CWCO - Consolidated Water: Throwing Off High Rates Of Return On Small Capital Requirements Rate Buy

2023-09-07 09:48:46 ET

Summary

- Consolidated Water is a capital-light compounder with attractive economics in the water industry.

- CWCO has experienced a sharp rebound in its core tourism markets, leading to high rates of return and attractive cash flow for shareholders.

- The company's Q2 FY'23 results showed significant growth across all business lines, and it has strong long-term revenue drivers in its services and manufacturing segments.

- Net-net, rate buy.

Industry briefing

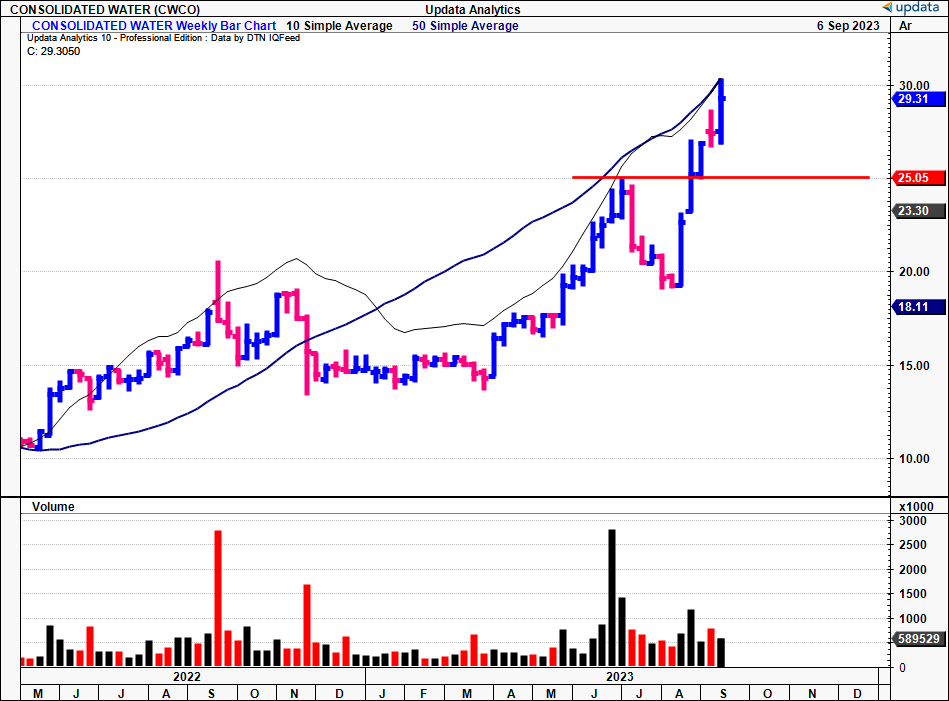

As far as capital-light compounders with attractive economics go, Consolidated Water ( CWCO ) fits the water bill in my opinion (no pun intended). The company's equity stock has broken above key psychological levels and posted multi-year highs at the time of writing.

The bullish repricing isn't without substance either. Recovery in its core tourism markets along with a sharp rebound from the pandemic are feeding an economic flywheel that 1) is recycling capital at high rates of return, and 2) spinning off attractive levels of cash to shareholders [dividends included, which are not discussed here].

This report will unpack the critical investment facts, that are fundamental and economic in nature. Net-net, I rate CWCO a buy, and I am eyeing $45-$48/share over the coming 12 months. This is based on the incremental earnings it is producing on reinvestments made each quarter.

Figure 1.

{kind=link}

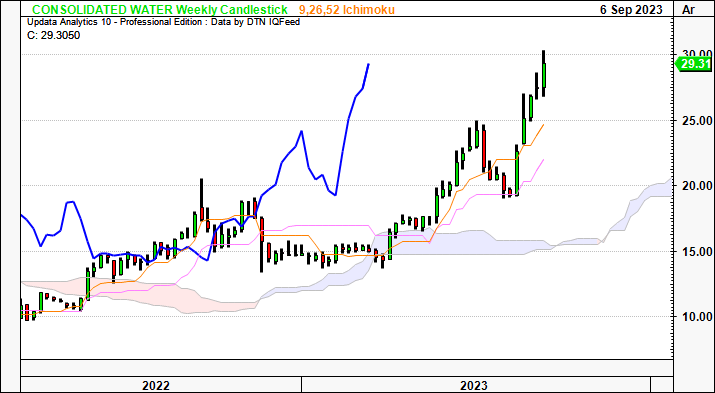

Figure 2. CWCO breakout above cloud support on weekly, which looks to coming months. The longer-term trend is bullish.

{kind=link}

Critical facts to investment debate

1. Brief overview of business operations

CWCO is a company that provides water-related solutions to its customers in the Cayman Islands, The Bahamas, the United States, and the British Virgin Islands. It specializes in using reverse osmosis technology to produce potable water from seawater, which is then sold to various customers, such as public utilities, commercial and tourist properties, residential properties, and so forth.

It also offers water treatment infrastructure and management services to commercial and governmental clients. Additionally, the company manufactures a range of specialized water industry-related products. It provides engineering, operating and other services applicable to water production and supply.

The global market for water utility services was recorded at $67.30Bn in 2022 and is anticipated to reach $89.67Bn by 2030, reflecting a compounding growth rate of ~3.82% during the period. In my view, CWCO's industry positioning sets it at the tip of the spear to capture a decent chunk of the profit pool in its core markets.

2. Q2 FY'23 insights-sharp rebound with tourist markets back online

CWCO demonstrated its mettle within this current market during Q2 FY'23. It put up $44.2mm in revenues , up 110% YoY. It pulled this to gross of 35% and booked $15.5mm on this, also up ~107% YoY. Consensus now calls for 51% sales growth in FY'23 for $142mm, which could generate 290% YoY growth in earnings to $1.48/share.

Critically, the significant escalation in sales was underscored by growth across all 4 business lines:

- Retail operations: Its retail water segment was up 14% YoY to $7.5Bn. Growth was driven by water volume in its Grand Cayman market, driven by the resurgence of tourist activity after the pandemic. This rebound in tourism has been instrumental in the market's recovery and will likely continue to be so for the remainder of FY'23.

- Services: The services business was the cornerstone of Q2 sales growth, up 375% YoY to clip $24mm for the quarter. The bulk of this was explicitly linked to its $82 million advanced water treatment plant project in Goodyear, Arizona, unveiled in May last year. Project construction is proceeding as scheduled, and CWCO anticipates another revenue stream after start-up, slated for mid-2024.

- Manufacturing: CWCO's operations and maintenance contracts clipped ~ $4 million in Q2, an 11% increase earned on similar contracts last year. This achievement highlights CWCO's exceptional abilities in efficiently managing and maintaining critical water infrastructure. Critically, manufacturing revenues were up due to the increased production, facilitated by improvements in the supply chain. Procurement of raw materials was also less of a challenge compared to last year.

Finally, CWCO's foray into the U.S. desalination market was made on a $204 million, 20-year contract to design, build, operate, and maintain a seawater desalination plant in Oahu, Hawaii. This adds to a lengthy list of contracts secured over the last 18 months, worth >$350 million in total.

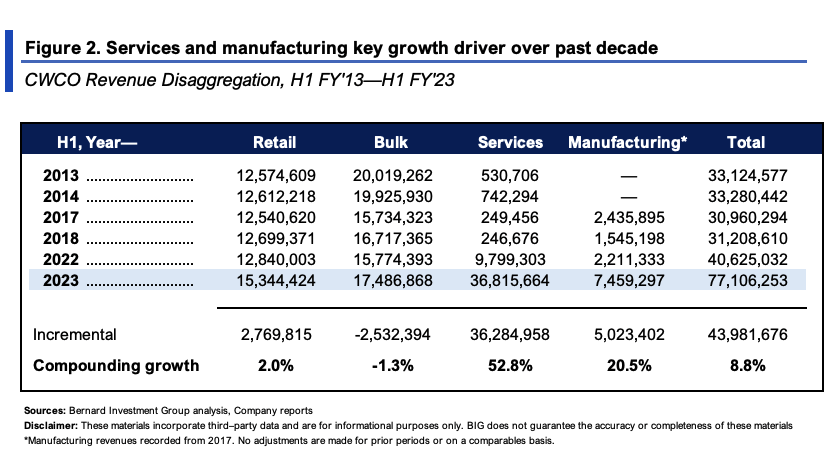

Related to point (2) above, the long-term revenue drivers are its services and manufacturing segments. Figure 2 shows this in detail. The H1 revenues across all segments are taken from 2013-'23. Turnover from services has compounded at ~53% over this time, manufacturing 20.5% since H1 2017 after its introduction.

{kind=link}

3. Economic leverage on capital employed

The economic highlights in CWCO's growth arsenal are a standout. Stepping away from the financial results and comparing profits as a percentage of capital invested tells an entirely different story.

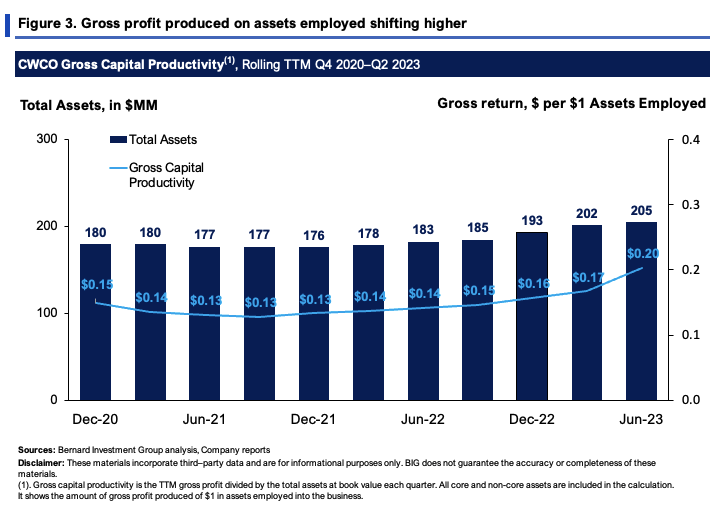

For one, gross capital productivity off total assets employed is shown in Figure 3 on a rolling TTM basis. All core and non-core assets are included. CWCO has grown gross income from $0.15 to $0.20 for every $1 of assets employed into the business. This 33% gain in gross occurred off just 13.8% asset growth.

{kind=link}

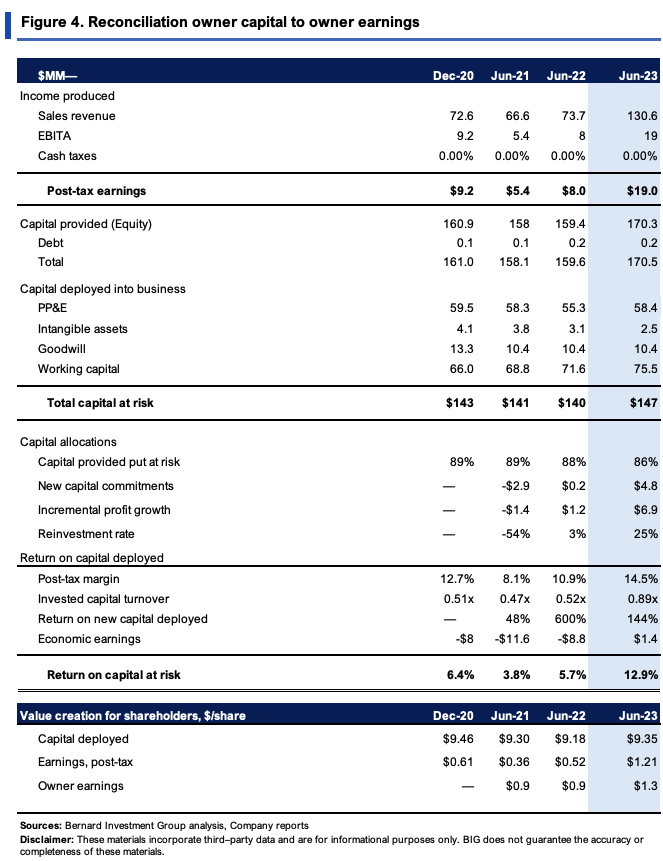

More granular analysis of how CWCO is creating shareholder value is equally as telling. Figure 4 outlines the tax-adjusted earnings produced on the total capital it has at risk in the business, $147mm in Q2.

Critically, the $147mm produces $19mm in tailing NOPAT (also called post-tax earnings here), up from $8mm produced on $140mm of capital in Q2 last year. This equates to $1.21/share in post-tax earnings off a $9.35/share investment made by the company, otherwise 13% rate of return.

More critically, are the returns on reinvested capital, otherwise the incremental returns on its new capital commitments. From Q2 '21-'23, it has produced exceptional gains in incremental returns on investment, tallying 144% trailing return in Q2.

These are simply exceptional economics, translating to a $0.17/share investment from CWCO producing $0.69/share in earnings after-tax in 12 months. Moreover, it has grown NOPAT in by ~$10mm the last 2 years on only $3mm incremental investment, a 333% return on incremental capital. A firm can compound its intrinsic value at the function of its reinvestment rate and the returns it can see on its new commitments. Given this, CWCO is compounding its intrinsic value at attractive rates, and spinning off high cash flows to shareholders-likely one reason it upped its dividend by 12% last month.

{kind=link}

Valuation

The stock sells at 18.8x forward earnings (a premium of ~16%) but sells at a discount of 15x forward EBIT (18% to the sector). It has created ~$2.50 in market value for every $1 in net asset value. I'd argue to value CWCO above the bottom line, looking at pre-tax earnings and NOPAT instead to get a better gauge of free cash flows going forward.

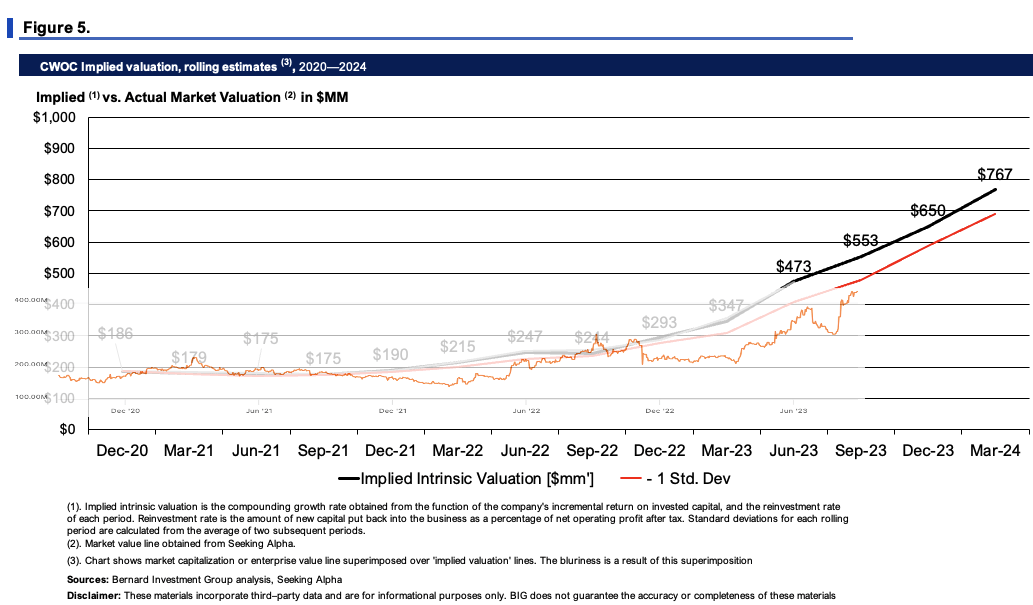

Figure 5 approximates this well. It draws on the calculus listed earlier, at the function of which a firm can compound its intrinsic value (ROIC x reinvestment rate). Applying this to CWCO's equity line gets you to an implied market value of ~$473mm at the time of writing, around 8% premium as I write. Looking out to FY'24, I get to $767mm in market value, $48/share, a 76% value gap.

{kind=link}

Further, investors have priced the company at ~2.7x EV/invested capital. This shows 1) the expectations on CWCO's earnings power, and 2) that its capital is valued highly by the market.

Critically, the incremental rates of return exemplify the growth yet to be priced in, in my view. Here I compare the return on new capital against the 12% hurdle rate we employ in our equity holdings. Both EV/IC and the ROIC/12% show returns produced on the firm's capital. One compares the business returns; the other, market returns on its investments. Because market values are a set of discounted expectations, it is fruitful to compare the two.

What shows is that it appears investors have only priced in ~22% of the firm's earnings power at its current market value. Making up the rest (~78% yet to be priced in) gets you to ~$710mm or $45/share, a shade off the numbers outlined above. This supports a buy rating.

BigInsights

In short

In summary, CWCO presents with multiple inflection points that could see it rate higher in the coming months in my view. This is an asset-light business that bodes in well during an inflationary environment and is 100% equity financed, meaning its rates sensitivity is low. Its core markets have turned up sharply after Covid-19, and it is now plowing high rates of incremental investment returns from its capital reinvestments. Net-net, rate buy at $45-$48 price target.

Risks to investment thesis

Before proceeding with any investment decisions, investors should realize the following set of risks:

- The company's business returns hinge on demand remaining high in its core markets. Another large sigma event could severely hamper its ability to book sales and feed profits to the bottom line.

- The returns on CWCO's existing capital base are quite thin, unlike the incremental growth rates it is throwing off. Should it stop investing new capital at such attractive rates, this would hurt the valuations shown.

- We can't ignore the macro-level risks that could put broad equity markets through a wave of selling pressure, and this could spill over to CWCO's equity stock.

- Being that it is a small cap equity, CWCO's market prices can become disconnected from fundamentals with small or indifferent catalysts. This should be factored in.

All of these risks must be understood in full before making any decisions around investment, as mentioned.

For further details see:

Consolidated Water: Throwing Off High Rates Of Return On Small Capital Requirements, Rate Buy