CTTAF - Continental Aktiengesellschaft: Staying On The Cautious Side

2023-03-09 03:24:47 ET

Summary

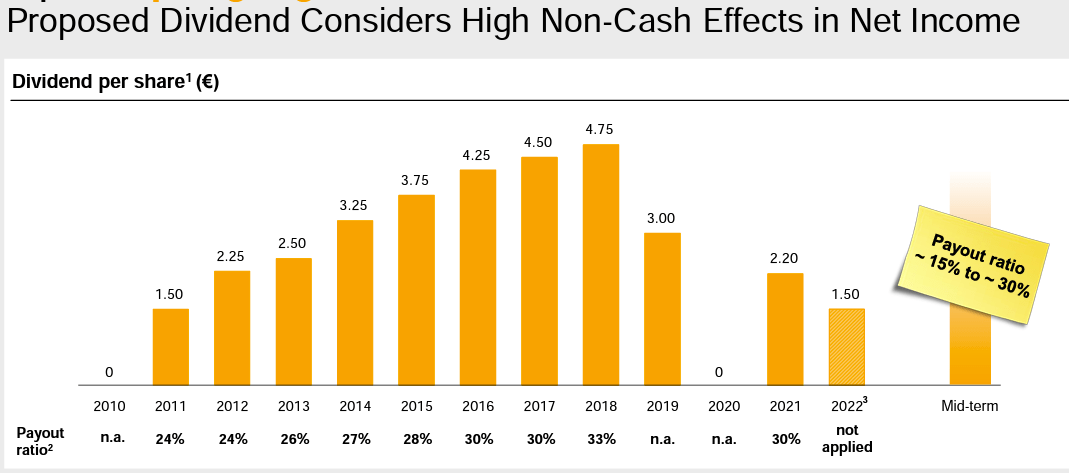

- DPS was further cut. The CEO is proposing a €1.5 per share.

- Versus management expectations, we are forecasting a lower margin in the 2023 second half. Q4 numbers were a positive confirmation. Still too many uncertainties for 2023.

- On a reverse P/E basis, we believe that Continental is fairly priced. Equal Weight reiterated.

After having analyzed Compagnie Générale des Établissements Michelin Q4 results , today Continental Aktiengesellschaft ( OTCPK:CTTAF , CTTAY ) released its Fiscal Year 2022 update. Last time, we were right to be cautious on Conti and the latest numbers just proved our concerns. In our previous publication, we analyzed how the Automotive segment was suffering and the company's CEO was proud to not increase its segment losses, while almost all OEM competitors were back to profitable growth. Regarding the tire division, here at the Lab, we anticipated that Conti's pricing power was not sufficient to cover raw material inflationary pressure and in our assessment, we are forecasting a lower margin in the 2023 second half. This is exactly what happened.

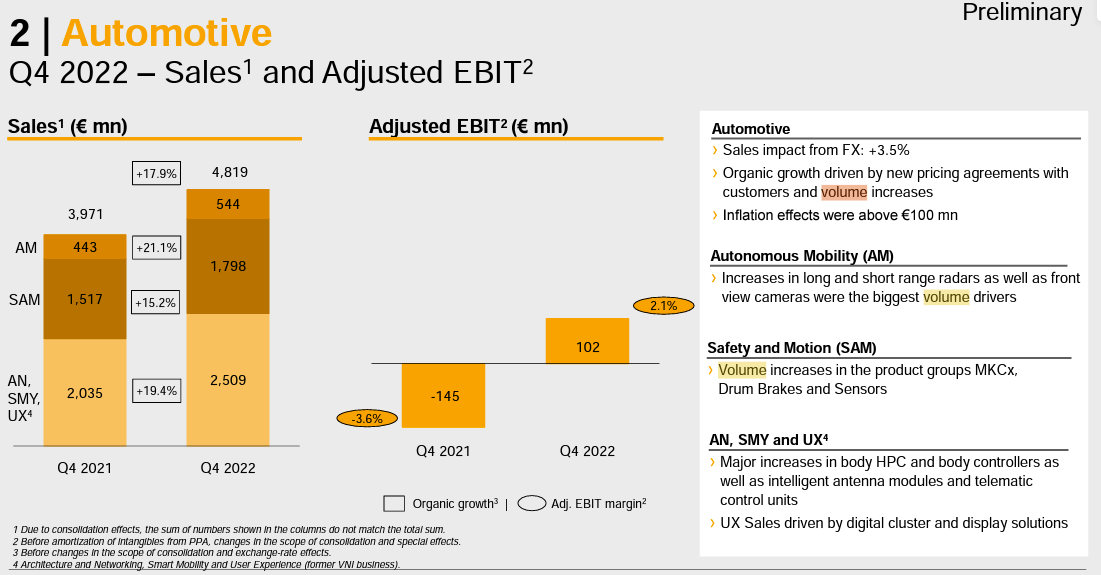

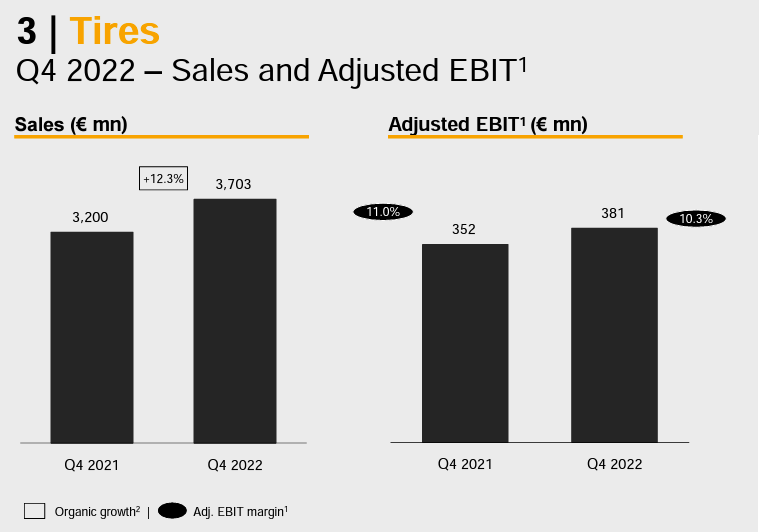

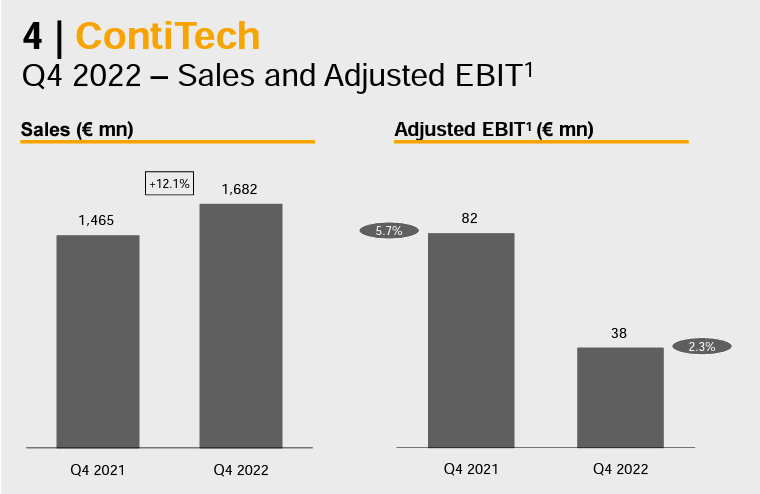

- Top-line sales increased to €39.4 billion, signing a plus of 16.7% compared to the previous year; however, adj. core operating profit decreased to 5% from 5.5% recorded in 2023. In Q4, looking at the divisional highlights, the tires adjusted EBIT decreased from 11% to 10.3% (Fig 2). The same negative performance was recorded in the ContiTech segment which moved from 5.7% to 2.3% (Fig 3), while the Automotive division was finally back in positive territory, but reached an. adj core operating profit of only 2.1% (Fig 1);

-

Going down to the P&L, the company was impacted by negative one-offs for more than €1 billion. Aside from the Russian asset impairment (for a total value of approximately €87 million), the company was negatively impacted by the Automotive division write-off for a total consideration of €880 million (Fig 4). Another negative aspect to report is the higher interest rate expenses that during the year increased by 30% from €180.4 million to €234.8 million (Fig 5). In the past fiscal year, as expected, Continental's financial indebtedness increased to almost €4.5 billion;

- Consequently, the company's net profit stood at €67 million compared to the €1.4 billion recorded in 2021. However, what is more important to emphasize is the negative FCF evolution, in detail, adj. FCF reached €200 million from €1.2 billion in 2021 and was lower for inventories buildup and higher CAPEX requirements. In the half-year analyst call, the CEO was expecting a positive flow and an improvement in cash generation, and was not in line with expectations;

- If approved, management will distribute a dividend of €1.50 per share. This contrast with Conti's historical payout ratio and its cash flow generation. According to our calculation, this implied a dividend cash out of €300 million for this year. While Michelin confirmed and increased its DPS by 11%, the Continental dividend is constantly decreasing year-on-year (Fig 6). Therefore, our conviction on Continental was our least preferred player, and Michelin our sector's top pick, once again, proved to be right.

{kind=link}

(Fig 1)

{kind=link}

(Fig 2)

{kind=link}

(Fig 3)

{kind=link}

(Fig 4)

{kind=link}

(Fig 5)

{kind=link}

(Fig 6)

Conclusion and Valuation

Looking ahead to the Q4 performance, we are more positive. On a Free Cash Flow basis, the company has the ability to pay its DPS (€300 million) without compromising its balance sheet. We are estimating a higher cost of €1.5 billion for wage inflation and materials prices; but in the mind time, Continental is now implementing further price increases to sustain a positive pricing delta and offset additional cost inflation. On an annual basis, we are forecasting an Automotive EBIT margin in line with Q4 results (in the 2/3% area), while ContiTech and Tires divisions are expected to increase their margin contribution. However, we are still far from the company's expectation to achieve a group operating core margin in the double-digit area. As already mentioned in our previous publication, Conti has a solid order intake (in the Auto segment reached €23.4 billion), while in the tires division, in 2023, we expect global production up by 3% for light commercial vehicles and cars. Despite that, here at the Lab, we still prefer Michelin and we continue to value Conti with a neutral rating. We expect another year of high levels of uncertainties when it comes to volume recovery and inflationary pressures and on a reverse P/E basis, valuing the German player with a ratio of 7x (based on its historical average), we should imply €11 in earnings per share. We are far from this and we believe that Conti's shares are fairly valued at this price. Our neutral rating is then confirmed.

For further details see:

Continental Aktiengesellschaft: Staying On The Cautious Side