CSTM - Constellium SE: Margin Decreases Are Likely Going Forward

2023-05-03 04:45:50 ET

Summary

- Constellium SE barely saw a shift in revenues on a yearly basis as seen in the last report which might indicate the company is in a stable position.

- The need for aluminum seems inconsistent as the end markets the company has, but the long-term trend seems positive.

- I think there is more downside to the margins which could create a better buying opportunity as the share price might fall, until then a hold is what I will do.

Investment Summary

Constellium SE ( CSTM ) is a company producing high-quality aluminum products and solutions. They operate in several countries across the world, including Europe, North America, and Asia, and serve a wide range of industries such as aerospace, automotive, packaging, and construction. Their product portfolio includes various rolled and extruded aluminum products Constellium's solutions range from lightweight automotive body panels to advanced packaging products that help to minimize food waste.

In the latest earnings report I think the result was a relief to investors as the revenues just saw a 1% decline YoY and in all honesty it could have been a lot worse given the lower price of aluminum compared to 12 months ago. The management seemed to have achieved what was expected and with inconsistent demand across different markets, I think there might be more room for the stock to fall before starting a position. Because of that, I will be rating it a hold for now. I believe in the long-term outlook for the market, but buying at a great price is also very important.

Quarterly Result

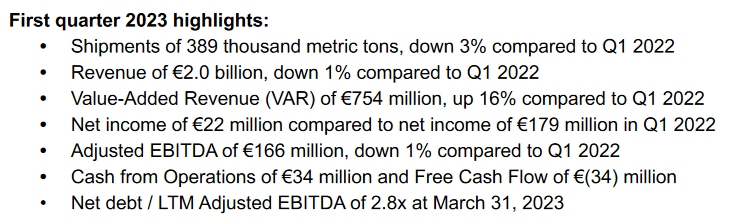

As reported in the last earnings presentation CSTM saw a 1% decline YoY in revenues as they came in at $2 billion. One comment that I found interesting and also reflects the situation was from the CEO Jean-Marc Germain " Looking across our end markets, the recovery in aerospace continued with shipments up over 50% compared to last year. Automotive demand also continued to improve with higher shipments of both rolled and extruded products. Packaging shipments were down in the quarter as demand softened, and we continued to experience weakness in certain industrial markets". I think this reflects some of the inconsistencies that will be happening for companies like CSTM in the coming quarters. The demand won't be as broad as before perhaps and it will be important to keep up margins whilst also investing in the segments that are seeing demand.

Report Highlights (Q1 Earnings Report)

{kind=link}

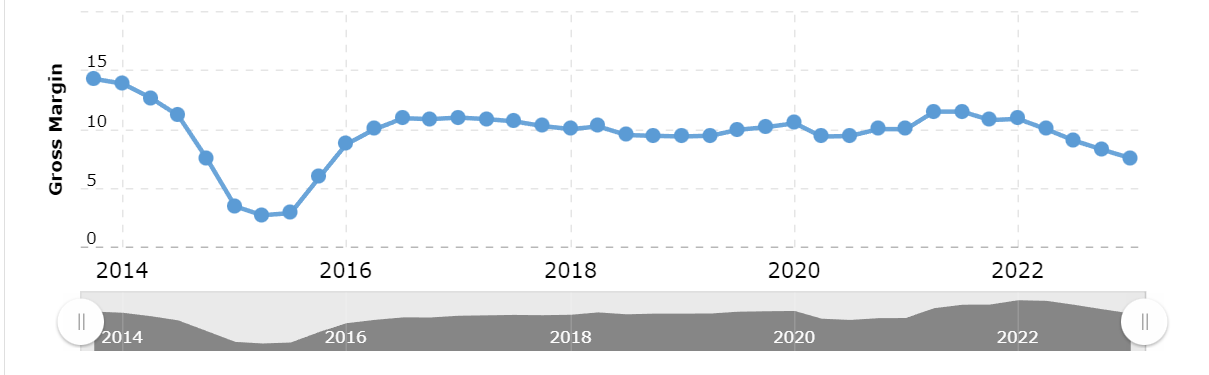

Apart from that, the margins have obviously taken a turn for the worse from last year. As the price of aluminum rose sharply so did the margins and revenues for companies like CSTM. This was reflected in the report too as the net income was $22 million for the quarter compared to $179 million a year earlier. The loss was explained to also be because of unfavorable changes in gains and losses on derivatives primarily related to the company's metal hedging positions. Paired with lower gross margins and this is the result you get.

Company Gross Margins (macrotrends)

{kind=link}

The CEO still remained optimistic about the outlook, however, stating they believe they will achieve their 2025 target of over $800 million in adjusted EBITDA. They also raised the cash flow guidance for the year to around $125 million for 2023. I don't think this raise is enough however to stop the slight share dilution that has happened during the last few years though.

All in all, I think the report didn't surprise me too much and the company seemed to have weathered the storm quite well. I still think there is more downside for the margins and it will be interesting seeing this in the coming quarters.

Risks

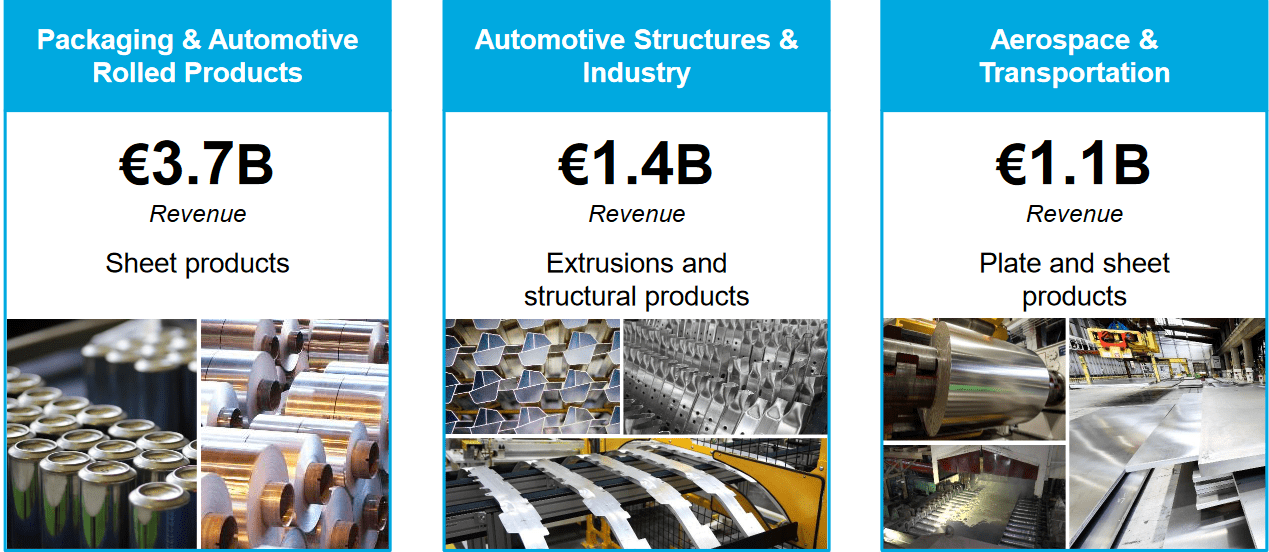

Investing in commodity companies can be risky since their revenues are directly tied to market prices. However, companies like CSTM have an advantage over others in their ability to generate more revenue and with better margins, resulting in significant increases in share prices during market booms such as in 2022. In the last earnings report the company noted that the segment seeing a lessened demand was also the largest one in the company, Packaging & Automotive Rolled Products. I think there is more pain ahead and this will be reflected in the coming earnings report too. With this segment also making up more than 50% of all revenues it places a risk that revenues will proportionally be affected despite other segments perhaps seeing an increase. This creates quite inconsistent growth and it becomes difficult seeing where the true value is.

Company End Markets (Investor Presentation)

{kind=link}

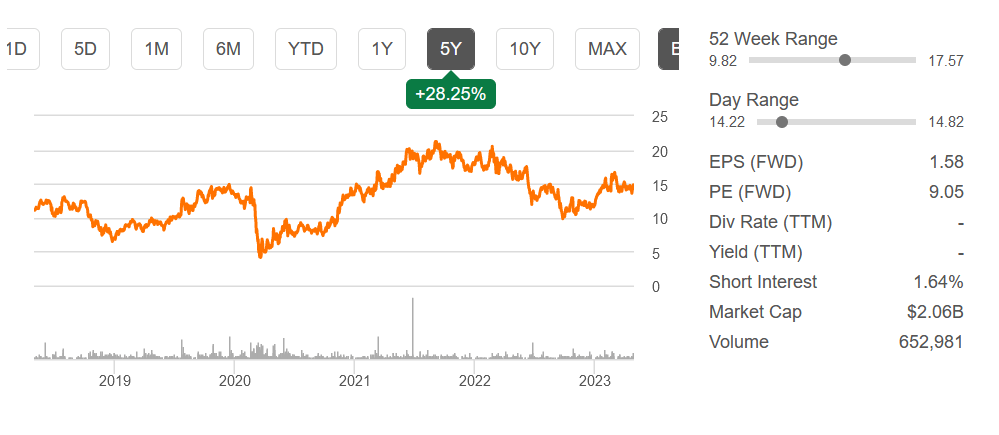

The biggest risk in purchasing a company like CSTM is buying too early. The best deals are often found when margins are at their lowest and there seems to be no end in sight for the decrease. Buying when margins are great is the opposite of value investing in commodity companies. As I said, I think there is more pain ahead that could make for a better buying opportunity. The forward p/e is still at just 9 and I think it could go significantly higher than that before and the investment case would be realistic.

Valuation & Wrap Up

Constellium SE has managed to hedge relatively well from a year ago, whilst other companies saw a drastic decrease in revenues and margins as prices became less favorable. But as I believe there is more downside to be had as we are still in a difficult macroeconomic environment the forward p/e could go up as estimated revenue gets a revision. Looking at the TTM numbers the company actually looks undervalued as p/cash flow is just under 4 and p/s is 0.23. But investing isn't done solely on previous numbers of course.

{kind=link}

I won't be investing or suggesting into the company until I see the margins being more stable and perhaps seeing a shift upwards too. I think that could indicate a new boom in the company revenues. Investing too early is dangerous when it comes to commodity companies and it usually opens up too much risk to a portfolio without too much appreciation in value. For now, I think the company deserves a hold rating and perhaps a buy rating when the share price goes down further.

For further details see:

Constellium SE: Margin Decreases Are Likely Going Forward