TAP - Constellation Brands: Beer Business Remains Key Driver

2023-04-27 11:27:57 ET

Summary

- Mexican beer portfolio of Constellation Brands continues to drive growth and will likely show sustained demand despite macroeconomic tightening.

- The company's Wine & Spirits business continues to underperform despite brand divestitures and suffers from higher operating inefficiencies compared to the beer business.

- Debt issuance to fund beer production expansion and share reclassification and higher CapEx will limit FCF generation over the near term.

By all accounts, the beer industry faces headwinds over the near term. However, with the industry losing its top spot for alcoholic beverages market share in 2022 and beer companies growing predominately through price increases, any company that can illustrate strong organic growth has a competitive edge. Constellation Brands (STZ) is one such company... kind of.

Through the COVID pandemic and beyond, STZ has done something that no other major American beer company has: grow volumes. Its high-margin, imported beer portfolio has continued to grow the top line as demand remains robust for STZ's products. However, for all the value the beer business has contributed, the Wine & Spirits business has mitigated STZ's net growth and profitability, suffering from declining revenue and weaker margins. Additionally, STZ's decision to rapidly expand its beer business by spending large swaths of cash on opening new breweries and updating those currently in operation will squeeze free cash flow yield over the coming years. Thus, due to the uncertainty around the Wine & Spirits performance (even after the divestiture of low-margin brands) and slowing FCF over the near term, STZ is a hold.

Beer Continues To Win

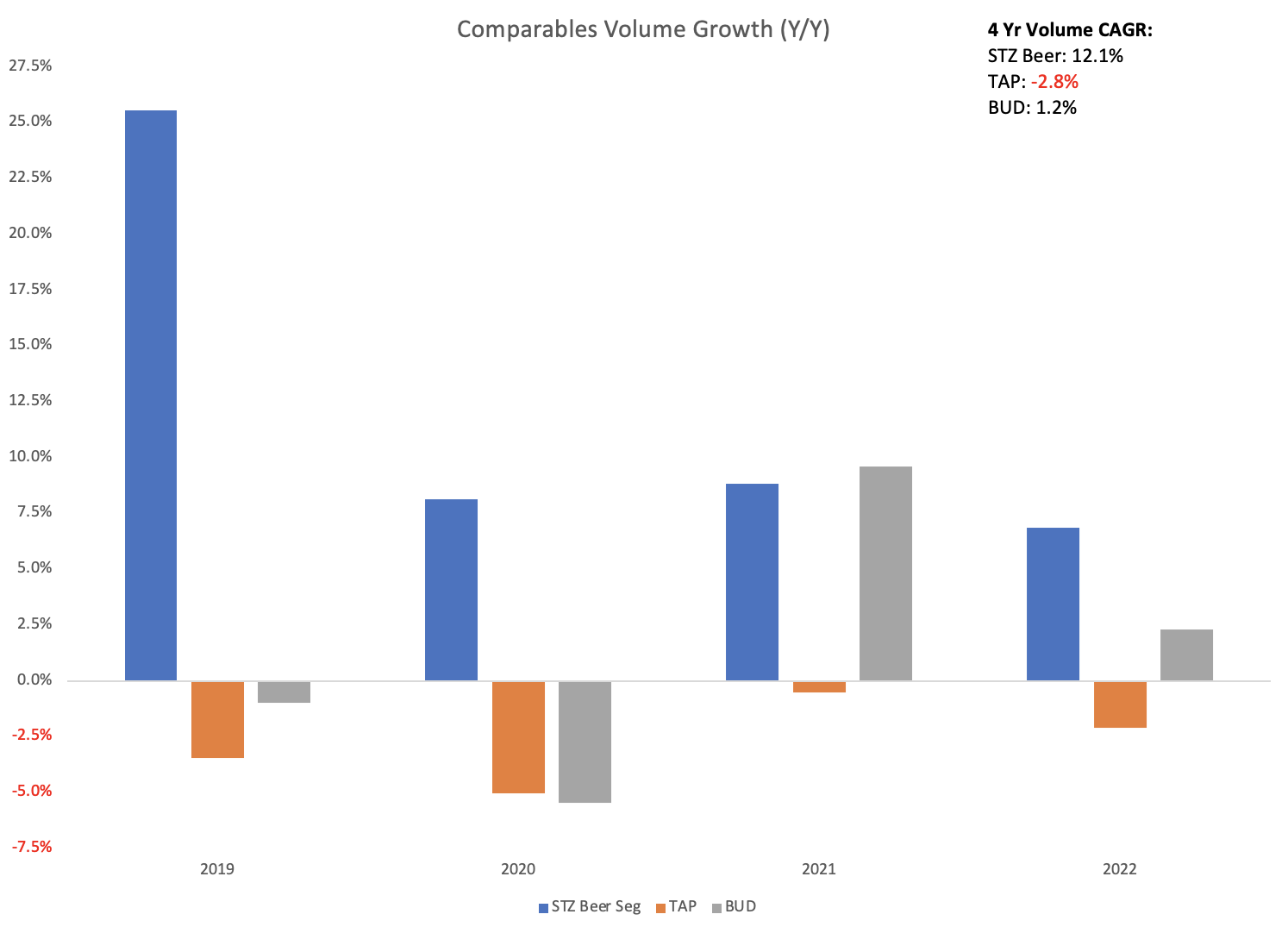

STZ released earnings on April 6, 2023, for Q4 and FY 2023, demonstrating a bottom-line beat and revenue aligned with expectations ($2 billion for Q4). As with previous years, the Beer business, whose portfolio consists of the Modelo product family, Corona products (including Corona Hard Seltzers), and a few craft beer brands, demonstrated strong revenue growth and delivered the 13th consecutive year of volume growth. This growth in volume alone reveals something STZ's beer portfolio has that competitors like Molson Coors ( TAP ) and Anheuser-Busch ( BUD ) don't: revenue growth through volume growth. While TAP and BUD have also seen Y/Y revenue growth, both firms have achieved these top-line gains primarily through consumer price increases. While STZ offset inflationary headwinds in 2022 with similar strategies, it also increased the physical quantity of products sold by 6.9% in 2022. TAP and BUD, at best, held their brand volumes constant Y/Y.

STZ beer shipments (12 oz equivalent), TAP financial volume, & BUD financial volume growth on annual basis (S&P CapIQ Pro; Company Annual Reports)

{kind=link}

One competitive advantage STZ has over TAP and BUD is its relatively less competitive market landscape. TAP and BUD are the Coke and Pepsi of the American beer world; they have been competing against each other for market dominance, primarily in the domestic and light beer space. In contrast, STZ's beer names fall into the imported beer market. Unlike domestic beer, consumers likely will not view European imported beers as apt substitutes for the Mexican beers STZ sells. And STZ dominates this market, holding the title of the number one imported beer company in the United States. Modelo and Corona are the number one and two-selling imported beer brands in the US, respectively. Mexican beer brands continue to remain popular among Hispanic communities in the US, and the continuing growth of Hispanic populations in the US will support demand.

As mentioned, the broader US beer market will face numerous headwinds through 2023 and likely into 2024 such as lingering supply chain and inflationary pressures in conjunction with demand slowdown from a weakening consumer. Despite this unideal macroeconomic outlook, STZ management projects high single-digit organic sales growth for the beer business, showing internal confidence that consumers will continue to consume premium Mexican beer. And management's guidance seems plausible if one looks at how STZ fared through COVID and the nature of its products. Notably, in recessionary environments, consumers will mitigate spending on higher-priced alcoholic beverages. Instead, they may opt for a lower-priced option like beer, supporting a positive outlook for STZ's beer names. Furthermore, over the medium and long terms, STZ's investment in their Mexican breweries highlights an appropriate capital allocation to meet growing consumer demand by expanding production capacity. As stated earlier, STZ's dominance in the Mexican beer market suggests that management can meet their organic top-line growth targets.

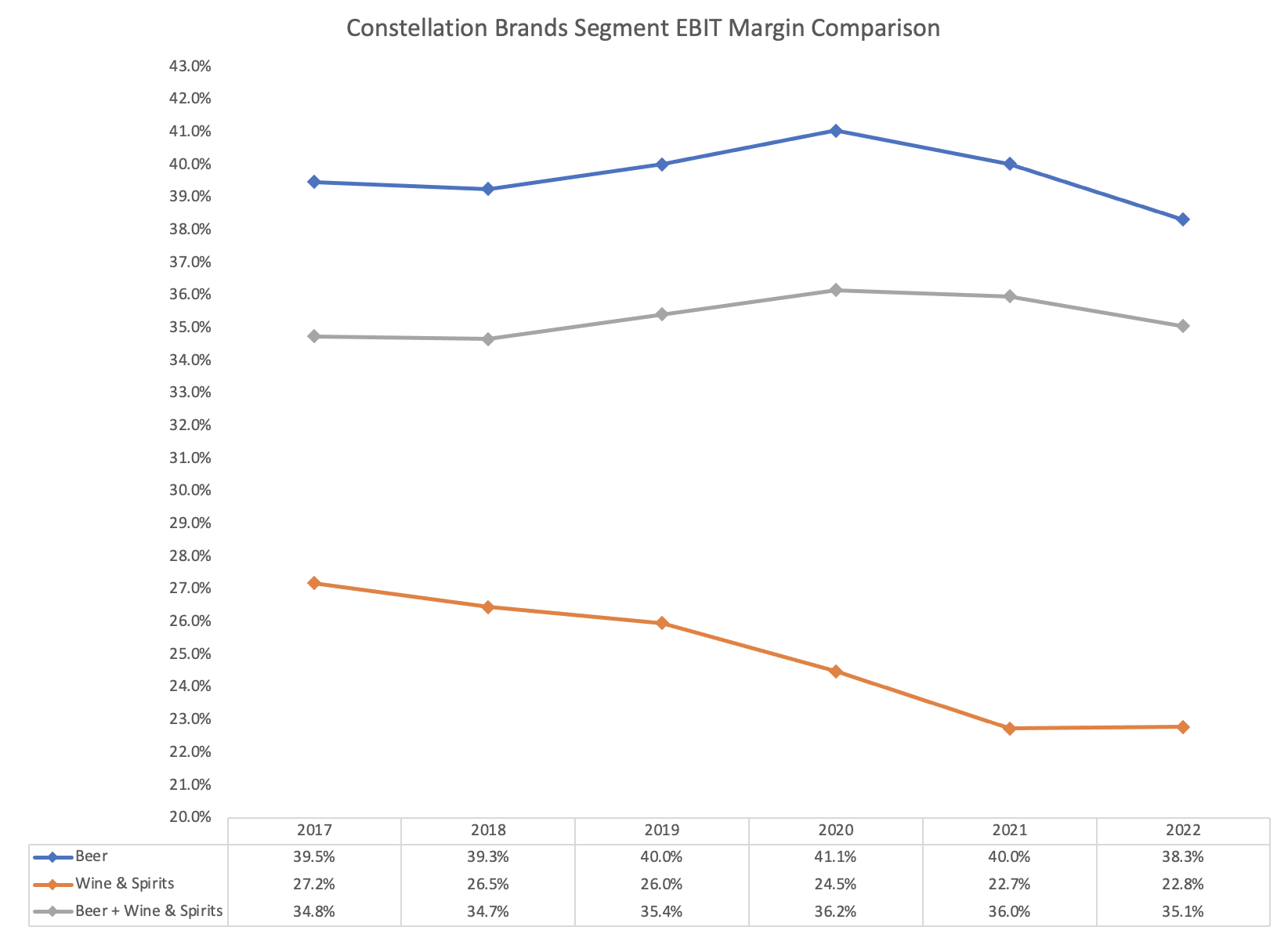

As seen with all major beer manufacturers, lower inflation for transportation and raw materials (like glass and grain) should allow margins to widen. However, even if cost inflation persists due to higher transportation costs from sustained high energy prices (e.g., OPEC+ cuts to 2023 oil output ), STZ's beer segment outperforms both TAP and BUD regarding operating profitability. From 2018 through 2022, STZ maintained an average EBIT margin of 39.7% compared to 13.3% and 27.9% for TAP and BUD, respectively. Furthermore, over the past five years, STZ has shown positive EBIT growth (5 Yr CAGR = 7.0%) compared to negative EBIT growth for TAP and BUD. While past performance does not guarantee future results, STZ's state-of-the-art brewery (currently under construction) in Veracruz will expand its production capacity to meet future demand. The company also has pledged a portion of the $4.0 billion to $4.5 billion in beer CapEx through 2026 to continue optimization and capacity expansion at the existing breweries in Nava and Obregon. Thus, through brewery expansion and CapEx investment that creates operating efficiencies, STZ will leverage more pronounced economies of scale to support margins in the historical high 30% to low 40% range.

Wine & Spirit Continues To Struggle

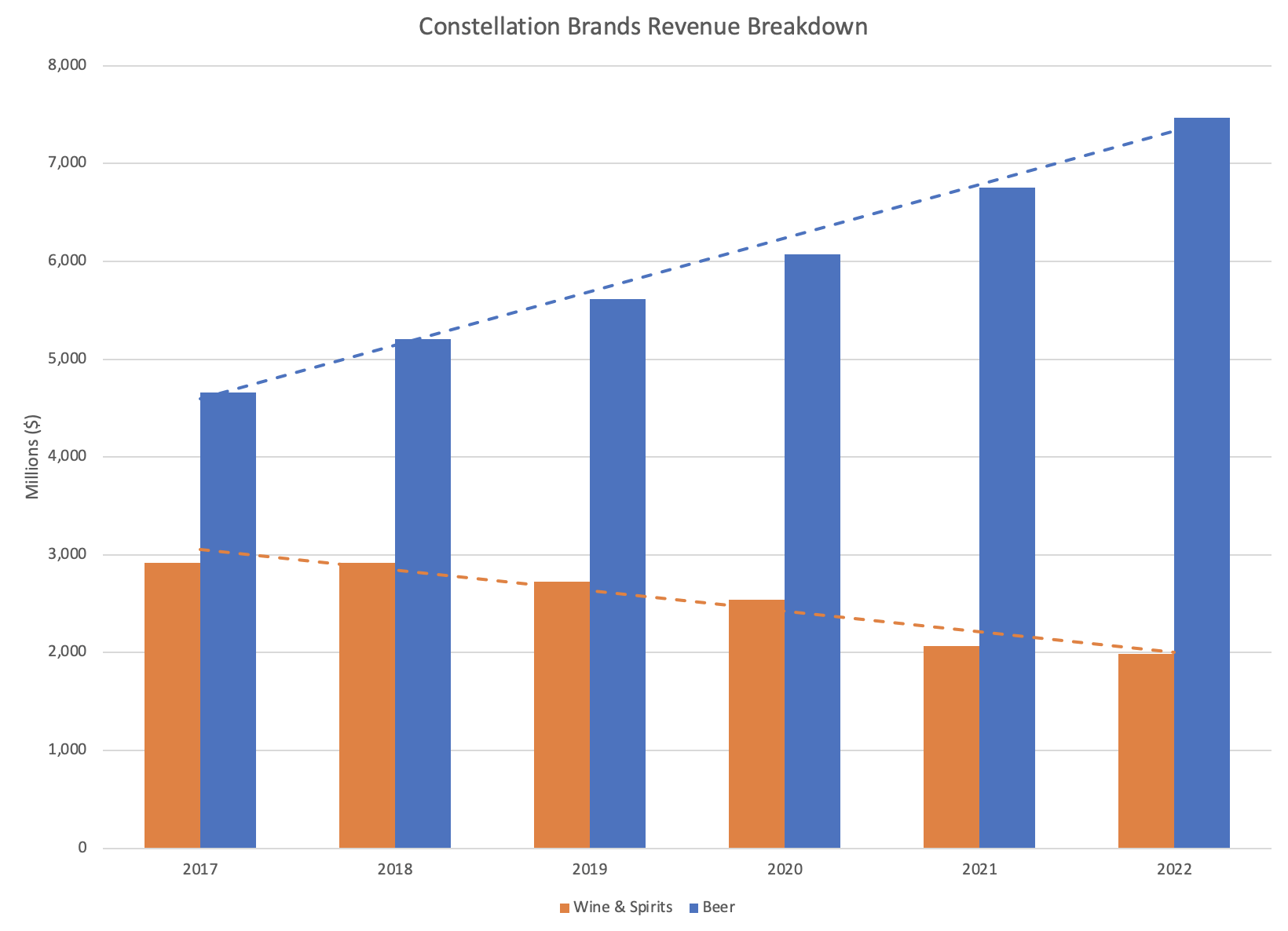

Despite STZ cutting low-margin, economy wine brands quarter after quarter, the Wine & Spirits ("W&S") business continues to underperform and operate far less efficiently than the beer business. In Q4, the W&S segment organic sales declined 9% Y/Y, and for FY 2023 (ended Feb 28, 2023), organic sales declined 2%. While the divestitures of certain wine brands in 2020 and 2021 helped to explain the declining overall segment revenue, the organic shrinkage in the wine business spotlights a red flag going forward, particularly in the wake of economic tightening. Due to its higher price point (which has been exacerbated by inflation over the past two years), wine typically is not as recession-resilient as beer , indicating that W&S revenue could continue to struggle over the near term as consumers opt for cheaper drinking options like beer or liquor (which offers more drinks per bottle).

S&P CapIQ Pro, Company Filings Beer EBIT margin has remained in historical range whereas W&S has consistently declined over the same period, negatively affecting the overall company's margin. (S&P CapIQ Pro, Company Filings)

{kind=link}

{kind=link}

Additionally, the W&S business requires higher marketing expenditure relative to its sales which puts it at a disadvantage relative to the beer business. For FY 2023, the beer business SG&A margin was 14.4% compared to 23.9% for W&S. While fixed marketing expenses and labor costs drive the SG&A figure, this high spending coupled with sales shrinkage does indicate a shortcoming in operational efficiency. Furthermore, the wine industry is highly competitive and far more fragmented than the beer industry, meaning STZ cannot create a moat similar to its position in the imported beer market. This exemplifies one of the key reasons I view the W&S segment as a negative for the company. Finally, while certain high-end brands like The Prisoner continue to perform, the broader W&S business continues to have organic sales and volume declines which a recessionary environment in the back half of this year can only amplify.

Debt Refinancing And CapEx Will Dampen FCF Yield

For FY 2023, STZ sustained net leverage of around 3.4x, down from 3.7x in the prior year. Despite double-digit EBITDA growth Y/Y, the net issuance of $1.2 billion in senior debt to help fund the Class B stock reclassification kept leverage elevated and increased interest expenses for the year by roughly 12%. In the earnings release, management stated that they anticipate $500 million in interest expense for FY 2024 due to variable rate debt and higher interest rates on the newly issued debt. While talk of Fed rate cuts through year-end spiked following the bank failures in March, a resilient labor market and sticky inflation in parts of the economy suggest the Fed might have to sustain higher rates for longer, boding poorly for STZ which has $900 million in senior debt maturing in 2024. Higher refinancing costs will squeeze free cash flow generation as the company faces higher interest expenses.

Additionally, STZ's BBB/Baa3 credit rating means it has little room for error over the coming years. A slip in demand or failure to capitalize on the beer business expansion could trigger a credit downgrade, leading to a higher cost of debt and further softening FCF generation. One thing worth mentioning, while STZ does have similar leverage to other beer firms like TAP, its leverage trend has been far less impressive compared to TAP, for example, which has steadily reduced leverage each year since the Miller acquisition (my analysis of TAP can be found here ). Thus, STZ's leverage situation encompasses more risk due to the lack of consistent deleveraging and the allocation of debt toward the share reclassification.

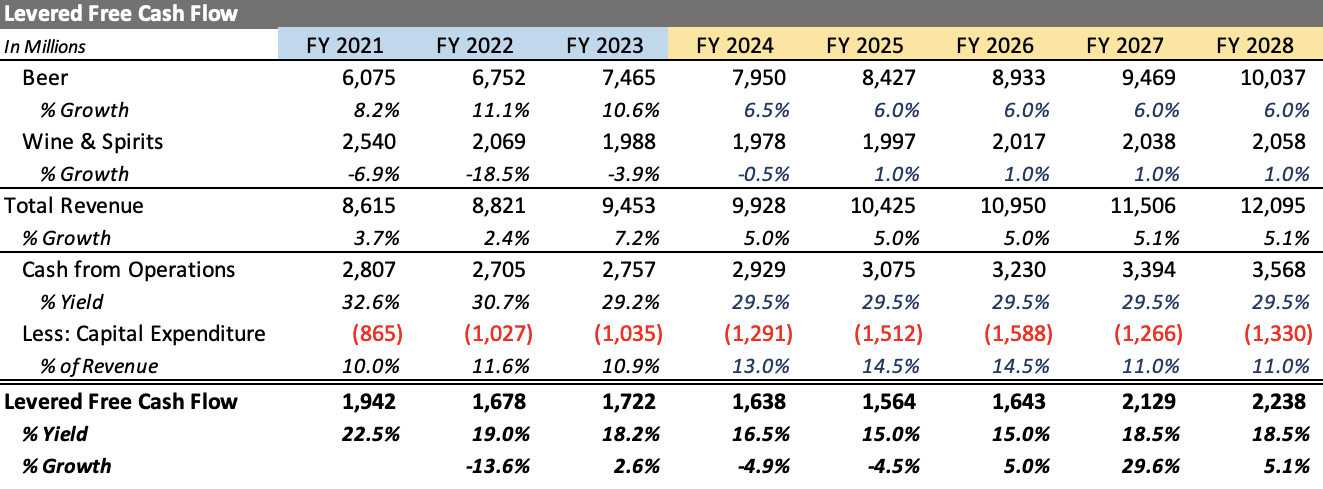

Higher CapEx represents another critical item that poses a potential headwind for STZ's free cash generation. In their FY 2024 outlook, management stated that they expect CapEx in the $1.2-1.3 billion range, with $1 billion going towards Mexican brewery expansion. Additionally, the company anticipates CapEx for the beer business between $4-4.5 billion over the next three fiscal years, suggesting FY 2024 CapEx for the beer business alone could increase by 20% and then again increase through 2026 to near $1.4 billion (not including roughly $100 million expenditure for W&S per year).

Projected levered FCF through FY 2028. CFO yield median from FY 2016 to FY 2023. CapEx % of revenue chosen to match CapEx projected values through FY 2026, then returned to historical levels. (Model: Myself, Data: S&P CapIQ Pro)

{kind=link}

As shown above, the increased capital spending to meet growing demand in the beer business could cut FCF yield by up to 300 bps over the coming years. Historically, STZ traded around 16x to 20x P/E (TTM basis) when FCF yield was near 16.5% during FY 2019. Given that the current forward P/E for FY 2024 is around 19.3x, this forward valuation falls within STZ's range, given the expected free cash flow over the near term. The slowing macro environment does put downward pressure on multiples; however, the capital investment in the breweries will drive top-line and bottom-line growth post-completion which offsets some of the risk associated with tighter conditions over the near term.

Beer's Strength Also Its Greatest Risk

The beer business made up 79% of FY 2023 sales. This has facilitated the higher revenue growth for STZ that other beer companies have not seen over the past five years. Mexican beer has boomed in the United States as Hispanic communities continue to grow, and more people, in general, have started consuming Mexican and other imported beers. However, this also means that most of STZ's top line rests on consumer preference for Mexican beer; this highlights a key vulnerability. Consumer preferences change over time, and a decline in demand would have profound consequences for both sales growth and profitability.

The $4 billion expansion over the coming years reveals that STZ will fully leverage the current market trends and fully commit to the strategy. Should those trends change, however, the business will have excess production capacity but insufficient demand, hurting margins and cash flow growth. Imported beer has stood out from the rest of the broader industry as a growing market despite beer as a whole seeing declining volumes (granted dollar amount of sales has increased); however, changing preferences still threaten STZ's long-term plans that should not be overlooked.

Despite this risk, the circumstances surrounding the Mexican beer industry bode well for its growth over the next decade. In the worst-case scenario, STZ will find itself in a position like TAP or BUD with slow top-line growth. However, the chance that demand pulls back to the point where the company has far too much capacity seems unlikely given that its current expansion is to catch up with demand.

Conclusion

In many ways, STZ's future is a game of tug-of-war. On the one hand, the beer business continues to deliver robust revenue growth and increased profitability. On the other hand, large expenditures on beer production capacity, debt-funded restructuring of the common equity, and a lagging W&S segment highlight potential pitfalls for the company. The current valuation for STZ matches the current position of the company and its growth outlook, particularly for the beer business. However, the company's goals are ambitious and rest upon many predictions coming to fruition such as a rebound in W&S business and continued demand growth for their beer products. Constellation Brands stands out among its peers in the beer industry in its ability to grow the volume of beer sold while others have seen shrinking volumes. If the company can successfully leverage its winning products and trim its inefficient operations, STZ will position itself as a market leader.

For further details see:

Constellation Brands: Beer Business Remains Key Driver