PRNDY - Constellation Brands: Premiumization And Brands Drive Value

2023-09-11 03:58:29 ET

Summary

- Constellation Brands operates leading brands in the alcohol beverage industry, such as Corona, benefiting from a loyal customer base and significant global scale.

- The company has achieved impressive financial returns with consistent commercial development of its diverse portfolio. Management has shown a willingness to conduct M&A or organically respond to trends where possible.

- Premiumization and adapting demand for beverages has contributed to healthy growth for STZ, although it has been unable to match its Spirit-focused peers. Nevertheless, we believe this will drive value.

- STZ stock is currently trading at its fair value we feel, with no material evidence to imply upside.

Investment thesis

Our current investment thesis is:

- Constellation Brands (STZ) operates a range of leading brands, including Corona, Modelo, and SVEDKA. The company marketing and industry penetration efforts have been successful, positioned to keep the business as a leader.

- Industry trends, such as premiumization, are working in STZ's favor, contributing to improved growth and margins. Compared to its peers, the business has good exposure to both the Beer and Spirit segments.

- STZ's performance relative to peers is modest, with superior margins but lagging growth. When considered in conjunction with its trading multiple, we do not see sufficient upside.

Company description

Constellation Brands operates a multi-category alcohol beverage business. Its business model involves producing, marketing, and distributing a wide range of alcoholic products. The company's portfolio includes well-known brands in beer (e.g., Corona, Modelo), wine (e.g., Robert Mondavi, Kim Crawford), and spirits (e.g., SVEDKA Vodka).

{kind=link}

Share price

STZ's share price performance during the last decade has been impressive, significantly outperforming the wider market. This has been driven by shrew management, with consistent commercial development contributing to impressive financial returns.

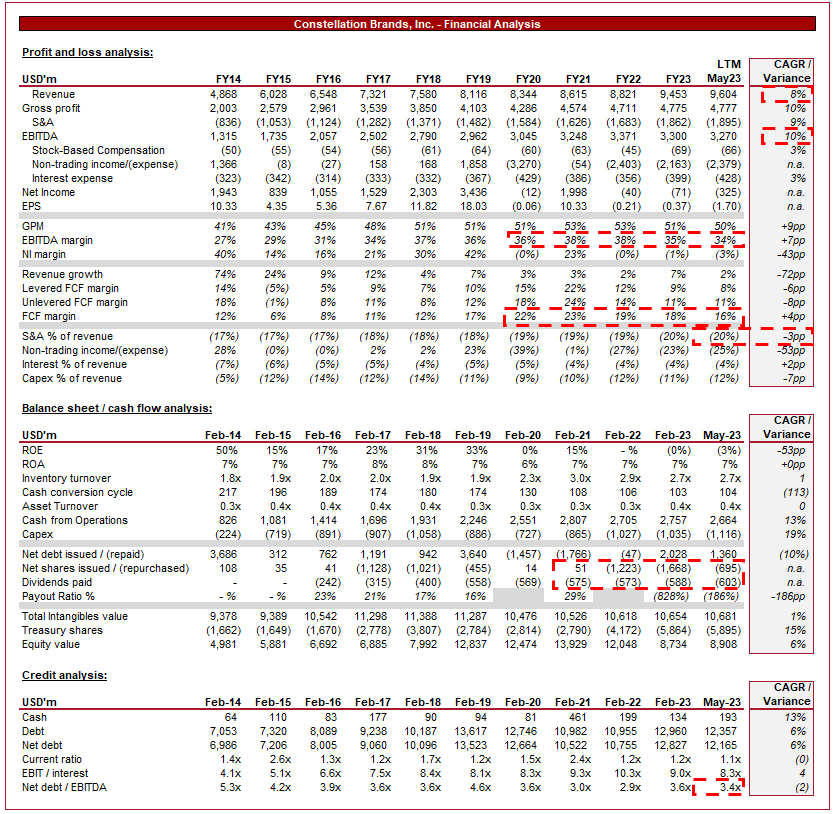

Financial analysis

Constellation Brands' financials (Capital IQ)

{kind=link}

Presented above are STZ's financial results.

Revenue & Commercial Factors

STZ's revenue has grown at a healthy CAGR of 8% during the last decade, with relative consistent gains YoY. This has been supported by M&A and healthy organic development.

Business Model

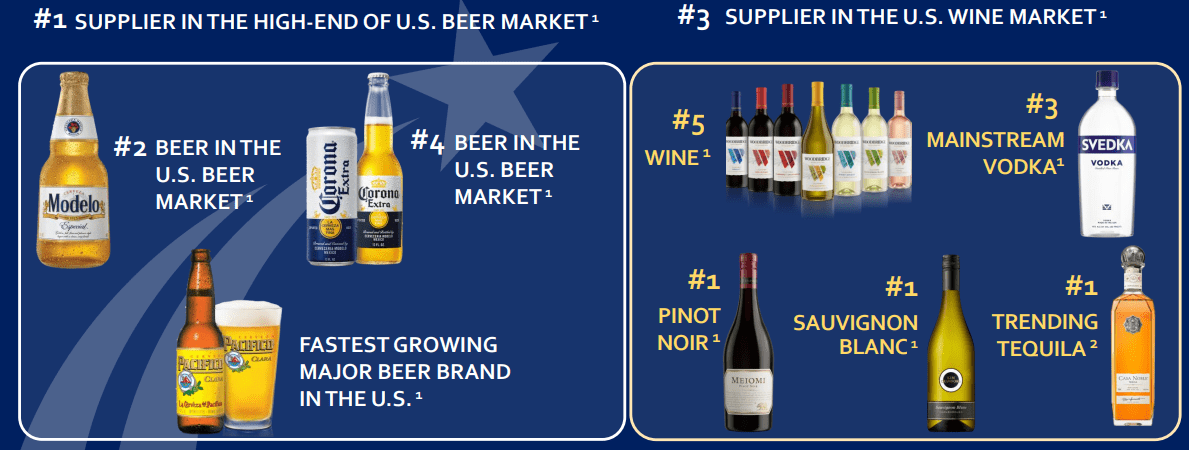

STZ has a diverse portfolio of well-known brands in different alcoholic beverage categories. This includes beer brands like Corona, Modelo, and Pacifico, wine brands like Robert Mondavi and Meiomi, and spirits brands like SVEDKA vodka. These brands have a significant presence in global markets, particularly in the West.

{kind=link}

Continued investment in brand development, particularly through innovative marketing strategies is critical to growing its customer base. Consumers are generally loyal to beverages they enjoy, which is why incremental customer wins against peers are highly lucrative.

STZ has a robust distribution network that spans various geographies, allowing for deep penetration within national markets. Similar to the importance of effective marketing, reaching consumers through "shelf space" (both in stores and social locations) is critical to maintaining and developing a market-leading offering. Underpinning this is a diversified global supply chain, allowing for incremental margin improvement as scale is achieved.

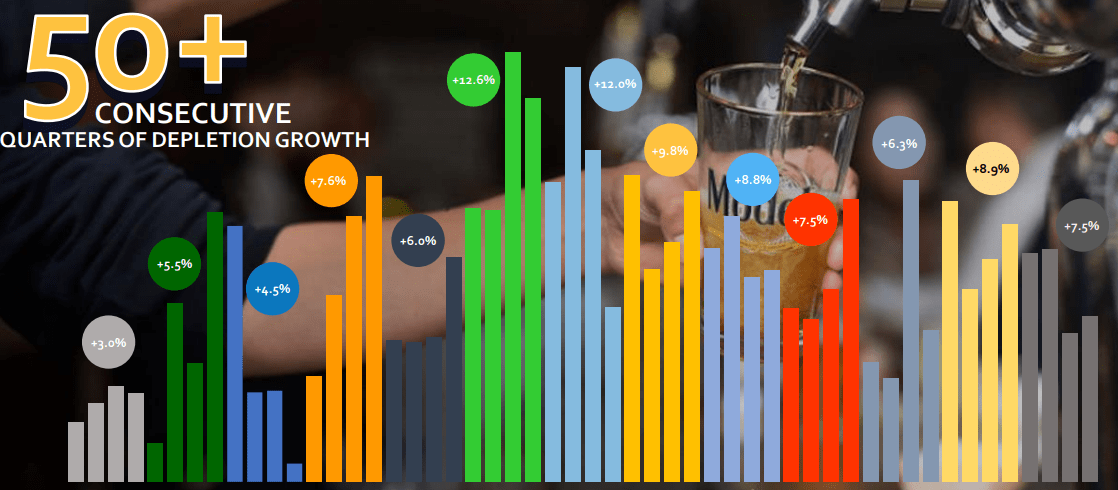

As the following illustrates, Management has been successful in delivering its strategic imperative, contributing to 50 successive quarters of depletion growth.

Depletion (Constellation Brands)

{kind=link}

The company has formed strategic partnerships with other beverage companies, enabling it to expand its portfolio and distribution reach. The biggest example is its partnership with Grupo Modelo, which grants it the exclusive rights to import and market Corona and other Modelo beers in the U.S. Following the Bud Light scandal, Modelo Especial gained the top spot in the US beer market ( May23 ).

STZ has made strategic acquisitions and investments to expand its portfolio, primarily to fill gaps, increase exposure to certain markets, and gain entry into emerging beverage categories. Industry trends have the potential to impact STZ's brands negatively but we are not overly concerned because it always has the optionality of M&A. Most recently, the business acquired My Favorite Neighbor and Lingua Franca.

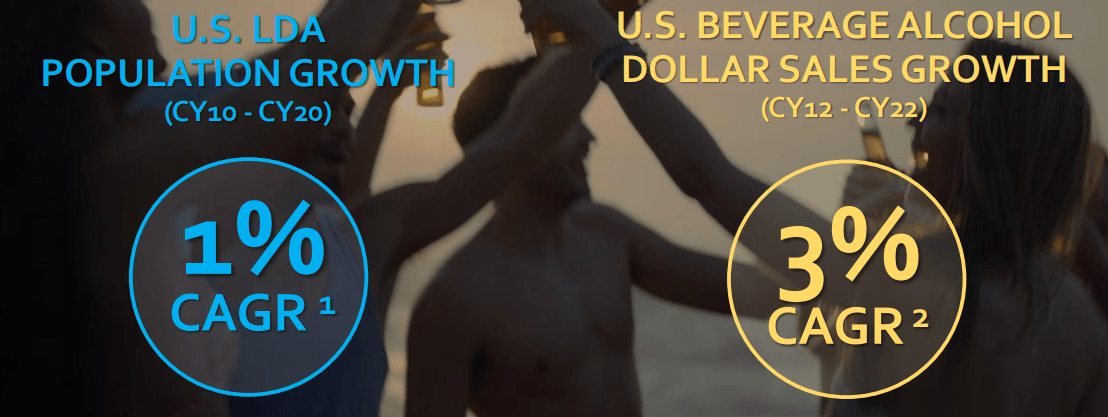

Alcohol Industry

The alcoholic beverage industry is incredibly lucrative, owing to the vast number of individuals who drink. For this reason, there is strong competition in the market, but equally high returns for those brands with a substantial position.

{kind=link}

The industry has grown well in the last decade despite its maturity, with leading brands outperforming this 3% CAGR. We see no reason why the coming decade will fall below this, implying a continuation of its current trajectory is possible.

{kind=link}

STZ faces competition from other global alcoholic beverage companies like Anheuser-Busch InBev (BUD), Diageo ( DEO ), and Pernod Ricard ( PDRDF ). Competition is based on brand strength, product quality, innovation, and distribution capabilities.

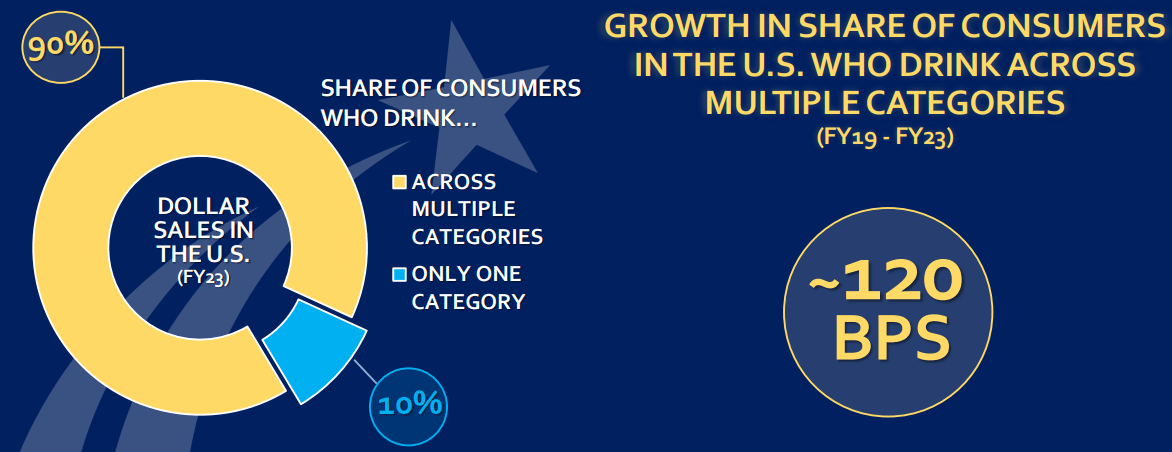

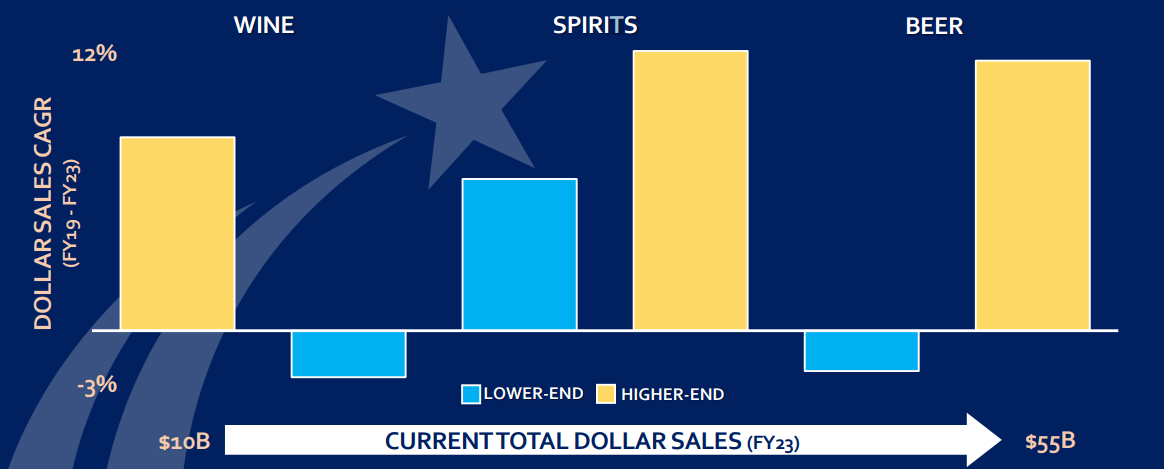

The alcoholic beverage industry has experienced a trend toward premium products, as consumers seek enhanced quality, new experiences, and premium brands. This is partially due to a specific rise in craft beer, premium wines, and craft spirits, with strong innovation attracting consumers seeking to try new things. STZ has a strong presence in the premium and high-end segments of the beverage alcohol market, allowing it to capitalize on this growth.

As the following chart illustrates, the growth delta superiority of the higher-end segment is substantial and is thus one of the key reasons STZ has been able to achieve its strong growth in recent years.

{kind=link}

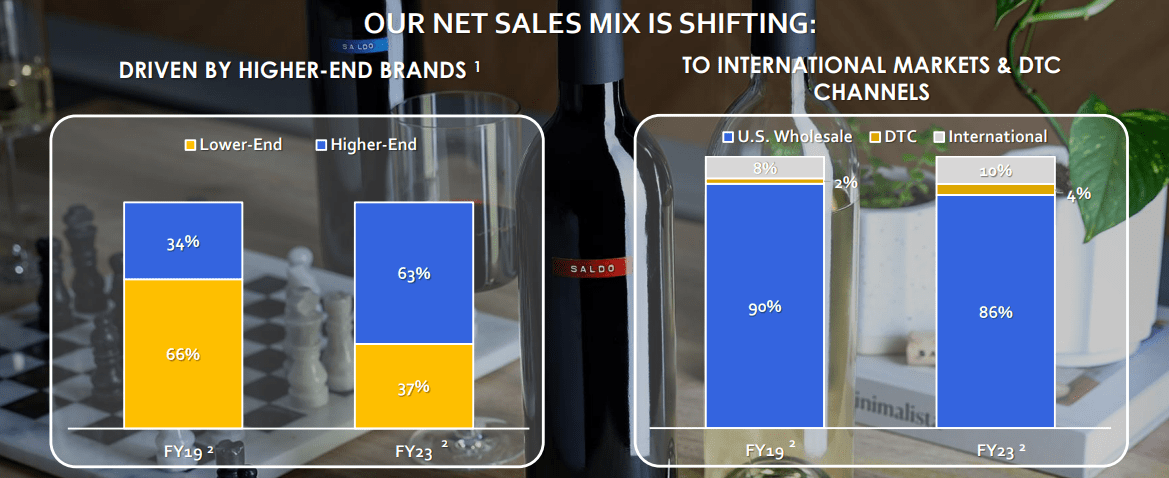

This has contributed to a revenue sales mix shift aggressively toward the premium segment. Our expectation is for this trend to continue, or at least remain robust, owing to the stickiness of demand once consumers find products they like.

{kind=link}

Going forward, Management sees the following as key growth opportunities:

- Growth in the better-for-you segment (25% CAGR L3Y) - This is another segment that we believe to be a key value driver, as consumers become increasingly health-conscious.

- Growth in flavored products in alcoholic beverages (22% CAGR L3Y) - This partially falls under the premiumization trend but is also an opportunity through partnerships. We have recently seen the release of a Jack and Coke can, as well as a Coco Vita Captain Morgan Mojito. We see a real opportunity for brand development through these partnerships.

- Growth in e-commerce beverage sales (3-5x L3Y) - The company's efforts to expand its online presence and direct-to-consumer sales channels have allowed STZ to improve its per-unit economics, aligning with the impressive growth in this channel. This is a win-win situation for STZ and we suspect further e-commerce outperformance is likely, as seen in other retail industries.

Economic & External Consideration

Current economic conditions have the potential to impact sales, as financial struggles contribute to reduced discretionary activities. In STZ's most recent quarter, it has broadly grown well (+6.4%), implying resilience thus far. This said, we remain cautious given the uncertainty.

Margins

STZ's margins have trended up in the last decade, although remain below the heights reached during the peak post-pandemic period. This improvement is driven by the premiumization trend, leading to increased sales of high-margin beverages. The most recent softening is a reflection of both demand and inflationary pressures on costs, although quarterly data implies this has stabilized (OPM - Q2'22 31.8%, Q3'22 30.4%, Q4'22 26.5% & Q1'23 31.0%).

Balance sheet & Cash Flows

STZ operates with an above-optimal level of debt in our view, with a ND/EBITDA ratio of 3.4x. This has contributed to interest payments of 4% of revenue, with a substantial amount of debt raised recently.

This decision looks to be to maintain its aggressive distribution strategy, a concerning choice in view given the lack of sustainability in this approach. We suspect a slowdown may be ahead, at least in buybacks with rates where they are.

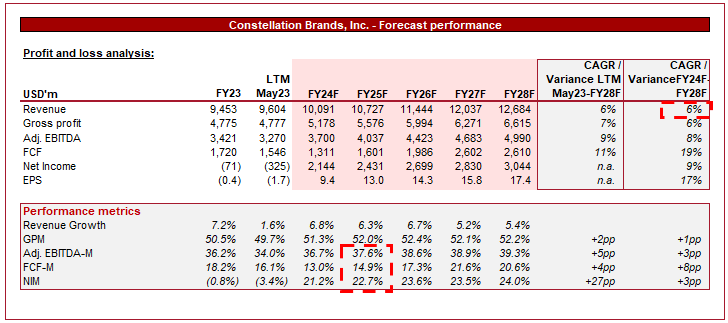

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a 6% growth rate into FY28F, alongside small incremental margin gains. This is a reasonable estimate in our view given the financial improvement achieved thus far and the likely softening of inflationary pressures, with STZ positioned to continue its current trajectory.

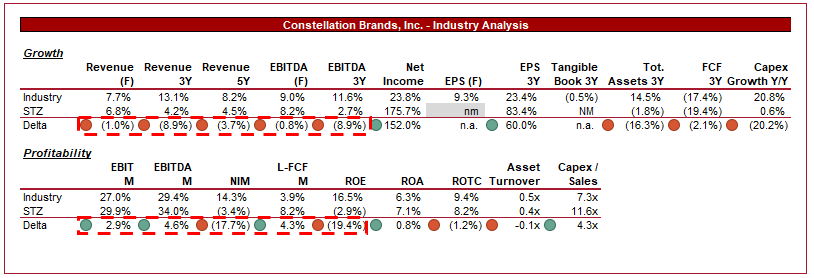

Industry analysis

Distillers and Vintners Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of STZ's growth and profitability to the average of its industry, as defined by Seeking Alpha (6 companies).

STZ's performance is respectable relative to peers. The company is lacking in growth, lagging behind its directly comparable peers. This is an underwhelming performance, particularly because Diageo and Pernod have both outperformed the business. This is likely due to its reliance on Beer, while the Spirits industry (and the peers compared) has performed better.

STZ's key strength is its margins. The company has a positive delta in both EBITDA-M and FCF and at a level that is unlikely to be lost. Given the maturity of the industry, this margin superiority is far more impressive than the industry's growth.

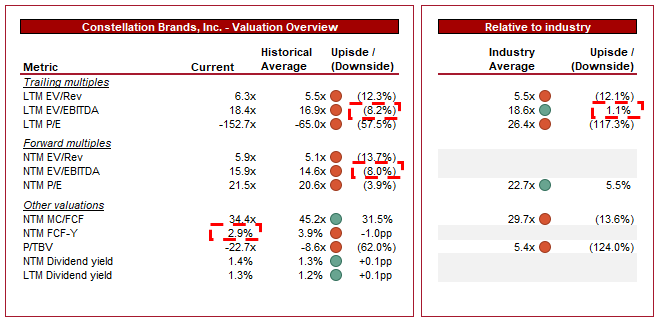

Valuation

{kind=link}

STZ is currently trading at 18x LTM EBITDA and 16x NTM EBITDA. This is a premium to its historical average.

A premium to its historical average is difficult to justify in our view. The business has developed well in the last decade but not above-and-beyond the amount expected at any point. Its margins remain broadly in line with the average during this period, as is growth.

Further, a small premium to its industry average looks to be the top-end of reasonable. This is due to its profitability premium and comparable scale to the larger market participants. STZ is currently trading at a 1.1% discount but when excluding Brown Foreman (which is trading at a uniquely elevated level), STZ is actually at a premium.

Based on this, we do not see any noticeable upside with STZ. This view is confirmed by the below-average NTM FCF yield (-1.1ppts).

Final thoughts

STZ is an attractively positioned beverage business. It has good exposure to the premiumization trend, while having a good balance between Beers and Spirits, unlike many of its peers. With its host of leading brands and quality strategic direction, we believe a continuation of its current trend is reasonable to expect.

When compared to its peers and its historical performance, we do not believe the business is priced for upside currently.

For further details see:

Constellation Brands: Premiumization And Brands Drive Value