FALN - Contrarian Idea For 2024: High-Yield Bonds With FALN

2023-12-14 09:34:29 ET

Summary

- High-yield bonds offer higher yields as compensation for higher risks associated with lower credit ratings.

- The U.S. economy is in a stage between late cycle and recession, but there are signs of recovery in the near future.

- Understanding how bonds perform in different stages of the business cycle is key to investing in bonds successfully.

- Although I consider myself a stock investor, strategically gaining exposure to high-yield bonds seems like a rational choice today.

As many of you know, I am primarily a stock investor. With an extensive investment time horizon spanning a few decades, I feel comfortable taking on the risks associated with stocks. I will, however, not shy away from investing in other asset classes strategically to exploit mispriced bets and lucrative opportunities.

This brings me to high-yield bonds, aka junk bonds.

Theoretically, high-yield bonds are fixed-income securities issued by companies with lower credit ratings than investment-grade bonds. They offer higher yields as compensation for the comparatively higher risks associated with these bonds. Before I present a case for investing in high-yield bonds today, let us briefly discuss some of the key characteristics of this asset class.

- Lower credit ratings: High-yield bonds are rated below investment grade (BBB or lower by rating agencies such as Moody's or Standard & Poor's). The credit ratings reflect the issuer's creditworthiness and the likelihood of timely repayment.

- Higher default risk: The main risk associated with high-yield bonds is the increased likelihood of the issuer defaulting on interest payments or failing to repay the principal amount at maturity. This risk is influenced by factors such as the financial health of the issuer, economic conditions, and industry trends.

- Market sensitivity: High-yield bonds are sensitive to changes in economic conditions and interest rates. Economic downturns or rising interest rates can increase the risk of defaults and impact the value of high-yield bond portfolios.

Investing in high-yield bonds is not for every investor. If you are a small-cap investor, some exposure to high-yield bonds does not sound unreasonable as you are already comfortable with bearing the risks associated with small companies. As a stock investor, I do not want to expose a major part of my portfolio to bonds. However, as I discuss in the remainder of this analysis, I am growing in confidence about the outlook for high-yield bonds in 2024, which has prompted me to consider investing in a high-yield bond fund today.

Understanding The Business Cycle Holds The Key

When I took my economics classes, my instructors taught me to think of the business cycle in four distinct stages. In this analysis, we will use the below terms to identify different stages of the business cycle.

- Early cycle

- Mid cycle

- Late cycle

- Downturn & recession

The early cycle is synonymous with the recovery phase of a business cycle where businesses feel confident about the economy after a recessionary period. According to Fidelity , the key characteristics of each stage in the business cycle are below.

| Business cycle stage |

| Characteristics |

| Early |

| A sharp recovery from recession, as economic indicators such as gross domestic product and industrial production move from negative to positive and growth accelerates. More credit and low interest rates aid profit growth. Business inventories are low, and sales grow significantly. |

| Mid |

| Typically the longest phase with moderate growth. Economic activity gathers momentum, credit growth is strong, and profitability is healthy as monetary policy turns increasingly neutral. |

| Late |

| Economic activity often reaches its peak, implying that growth remains positive but slowing. Rising inflation and a tight labor market may crimp profits and lead to higher interest rates. |

| Recession |

| Economic activity contracts, profits decline, and credit is scarce for businesses and consumers. Rates and business inventories gradually fall, setting the stage for recovery. |

The U.S. has so far avoided a recession, but I believe it would be naive to conclude that the country is still in the late stage of the business cycle either. I believe we are somewhere in between. The odds of a recession have fallen dramatically this year regardless of which metric you use. Economists, at the beginning of this year, pinned the probability of a recession within the next 12 months at a staggering 65%, which has declined to less than 40% today. The probability of a recession predicted by the U.S. Treasury spread has also fallen to 52% from a high of over 70% a few months ago.

Exhibit 1: The probability of a recession predicted by the U.S. Treasury spread

Federal Reserve

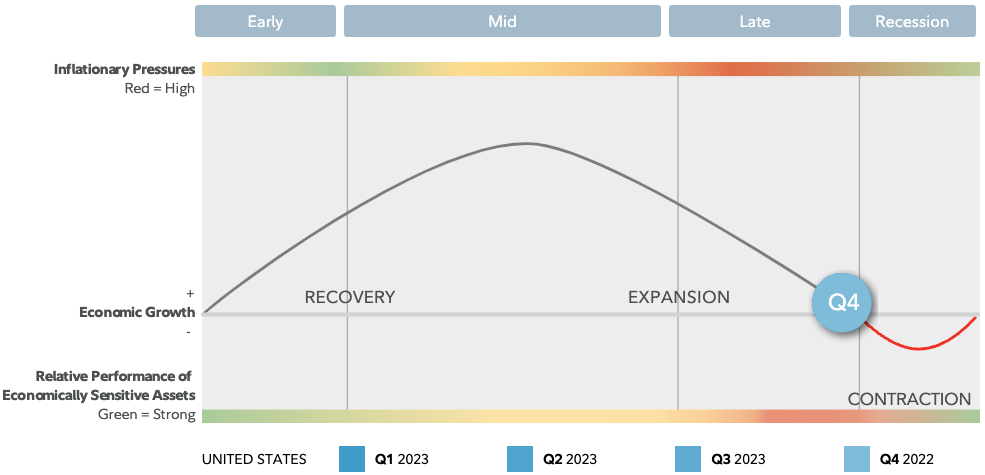

According to Fidelity, the U.S. economy is in the late cycle and is on the verge of entering recession territory.

Exhibit 2: The U.S. business cycle

{kind=link}

The U.S. may enter a recession in the coming months, which is a risk that I do not want to rule out. That said, I believe the economy is well-positioned to enter the recovery phase sooner rather than later, which is why I believe investors should make investment decisions based on this assumption to beat the market in the coming year.

As markets are forward-looking, I believe it makes sense to focus on the most likely direction of the U.S. economy in the year ahead, which, in my opinion, is toward recovery.

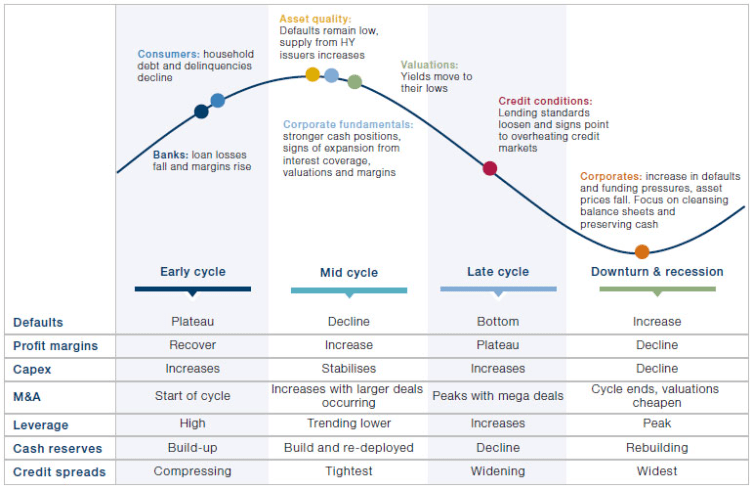

High-yield bonds have historically performed well during the early stage of the business cycle as corporate profit margins recover in this period, allowing companies to strengthen their balance sheets. Credit spreads usually start compressing at this stage while corporate cash reserves tend to move higher.

Exhibit 3: Corporate fundamentals across the business cycle

{kind=link}

Even in the expansionary mid-cycle phase, economic and credit conditions tend to improve aided by expansionary monetary policy decisions. This is good for high-yield bonds.

As we move closer to 2024, I believe we are getting closer to favorable monetary policy decisions and a further reduction in inflation. Even if the economy enters a recession in the first half of the year, I believe we will see notable improvements in the second half of the year, paving the way for high-yield bonds to outperform other asset classes including equities.

Another reason to invest in bonds - not just HY bonds but bonds in general - is the historical performance of bonds following a pause in rate hikes. As illustrated below, bonds have delivered stellar returns, on average, in the first 12 months following a Fed pause.

Exhibit 4: Bond returns following a peak in Fed hikes

Columbia Threadneedle

Bonds are bound to do well when interest rates fall. As an investor with an above-average risk tolerance, I am more attracted to high-yield bonds today. In the following segment, I will introduce you to a top-of-the-class ETF to gain exposure to HY bonds.

iShares Fallen Angels USD Bond ETF

Investing in high-yield bonds is not my normal cup of tea. I am a stock investor - not a bond investor - so rather than handpicking corporate bonds, I thought it made more sense to invest in a reliable ETF with a proven track record and one that came with a reasonable fee structure. After sifting through the market, I decided to invest in iShares Fallen Angels USD Bond ETF (FALN) for a few reasons.

- This fund seeks exposure to high-yield bonds that were previously rated investment grade, hence the term "fallen angels". I found this to be an attractive strategy to gain exposure to companies that have been doing well until recently. With economic conditions tipped to improve in the coming quarters, I thought this fund would give me exposure to a subset of bonds that are likely to be serviced efficiently.

- I am familiar with many of the issuers of bonds in which FALN has a notable concentration. The top 10 holdings of FALN include bonds issued by Vodafone Group (VOD), Newell Brands (NWL), Rolls-Royce (RYCEY), and Las Vegas Sands Corp. (LVS), all of which are companies I have been following for some time.

- The top 10 holdings of FALN account for just 15% of the total fund, which suggests the fund manages a well-diversified portfolio.

- The expense ratio of 0.25% pins FALN as one of the most reasonably priced high-yield bond funds in the market today.

- The NAV is up 10.7% YTD while the fund price has risen by 5.2%. With an improvement in credit conditions on the cards for 2024 along with the possibility of a rate cut, I believe the fund will see a meaningful increase in its market value in the foreseeable future.

- The current dividend yield of close to 5.4%, in my opinion, will prove to be above average toward the end of 2024 assuming rates will decline. This will create a strong platform for FALN prices to increase.

I added FALN to my portfolio last week after identifying its appeal.

Takeaway

Bonds are looking increasingly attractive at a time when rates are expected to decline. The U.S. economy is not out of the woods yet, but I expect a swift recovery even if it were to enter a recession in 2024. Going by the business cycle effect, I believe high-yield bonds have a lot to offer investors today, which is why I decided to gain some exposure to HY bonds through FALN.

For further details see:

Contrarian Idea For 2024: High-Yield Bonds With FALN