CPS - Cooper-Standard Holdings: Solid Quarterly Results And Technical Chart

2023-11-09 01:18:27 ET

Summary

- Cooper-Standard Holdings recently announced solid Q3 FY23 results, posting a profitable quarter for the first time since 2021.

- CPS's sales for Q3 FY23 rose by 12% compared to the previous year, with increased sales in Europe and North and South America.

- The company's financial turnaround and positive technical chart indicate potential growth, making CPS a rewarding investment opportunity.

Company Overview

Cooper-Standard Holdings ( CPS ) manufactures sealing, fluid transfer, and brake delivery systems. Its products include dynamic seals, encapsulated glasses, tube coatings, frameless systems, metallic brake lines, and many more. The company was established in 1960 and operates in countries like the United States, Canada, China, France, and Mexico.

Investment Thesis

CPS recently announced solid Q3 FY23 results. Due to the cost-cutting and lean-saving initiative, they were able to post a profitable quarter for the first time since 2021. In addition, its technical chart is indicating a turnaround, so I believe it might be rewarding in the coming times. Hence, I assign a buy rating on CPS.

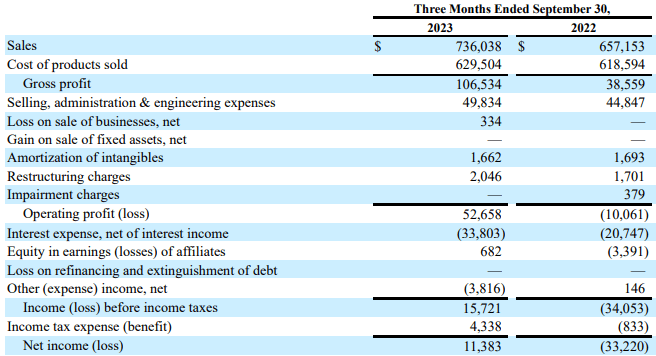

Financial Analysis

CPS recently announced its Q3 FY23 results . The sales for Q3 FY23 were $736 million, a rise of 12% compared to Q3 FY22. A favorable volume and mix helped them to increase sales in Europe and North and South America, which was the major reason behind the company's increased sales. Its sales in Europe, North America, and South America increased by 29.8%, 17%, and 26.8%. Its adjusted EBITDA for Q3 FY23 was $79.1 million, which was $20.5 million in Q3 FY22. The improvement was mainly due to management's operational efficiency and lean saving initiative.

{kind=link}

The net income for Q3 FY23 was $11.3 million compared to a net loss of $33.2 million. For me, this was the highlight of the results. Seeing the company being profitable was a pleasing sight. Since 2021, the company has failed to post a profitable quarter, so in my opinion, this quarter was quite impressive. The management has raised the FY23 sales guidance considering the increased production and strong demand. Now, it's around $2.75 billion, which is higher than the FY22 revenue. In fact, it will be the highest in the last three financial years, showing that the company might have fully recovered from the COVID-19 impact. So, I believe the financial turnaround might positively impact the company's share price in the coming quarters. The Q3 FY23 was the best-performing quarter for the company in FY23 in terms of sales growth, margins, and profitability. The Covid 19 disrupted auto production, which affected the company's sales to a great extent, and it was reflected in the financial results till the last quarter. The supply chain was disrupted, but in the last few months, the supply chain has improved and will continue to improve, which I believe will boost global auto production in the coming times. In addition, the continuous rise in the EV market is also a tailwind for the company, and it might boost its sales in the coming quarters. So I think there are several tailwinds for the company, like increased auto production, easing supply chain, and EV trend. However, I want to point out one headwind that will impact the company's sales. The interest rates in Europe are sky-high, which can affect the demand in the European region, and the company might struggle in Europe.

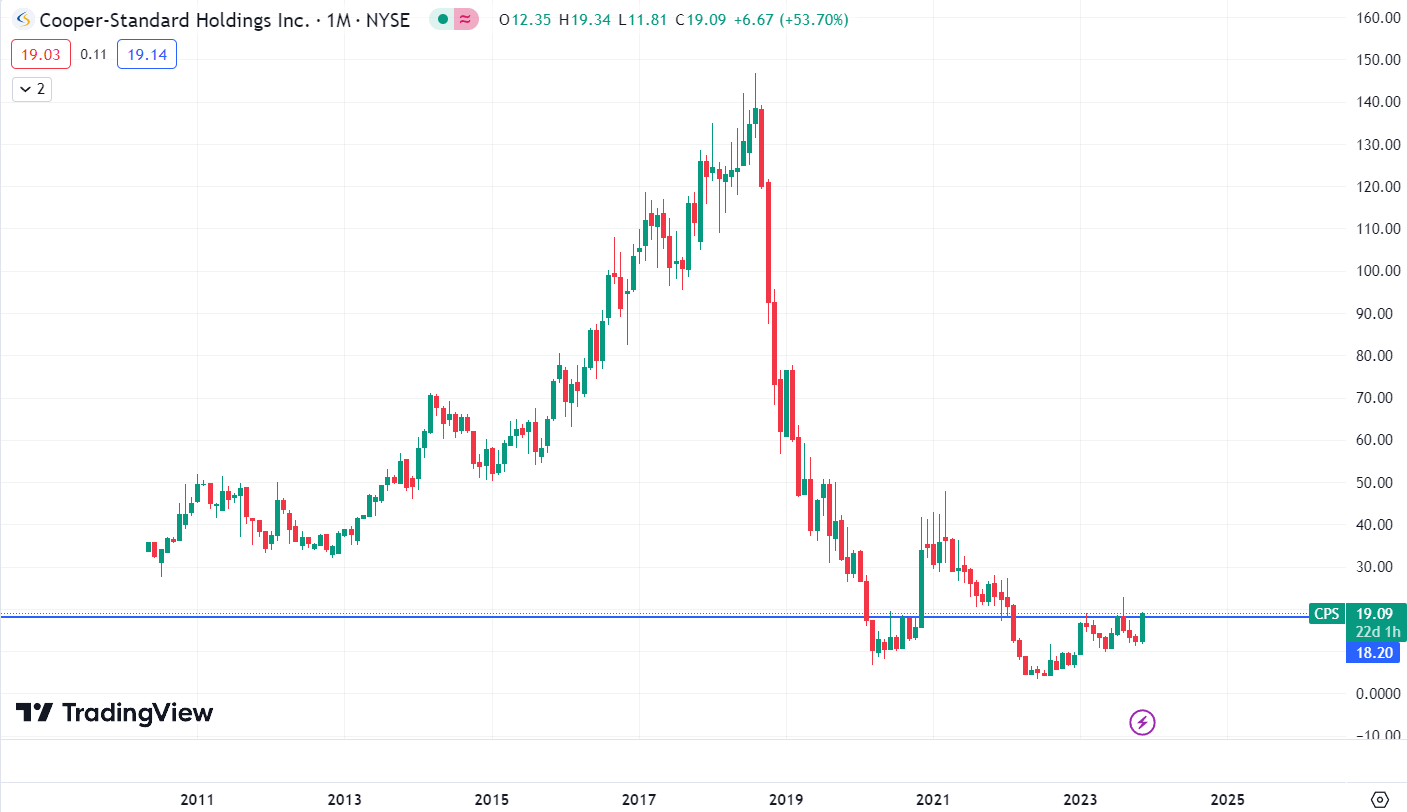

Technical Analysis [Monthly Analysis]

{kind=link}

CPS is trading at $19. The price chart of CPS is looking quite solid, and it might be rewarding in the long term. After making a high of $146 in 2019, the stock price has fallen about 87% since then. But the monthly time frame of CPS is showing a turnaround. The stock has given a breakout above the $18.5 level, which it has been trying to break since January 2023. So, the breakout shows that buyers are now active in this stock, and the second reason I am bullish on CPS is because of the change of structure. The stock has started to form higher lows, which is a positive pattern change, and the stock is moving up slowly and steadily, so the probability of the breakout being successful is high.

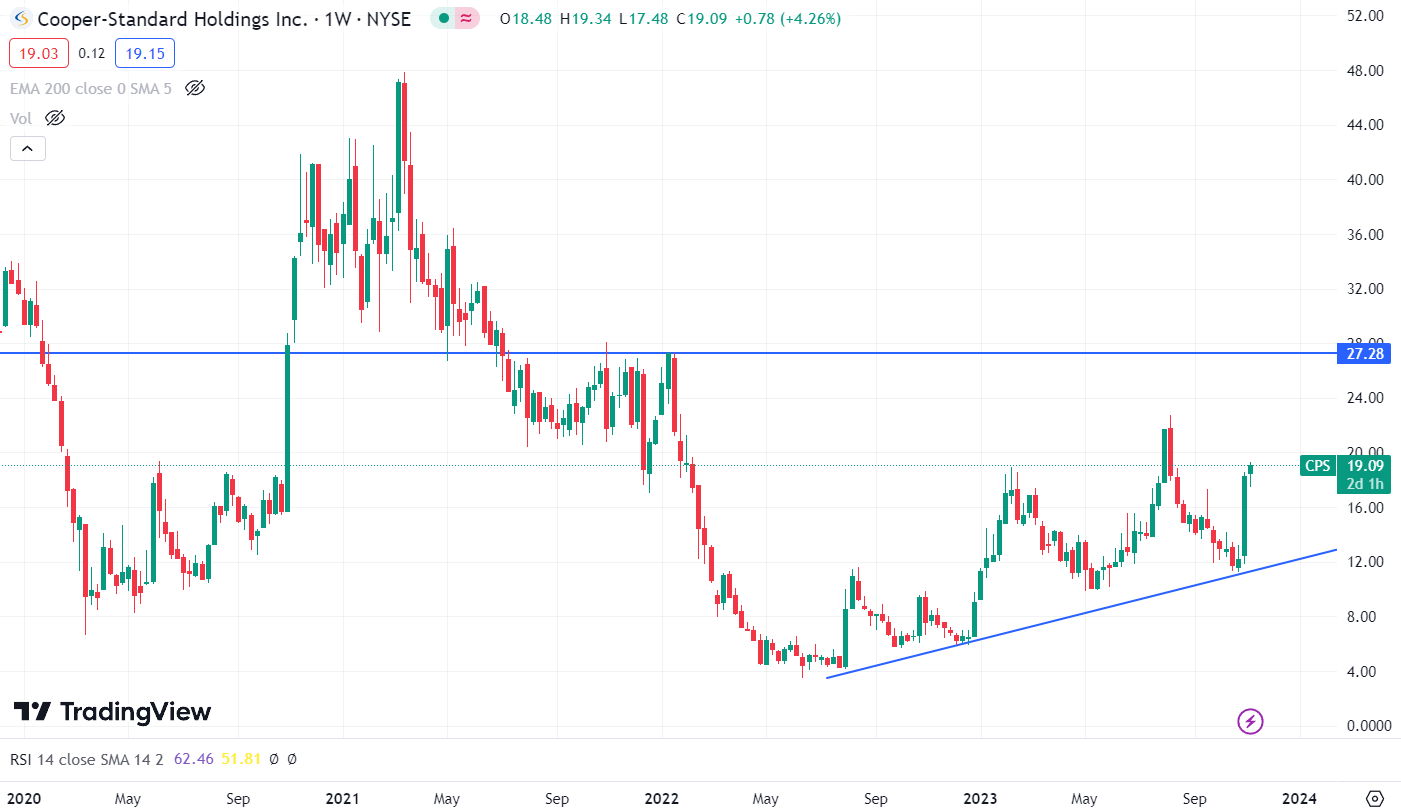

Technical Analysis [Weekly Analysis]

{kind=link}

After doing a monthly time frame analysis, I believe CPS is looking good for the long term and not only long term; it is looking good for the next twelve months. The stock has started to follow a trendline and started to form higher highs and higher lows, which is a bullish indication if we look at the recent candle. It was a huge green candle, which shows there are people buying it in huge quantities near the trendline. Looking at the structure, I believe the stock will now try to form a new higher high, and the next resistance level that I see is around $27, which gives us an upside of 40% from the current level. Hence, I am bullish on CPS in both the long and short term.

Should One Invest In CPS?

It is looking good both on the monthly and weekly charts, and I believe the recent improvement in the stock price is mainly because of the positive results. It was struggling to be profitable, but the management achieved it through operational efficiencies, and being profitable was a huge positive for them. Now, looking at CPS's valuation . CPS has an EV / EBITDA [TTM] ratio of 8.11x compared to the sector median of 10.19x and has a Price / Sales [TTM] ratio of 0.12x, which is also lower than the sector ratio of 0.81x. Its valuation also looks favorable and looks financially and technically strong. Hence, I believe it can be rewarding in the coming times.

However, I want to point out one risk: if we look at the balance sheet, we can see that its short and long-term debt has increased. Its short-term debt at the end of September was around $169.3 million, and the long-term debt by the end of September was $1 billion, which is 4.8% higher compared to December 2022. So, looking at the company's history of struggling to be profitable raises some concerns. If it continues to struggle with profitability as it has been for the past three years, then the debt can be a huge concern.

Risk

Their whole cost structure could increase due to inflation, which could have a negative impact on their business, finances, and operational outcomes. Wages, the price and accessibility of components, raw materials, and other inputs, as well as their capacity to satisfy consumer demand, may all be impacted by further inflationary pressures. Other risk considerations, such as supply chain disruptions, risks associated with overseas operations, and the hiring and retention of talented personnel, may be made worse by inflation. Their profit margins and cash flows could be negatively impacted if they are unable to convince their clients to raise the prices of their goods at a pace that would keep up with inflation.

Bottom Line

CPS posted solid quarterly results, and this was the first profitable quarter since 2021, which is huge. In addition, the technical chart indicates a potential turnaround in the stock. So, looking at the financials, technical chart, and favorable valuation, I think it can be rewarding. Hence, I assign a buy rating on CPS.

For further details see:

Cooper-Standard Holdings: Solid Quarterly Results And Technical Chart