CPS - Cooper-Standard Holdings: An Impressive Turnaround Story That's Just Getting Started

2023-08-23 03:35:15 ET

Summary

- The recovery in auto production and the increasing prominence of EVs will present a substantial revenue opportunity for Cooper-Standard in the forthcoming years.

- Strategic cost-cutting measures, coupled with commercial agreements to recoup costs incurred during the recent years of economic downturn, have already and will continue to substantially enhance the company's bottom line.

- The confluence of recovering auto production, the rise of EVs, and new product launches, coupled with the comprehensive cost-cutting and recovery measures, renders CPS shares an enticing opportunity.

Editor's note: Seeking Alpha is proud to welcome Michael Wolman as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

Cooper-Standard Holdings (CPS) continues to achieve what I believe is a remarkable commercial turnaround. The company's cost-saving measures have had a positive impact on its adjusted EBITDA, amounting to approximately $479 million between 2019 and 2022. Furthermore, management has set an FY 2023 outlook of $162.5 million, marking a 330% increase over the $37.8 million in FY 2022. In my opinion, Cooper-Standard has reached an inflection point with its corporate restructuring, cost-saving strategies, enhanced commercial agreements, recovering global light vehicle production rates, and the emergence of new opportunities such as electric vehicles (EVs).

Thematics

After reaching a peak of around 97 million units in 2017, global motor vehicle production output experienced a sharp decline, plummeting to approximately 78 million units in 2020. In my view, this staggering drop of about 20% over the span of three years can largely be attributed to the global coronavirus pandemic that spanned 2019 and 2020. The pandemic led to a substantial decrease in auto demand, exacerbating an already challenging situation due to the subsequent deterioration of global economic conditions. This profound collapse in global production significantly impacted Cooper-Standard's financial performance, affecting both its top and bottom lines. The extent of Cooper's reliance on global production becomes evident when comparing the relevant figures.

CPS Filings, OICA.net 1999 to 2022

I believe that we are beginning to emerge from this period of production stagnation. The company's 2023 guidance points to approximately 86.7 million units on a global scale, based on current production schedules and forecasts. To me, this represents an encouraging initial stride as we transition into the upcoming years.

Furthermore, according to S&P Global Mobility , the average age of light vehicles in operation reached 12.2 years in the United States, marking an all-time high.

S&P Global Mobility

In my view, the significant average age of vehicles on the road will provide an additional boost to U.S. auto demand in the coming years.

I am cautiously optimistic about the prospect of this recovery trend persisting, potentially leading to Cooper's revenues regaining their levels from 2017 and 2018 within the coming years.

The Rise of EVs

Alongside the global production rebound, Cooper-Standard is poised to leverage opportunities in terms of revenue, total addressable market ((TAM)), and margin expansion through the increasing prominence of electric vehicles (EVs). A slide from Cooper's Q4 2022 earnings presentation underscores the significant potential of the EV market.

Cooper-Standard Q4 2022 Earnings Presentation Slides

In 2022, a remarkable 80% of net new business stemmed from EV awards, establishing Cooper as a current supplier for 3 of the top 5 and 9 of the top 15 EV nameplates. With a distinct advantage in design, manufacturing processes, and materials science, the company stands in a league of its own when it comes to crafting superior cooling and sealing systems that enhance the operational efficiencies of EVs. This segment of the business boasts higher margins than traditional internal combustion engine ((ICE)) vehicles, which I believe is a particularly advantageous position in an industry where sales and production are projected to achieve a 43% and 28% compound annual growth rate ((CAGR)) respectively through 2027.

Fortrex: Expanding Cooper's TAM

The company is continuing its efforts to introduce its Fortrex foam and rubber material products to both automotive and non-automotive customers. Now available for auto-sealing applications, Fortrex boasts lower material densities, approximately 26% weight reduction, and a reduced carbon footprint in its manufacturing process. During their Q2 2023 earnings presentation , management expressed excitement about their new optimized manufacturing process for Fortrex 2.0, which is scheduled for implementation in early 2024. With improved weight and density, it's evident why EV manufacturers are showing keen interest in this product.

As of the Q2 2023 call, the company has already recorded approximately $50 million in revenue from Fortrex sealing products used in the automotive industry. They anticipate the revenue potential for Fortrex sealing to reach around $150 million within the next few years. Additionally, the company has received requests from current customers to collaborate with tire manufacturers in developing a Fortrex-based product that would reduce friction and further enhance the efficiency of EVs.

Commercial Turnaround

In conjunction with the suppressed revenues resulting from the auto production slump, economic headwinds such as general and material price inflation and currency fluctuations significantly impacted Cooper's bottom line. Since then, Cooper has prioritized key strategic initiatives, including company-wide restructuring for improved efficiency, recuperating costs incurred due to inflation, and refinancing while enhancing the maturity schedule of their debt up to 2027. One of the primary focuses during recent earnings calls has been fostering engagement with customers and securing index-based materials pricing contracts. This move is in response to the substantial impact of inflation in materials pricing on the company's profitability. As of the Q1 2023 earnings call , index-based pricing agreements on raw material costs have been successfully implemented with virtually all customers worldwide. During their Q3 2022 earnings call , management reported a recovery rate of around 70% for all raw material inflation, encompassing 2021 and 2022, and moving forward into 2023+. With the conclusion of these commercial negotiations, I believe that a noticeable positive impact on Cooper's adjusted EBITDA has begun to materialize, evident in the company's performance as it transitioned from 2022 into 2023.

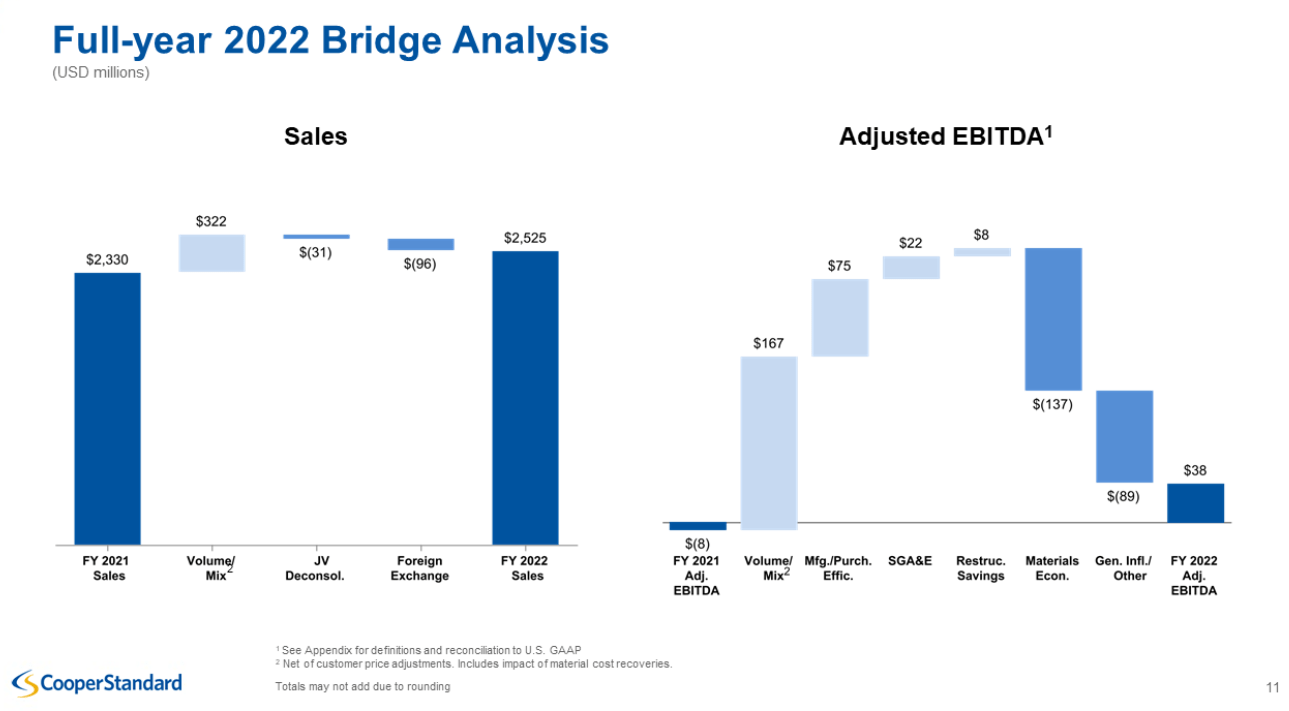

This slide from the company's Q4 2022 earnings presentation illustrates what I believe to be the remarkable extent to which these cost optimization measures have contributed to Cooper's adjusted EBITDA.

Cooper-Standard Q4 2022 Earnings Presentation Slides

The bridge analyses offered by the company in its Q4 2022 earnings presentation provide clarity regarding the substantial bottom-line improvements facilitated by these agreements and cost savings in 2022. They also offer insight into the anticipated enhancements for 2023.

Cooper-Standard Q4 2022 Earnings Presentation Slides Cooper-Standard Q4 2022 Earnings Presentation Slides

{kind=link}

Management emphasized that alongside these new index-based pricing agreements, the recovery of non-material-related costs and the establishment of new sustainable pricing agreements will play significant roles in enhancing the company's bottom line in 2023 and beyond.

With the negotiation of indexed-based material pricing agreements concluded in early 2023, Cooper-Standard is now focused on achieving equitable and sustainable pricing. This pricing strategy takes into account current input costs, market dynamics, and the value the company provides to its customers. The initial focus was on the European segment of the business, aiming to address negative margins and unsustainable cash flow. The majority of customers were supportive, leading to successful negotiations. The company anticipates wrapping up more negotiations in the third quarter.

Furthermore, Cooper-Standard has been making strides in improving cash flows, with progress evident as of Q2 2023. This progress includes implementing more favorable payment terms on trade receivables, customer-owned tooling, and supplier-funded tooling. The company expects these improvements to have a significant positive impact on its cash flow moving forward.

Financials & Projections

With these improvements in profitability along with recovering global production, we look to the company's financial results to confirm that these shifting dynamics are being realized.

Cooper-Standard Public Filings Cooper-Standard Public Filings, Earning Presentations, Q&A Sessions. 2025/2026 Projections are Author's Calculations

(2025/2026 revenue & Adjusted EBITDA projections are my own estimates based on CPS Filings, Global automotive production recovery, Quarterly Earnings Presentations, and Q&A Sessions)

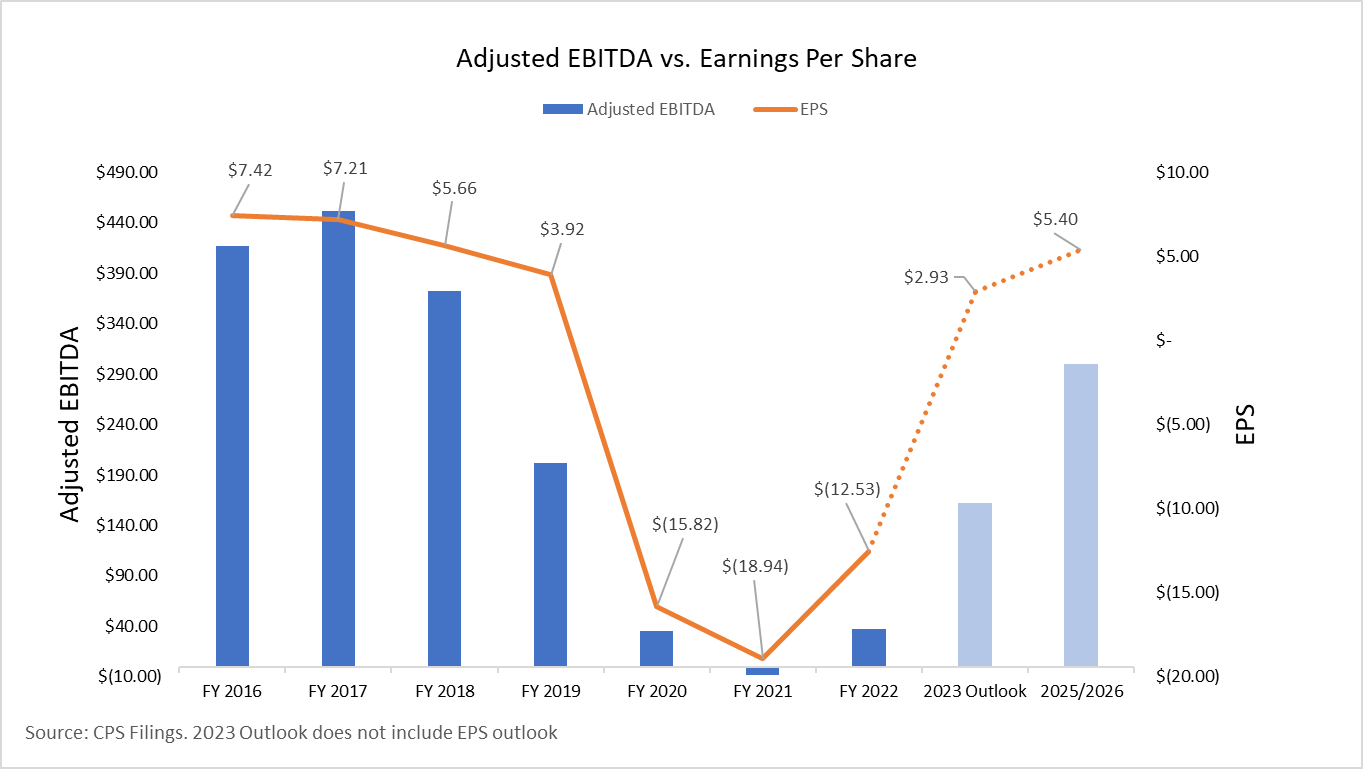

On both quarterly and yearly timeframes, we're seeing revenues and adjusted EBITDA improving significantly over the same period in 2020 and 2021. While revenues continue to grow sequentially in the upper single digits, management expects adjusted EBITDA to increase from $37.8 million in 2022 to $162.5 million in 2023, a 330% increase year over year. Further, the company has indicated that they expect adjusted EBITDA margins to increase into double digits within the next few years. I expect revenues to recover into the $3 billion territory for '25-'26. My own conservative estimate of a 10% adjusted EBITDA margin would put us at an adjusted EBITDA of around $300 million, a further 85% increase over Cooper's current 2023 outlook.

In my view, the company's cash flow and liquidity appear robust as we enter the second half of 2023. CFO Jon Banas addresses a crucial question for investors in the following quote from their Q2 2023 earnings presentation:

Looking at cash flow and liquidity. Cash used in operations was approximately $13 million in the second quarter of 2023, which reflected semiannual cash interest payments made in June, the payout of prior year compensation-related accruals, and other changes in working capital, all of which offset improved operating income.

As mentioned earlier, CapEx was approximately $17 million in the second quarter, primarily reflecting the timing of program launch activity. Free cash flow was an outflow of approximately $31 million in the quarter. With this free cash result, we ended June with a cash balance of approximately $73 million.

Our revolving credit facility was undrawn at quarter end. With $157 million of availability on our ((ABL)) and cash on the balance sheet, we had solid total liquidity of approximately $230 million as of June 30th. We believe that the cash balance at the end of the quarter was likely the low point for the year based on seasonality, increasing sales volume, and the timing of payments from our customers. So, we do expect stronger cash flow in the second half of the year, and it's important to note that during July, our cash balance had already significantly improved from June 30th.

Based on our current outlook and expectations for light vehicle production, improving operating efficiencies and subject to the successful completion of and the further benefit from enhanced commercial agreements from our customers. We believe there will be cash flow positive in the second half and for the full year. Further, we believe our current cash on hand, expected cash generation, and access to flexible credit facilities will provide sufficient resources to support our ongoing operations.

Where's the EPS?

This is all encouraging, but how does it get us back to positive earnings per share?

Cooper-Standard Public Filings & Presentations, EPS Projections are Author Calculated

{kind=link}

(Projections for FY 2023 EPS and 2025/2026 revenues & EPS are my own estimates based on historical data and ratios)

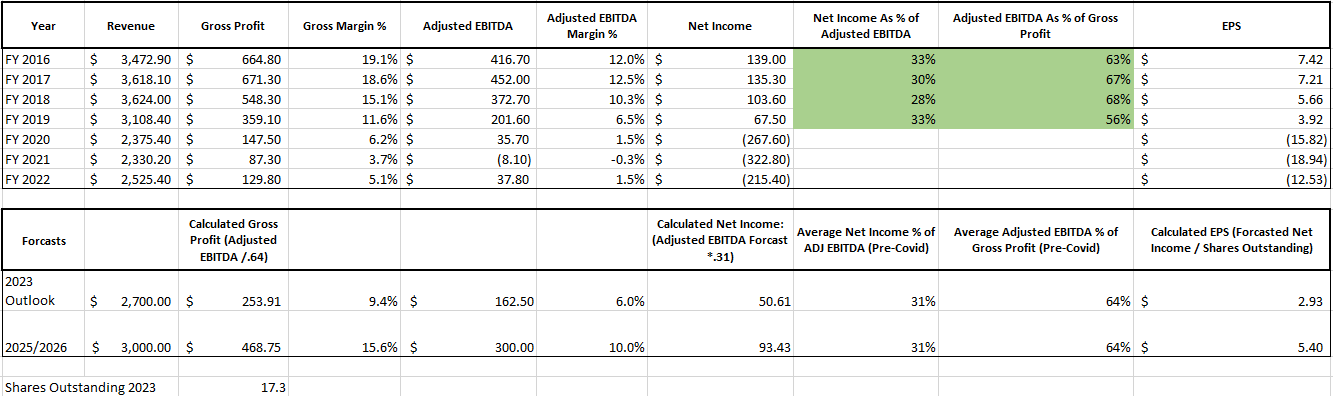

By analyzing the company's pre-COVID financial data and extrapolating it over the next few years, I can discern a clear path for Cooper-Standard to achieve earnings of $5.00+ per share in the 2025/2026 timeframe. The subsequent table provides a more comprehensive insight into the basis of these projections for the company.

Cooper-Standard Adjusted EBITDA and EPS analysis (Author's Calculation using Cooper-Standard Public Filings, Earnings Presentations, and Q&A Sessions)

{kind=link}

By analyzing pre-COVID data, I established a benchmark for how the company's adjusted EBITDA has historically translated into Net Income. During the Q&A session of the Q2 2023 earnings presentation, management expressed an expectation for achieving double-digit EBITDA margins within the next couple of years. Assuming that global production rates, and consequently Cooper's revenues, continue to improve, a return to FY 2017-2019 revenue levels becomes plausible.

Taking what I believe to be a conservative revenue estimate of around $3 billion for the 2025/2026 period and applying a 10% EBITDA margin, I arrived at approximately $300 million or higher in EBITDA within the upcoming years. Based on public filings, the company demonstrated an average net income as a percentage of adjusted EBITDA of roughly 31% in the four years before COVID-19. Applying this conversion rate of 31% to the projected EBITDA for the 2025/2026 period yields an approximate net income of $93.43 million, or $5.40 per share based on the 17.3 million outstanding shares in 2023.

In these calculations, I've opted for the most conservative figures and conversion ratios. However, I believe these estimations could prove to be overly cautious, considering the company's focus on cost savings, sustainable commercial agreements, and ongoing restructuring, all of which are likely to continue benefiting Cooper's bottom line. This aligns with what I believe to be a period of recovering global production and a significant share of higher-margin EV business through new agreements.

Taking my conservative estimate of $5.40 per share in the 2025/2026 timeframe and applying a 10x multiple to it, the result is a stock price in the vicinity of $54. This represents a 215% increase over today's closing price of $17.14.

Risks

Like any investment, there are risks and uncertainties associated with owning Cooper-Standard shares. Risks that would challenge the bullish thesis on Cooper-Standard include but are not limited to:

Automotive Sector Risk: Delayed automotive production schedules or a slowing of the production rate recovery as a whole could materially impact Cooper-Standard's revenues and cash flows.

Commercial Agreements Delays: Delays or the inability of management to continue securing sustainable pricing agreements with customers could pose a significant threat to the company's bottom line, cashflows, and liquidity.

Stock Volatility: Shares of Cooper-Standard could experience short- to medium-term volatility. Negative news related to the automotive industry could act as a temporary adverse catalyst. The company's stock price has appreciated significantly over the past few quarters. The potential for consolidation and volatility exists as the market anticipates upcoming earnings results.

These risks should be monitored diligently, as they can affect Cooper-Standard's performance materially.

An Attractive Investment

Quarter after quarter, management has consistently underpromised and over-delivered, achieving a remarkable commercial turnaround during times of economic uncertainty and industry headwinds. I have full confidence in Cooper-Standard's management team to continue forging sustainable commercial agreements and capitalizing on their recent success, thereby propelling the company towards once again becoming a cash-generating enterprise. In the short term, I believe that the stock will undoubtedly experience some volatility, but I firmly believe that with the ongoing commercial turnaround, significant impending revenue opportunities, and the continued expansion of their higher-margin EV business, all the necessary conditions are in place for this company (and its stock) to act as a coiled spring ready to propel forward. I am prepared to embrace any short to medium-term stock price fluctuations while eagerly anticipating the promising prospects that lie ahead for the company in the next 2 to 5 years.

For further details see:

Cooper-Standard Holdings: An Impressive Turnaround Story That's Just Getting Started