CSTM - Constellium: Sensitivity To Exogenous Factors Capping Upside Potential Rate Hold

2023-10-26 01:17:51 ET

Summary

- Constellium has potential for a rebound in FY'22 due to changing macro regime and attractive risk-reward profiles in adjacent sectors.

- CSTM's Q3 FY'23 earnings were below expectations, with reduced shipments and softer aluminum pricing impacting its operations.

- The uncertain outlook on aluminum pricing and the high correlations between spot aluminum and CSTM's stock price are important factors to consider.

Investment Brief

A changing macro regime, along with more compelling risk-reward profiles in adjacent sectors to tech and healthcare, means there is scope for specialty metals companies to catch a bid in FY'22. Constellium ( CSTM ) has been heavily sold in recent weeks and came onto our radar earlier this month, trading at compressed multiples, and pushing to its 200DMA.

CSTM posted its Q3 numbers today, and results were a downside versus consensus expectations. Challenges were observed throughout its operations last quarter not in the least related to reduced shipments and softer aluminium pricing. This hasn't come as a surprise, seeing as aluminum price weakness is often correlated with sharp and violent pullbacks in the company's stock price.

Critically, the distribution in (i) the projection of its future cash flows, and (ii) market pricing going forward, are likely to be biased to the downside in my opinion. This is supported by factors raised in this report. Net-net, I rate CSTM a hold.

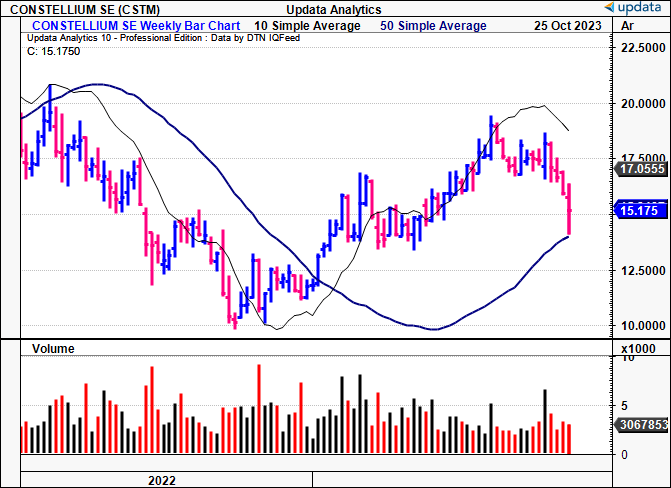

Figure 1. CSTM long-term price evolution, cycling within wide range, now trades below 50DMA and touching 200DMA.

{kind=link}

Critical facts pattern to hold thesis

1. Macroeconomic backdrop

Uncertain outlook on aluminum pricing

The key macro numbers continue to dominate market tensions and capital flows in the back end of 2023. The yield on the 10-year has pushed above a 5 handle, having increased by ~125bps since its flattening in July. According to a recent note from UBS, " the negative market sentiment is currently in the driver’s seat for yields ". It says the data has persistently surprised to the upside on:

(i). Growth and consumer resiliency, evidenced in key economic data,

(ii). The market's inability to conceive the magnitude of Fed hikes at each point along the way.

" These variables have been the driver of rising yields ," it says. "[ I]t’s the consistently above-consensus economic data releases coming out of a very difficult forecasting environment that has been the main driver ".

Meanwhile, prices of industrial metals remain at elevated levels, despite their broad selloff over the last 12 months. Aluminum sits in an interesting position. Demand for the metal is high, but there is a high cost of energy in its production. In a separate note from August, UBS also said that " [g]iven the high energy consumption in aluminum and zinc production, lower energy prices in Europe and better availability of power in China have reignited the risk of increased aluminum and zinc supplies in 2H23" .

It notes that smelting production in China's Yunnan province could add 1.2mm tonnes of capacity, expecting rates to lift in H2 this year. Critically, it also notes the bulk of aluminum stored in LME warehouses is produced in Russia, which, if removed from the LME system, would reduce 80% of the visible inventories would fall to "extremely low levels". It looks to a 2,500/mt price target on aluminum over the long term.

Figure 2.

Source: UBS Investment Research

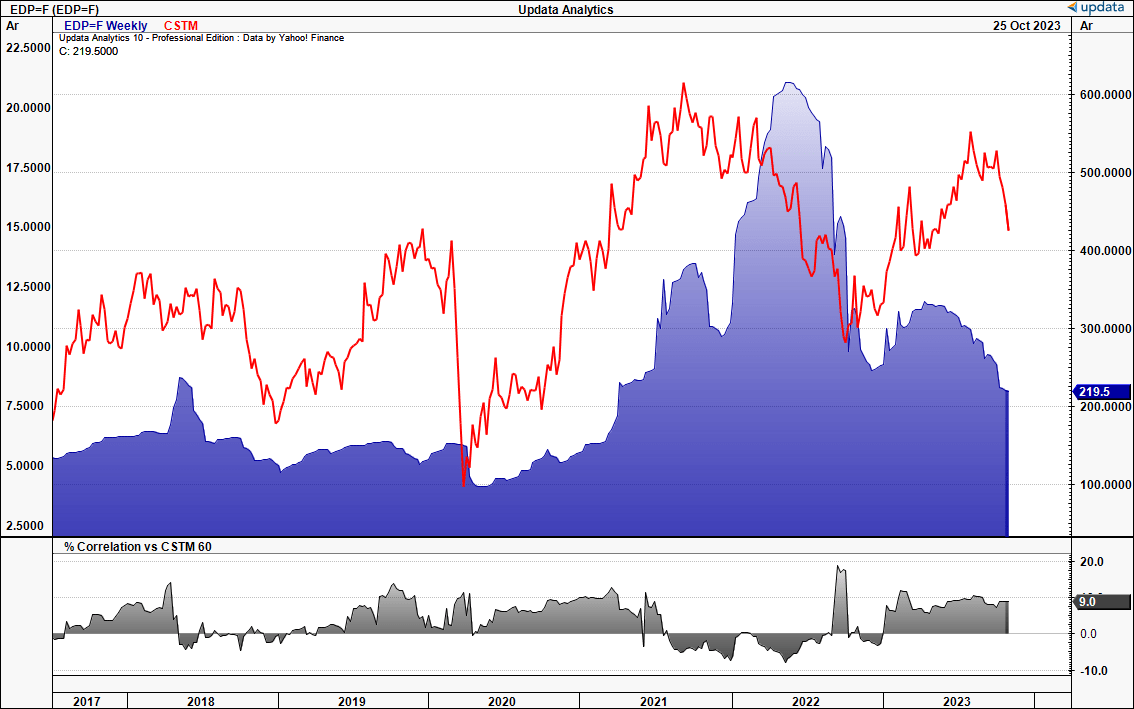

This is important data for CSTM, given 1) it is in many ways a price taker on the market's pricing of aluminium and 2) the high correlations between spot aluminium and its stock price over the last 5 years (Figure 2a). No surprises on the 2nd point, but it's important to consider moving forward. We've not got CSTM selling back at its 2019 levels, whilst aluminum prices remain elevated.

Figure 2a.

{kind=link}

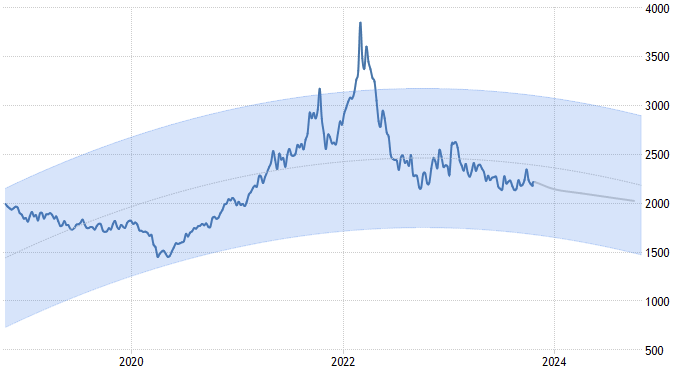

There is scope for spot aluminum to trade at the $2,500/mt level. Those at Trading Economics project the breadth of price ranges based on historical data. The key fact is that trends are declining, and the most likely path could be within the $2,000–$2,200/mt region.

Figure 3.

{kind=link}

2. Q3 FY'23 earnings analysis

Critical insights

Analysis of CSTM's economics and financial results from Q3 reveals it was a mixed period for the company. The four most critical insights in my opinion are as follows.

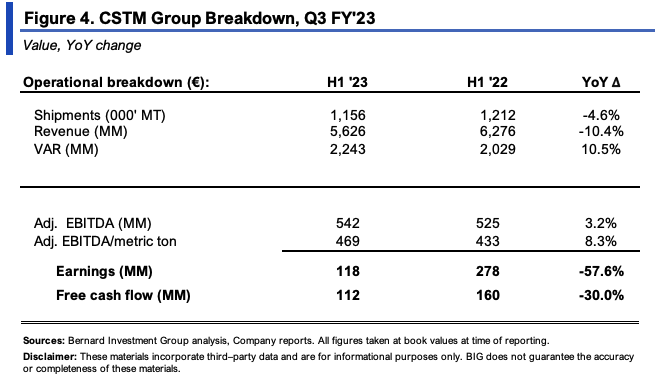

One, total shipments for the quarter amounted to 369,000 metric tonnes, marking a 4.6% decrease in comparison to Q3 2022. This brings shipments to 1.2mm metric tonnes for the YTD, also down 500bps YoY. This decline is attributed to several factors impacting the company's operations.

Two, revenue for the same period reached €1.7Bn, representing a 15% decrease from Q3 last year. Consensus estimates were €1.9Bn and 6% decrease, so the miss was more than double in percentage terms. This was due to a combo of (i) lower shipments and (ii) reduced metal prices. Looking ahead, management forecasts adj. EBITDA between €700mm —€720mm, on FCF of ~€150mm.

Three, it pulled this to adj. EBITDA of €168mm, up 5% YoY, on earnings of €64mm, a decrease from the €131mm last year. It converted 44% of adj. EBITDA as FCF (€74mm), amounting to €112mm in FCF spun off this YTD. Both are down YoY, as CapEx charges were higher—likely a result of asset/cost inflation.

Four, and conversely, it put up value-added revenue ("VAR") of €704mm, reflecting a 5% increase YoY. This was up 11% YoY for the YTD to €2.2Bn. This growth can be attributed to improved pricing and product mix. However, these gains were hindered by lower shipments, metal costs, and FX headwind, thus weren't realized below the top line.

{kind=link}

As to the divisional highlights:

- Packaging & Automotive Rolled Products—

- Shipments: 261,000 metric tons, down 2% YoY.

- Q3 2023 revenue: €1.0Bn, down 16% YoY.

- Primary factors for revenue decreases: Lower shipments and metal prices, "challenges at [its] Muscle Shoals facility", despite some improved pricing and product mix.

- Q3 2023 adj. EBITDA: €67mm, down 14% YoY.

- Reasons for the decrease: Lower shipments, increased OpEX (due to inflationary inputs), compounded by the lower metal costs.

- Automotive Structures & Industry—

- Shipments: 55,000 metric tons, a decrease of 15% YoY.

- Q3 2023 revenue: €370mm, down 22% YoY.

- Primary drivers for the revenue decrease: Lower shipments and metal prices, countered by enhanced pricing and product mix.

- Q3 2023 adj. EBITDA: €26mm, down 27% YoY.

- Reasons for the decrease: Reduced shipments and higher OpEx.

- Aerospace & Transportation—

- Shipments: 53,000 metric tons, down 3% YoY.

- Q3 2023 revenue: €404mm, reducing by 6% YoY.

- Main contributors to the revenue decrease: Lower shipments, metal prices, and offset by better pricing and product mix.

- Q3 2023 adj. EITDA: €79mm, up 76% YoY.

- Key driver for increase: Enhanced pricing and product mix—despite the lower shipments—and increased OpEx.

3. Technical factors to price visibility

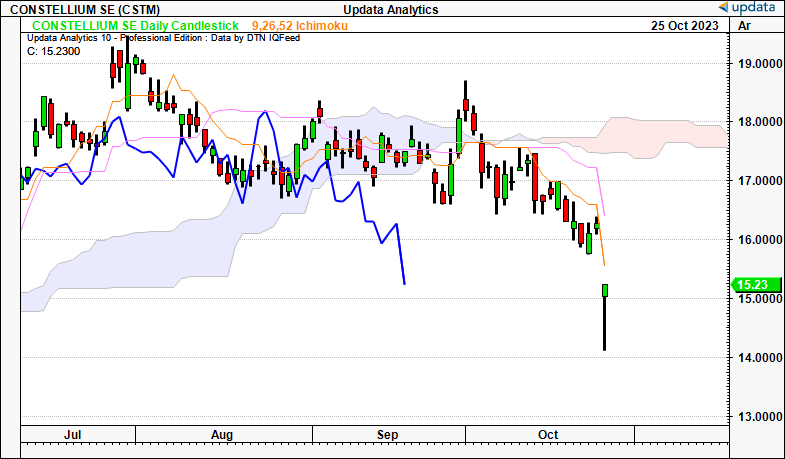

CSTM has traded within a wide distribution in the last 3 quarters before gapping down following a sharp vacuum pulling prices lower at the $15 region. Markets tend to move from pockets of high usage to low usage, so there is risk that CSTM could continue selling lower to complete the distribution shown in Figure 5. This would continue the downtrend set earlier this quarter.

Figure 5.

Data: Updata

The distribution is also in a positive skew adding weight to the prospect of a series of ongoing small losses, continuing the downside. The catalyst to change this setup would be related to aluminum market pricing in my view.

Figure 6.

Data: Updata

With the selloff in pre-market as I write, we have activated the $13 downside target, and I believe that the stock will push to this level in the coming days given the miss and what's been seen since it topped in July.

Figure 7.

Data: Updata

The gap down following the update has only extended its position away from the cloud, adding to the negative positioning. In my view, this tells me to remain neutral over the coming weeks at least. A break above $18 is needed to suggest we are bullish again. This looks to be a key level for CSTM as well (the $18 level).

Figure 8.

{kind=link}

Valuation and conclusion

The stock now sells at 6.15x forward EBITDA estimates, quite the discount when the sector is priced at 7.55x forward. However there is far too much risk to contend with in my view.

One of the issues I have with those in the metals space is there is typically no differentiation on price or product. Specialty metals such as aluminum do a good job at overcoming this, by providing select products to industry—in CSTM's case, its offerings in packaging + automotive and aerospace + transportation. But it all boils back to the original input, being the underlying metal (spot price of aluminum). Companies hedge along the futures curve in these markets, but their offtakes all stem back to what the market is doing, which is influenced by many variables, not in the least supply + demand.

This makes cash flows cyclical and less predictable, ultimately broadening the range of possible distributions when it comes to valuation. There is money to be made in this substrata of the market, but it does not align with our core investment tenets, that call for robust economics, low capital intensity to support a competitive position, and predictability + defensibility in future cash flows.

At 6.15x forward EBITDA of €720mm (which converts to USD $761mm at the time of writing), implies a value of $4.68Bn in EV for the company as I write, marginal upside given the risk involved, and value gap of 5.6%. This supports a hold in my view. I would note, the quant system agrees with this notion, also rating the company a hold based on a composite of objective factors.

Figure 9.

{kind=link}

In short, CSTM's selloff looks set to continue, and there is little evidence to corroborate a reversal any time soon. Its fundamentals are sound, but sensitive to exogenous factors that suit a certain type of investor willing to position along the aluminum value chain. Net-net, rate hold.

For further details see:

Constellium: Sensitivity To Exogenous Factors Capping Upside Potential, Rate Hold