WISH - ContextLogic: Not Even Liquidation Can Save This Stock

2023-09-26 17:13:18 ET

Summary

- An activist investor put out a letter to the board of WISH urging them to cease operations and return the cash to shareholders.

- We find that the net cash per share is lower than what the activist says and we believe it is not worth taking the risk.

- Liquidation news or a short squeeze can make the stock jump in the short-term. However, be aware of the risk associated with this trade.

Investment Thesis

ContextLogic ( WISH ) is a global mobile ecommerce company that operates the Wish platform, which connects buyers and sellers around the world. On September 25th, Cannell Capital LLC made public a letter sent by their managing member to Jun "Joe" Yan, WISH CEO, urging him and the board to cease operations and return the company's cash to shareholders. Cannell argued that WISH trades at a negative enterprise value of $(430) million today, which amounts to $22.33 dollars per share vs the current stock price of $4.25.

After digging deeper into the balance sheet, we discovered that the net cash per share is significantly lower than Cannell's claim. Our estimate suggests that the net cash at the end of Q3 is approximately $10 per share. Although we believe the company is ultimately headed for bankruptcy, a liquidation event may occur beforehand. However, we don't see this very likely and we estimate that in such a scenario, the cash per share that investors would receive would be much lower than the current value. Given the significant amount of risk associated with this stock, we strongly recommend staying as far away from it as possible.

Business

The WISH platform is known as a third-party 'dropshipping' platform for Chinese vendors who offer low-cost (albeit low-quality) products and often slow delivery times that can stretch to a week or more. We personally never use it, but we've seen ads about it, and they don't transmit any confidence or desire to use it. Wish makes money via sales fees, logistics services offered to merchants, and by selling ads (called ProductBoost) on its platform.

Since its IPO in late 2020, WISH has seen dismal performance. In the period from February 1, 2021, to the present day, the company's market value has plummeted by $18.2 billion to just $100 million today. Over the past ten quarters, it has consumed $1.6 billion in cash flow from operations, and insiders have unloaded approximately $234 million in shares. This situation is unsustainable and represents a significant example of wealth erosion and a breach of fiduciary duty to shareholders.

Year to date, revenues decreased 46% from $323 million a year ago to $174 million, while the net loss widened from $150 million to $169 million. The company is just burning cash to operate, and they have no realistic plan to turn things around in the short-term. For Q3 2023, they guided for revenue to be down ~50% YoY, and they will probably burn through another $80 million in the quarter. The situation is unsustainable in my view, which is why bankruptcy is highly likely. But before that, we also have to consider a liquidation event. In such scenario, how much would the stock be worth?

Balance Sheet

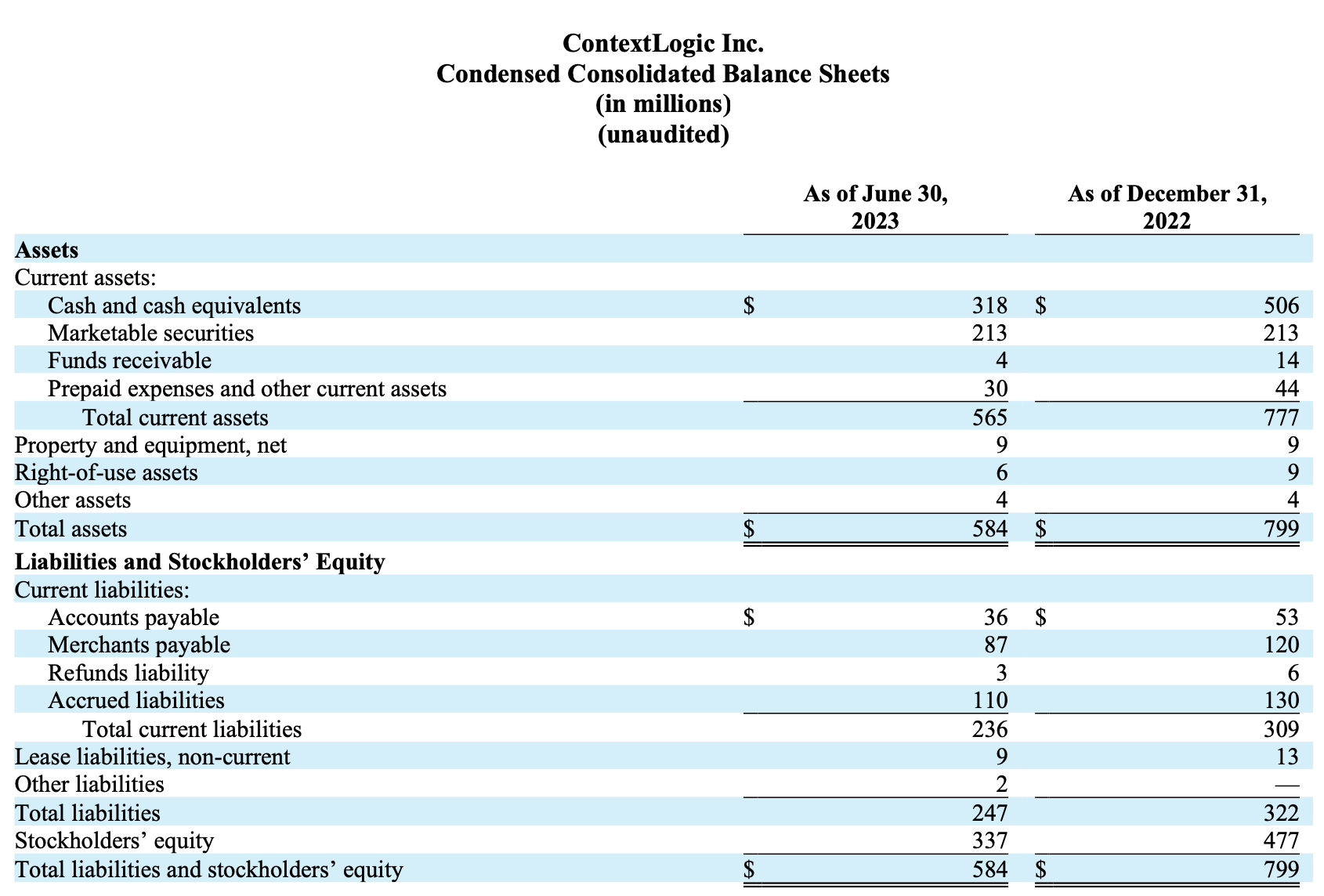

WISH balance sheet is rather simple to read and understand. Here is how it looked like as of June 30, 2023 :

{kind=link}

WISH Balance Sheet

WISH had a total of $584 million in assets at the end of Q2 2023, of which $531 million were cash, cash equivalents and marketable securities, compared to $719 million six months ago (a decrease of 33%). In other words, 90.9% of the assets are highly liquid.

However, we are almost at the end of Q3, and I bet the cash numbers look very different now. For starters, WISH has burned $90 million per quarter this year, so if this trend continued into Q3, cash and equivalents should be around $230 million. Moreover, the marketable securities mainly consist of short and long-term treasuries, and given that yields have been rising during the quarter, this number can be easily down at least 5% to $200 million. I estimate that cash and cash equivalents at the end of September sit close to $430 million, which is $100 million less than the last quarter.

On the other side, total liabilities amounted to $247 million. The biggest liabilities the company had were accrued expenses and merchandise payables. The company does not have any financial debt. I don't expect total liabilities to increase or decrease much quarter to quarter.

Overall, we estimate that net cash now is $225-$200 million, which means that WISH trades at a negative EV of $(100)-$(125) , not $(430) million. This translates into $9.93 net cash per share vs the $22.33 Cannell estimate . In Cannell's calculations, they didn't subtract any liabilities from the cash position. However, in the event of liquidation, they will have to pay them, so we deducted them. Nonetheless, one thing is certain: the cash amount is significantly lower than a quarter ago.

Short-Term Opportunity?

After reviewing the balance sheet, the opportunity of a liquidation may not seem very compelling, but there are still some catalysts that can propel the stock higher in the short term.

The first one is if management takes action right now and actually decides to liquidate the company. Every day it passes the company keeps burning cash. Time is not in the shareholders favor right now. But although it is unclear how much cash the company would be left with, the news should make the stock rise in the short term.

In the letter by Cannell, the investment firm said that they would wait until September 27 to hear back from management. If not, they would initiate legal actions against the board and management.

If a liquidation were to be announced, the rally could be exacerbated by short investors covering their positions. Right now, WISH has a short float of 14.4% according to Seeking Alpha and 15.2% according to Finviz . We have seen what could happen in this cases in the past.

But how probable is this to happen? In my view, it's not very likely. Consider this: What's in it for the management? Since they have minimal ownership, all they have been doing over the past year is exercising options and selling them immediately. What's stopping them from continuing to do so until bankruptcy? The board has proven to be negligent all along, and we don't see why this would change now.

However, it is important to consider the many risks this trade faces. In the not-so-distant future, I believe this company is going to go bankrupt and the equity will be worth $0 , so the trade is highly speculative. Moreover, shareholders will continue to face dilution over the coming months and the company will continue to bleed cash at high levels.

Ultimately, I recommend staying as far away from this stock as possible unless you think a short squeeze or liquidation news is around the corner, which could cause the stock to rise in the short-term. I don't think a liquidation will happen and if I were forced to make a prediction, I would say that a year from now, WISH will no longer exist.

For further details see:

ContextLogic: Not Even Liquidation Can Save This Stock