CNSWF - Constellation Software And Topicus: Compounding At A Fair Price

Summary

- Constellation Software is a business of rare quality that investors should be seeking to own a piece of whenever an opportunity comes around.

- Constellation is starting to find it difficult to spend all its cash flow at its historical rates of return and thus faces some uncertainty.

- Spin-out subsidiary, Topicus.com, is a compelling piece to own as it is the same size as Constellation was in 2013-2014, has the same playbook, but no trouble reinvesting cash.

- Since 2013-2014, Constellation has returned 15x investors' money, making Topicus look especially attractive, even if it appears fairly valued.

Introduction

I think of investing in companies in the same way I think of owning a house; I think long-term and pay attention to the quality and value of the house over time, rather than its price fluctuations. I'm not speculating, trading, or even investing, I'm owning.

As a result, I prefer to invest in companies that have high returns on capital, indicating they will be able to compound over time, and with managers that have a sizable, personal stake in the business, meaning they will think like owners rather than employees. I wouldn't buy a low-quality house or let tenants make decisions about that house, and I expect the same of my stocks.

For example, I wrote about Brookfield (BAM), whose executives own 20% of outstanding shares, invests alongside 3rd parties in its own funds and has historically compounded at 20%. I also wrote about Nuvei (NVEI), whose founder owns 20% of outstanding shares, who, upon going public, issued each employee equity worth $100,000, and has high returns on capital. Most recently, I discussed SSC Security Services Corp . (SECUF), whose management team owns 36% of outstanding shares, whose returns on capital are in the mid teens and has a track record of compounding. These three businesses are more than just investments to me, they're ownerships.

I'm adding a couple to the list today: Constellation Software (CNSWF) (CSU:CA) and its Europe-based spin-off, Topicus.com (TOITF) (TOI:CA).

The Story

Constellation Software acquires mission-critical software companies that make and provide specific solutions for specific industries ("Vertical Market Software" or VMS). Constellation then collects the cash flows and redeploys that cash into acquiring more similarly promising companies. It has done so with now legendary success. Early investors have been rewarded with a 1,300-bagger, an investment of $10,000 has become $1,300,000. It's an astounding achievement.

Constellation Software is one you wish you'd known about and had the wherewithal to buy and hold early on (Seeking Alpha)

{kind=link}

One of the reasons this has been possible is because, though Constellation has grown into a large company, it functions like 100s of much smaller ones, called BUs, or "Business Units." To illustrate the point , only ten people occupy headquarters, despite there being tens of thousands of employees; CSU is hugely decentralized. It is like Berkshire Hathaway (BRK.A) (BRK.B) in this sense, which, for much of its existence didn't have more than ten people in its headquarters either, despite operating a business that measured revenues in the billions.

How it is not like Berkshire Hathaway in that each BU manager has significant autonomy over capital allocation; instead of funneling all the cash flow to the top where it is re-distributed, the local manager is largely in charge or choosing what to do with his/her BU's cash flow, though they receive minimum required rates of return on investment from higher up. That's another reason Constellation has been able to scale and compound so consistently; it doesn't rely on one person's competence in allocating a pile of cash, it has many smaller players finding smaller ideas with smaller amounts of cash.

The operating companies of Constellation Software (Constellation Software Website)

{kind=link}

Part of how this is achieved is by tying managers' bonuses to high cash returns on capital and organic growth, a unique system compared to the more common issuance of stock options to executives (which ties incentives to price not value). Essentially, each manager is paid based on how much value they create for the company. This is clearly good incentivizing, especially when we pair it with the fact that these managers are required to spend a large chunk of their bonus on buying Constellation stock on the open market and to hold it for at least 3-5 years. This policy not only avoids dilution, but it also aligns the capital allocators' interests with those of the shareholders/owners because they become one themselves. This decentralized autonomy and alignment of incentives with ownership underpins Constellation's success. The results are clear to see.

What I find most remarkable about this story is that Constellation's results rely on the decisions of hundreds of different internal investors, the majority of which deliver 20%+ annual returns; essentially, CSU has found a way to create hundreds of Warren Buffetts. This takes more than just managers being aligned with owners and well-designed incentives. How is it possible that one organization could have such a concentration of amazing investors when the investing world is replete with asset managers and hedge funds that can't even beat the S&P 500?

For that answer, we need to introduce the founder and fifth largest shareholder, Mark Leonard. One institutional investor letter described him as, "…the blueprint for an extraordinary CEO and deserves to be studied alongside the likes of Warren Buffett." Like Buffett, his shareholder letters are great place to learn, and to give us a sense of who Mark Leonard is, I'll use them extensively.

To put it simply, from what I can tell, Leonard has imbued Constellation with an extraordinary culture of learning, humility, and excellence. For example, in his 2013 letter he recommends Daniel Kahneman's, "Think Fast and Slow," saying, "Understanding the major findings in behavioral economics provides profound insights into investing and managing." I like this example because that book is a favorite of mine as well, while showing that Leonard not only reads, but reads to learn, something I consider important, but subtle.

He also is very familiar with the concept of deliberate practice (another favorite of mine), having read Ericson's work, now known commonly as the study that showed that 10,000 hours of proper practice creates an expert. In his 2013 letter, he uses this finding to describe the kind of people he wants sitting on the board and running the company. His idea is that these experts with 10,000 hours of VMS software investing can be coaches for those not as knowledgeable; Leonard is not just building value, he's building a culture of excellence.

Lastly, the realism with which he writes his expectations for Constellation are in stark contrast to the usually rosy views in which management teams frequently present themselves and their company. It's similar to Buffett, who wrote in 1985, "We will need also need a full measure of good fortune to average our hoped-for 15% - far more good fortune than was required for our last 23.2%." Fast forward to 2023 and Berkshire-Hathaway appeared to find that "full measure of good fortune," returning average 20.1% annually at last count. Leonard, in his 2018 letter, writes "I have difficulty forecasting long-term growth in Constellation's intrinsic value per share that exceeds 12% per annum." The frankness and honesty are refreshing. If replicating Buffett's style is anything to go on, we perhaps should take it with a grain of salt though; Constellation could have many years of 20% annual return left.

Mark Leonard's commitment to learning, evident humility and high standards seem to have been embedded in Constellation and must surely play a part in why hundreds of talented investors have been created in one company and generated such remarkable compounded returns. Constellation is to software investors what Brazil is to soccer players or Renaissance Florence was to artists; there's something about it that routinely creates "geniuses." CSU is a company of rare quality.

Leonard's assertion that he sees growth levelling out, should be taken seriously, however. Noticing that Constellation is beginning to generate more cash flow than it can reliably invest back into small, lowly valued VMS companies, he remarks in his latest shareholder letter, "If we are successful in acquiring one or two large VMS businesses per annum, then I anticipate CSU's return on investors' capital will decrease, but we will not have to return any of our free cash flow to shareholders." Essentially, Leonard sees a dilemma where they are having to choose between accepting a lower return or stick to their hurdle rates and be unable to reinvest all their money. In either situation, Constellation will not be able to match historical returns.

There is a possible remedy to this situation; Constellation finds an area outside VMS companies in which to invest with similar success. Leonard suggests they're looking at options: "…we are trying to develop a new circle of competence. We are seeking attractive returns, a sustainable advantage, and the ability to deploy large amounts of capital outside of VMS." Every investor looks for this, whether they find it or not, we'll just have to see whether they do. If there was ever an organization to do it though, it would be one like Constellation.

Leonard suggests we think along those lines, saying, "This will require highly contrarian thinking and is likely to be uncomfortable in the early going. Hopefully, we have built enough credibility to warrant your patience as we explore new and under-appreciated sectors." Personally, even if Constellation is like Berkshire-Hathaway and will always find ways to generate high rates of return, I think this sounds like future buying opportunities will come available as they go through that transition. I'd prefer to wait and see with Constellation for this reason, especially because there are other ways to invest in the company that can still invest all their capital at high rates of return.

Topicus

Topicus B.V., a Dutch VMS provider that grows organically, was acquired by Constellation, merged with TSS, an existing Business Unit focused on acquisitions according to the Constellation playbook, and spun-out in 2021 to create the new Topicus.com. The result is a Europe-focused VMS software acquirer and organic grower. Just because it's spun-out doesn't mean it's cut-off from Constellation though; to the contrary, CSU owns a 50.1% stake, controls the board, and the CFO of Constellation, Jamal Baksh, is also the CFO of Topicus. It even releases earnings with Constellation. Topicus is far from being separate; it is optimistically thought of as Constellation Software in Europe, except with roughly the cash flow of Constellation in 2013-2014 and more organic growth.

Investors are justifiably excited. If it can replicate Constellation's success over the last 10-15 years, Topicus is a must-own stock. The addition of higher expected organic growth is also significant. In Leonard's 2013 letter, he described how he asked all their analysts to send them their valuation models for Constellation. After fiddling with them, he found that, "Varying the organic growth assumption has a tremendous impact on the intrinsic value of a CSU share. Add in another 2.5% organic growth to the base line assumption and you get more than double the intrinsic value." In short, more organic growth is a big deal.

Unfortunately, Topicus has not been delivering on that front so far. Below is Topicus' organic growth of revenue for the last 8 quarters:

The impact on organic growth as a result of the addition of Topicus B.V. to TSS in 2021 is clear to see, but it's fallen off. (Author's Chart - Numbers from Q3 Earnings Report)

This is not any better than Constellation ever achieved, and not what was expected when Topicus was spun-out. That said, it's been a wild couple years with the pandemic and inflation, particularly in Europe. Topicus will need some time to show what it can do on the organic growth front in a more "normal" environment (if that exists).

According to CEO Daan Dijkhuizen in their Q1 earnings call, they plan to grow organically by adding value to existing verticals (like educational administration software to student tracking), hopping into adjacent verticals (like mortgage solutions to wealth management) and expanding geographies (by following existing clients to other countries). Whether this works or not remains to be seen, but it has worked in the past, and the present is surely obscured by several unusual macro factors including the pandemic, inflation, the Russian invasion, and the possibility Europe has been in a recession. If Topicus can get back to growing at 7-10% organically, it has an edge over Constellation in the 2010s.

The other part of the business, TSS, focuses heavily on acquiring niche VMS companies at high rates of return, like Constellation. On that front, Topicus has been very successful.

Note how they gathered cash in 2020 and deployed in 2021, to take advantage of good prices. (Author's Chart - Numbers from earnings reports)

Topicus has successfully deployed all its cash, something Constellation is beginning to struggle with (that's why it pays a dividend). Simply acquiring businesses is not altogether difficult however, we would also like to see that these are quality businesses being bought at good prices.

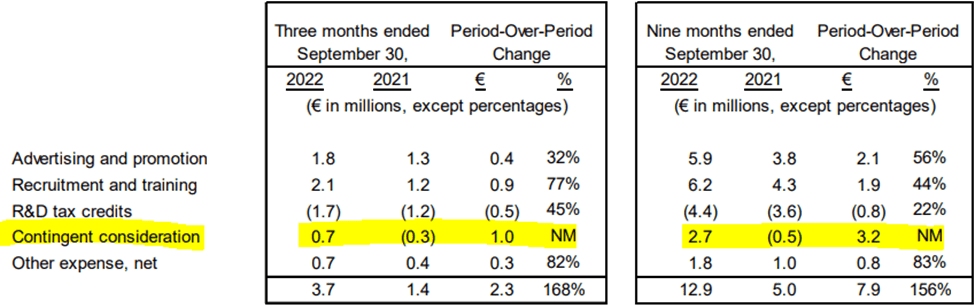

One way to check is to see whether they've had to expense any impairments, meaning they paid too much. A second related factor is to check contingent considerations, the amount paid by the acquirer to the acquiree if the purchased company performs above expectations. No impairments and high contingent considerations are what we're looking for because it means Topicus paid a good price and the companies bought are performing well.

Here are the contingent considerations:

Contingent considerations are positive, indicating the businesses Topicus purchased are performing well. (Topicus Q3 Earnings Report)

{kind=link}

Here are the impairments:

Thus far, in 2022, there have been no impairment charges. A good sign for investors! (Topicus Q3 Earnings Report)

{kind=link}

The lack of impairment charges indicates they didn't overpay and the increased contingent considerations shows those companies they purchased are performing well. Clearly, Topicus can invest in quality companies at decent prices, just like Constellation. However, if those investments don't have high cash returns on capital they will not be worth it. Below is Topicus' current cash return on invested capital compared to Constellation's:

TOI is in euros and CSU is in CAD. Also, the idea that ~40% of capital invested gets returned as cash is remarkable. (Author's Calculations, Numbers from Seeking Alpha)

Both TOI and CSU have monster returns on capital, making them both very desirable businesses to own. That said, Topicus gets the nod from me because it appears to be as adept at acquisitions as Constellation except is a similar size to Constellation in 2013-2014, when it had little trouble reinvesting all its free cash flow at high rates of return. Though it hasn't shown it yet, Topicus also has the potential for more organic growth than Constellation ever had. In short, Topicus is at least as attractive as Constellation was ten years ago, which is saying something considering CSU's cash flow has increased 600% since then.

Everything has a price however, which we'll investigate next.

Valuation

To get a very general sense of valuation I like to first check the multiple the stocks are trading at compared to their historical mean. If Topicus is indeed a small Constellation, then CSU's historic multiple will be a useful comparison.

I take it for granted that Topicus will trade similarly to Constellation, especially once it gets off the Canadian Venture Exchange and onto a larger exchange (Seeking Alpha)

{kind=link}

According to Seeking Alpha, Constellation is trading near the higher end of its historic multiple, while Topicus is in the lower range. This makes me look even closer at Topicus than I was before. To be honest, this may be all we need to know. We can buy into an extremely high quality compounder at the lower end of its trading range. Personally, I like to take a closer look, incorporating future growth into the equation, but this is already looking promising.

To take a closer look, a discounted cash flow analysis is preferable. It allows us to test assumptions, and estimate fair value based on those. One of the issues with DCF analyses of perennial compounders like Constellation (and probably Topicus) though is that to be conservative we only estimate out the next 5-7 years growth in free cash flow, then assume it slows, and use that to value the business. But compounders, by definition, don't slow. As a result, the method we are using will probably undervalue the business to a substantial degree, simply because it assumes the company will eventually slow and/or stop growing.

To value Topicus I'm going to use 7 years of estimated future growth, simply because that's the farthest into the future I can prudently allow myself, even while acknowledging that the model has limitations. Also, because TOI was recently spun-out and we have limited trading data, I use CSU's history as a model for Topicus' future. This is also a weakness, but for the all the reasons I mentioned earlier, not unwarranted.

With that said, here are the assumptions and explanatory notes:

Shares outstanding are left out, as stock-based compensation doesn't exist for Constellation or Topicus and their capital can be invested in better opportunities than their own stock (Author's DCF Assumptions)

{kind=link}

These assumptions are lower than historical means but still not particularly conservative, especially combined with the fact we're using 7 years of cash flows instead of the more typical five. I think this is justified though because CSU has been remarkably consistent and predictable. The resulting fair value estimate is below:

The stock is trading around fair value (Author's Calculations)

As we can see, if we require a 15% return, we would be buying TOI up to $87CAD. I prefer to have a margin of safety though. Since its current price is around $76CAD, we could buy it with a 12% margin of safety. It's worth noting, if we only use five years of data instead of seven, the stock has no margin of safety and instead trades around fair value. The exchange rate also plays a part since Topicus operates in Euros but is denominated in Canadian dollars (it trades in Canada like Constellation). Personally, this valuation does not make me salivate, in fact it leaves a slightly unpleasant taste in my mouth. I don't love buying stocks at or around fair value; I much prefer to buy them below fair value.

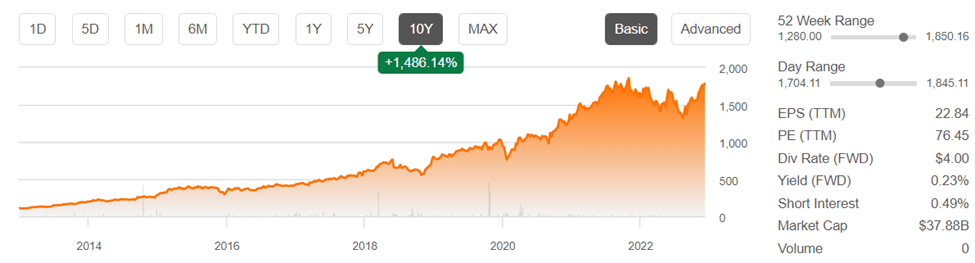

Chris Mayer, the author of "100-Baggers" and long-time owner of Constellation Software made the astute observation that high-returning stocks will spend most of their time, by definition, at all-time highs. Buffett, in his 1987 letter quipped the inverse but with the same message, "I searched for 'bargains' - and had the misfortune to find some." The message: when it comes to elite businesses, bargains are exceedingly rare.

They are also not necessary for a great return. Take Constellation for example, it has never been cheap, almost always trading above 20x, but if you'd bought 10 years ago here's how you did:

Constellation Software's return over the last 10 years (Seeking Alpha)

{kind=link}

To be fair about a 1/3rd of that 1500% is multiple expansion, take that out and you would still have 10x your money in 10 years. This is despite the stock trading at a seemingly "high" 20x cash flow when you bought it. It seems more important to not overpay than it is to get a bargain when buying great businesses.

Personally, that's a hard concept to wrap my head around, as I see stocks in the current market that according to all traditional methods of valuation appear far cheaper. This is especially the case as value investing is a term that has almost become a moral imperative. If we look at return potential though, by buying Topicus at its current price, around what our valuation methodologies consider "fair value," we are giving ourselves a chance at a huge return, and almost certainly something superior to the bargains that may appear so attractive in the present.

As such, Topicus' valuation is not a concern, simply because it is not overly demanding.

Conclusion

Constellation Software is a remarkable business that can be justifiably compared to Berkshire-Hathaway. CEO Mark Leonard has found a way to make a multi-billion-dollar business operate like hundreds of smaller businesses, with most managers generating returns on capital well in excess of 20% per annum. Constellation Software is the type of business you want to own, like house, not just as an investment. That said, it has become large enough now though where new ideas are going to need to drive the next phase of growth, if it wants to match historical returns. Leonard could pull off a Buffett and just keep compounding, but we don't have to bet on it.

Topicus.com, spun-out of Constellation in 2021, is about the size of its parent in 2013-2014, and essentially a replica of it too, but with potentially more organic growth and a lower valuation. For these reasons, it is, to me, more compelling. Fair value of its stock is somewhere between $76 CAD and $90 CAD, but we shouldn't be discouraged by the fact Topicus is trading around its conservative fair value; Constellation was too in 2013-14 and is up 15x since then.

I am a long-term owner and a buyer of Topicus at current prices.

For further details see:

Constellation Software And Topicus: Compounding At A Fair Price