}

Most of the world, however, is not as fortunate as the U.S. in terms of access to fresh water. For other countries, desalination is salvific and it is one of few areas where foreign technology is arguably more advanced than the U.S. versions. However, since water is such a crucial piece of infrastructure there are security concerns about allowing foreign entities to control the water infrastructure.

CWCO bridges that gap. The U.S. government is comfortable making contracts with CWCO yet having operated for decades in areas where desalination is essential, CWCO has the cutting edge technology.

Overall, there are three reasons why CWCO will get a large portion of the upcoming infrastructure contracts:

- Expertise and proprietary technology

- Vertical integration

- Precedence in contracts with the U.S.

Valuation

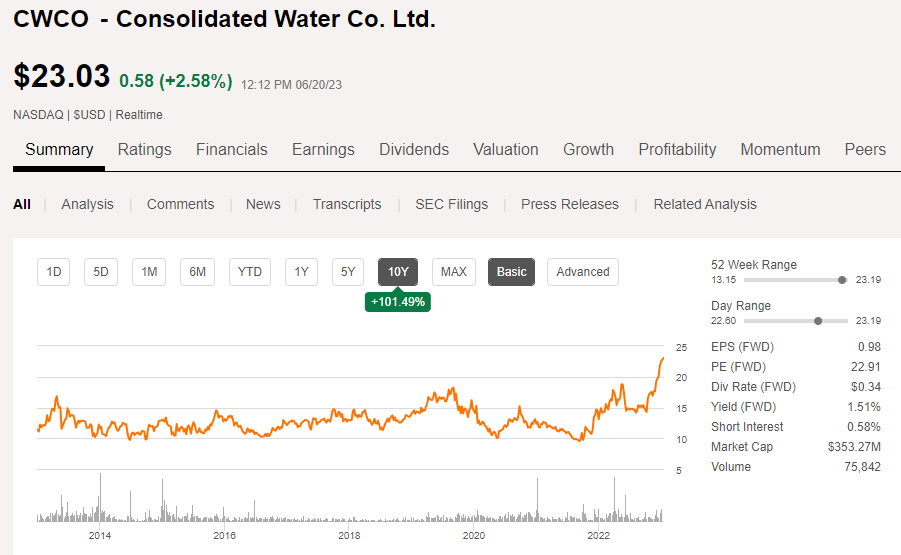

CWCO has recently hit a 10-year high.

{kind=link}

As a value investor it is difficult for me to continue holding stocks at 10-year highs, but despite the way the chart looks, fundamental valuation suggests CWCO is still opportunistically cheap.

Even at the appreciated price its valuation is roughly in line with the S&P at 23X earnings, yet CWCO’s growth potential is far greater. If contracts continue coming in at a pace similar to the last 13 months, CWCO can grow rapidly at a pace that justifies a much higher multiple.

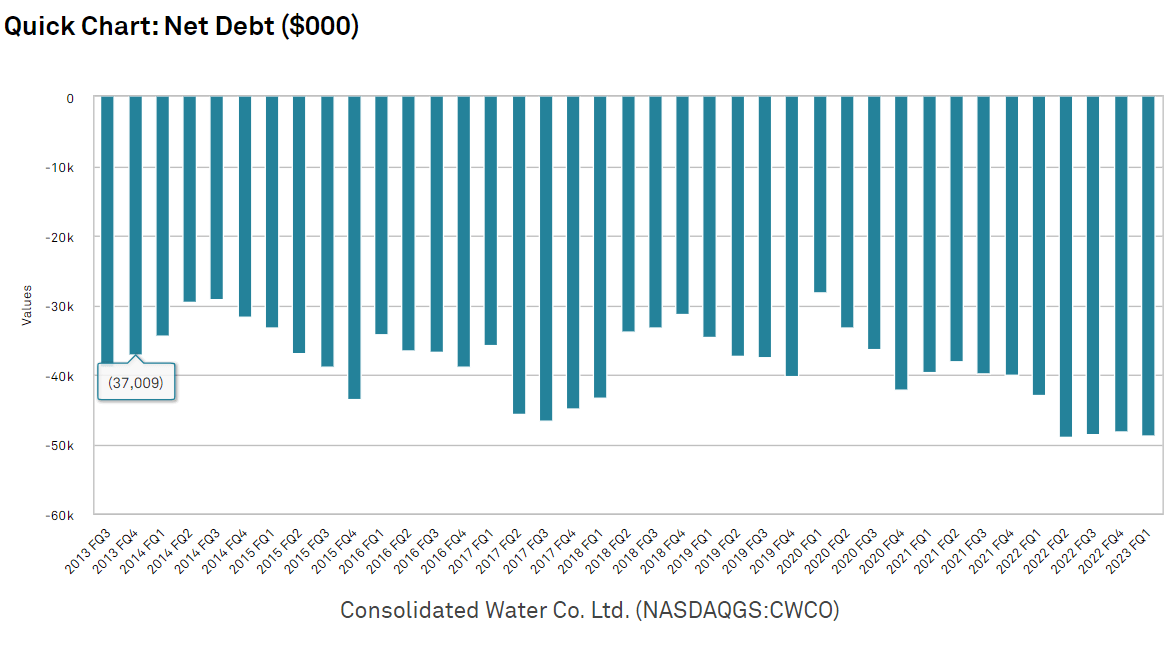

Another aspect that makes CWCO cheaper than its raw price to earnings is its debt, or rather lack thereof.

{kind=link}

With approximately negative $50 million net debt, CWCO is carrying about $50 million in cash in excess of their debts.

Thus, CWCO’s enterprise value is actually lower than its market cap. With 2023 consensus estimated EBITDA of $23.8 million, CWCO is trading at only 13.4X EBITDA.

That strikes me as a great value given the growth prospects.

For further details see:

Consolidated Water Is Capturing Market Share In Infrastructure Spending