CSTM - Constellium: Benefiting From The Strong Market Position And Pricing Power

2023-08-07 00:42:42 ET

Summary

- Constellium reported another slump in Q2 2023 revenue while maintaining its pricing power and strong positions in aerospace and automotive end markets.

- The outlook for the company remains favorable due to business model streamlining and focus on higher-margin areas and value-added production.

- The valuation model incorporates more resilient revenue pattern consideration, resulting in up to 17% upside potential.

Constellium (CSTM) is experiencing a downturn in revenue growth, which is driven mainly by packaging end-market weakness. However, the company is coping relatively well due to its pricing power and ability to exploit more successfully the momentum in the aerospace market. In addition, Constellium streamlined its business model in order to emphasize higher-margin areas in the product mix. With this in mind, I believe the company could go beyond the management's EBITDA forecast due to the strong focus towards more value-added products. In my previous piece on CSTM , I estimated a 62% upside as a result of the company’s favorable position in resilient and secular growth driven end-markets and cost management activities. Since then, CSTM realized 50% of it and I believe that another 17% upside is still hanging around. With this coverage, I would like to reaffirm my Buy rating on Constellium going through the second-quarter financial overview, new expectations and some tweaks to the valuation model.

Financial overview and outlook

In my previous article, I stressed the Packaging end-market as a fulcrum of continued profitability for Constellium even in turbulent times. The market indeed showcased resilient growth during the COVID period, while the prolonged inflationary environment brought demand weakness here as well. As a result, the company is going through a downturn in its anchor segment, which used to shape around 40% of the revenue-mix. However, thanks to the diversified business model, Constellium is limiting the damage by exploiting the strong momentum in the Aerospace end-market. Let’s now dig into the recent financial results.

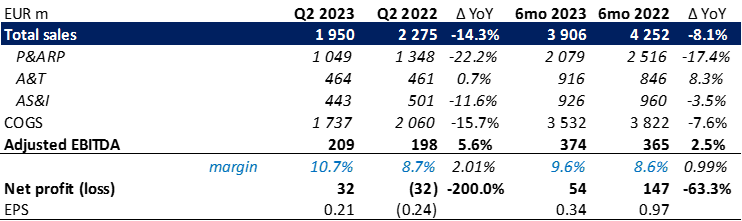

Q2 2023 financial results (company reports)

{kind=link}

Constellium reported a 14.3% decline in second-quarter revenue despite favorable pricing and mix effects. The main reasons could be attributed to lower shipments, which were down by 6.1% YoY to 398k mt, and aluminum price normalization.

The P&ARP segment took the hardest hit with a 22.2% YoY drop in revenue to EUR 1.05 billion, due to the weakness mentioned in the Packaging end-market. Total shipments fell by 6.8% YoY mainly as a result of 12.2% YoY decline in packaging rolled products, which was partially offset by 16.4% growth in automotive rolled products. In the AS&I segment, CSTM reported an 11.6% revenue decline as a consequence of an 8.3% YoY lower shipments, where the automotive extruded products balanced the decline in the extruded products to other markets.

Switching the focus to Aerospace, at first glance revenue in the A&T segment was flattish in the second quarter. Shipments also remained unchanged, which was a trade-off between 30% YoY growth of aerospace rolled products and 15% YoY decline of transportation, industry and defense products. However, the adjusted EBITDA showed completely different numbers, or 53% YoY surge, which is really striking how much pricing power the company has in this segment. Overall, the Aerospace industry reported strong results in the first half of the year, where the two major OEMs, Boeing and Airbus, delivered 582 commercial jets , or 14% more than a year ago. As a result, CSTM left EUR 209 million profit on Q2 EBITDA line, up from EUR 198 million in the base period.

Now let’s highlight the favorable pricing & mix effect, which was the main contributor (EUR 256 million) to the value-added revenue.

Value-added revenue bridge (company presentation)

The latter increased by 11% YoY to EUR 785 million, which reflects sales without the cost of metal. We can think about this metric as a profit measure, where the pricing effect clearly came from the solid performance in the Aerospace market.

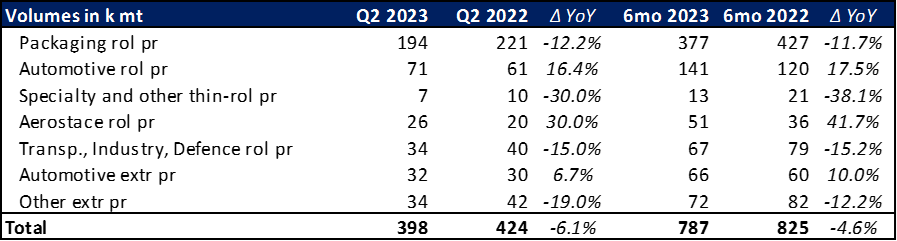

Shipments by product line (company reports)

{kind=link}

Looking at the product mix, it's hard to say that it has improved just because of the drop in the packaging, specialties and TID shipments. However, the improvement could happen in the next few quarters to come as a result of the sale of three extrusion plants for a total cash consideration of EUR 48.8 million. The facilities are dedicated to serving the lower-margin construction, industry and transportation markets, which are going through a cyclical weakness and are far from a key focus point of the CSTM business model.

In the meantime, the share of the core end-markets, packaging, automotive and aerospace, accounted for 77% in the TTM revenue. Going forward, I believe that the share could reach 80% in the back half of the year due to lower specialties products (as a result of the divestments), strong momentum in aerospace and resilient automotive.

EU new passenger car registrations (ACEA)

{kind=link}

From the above chart, we can see that the company’s automotive rolled and extruded shipments are matching the growth of the EU vehicles registration. The same goes for the US market, which is trending with strong double-digits as well.

Overall, I expect 5% YoY growth for automotive rolled and extruded sales in the third quarter of 2023, and a solid 30% YoY surge for aerospace rolled product sales. On the other hand, I would incorporate a 20% YoY decrease in packaging rolled product sales, and a 25% YoY shrink for specialties and TID sales.

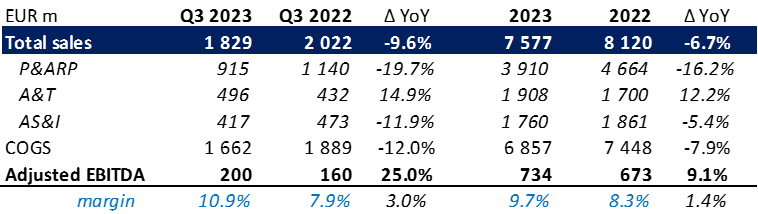

Q3 and FY2023 forecasts (company reports; author’s estimates)

{kind=link}

The above assumptions should result in the following segment performance in Q3: P&ARP (-19.7% YoY) due to the inventory adjustments in the packaging market; A&T (+14.9% YoY) thanks to the strong pricing and demand profile in aerospace; and AS&I (-11.9% YoY) as a consequence of weak specialties shipments. For FY2023, I assume a 6.7% sales decrease to EUR 7.57 billion and a favorable 80% revenue-mix as mentioned earlier. Adjusted EBITDA is estimated at EUR 734 million (700-720 guidance range) on a margin of 9.7%, +140 bps improvement.

Valuation takeaways

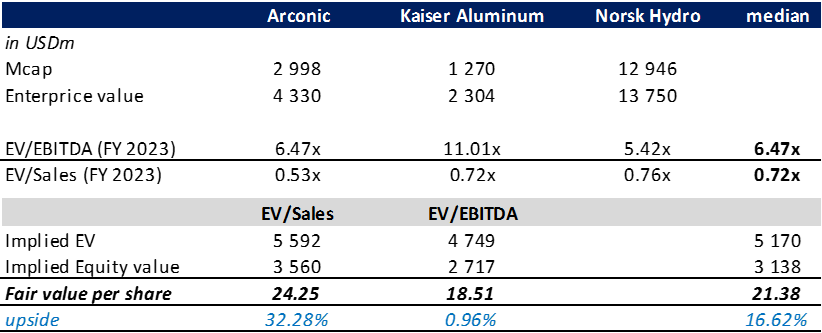

Compared to the competitors like Arconic ( ARNC ), Kaiser Aluminum ( KALU ) and Norsk Hydro ( NHYDY ), the company is trading at a 5.96x forward EBITDA multiple, which represents an 8% discount.

At the same time, CSTM stock is quoted at 0.57x next-year Sales multiple, pointing out a 23% discount compared to the selection.

Applying my estimate of EBITDA for 2023 should yield $4.75 billion enterprise value and $18.5 fair value per share, implying that the company is fairly valued at the moment. This valuation is the same as in my previous coverage. However, I believe that the EV/Sales consideration should be incorporated into the model and the following trends could make it clear why.

Although Constellium has relatively the largest exposure to the packaging market, which is in a downturn currently, the company managed to keep up a more resilient revenue pattern, or less negative to be more precise. It seems to me that CSTM is more successfully exploiting the strong momentum in the aerospace and automotive end-markets, and has superior pricing power. As a result, it makes sense to add these thoughts to the valuation.

Valuation (Seeking Alpha; author’s estimates)

{kind=link}

With the EV/Sales multiple alone, the company appears in a new light with an implied enterprise value of $5.59 billion and $24 value per share. However, I would play this around with equal weights in between to conclude that CSTM has a potential for 17% upside up to $21.4 value per share.

To sum up, I believe that CSTM still commands a decent upside to be a Buy rated. Constellium has a strong consumer base, which could allow it to extract maximum momentum from the outperforming strategic end-markets and limit the damage from the weak segments. Moreover, CSTM took the right step to streamline the business model and focus on higher-margin areas to drive a favorable tilt in the revenue-mix. With these in mind, I am inclined to believe that Constellium could surpass the high-end of the management EBITDA forecast of EUR 720 million.

Risk factors

Operational challenges at Muscle Shoals remain a constraint factor to the company’s financial results, as it’s mainly focused on servicing the packaging end-market. The latter is going through unfavorable developments, which could further drive the shipments down. Although the automotive market remains resilient, the continued inflationary environment could bring weakness to automotive rolled products demand as well.

For further details see:

Constellium: Benefiting From The Strong Market Position And Pricing Power