MATX - Continuing To Avoid Matson Inc.

Summary

- Matson has just released financials, so I thought I'd review the name yet again. I'm very impressed with how things have gone, though note that growth is slowing.

- The problem for me is that in a world where it's possible to earn a 5% guaranteed return on Treasuries, stock valuations have to be compelling. This one is not.

- We're not trying to earn "returns." We're trying to earn "risk-adjusted returns", and potential risk-adjusted returns aren't high enough in my view.

I'm not going to lie to you. Of my many negative qualities, vindictiveness is in the top 30. It's in that frame of mind that I write about Matson Inc. ( MATX ). I've been cautious about this name for a while, and have been pilloried by readers in the comments section for my views. For that reason, I am very pleased to announce that since I wrote my " avoid " piece on this name about 13 months ago, and since then, the shares have returned a negative 26% against a loss of 8.5% for the S&P 500. Since the company has just released earnings, I thought I'd review the name again. I try to be open minded, so I'm willing to reconsider the investment merits here. I'll work out whether or not it makes sense to buy the stock at current prices, because an investment at $65.40 is less risky than an investment priced at $90. I'll review these recently released financial statements, and will look at the valuation of the stock itself to make that determination. Finally, I think the vituperative reaction of the readers in this case relates to a common human problem assuming that "price" and "value" are the same thing, and that because a price is rising, a bullish position is vindicated. I think this misunderstanding is why the idea of "buying low and selling high" is simple to understand, and very challenging to execute.

Welcome to the "thesis statement" portion of the article. This is designed for those people who want a little bit more than what they would get from a title and a few bullet points, but want much less Doyle mojo than they would get from a full length article. I'm of the view that this is a great business in many ways. The capital structure has improved nicely, revenue and net income are up strongly, and the dividend is very secure. The problem is that not even the best business is worth any price. The price we pay matters a great deal, because we're not seeking "returns." We're seeking "risk adjusted returns", and I think the risk here is still too great. Finally, in the relativistic world of investing, we're always on the hunt for the best risk adjusted alternative for our capital. When an investor can earn over 5% guaranteed by Uncle Sam, my hurdle rate for stocks in general is somewhat high. For that reason, I'm going to continue to avoid this name.

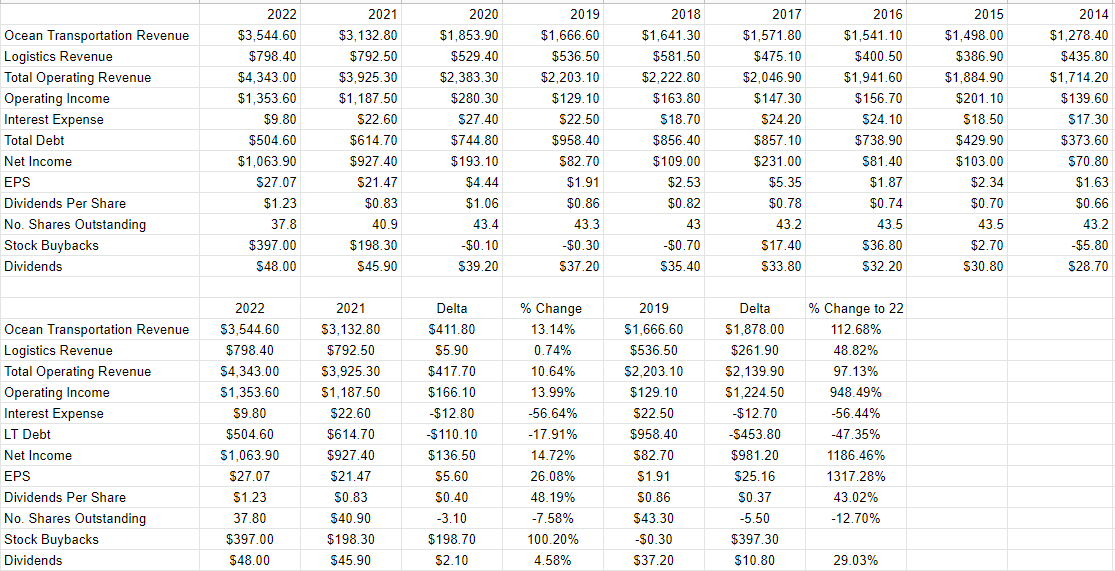

Financial Snapshot

The financial results have been quite good in my estimation. For example, relative to 2021, revenue and net income are up by 10.6%, and 14.7% relative to last year. These results were also quite good relative to the pre-pandemic era also, with revenue and net income higher by 112% and 1186% respectively. The company has rewarded shareholders with this performance by increasing the dividend aggressively, up about 48% relative to the same period in 2021.

At the same time, the capital structure has improved massively over the past year. Long term debt is down about 17.9% relative to the same period a year ago. As expected, interest expense is down about 56.64% relative to 2021. I also like the timing of debt cash flows, because a company rolling debt this year would be troublesome, given the current interest rate. I think indebtedness here is actually not a significant problem, per the following plucked from page 59 of the latest 10-K for your enjoyment and edification.

Matson's Debt Maturities (Matson latest 10-K pp. 59)

To put the $60 million, followed by a series of $51.7 million maturities into context, over the past three years, the company has generated an average of $554 million in cash from operations. Given all of the above, I'm reasonably confident that the future dividend payment of ~$45-$50 million is reasonably secure, and for that reason I'd be happy to buy this stock at the right price.

{kind=link}

The Stock

If you subject yourself to my stuff on a regular basis, you know that I consider the stock and the business to be distinct from each other. The business provides ocean transportation services to the domestic non-contiguous regions of Alaska, Guam, and Hawaii. The stock is a speculative instrument that gets buffeted by a host of factors, some of which have nothing to do with transporting dry containers or refrigerated commodities. One of the things that affects the performance of a given stock, for example, is the crowd's ever-changing views about the desirability of "stocks" as an asset class. I really hate to remind you about the 26% drop in the value of these shares over the past 13 months, but a compelling argument could be made to suggest that some of that loss was driven by the fall in the S&P 500. After all, if investors eschew "stocks" in general, it's quite challenging for a given equity to perform well. Additionally, people may decide to eschew the shares because they can get better risk adjusted returns elsewhere .

So, this is why I consider the stock as a thing distinct from the business. The former is often a poor proxy for what's going on at the company, and I think it's possible to profitably exploit this disconnect. In my view, the only way to successfully trade stocks is to spot the discrepancies between what the crowd is assuming about a given company and subsequent results. What I want to see in this regard is a stock that the crowd is somewhat pessimistic about that goes on to exceed expectations. When the crowd is pessimistic, the shares are cheap, which is why I try to buy only cheap stocks. So today the work involves deciding whether or not the shares are reasonably priced.

I work out whether or not the shares are cheap in a few ways, ranging from the simple to the more complex. On the simple side, I look at the ratio of price to some measure of economic value, and I want to see the stock trading at a discount to both the overall market and to its own history. When last I reviewed this name, the shares were trading at a price to sales ratio of 1.164, which was up fairly massively from the period 2014-2020. Now that the shares have cratered in price, they are about 54% cheaper on that basis, per the following:

At the same time, as we see in the chart below, there's no getting around the fact that the dividend yield is currently about 315 basis points lower than the 1 Year Treasury Bill .

In addition to looking at ratios, I want to see what the market is currently "thinking" about a given name. If you read my articles regularly, you know that I rely on the work of Professor Stephen Penman and his book "Accounting for Value" for this. In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is "thinking" about a given company's future growth. This involves isolating the "g" (growth) variable in this formula. In case you find Penman's writing a bit too thick, you might want to crack the spine on "Expectations Investing" by Mauboussin and Rappaport. These two have also introduced the idea of using the stock price itself as a source of information, and then infer what the market is currently "expecting" about the future. Applying this approach to Matson at the moment suggests the market is assuming that this company will grow at a rate of about 35% in perpetuity from current levels, which I consider to be a very optimistic forecast. I think the company is fine, and is profitable, but the shares are not cheap enough to get me excited, so I'm going to continue to avoid this name.

For further details see:

Continuing To Avoid Matson Inc.