WISH - ContextLogic Reduces Losses Amid Intense Competition (Rating Downgrade)

2023-12-12 15:39:52 ET

Summary

- ContextLogic Inc. reported Q3 2023 financial results, beating revenue but missing earnings estimates.

- The company faces intense competition and has initiated a process to pursue strategic options, including a sale of the company.

- Despite reduced losses, my outlook on ContextLogic is to Sell due to its revenue decline and poor performance.

A Quick Take On ContextLogic

ContextLogic Inc. ( WISH ) reported its Q3 2023 financial results on November 7, 2023, beating revenue but missing consensus earnings estimates.

The firm has created a mobile-centric ecommerce platform for consumers and merchants primarily in China, North America and Europe.

I previously wrote about WISH with a Hold outlook in early 2022 on the firm’s efforts to turn the company's poor performance around.

While the firm has implemented significant cost reductions, it faces extreme competition from market players spending to gain users, and the Board has initiated a process to pursue strategic options, including a sale of the company.

Despite its reduced losses and given its revenue decline, my outlook on WISH is to Sell.

ContextLogic Overview And Market

California-based ContextLogic enables merchants to effectively engage with prospective customers via the firm's mobile ecommerce platform.

Management is headed by CEO Joe Yan, who has been with the firm since September 2022 and is an operating partner at venture capital firm GGV Capital.

The company’s primary offerings include:

-

Sell on Wish

-

Wish Local

-

Wish App.

According to a 2023 market research report by Tenba Group, the Chinese e-commerce market is expected to reach a value of $2 trillion by the end of 2025.

If achieved, that would be the result of an average growth rate of around 6% in recent years.

The report estimates growth in e-commerce in China through 2025 as a result of the pandemic and a shift in consumer behavior toward more online purchasing.

Also, social commerce is expected to grow substantially due to the wide penetration of smartphones and user interactions with each other to achieve cost savings.

The company is also active in major global markets in North America and Europe.

Major competitive or other industry participants include:

- Amazon

- Alibaba

- JD.com

- Xiaohongshu [Red]

- Walmart

- Target

- Others.

ContextLogic’s Recent Financial Trends

Total revenue by quarter (blue columns) has continued to shrink rapidly due to lowered advertising spending; Operating income by quarter (red line) has remained heavily negative because of the need to retain headcount to improve its app and continue building partnerships.

Seeking Alpha

Gross profit margin by quarter (green line) has risen in the most recent quarter as a result of higher commission rates, additional cost savings and higher logistics margin; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have been high and volatile due to a lower employee headcount:

Seeking Alpha

Earnings per share (Diluted) have remained heavily negative, although they have come off their worst lows of the past few years:

Seeking Alpha

(All data in the above charts is GAAP.)

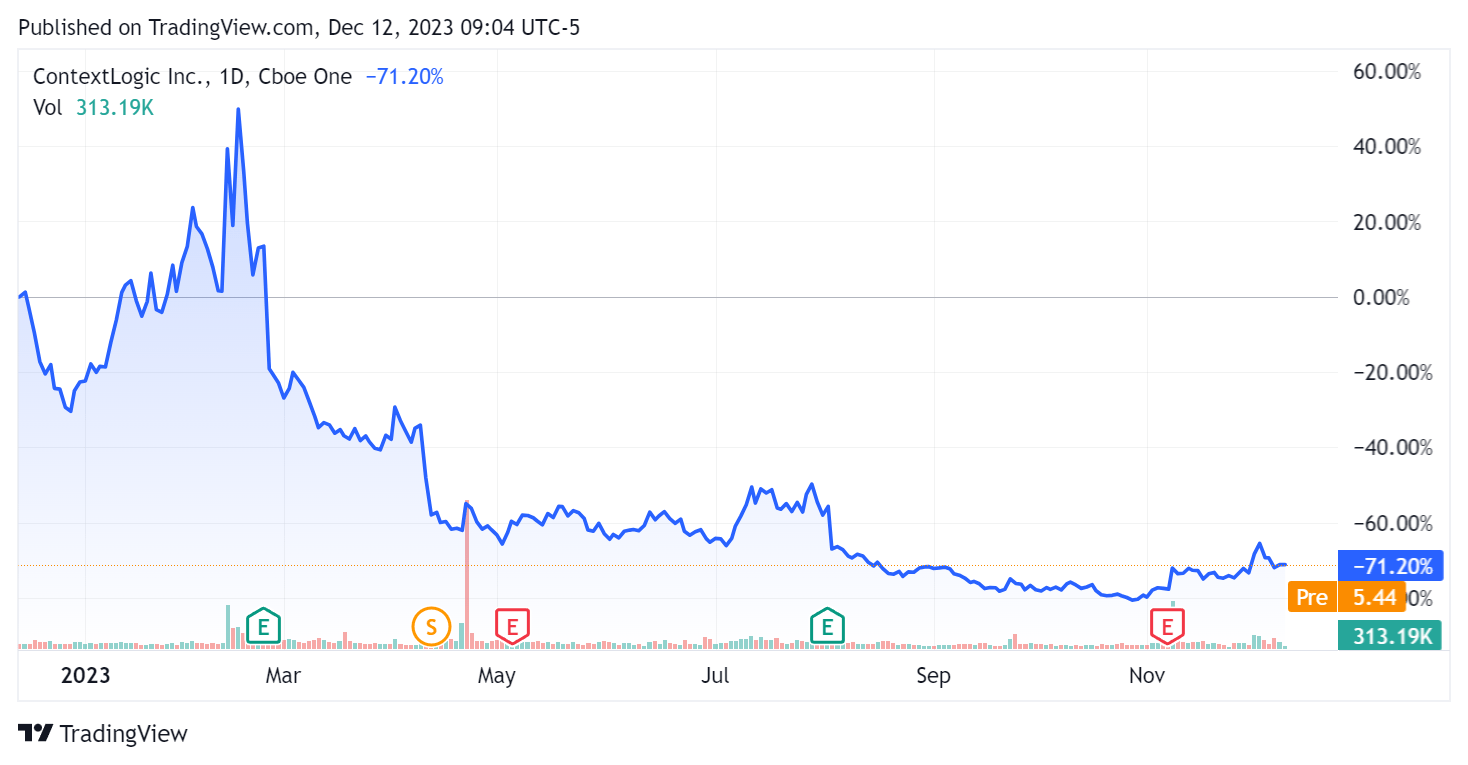

In the past 12 months, WISH’s stock price has fallen 71.2%:

{kind=link}

For balance sheet results, the firm ended the quarter with $445.0 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash used was a whopping $378.0 million, during which capital expenditures were $3.0 million. The company paid $78.0 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For ContextLogic

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| NM |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 0.4 |

| Revenue Growth Rate |

| -51.6% |

| Net Income Margin |

| -100.6% |

| EBITDA % |

| -93.0% |

| Market Capitalization |

| $130,850,000 |

| Enterprise Value |

| -$300,150,000 |

| Operating Cash Flow |

| -$375,000,000 |

| Earnings Per Share (Fully Diluted) |

| -$15.36 |

| Forward EPS Estimate |

| -$10.37 |

| Free Cash Flow Per Share |

| -$16.14 |

| SA Quant Score |

| Strong Sell - 1.33 |

(Source - Seeking Alpha.)

WISH’s most recent unadjusted Rule of 40 calculation was negative (169.9%) as of Q3 2023’s results, so the firm has performed very poorly in this regard, per the table below:

| Rule of 40 Performance (Unadjusted) |

| Q3 2023 |

| Revenue Growth % |

| -51.6% |

| Operating Margin |

| -118.3% |

| Total |

| -169.9% |

(Source - Seeking Alpha.)

Commentary On ContextLogic

In its last earnings call (Source - Seeking Alpha ), covering Q3 2023’s results, management’s prepared remarks highlighted the Board’s decision to start an exploration of strategic options, hiring JPMorgan to likely seek a buyer for the firm’s assets.

Revenue dropped due to lower advertising spending even as the company gained a number of partnerships designed to help improve its delivery convenience and expand its activity in Europe.

Management’s workforce reduction was completed by the end of the quarter and the firm expects to achieve annual savings of $44.5 million at the midpoint.

I prepared a chart showing the frequency of various keywords and terms used by management and analysts on the conference call:

Seeking Alpha

The chart illustrates a number of negative terms, most notably the "macro" challenges and headwinds it has been facing.

Analysts questioned the leadership about competitive pressures and the macroeconomic environment leading into the Q4 holiday season.

Management replied that the company faces intense competition as market participants offer deep discounts to gain new users, so the company is focused on sustainable growth and increasing average transaction value.

Leadership did not characterize the first month of the Q4 holiday season other than to say that for its "Every Day is Black Friday" campaign, the "momentum is pretty strong."

For the quarter’s results, total revenue dropped 52% year-over-year and gross profit margin fell by 2.2%.

Selling and G&A expenses as a percentage of revenue dropped by 7.7% YoY, while operating losses were reduced by 44.5% but remained extremely high at $71.0 million for the quarter.

The company's financial position is not good, with plenty of cash, no debt, but heavy use of cash in the past twelve months. The company has reduced its headcount to lower its use of cash.

WISH’s Rule of 40 performance has been very poor, indicating a combination of sharply dropping revenue and high operating losses.

Looking ahead, the 2023 full-year revenue decline is expected to be 49.3% versus 2022.

A potential upside catalyst to the stock could include a better-than-expect holiday season or a buyout offer.

However, I’m not optimistic on either count as the firm continues to face extreme competition for users.

My outlook on ContextLogic Inc. stock is to Sell.

For further details see:

ContextLogic Reduces Losses Amid Intense Competition (Rating Downgrade)