BEPC - Constellation Energy Is Cheap With An Inflation Reduction Act Underpin!

2023-03-06 13:42:40 ET

Summary

- Recently spun off from Exelon Corp, Constellation Energy has gone unnoticed and is underfollowed.

- The Inflation Reduction Act has allocated $391 billion to energy and climate change and with the largest fleet of non-carbon nuclear plants in the USA, Constellation Energy is well positioned to benefit.

- Tax credits provide a floor to earnings and make the company's cash flows predictable.

- Recent share price declines provide a great entry point, in my view.

- Per my analysis, the stock is cheap across multiple valuation frameworks and is a buy.

Editor's note: Seeking Alpha is proud to welcome More Ideas Than Money as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Who is Constellation Energy?

For those unfamiliar with the company, Constellation Energy (CEG) was founded in 1999, became a Fortune 500 company and was one of the largest producers of electricity in the country until it was acquired by Exelon Corporation ( EXC ) in 2012. Simply put, that merger has now been reversed and CEG was relisted in 2022.

Constellation Energy is one of the USA's largest producers of carbon-free energy. They produce enough energy to power 15 million homes which is roughly 11% of the total in the country. They are already the lowest carbon emitter of any major investor-owned US power generator, yes lower than NextEra Energy ( NEE) and Duke Energy ( DUK ) and have a goal to eliminate all their greenhouse gas emissions by 2040.

Current capacity exceeds 32,400 megawatts of which 90% is carbon free. The business is well diversified too with a dominant nuclear offering supported by an ever-increasing presence in hydro, wind & solar.

Around 65% of their portfolio is Nuclear and they have the nation's largest non-carbon nuclear fleet of power generators in their portfolio. It's precisely because of this that I find CEG attractive.

The Merits of Nuclear

My argument is that there is a growing place for Nuclear as an energy source and I make my case as follows:

- Nuclear power is a clean power source. It's not renewable but it's a far better way to go when generating power than burning coal for example.

- Nuclear plants can have onsite fuel for up to 24 months which provides stability and reliability no matter the weather.

- It allows for the deployment of wind and solar which is green and clean without requiring a fossil fuel backup.

- With pending License Renewals, the life of plants will extend to 80yrs 3x more than the useful life of renewables and twice that of coal.

Why now is a suitable time to invest

The Inflation Reduction ACT (IRA) will make $391 billion available for spending on energy and climate change and is the largest single investment in addressing climate change in US history. The following supporting points about Nuclear were made by the office of Nuclear Energy:

"Momentum is building for U.S. nuclear energy and the investments and tax incentives included in IRA guarantee a commitment to nuclear energy that will continue well throughout the nation's journey to net-zero."

"One real IRA game changer for nuclear energy is a production tax credit to help preserve the existing fleet of nuclear plants."

"This is a huge priority for our office."

"The production tax credit will support our existing fleet and make sure America maintains its largest source of clean power as well as the high-paying jobs that accompany it!"

The IRA adds stability to the company's cash flows. The nuclear production tax credit ((PTC)) effectively sets downside protection on power prices at $40-$43.75/MWh. This becomes what is essentially a set floor contract with the US government as a counterparty and with an inflation adjustor on price each year.

With enormous clarity on its cash generating/return capacity the company has decided to pivot to growth, and this was announced in the results which were released on the 16th of February. This did surprise the market which had modelled for share buybacks and deleveraging and resulted in two analyst downgrades which have taken the stock price down by 7% since the numbers were released. I believe this provides us with a great entry point.

In an incredibly shrewd move by management, they announced that their largest growth project will be in the form of a pink hydrogen plant (pink hydrogen is hydrogen produced from nuclear power) and this means the project can benefit from both the nuclear AND the clean hydrogen production tax credit.

Also, in a sign of confidence, the company doubled its quarterly dividend from 14.1c to 28.2c and reiterated the post spin plan to grow the dividend by 10% per annum.

Peers

When looking at clean or renewable energy investments in the Utilities space, most investors like to look at the 'behemoth' in the room. NextEra Energy with a market cap of $145 billion, Duke Energy at $74.5 billion and The Southern Company ( SO ) at $70.3 billion are probably the most popular. This is also evidenced by the number of followers they have on seeking Alpha. NEE with 82.6k, DUK with 92.34k & SO with 83.41k absolutely dwarf the CEG following of just 4.65k followers. Constellation Energy, CEG is hidden in plain sight.

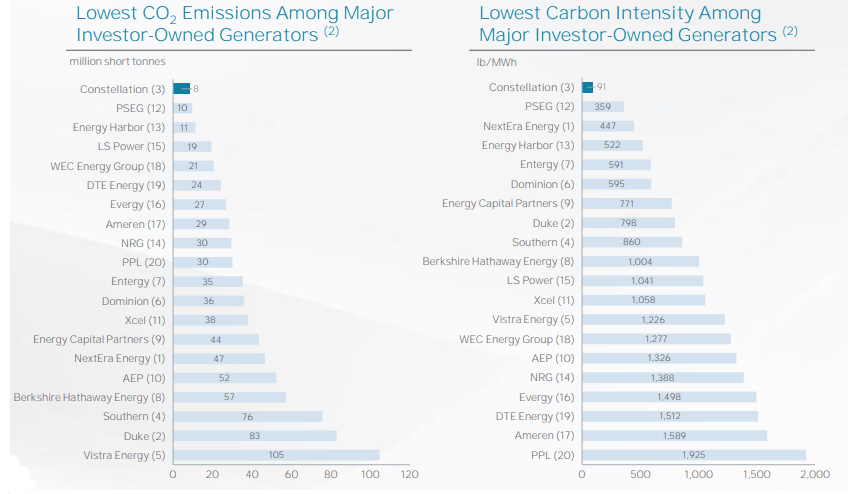

This might surprise you. CEG are the largest producer of Carbon-Free energy in the country (yes bigger than NextEra Energy, Duke Energy and The Southern Co). They have the lowest CO2 emissions among major investor-owned generators (NEE is 15th on the table whilst SO and DUK are 18th and 19th out of 20, respectively) and they have the lowest carbon intensity among major investor-owned generators too (NEE 3rd, DUK 8th and SO 9th). So, while NEE in particular has done a wonderful job of marketing themselves as a clean and green energy leader, CEG is in fact ahead of them in many key metrics. This places them right up there as a company that can do well by doing good!

Largest Producers of Carbon-Free Generation (CEG Investor Deck) Lowest Emissions and Intensity Among Major Investor-Owned Generators (CEG Investor Deck)

{kind=link}

Valuation

Looking at the immediate peer group, we'll see that CEG is valued in line with the large members of the group.

Direct peer group comparison CEG (Seeking Alpha)

However, because the largest part of their business has received a massive boost from the IRA, the result of which allows for a large degree of visibility into earnings and cash flows courtesy of the tax incentives and floor pricing, I think they should be valued more as an infrastructure play.

They hold large expensive, long-life assets and collect revenue on these assets like clockwork courtesy of a floor priced, inflation-adjusted contract with the US government, which makes them more like a 'toll booth' operator as a result. If you compare them to Infrastructure peers, the stock looks quite cheap.

Infrastructure peers trade at an average EV/EBITDA of 17x vs CEG's valuation of 10.34x as per Seeking Alpha screens.

EV/EBITDA Values of the peer group (Seeking Alpha)

Applying an EV/EBITDA multiple of 13x in line with Clearway Energy (CWEN), for example, puts the share price at $127.22.

DCF modelling is instructive too.

We have long-life assets generating long-term revenues as tax credits apply a floor to income until at least 31 Dec 2032. Assuming a risk-free rate of 4% (current 10yr bond yield = 3.92%) and a long-term market return of 8.5% (vs a long-term average of 11%) gives us an average of 6.25% which I'll use as my discount rate.

Being a Utility / Infrastructure investment, I'd expect far less risk and volatility from this type of company. For my growth forecast, I'll use 10% per annum for the next five years which will likely be skewed to the latter end of it from 2026 onward when a sizeable portion of the growth initiatives kick in and then reduce that to the long-term US inflation rate of 2% (in line with long-term inflation expectations). Overall, this produces a price target of $124.72.

CEG DCF (Author Inputs)

Combining the outcome from the two frameworks discussed above, we get a blended value of $125.97. Even if we then apply a 10% discount to this for those that don't like the 'Nuclear' Angle, we'd still get to target price of $113.37. At a current price of $77.00, there is a huge margin of safety here, almost 50%. This gives me some comfort that even if my assumptions are too bold, we have a lot of leeway.

Shareholder Returns

After its spinoff from Exelon Corp , the company began paying dividends at a fairly muted pace but did allude to the fact that the dividend would grow at 10% per annum. At the 16 Feb results announcement, this was reiterated however and, in a strong show of confidence, management doubled the current quarterly dividend from 14.1c to 28.2c which immediately doubles the base from which the 10% per annum growth will be achieved from. At the same time, they approved a $1 billion share buyback which effectively boosts shareholder returns to 5.5% (1.46% dividend yield and 4% of market cap bought back).

Risks

As with all investments, there are risks we need to consider. Over and above normal market and company risk for this industry, the following are also appropriate.

Regulatory oversight is a constant risk for Utilities as they need to work with government departments to ensure that they are adequately compensated for the capital spent on their infrastructure, both to develop and then subsequently maintain.

Interest rate risk is another. Utilities tend to have large amounts of debt on the Balance Sheet. They can do this due to the very reliable cash flows and strong line of sight they have to those cash flows. They need to make sure they make a suitable return after the cost of debt is taken into account.

The Nuclear production tax credits announced in the IRA are set to expire in 2032. Failure to renew them in some way or form may negatively impact returns.

Nuclear power plants have had two notable accidents, Chernobyl (1986) and Fukushima (2011). Although the real risk of Nuclear isn't as large as many fear, these events have caused angst amongst the public and officials and so need to be considered.

Input costs such as Uranium fuel prices are a risk and so is the price of power in general. Power prices need to be above their cost to generate so that companies can turn a profit.

Conclusion

As a recent spinoff from Exelon Corporation, Constellation Energy seems unknown and underfollowed by the broader market as is immediately noticeable by the clear lack of followers on Seeking Alpha. As the largest investor-owned carbon-free power generator in the USA, it's a company which will appeal to those investors looking to participate in the green energy revolution and the Inflation Reduction Act. As an owner of critical infrastructure with long-term contracts in place that are essentially guaranteed and backstopped by the US Government, the risk has reduced considerably. At a clear discount to infrastructure peers and a near 50% discount to my blended EV/EBITA and DCF valuation, I consider Constellation Energy a Buy at current prices and have added it to my model portfolio.

For further details see:

Constellation Energy Is Cheap With An Inflation Reduction Act Underpin!