CSTM - Constellium: Strong Q2 2023 Results Support Long-Term Investment Thesis

2023-08-02 20:30:38 ET

Summary

- Constellium's stock has appreciated 50% year-to-date and 30% in the past 12 months.

- Q2-23 results show strong performance in value-added revenue and the aerospace & transportation segment.

- The acquisition of Arconic by Apollo Funds provides a compelling comparable valuation for Constellium, supporting a 12-month price target of $25.

- Strong free-cash-flow generation should lead to further deleveraging of the balance sheet and thereby support re-rating shares higher.

Introduction

We analyzed Constellium ( CSTM ) on this platform during late 2021 in a deep dive article that was named Top Idea. While shares are only up 5% since that article was published, in large part due to the unforeseen deteriorating macroeconomic environment with hyperinflation. However, year-to-date, the stock is up more than 50%, and during the past 12 months the stock has appreciated 30%. Our original article can be found at this link:

Constellium: An Overlooked Automotive Transformation Vehicle

The primary purpose of this company update article is to re-examine our investment thesis based on two factors: (1) recently announced Q2-23 results and updated full-year 2023 outlook; and (2) the recently announced acquisition of Arconic ( ARNC ) by Apollo Funds.

Company Overview

Constellium is a global industrials company that manufactures innovative, value-added aluminum products for various markets and applications, including packaging, automotive, and aerospace.

Stock Chart

Q2-23 Results

Summary

In the context of the overall challenging macroeconomic environment, Q2-23 results appear relatively strong. Despite shipments down 6% to 398k metric tons and revenue dropping 14% to 1.95 billion (Euro), adjusted EBITDA grew 5% to 209 million (Euro). In our view, one of the most important performance metrics for CSTM is value-added revenue, since this is revenue from high-margin, specialized aluminum products. During Q2, value-added revenue increased 11% to 785 million (Euro) and was primarily responsible for the adjusted EBITDA per metric ton growing 12% to 525 (Euro).

Segment Highlights

Constellium operates in three segments: Packaging & Automotive Rolled Products; Aerospace & Transportation; and Automotive Structures & Industry.

Aerospace & Transportation is clearly the best performing segment and mitigating weakness in the others. Despite flat shipments of 60k metric tons and revenue up 1% to 464 million (Euro), adjusted EBITDA and adjusted EBITDA per metric ton both grew by 53% to 96 million (Euro) and 1,613 million (Euro), respectively. The mix shift skewed towards aerospace over transportation, industry, and defense, driving those results.

For the Packaging & Automotive Rolled Products segment, adjusted EBITDA dropped 17% to 79 million (Euro), primarily due to lower shipments, higher operating costs, and execution issues at the Muscle Shoals facility. Strength in shipments for automotive rolled products was more than offset by weakness in packaging and specialty rolled products. We suggest that better execution / operating efficiencies at Muscle Shoals will be a tailwind over the next 12 to 18 months.

Performance was similar for the Automotive Structures & Industry segment. Adjusted EBITDA declined 12% to 443 million (Euro), primarily due to lower shipments and higher operating costs. Shipments of automotive extruded parts demonstrated growth, however that was more than offset by weakness in shipments to other end markets.

In our view, strength in the automotive end market is somewhat obstructed by Constellium's segment structure, whereby automotive is split into two reporting segments. Moreover, management acknowledged in its Q2-23 earnings presentation that production of light vehicles remains well below pre-pandemic levels. The issue appears to be supply-chain driven at the automotive OEM level, since dealer inventories remain low and consumer demand for luxury cars, light trucks, and sport utility vehicles remain strong. Therefore, our conclusion is that CSTM is performing well especially for this end market, given macro-industry dynamics. Moreover, the investment thesis remains intact for CSTM to benefit increasingly from longer-term secular trends in automotive of light weighting and electrification.

As further evidence of the potential for the automotive end-market, we note news on August 1st, 2023 that Ford restarted production of the F-150 Lightning with annualized capacity reaching 150,000 vehicles (triple prior capacity) by the end of September. Recent price cuts have increased demand by 6 times for this vehicle. Constellium previously disclosed that its supplies Ford ( F ) with aluminum structural components for the F-150 Lightning.

Balance Sheet & Free Cash Flow

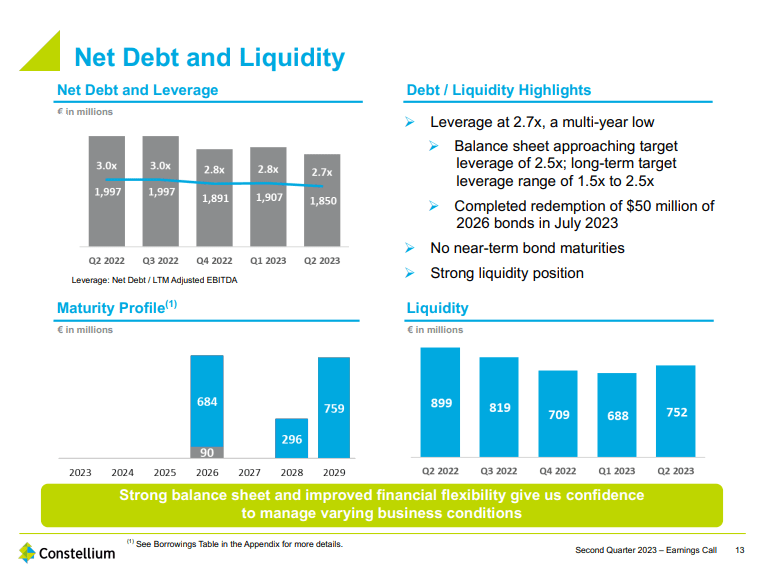

Constellium maintains a strong balance sheet with ample liquidity, no near-term debt maturities, and gradual de-leveraging. Net debt to trailing twelve month EBITDA was 2.7x at the end of Q2-23, significantly lower than the 3.6x at the end of Q3-21 (the time of our original article).

Constellium Net Debt & Liquidity (Constellium Investor Presentation)

{kind=link}

Part of our investment thesis continues to be that CSTM generates strong free cash flow. While the 1H:23 was hurt by higher capital expenditures with only 34 million (Euro) compared to 86 million (Euro) last year, management has guided full-year 2023 free cash flow to be more than 150 million (Euro).

EBITDA Model

In our initial article, we projected adjusted EBITDA of 648 million (Euro) and 730 million (Euro) in 2022 and 2023, respectively. Constellium reported 673 million (Euro) for 2022 and is currently guiding to between 700 million and 720 million (Euro) for 2023. We currently estimate 710 million (Euro) for 2023 and 760 million (Euro) for 2024, based on mid-single digit growth.

Valuation

In our view, the recent announcement that Arconic will be acquired by Apollo Funds provides a compelling comparable valuation for Constellium, since this marks a private-equity price and reduces the short-term noise of the stock market. In other words, we suggest that private-equity valuations are more indicative of true long-term value. The acquisition price values ARNC with a $5.2 billion enterprise value, equating to 7x forward EV/adjusted EBITDA based on the consensus estimate.

When determining the appropriate valuation multiple for Constellium, we think investors need to understand the dynamics of the aluminum supply chain. Specifically, since CSTM produces end-market aluminum products, with a focus on higher-margin (value-added) specialty products, Constellium should be considered a downstream company, compared to Alcoa ( AA ) which is an upstream player and processes unrefined aluminum. Downstream players, such as CSTM, are also less sensitive to changes in aluminum prices since they pass-through higher prices to their customers.

The comparable group in the downstream segment is Arconic and Kaiser Aluminum ( KALU ). Of these two, ARNC is a closer peer to CSTM, given global footprints and automotive end market focuses. KALU currently trades at 11x, which we think is aggressive given the macroeconomic environment and the fair buyout multiple for ARNC.

Based on our calculation, CSTM currently trades at 6x based on 2023 adjusted EBITDA estimate. We believe CSTM should be valued at 7x, in-line with Arconic. Therefore, our 12-month price target is $25, representing approximately 35% upside. In our view, reasonable downside risk is to the mid-teens, or $15.

Catalysts

We think the key near-term catalysts are: another raise to 2023 full-year guidance in its Q3-23 earnings report, further balance sheet deleveraging from better-than-anticipated free cash flow generation or another non-core asset sale, quicker than expected easing of inflation (globally), and improved conditions for the packaging end market.

Risks

We suggest that the key risks are: persistently high inflation or other macroeconomic deterioration, which would pressure operating expenses; the loss of Jean-Marc Germain as CEO, since he has been a transformational leader for Constellium for the past several years; weakening trends in the automotive sector, including decline in demand for vehicle light weighting or electrification; and supply-chain disruptions.

Conclusion

In our view, Constellium is an exceptionally well-managed industrial / specialty metals company. As a result, we believe CSTM is a solid investment for exposure to this sector, given its above-average growth, balance sheet deleveraging, and attractive valuation. While the stock isn't a value stock trading at 6x forward EV/adjusted EBITDA, we think there is an opportunity for the stock to be re-rated higher. Due to its current 2.7 leverage ratio (net debt / trailing 12-month EBITDA), each 1x valuation multiple represents significant upside for CSTM. Nonetheless, we acknowledge that global macroeconomic challenges may limit upside in the near-term.

For further details see:

Constellium: Strong Q2 2023 Results Support Long-Term Investment Thesis