CPS - Cooper-Standard Wows: Beats EPS Issues Strong Guidance Despite UAW Concerns

2023-11-14 01:53:14 ET

Summary

- Cooper-Standard Holdings has delivered strong Q3 results, with revenue increasing by 12% YoY and net income improving significantly.

- The company has raised its revenue and adjusted EBITDA targets for 2023, indicating confidence in its future growth.

- CPS is well-positioned to capitalize on the growing electric vehicle market, which presents a significant revenue opportunity for the company.

- The worst of the UAW impact appears to be coming in Q4 but is already considered in the company's raised guidance.

Today, I am reiterating a "buy" rating on Cooper-Standard Holdings (CPS) with an initial target price of $54. The stock is now trading around $17.27, an increase of 9.44%, since the publishing of my establishing article .

Thesis

Cooper-Standard Holdings continues to achieve what I believe is a remarkable commercial turnaround. The company appears to have reached an inflection point with its corporate restructuring, cost-saving strategies, enhanced commercial agreements, recovering global light vehicle production rates, and the emergence of new product offerings. In my view, the company's achievements in the third quarter have strengthened the bullish thesis. Management has confidently navigated headwinds like the United Auto Workers ((UAW)) strike and the continuation of commercial negotiations with suppliers. Positive catalysts such as the rise of hybrid electric and battery electric vehicles, new products that improve the company's content per vehicle, and a wholly-owned AI startup that has achieved its first commercial contract give the company an opportunity to realize revenues and profitability higher than pre-pandemic levels.

Thematics

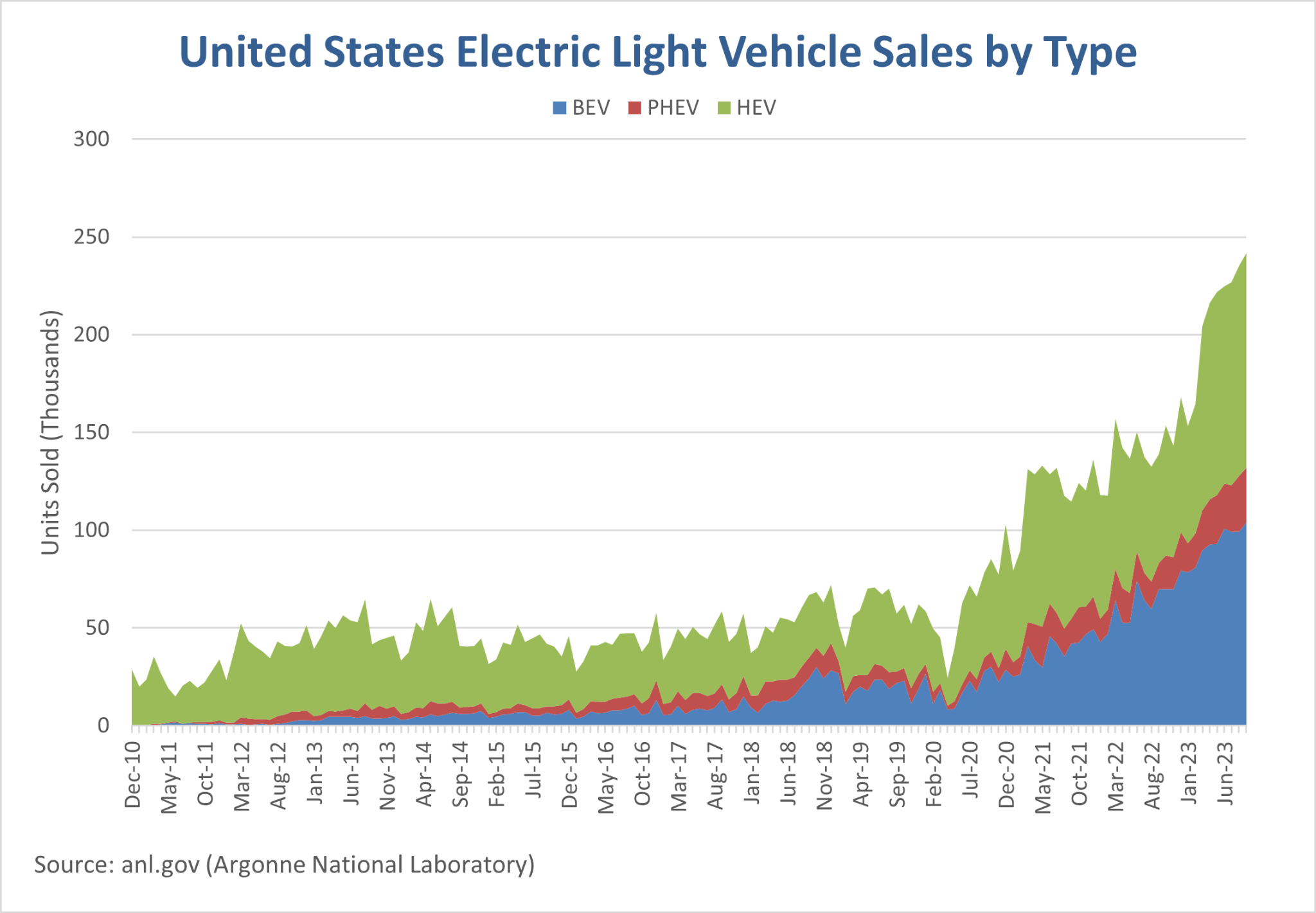

While many forecasts and analyses for Cooper-Standard have focused solely on a recovery to pre-COVID levels in the light vehicle industry, the underlying dynamics have begun to change markedly. The chart below introduces a new theme that could enable Cooper-Standard to capitalize on a significant revenue opportunity, should production levels rebound to those seen before the pandemic.

anl.gov (Argonne National Laboratory)

{kind=link}

Since the COVID trough in light-duty vehicle ((LDV)) sales, battery electric ((BEV)), plug-in hybrid electric ((PHEV)), and hybrid electric ((HEV)) vehicle sales have increased by a staggering 1191%, 1290%, and 669% respectively. With this growth in the EV segment comes a significant revenue opportunity for Cooper-Standard, as these vehicles require more complex internal systems like engine, motor, and battery cooling systems, cabin heating, drive inverters, and CPU cooling. For instance, Cooper-Standard supplies about 8 parts for a traditional internal combustion engine ((ICE)) vehicle, HEVs require 28 parts, while BEVs require 20 parts. According to the company, there's a 20% increase in content per vehicle ((CPV)) in BEVs versus ICE-based vehicles. These trends begin to shine through when looking at the company's net new EV awards totaling approximately $88.4 million thus far in 2023.

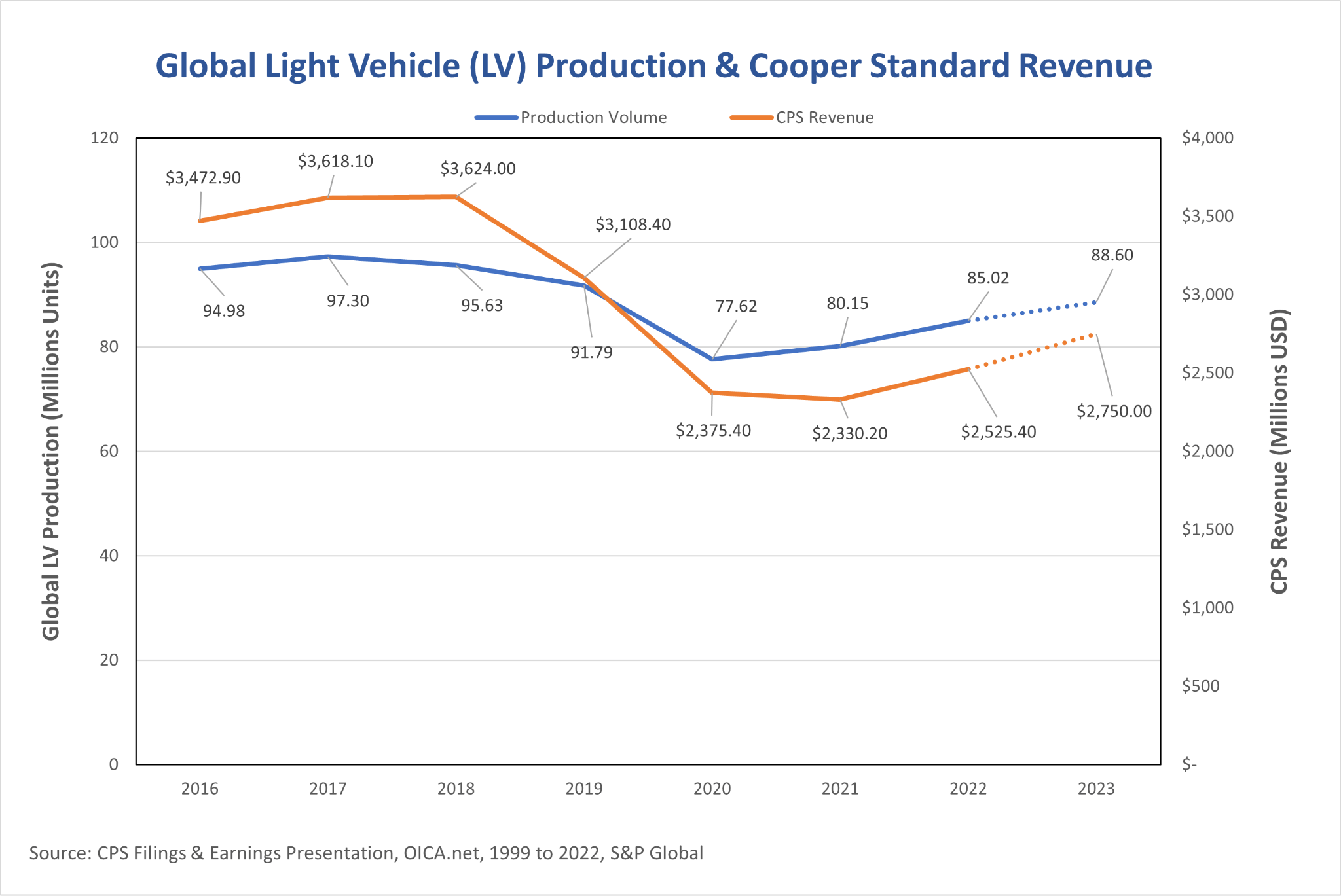

In my view, these improvements to CPV begin to shine through when looking at comparable growth rates between Cooper-Standard's revenues and global light vehicle production.

CPS Filings & Earnings Presentations, OICA.net 1999 to 2022, S&P Global

{kind=link}

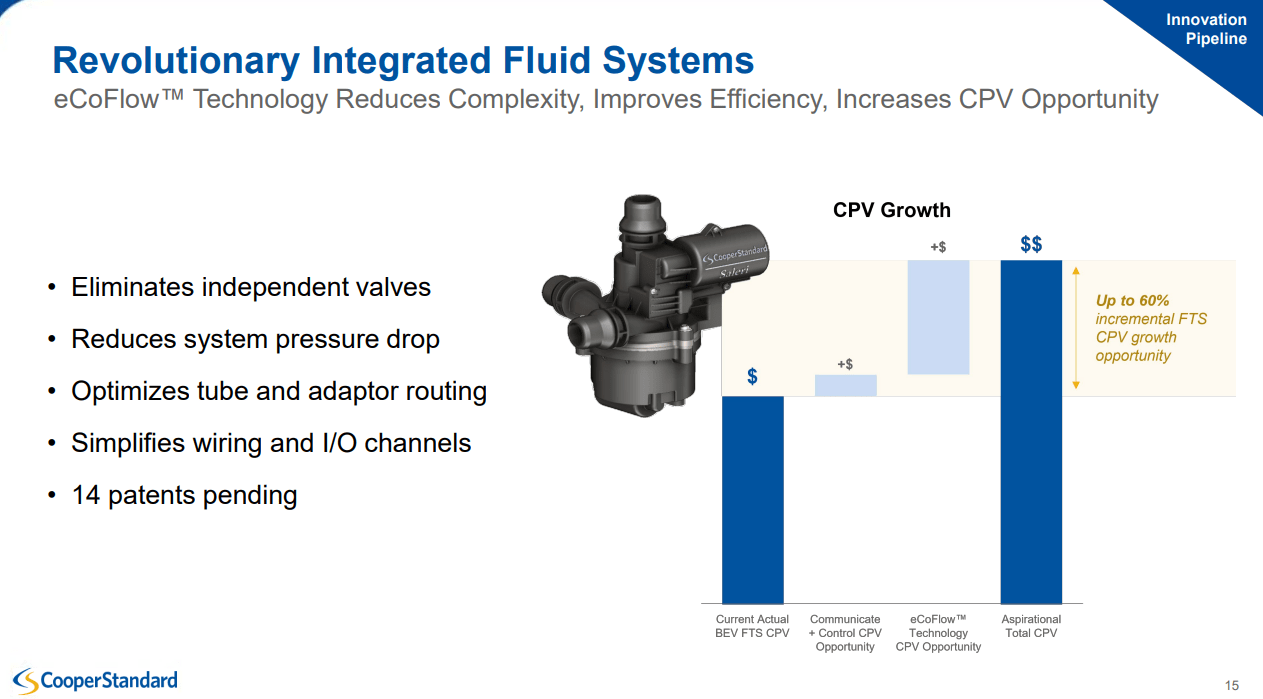

In FY 2023, Cooper-Standard's revenues are expected to increase approximately 8.89% over FY 2022. This is over double the expected growth rate of global light vehicle ((LV)) production for the same period. In my view, this outperformance in growth is a result of the company's strategic efforts to increase its content per vehicle ((CPV)) through innovative products such as an upcoming integrated fluid system called eCoFlow.

Further, the company has set an aspirational goal of an incremental increase in CPV of up to 60% in its Q3 2023 earnings presentation .

Cooper-Standard Q3 2023 Earnings Presentation

{kind=link}

Simply put, Cooper-Standard is demonstrating a clear focus on an innovation pipeline that unlocks significant incremental revenue opportunities per vehicle produced. Consequently, I expect the company's revenue growth to continue to outperform the increases in global light vehicle production into and beyond 2024.

Cooper-Standard 's AI Initiative

The company shed some light on an initiative that most investors are fully appreciating at the moment. Liveline Technologies achieved a crucial commercial milestone, signing its first external contract for Advanced Process Controls ((APC)). Liveline is a proprietary artificial intelligence ((AI))-based APC that was initially developed for internal use at Cooper-Standard facilities. Internally, the technology is being used on 20 lines in 4 different countries. This APC technology has achieved significant efficiency and scrap reduction internally, with management stating a typical controllable scrap reduction of 50%, and "significant" realized savings. The company believes that this technology has the potential to benefit many manufacturing companies across a wide range of industries. That brings us to Liveline Technologies, a wholly-owned AI startup subsidiary meant to market this product to external customers. Though details on pricing were not given, this is something I will be watching closely in the coming quarters as it has the potential to be an interesting new revenue opportunity for the company.

Financials

The company has now started to realize the full benefits of its lengthy process of renegotiating customer agreements. In Q3, Cooper-Standard reported that the majority of these customer negotiations were successful. The outcomes included sustainable pricing agreements, recovery of increased costs and inflation, improved payment terms for trade receivables, and better payment conditions for tooling owned by customers.

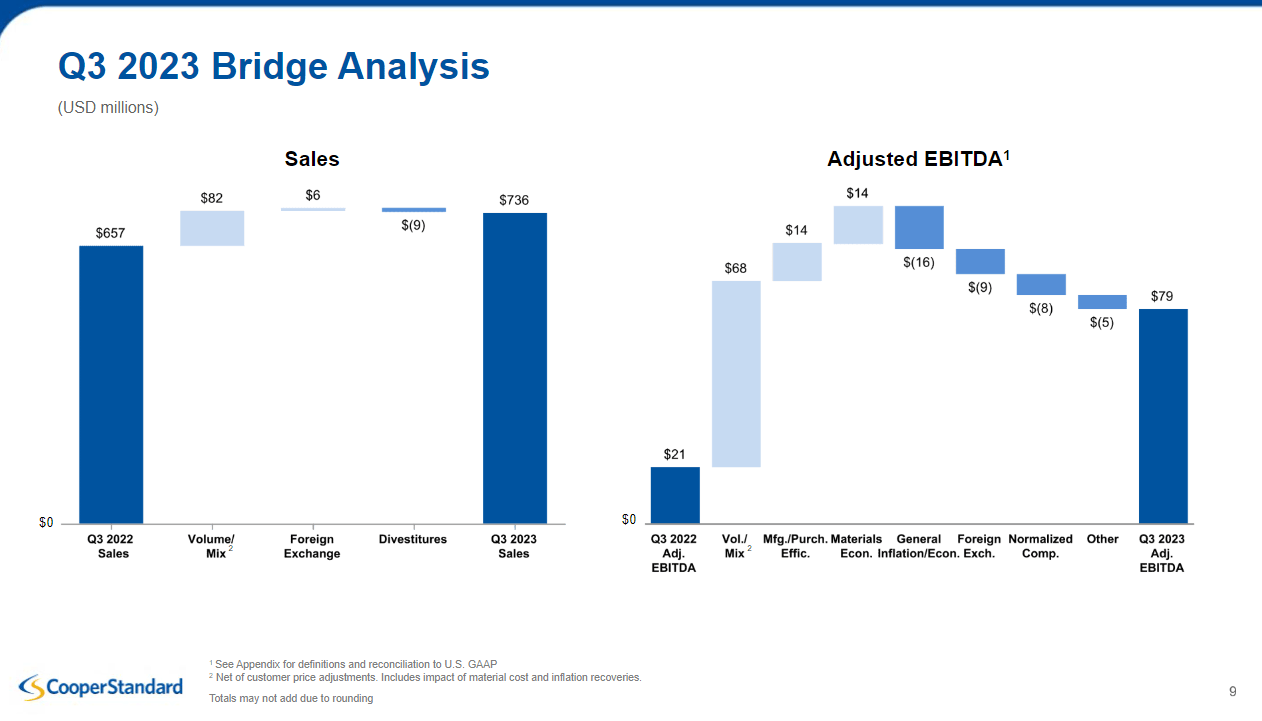

The following bridge analysis from the company's Q3 earnings presentation underscores the significance of what management has accomplished.

Cooper-Standard Q3 2023 Earnings Presentation

{kind=link}

In terms of both sales and adjusted EBITDA, volume and mix were the largest contributors to year-over-year improvements. In addition to higher production volumes and a more favorable mix of higher content per vehicle ((CPV)) such as electric vehicles (EVs) and hybrid vehicles (HVs), retroactive cost recoveries, including materials and inflation recovery, also contributed approximately $25 million to $30 million between sales and adjusted EBITDA.

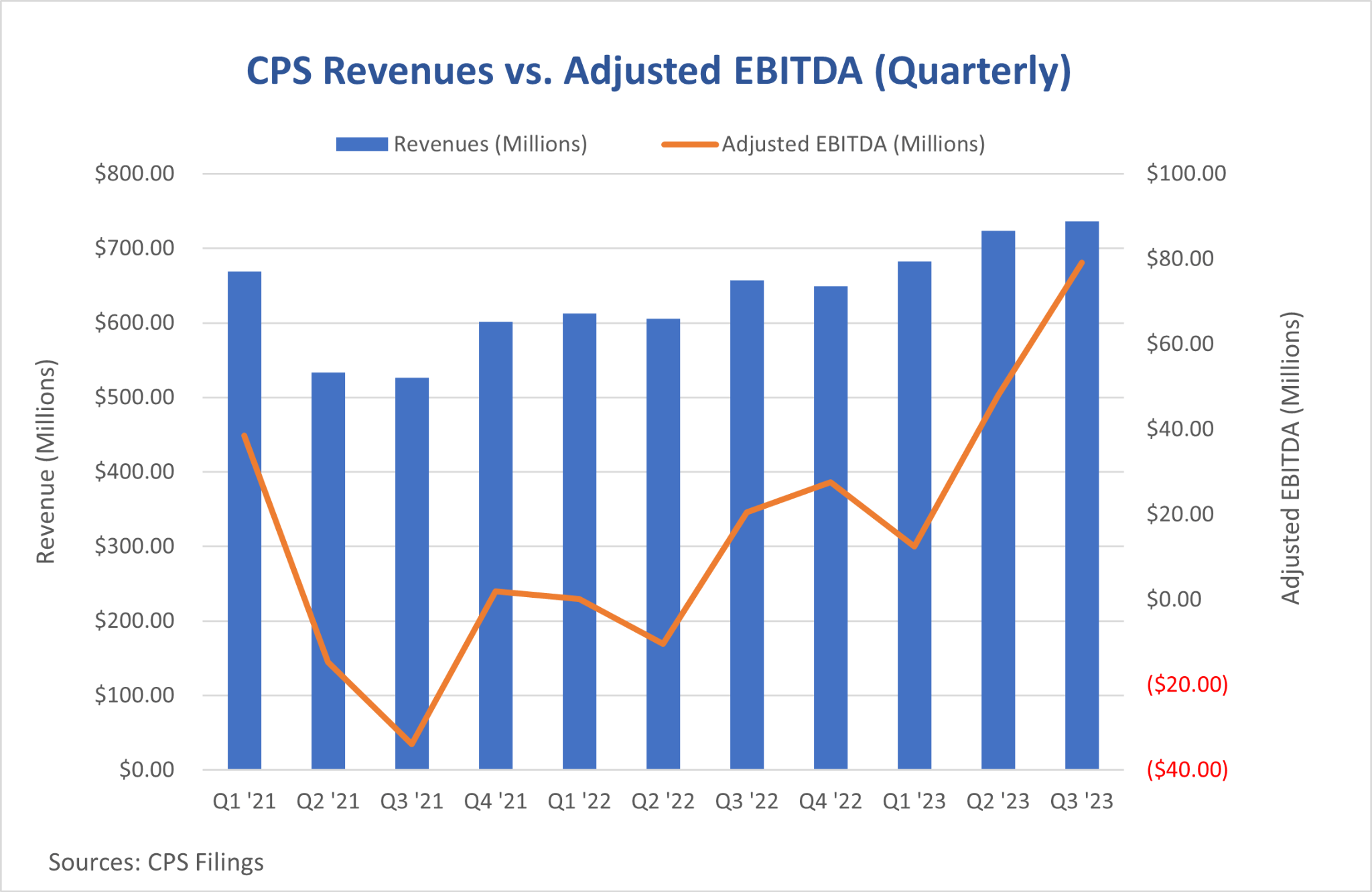

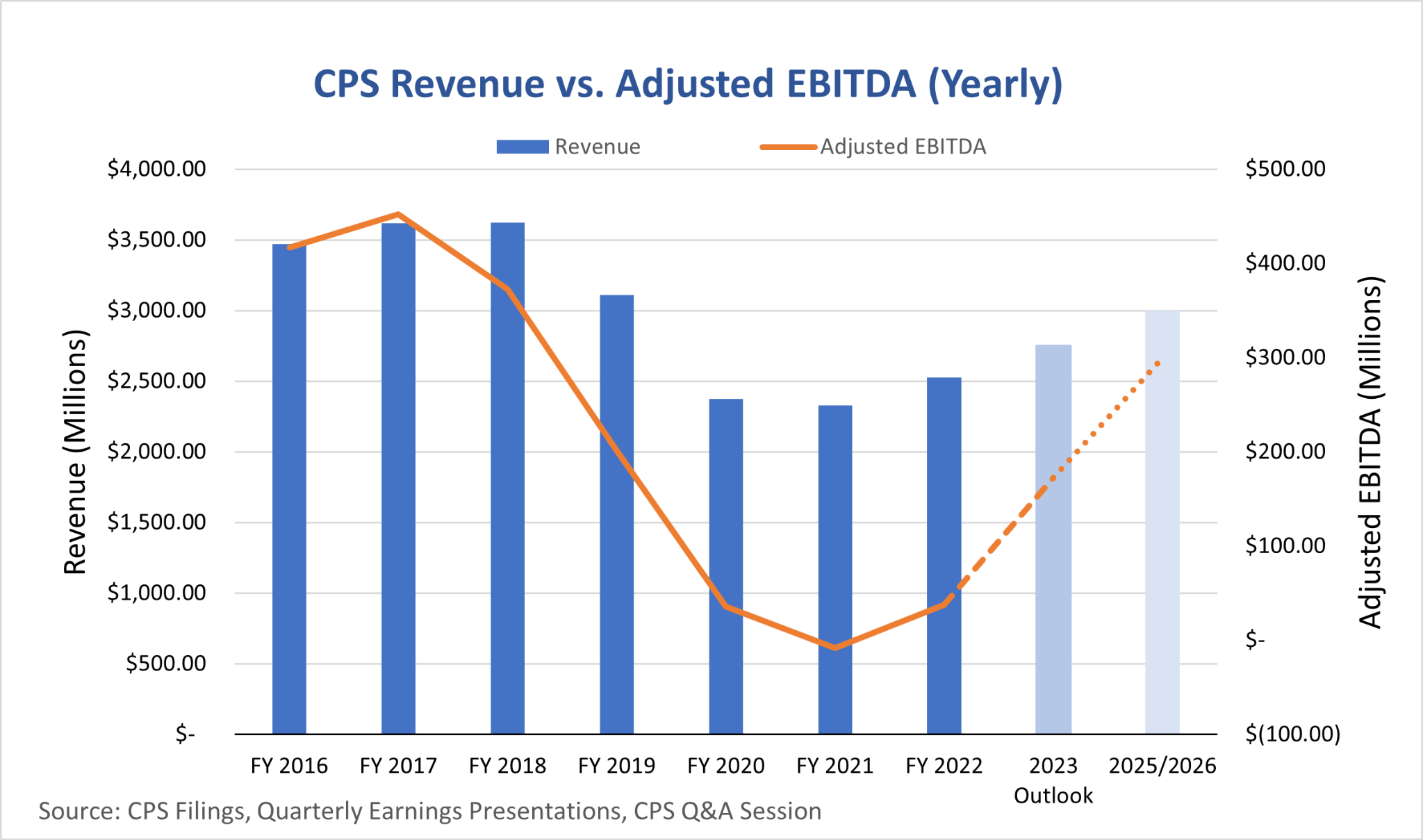

By zooming out a few years, we can get a better sense of how far the company has come in terms of improving adjusted EBITDA.

Cooper-Standard Public Filings

{kind=link}

Cooper-Standard Public Filings

{kind=link}

On both quarterly and yearly timeframes, Cooper-Standard continues to make significant progress toward its recovery and subsequent profitability.

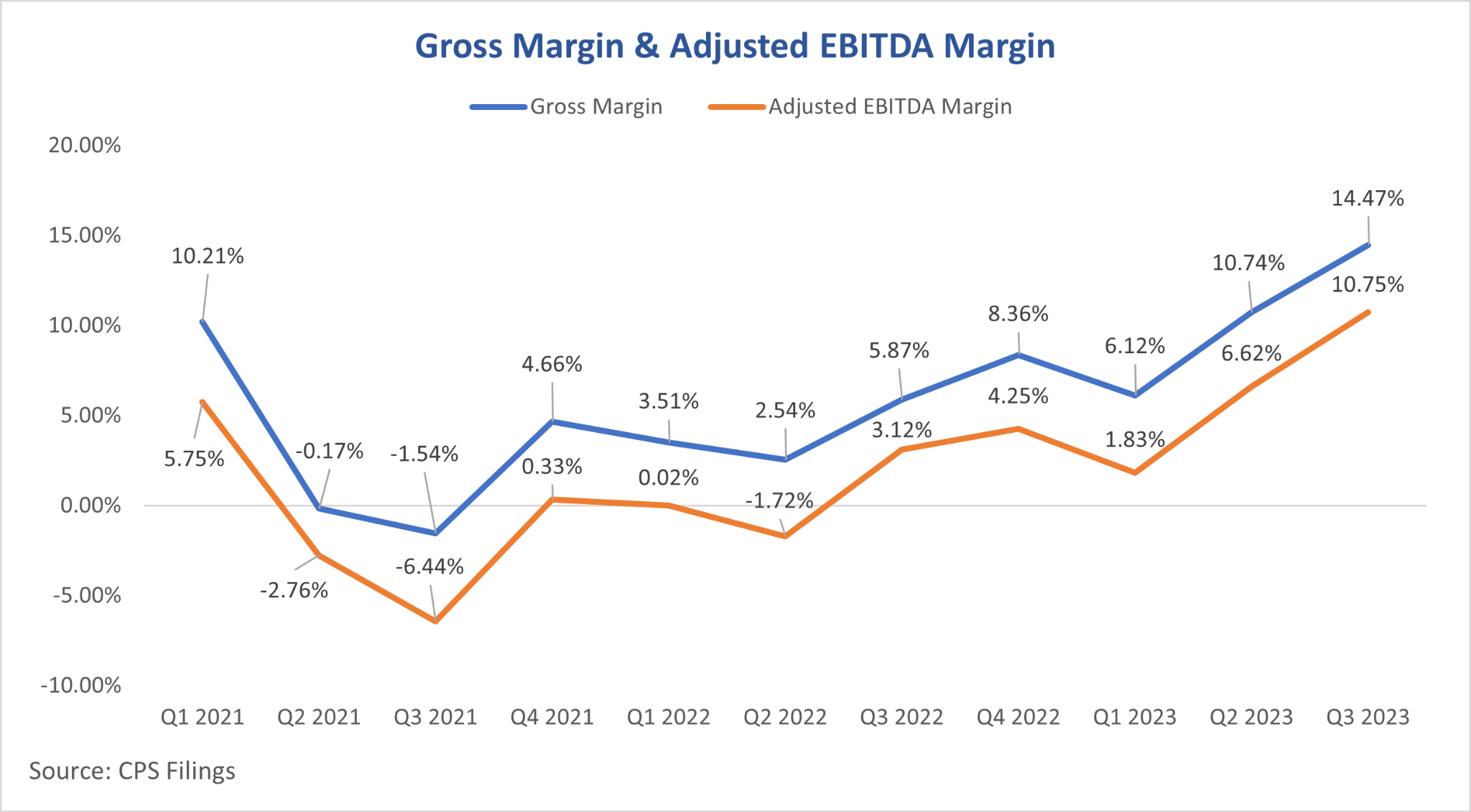

Margin Expansion

Cooper-Standard Public Filings

{kind=link}

As production volume, mix, and Cost of Goods Sold ((COGS)) improve, the company continues to achieve new highs over a multi-year period in both gross profit and adjusted EBITDA margins. In just two years, the company has improved its gross margin from -1.54% to 14.47% and its adjusted EBITDA margin from -6.44% to 10.75%. It appears that we are now within reach of the company's previously stated goals of normalized double-digit gross and adjusted EBITDA margins.

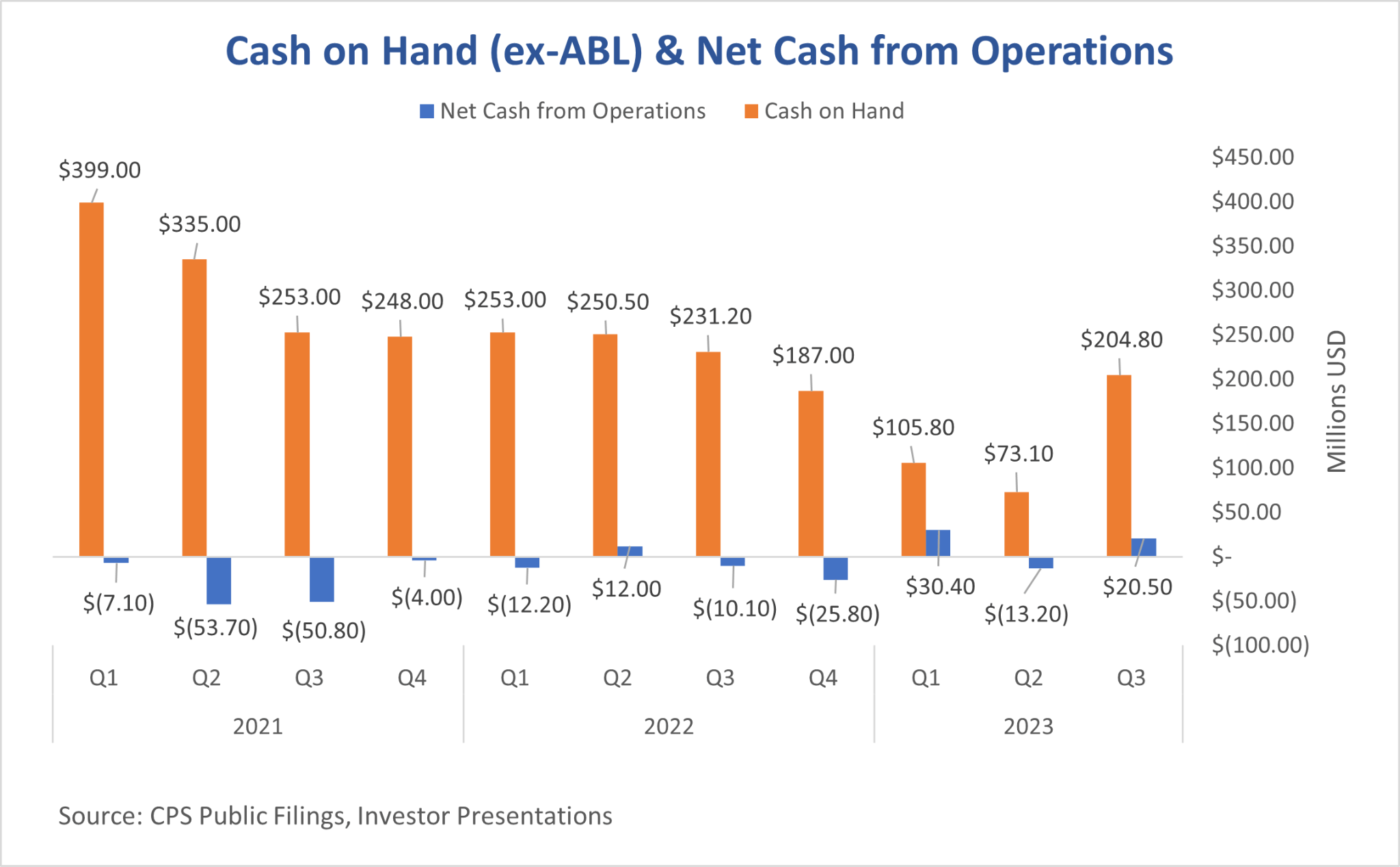

Liquidity

In my view, the company continues to demonstrate robust liquidity. Including its Asset-Based Lending ((ABL)) facility, Cooper-Standard had a solid total liquidity of approximately $259 million at the end of the quarter.

I believe the following quote from CFO Jon Banas on the company's Q3 2023 earnings call highlights their confidence in the current liquidity situation:

We ended September with a cash balance of approximately $205 million. This included a draw on our ABL facility of $120 million, which we opted to take prior to quarter end, as a precautionary measure, due to the uncertainty and anticipation of potential production disruptions related to the OEM labor negotiations.

Because we had this cash on hand from the ABL draw, we did not factor our receivables in Europe, as we typically would. And this had the effect of reducing free cash flow in the quarter by approximately $15 million. With $55 million of remaining availability on our ABL, and cash on the balance sheet, we had solid total liquidity of approximately $259 million, as of September 30.

With the OEMs and the UAW, having recently reached tentative labor agreements, which has significantly reduced the risk of further production disruptions. We no longer felt carrying the incremental cash from the ABL borrowings was necessary. And we repaid the $120 million this morning.

Cooper-Standard Public Filings, Investor Presentations

{kind=link}

The repayment of the previously mentioned ABL draw appears to be a clear sign of management's confidence moving forward. In addition to this decisive move, the company also believes that its present cash reserves, anticipated future cash flows, and access to flexible credit facilities will furnish ample resources to support ongoing operations. These reserves are expected to be further strengthened by projected positive cash flow in the fourth quarter.

UAW Impact

Though the United Auto Workers ((UAW)) strike began in the third quarter, there was a minimal impact of approximately $5 million on Q3 revenues. The company expects a Q4 revenue impact of $30 million and an EBITDA impact of $8-10 million. It is important to note that the impacts on the company's Q4 results could end up being higher or lower, depending on the re-ramp of OEMs. In my view, the worst is behind us, with the UAW striking tentative deals with Stellantis , Ford , and now General Motors .

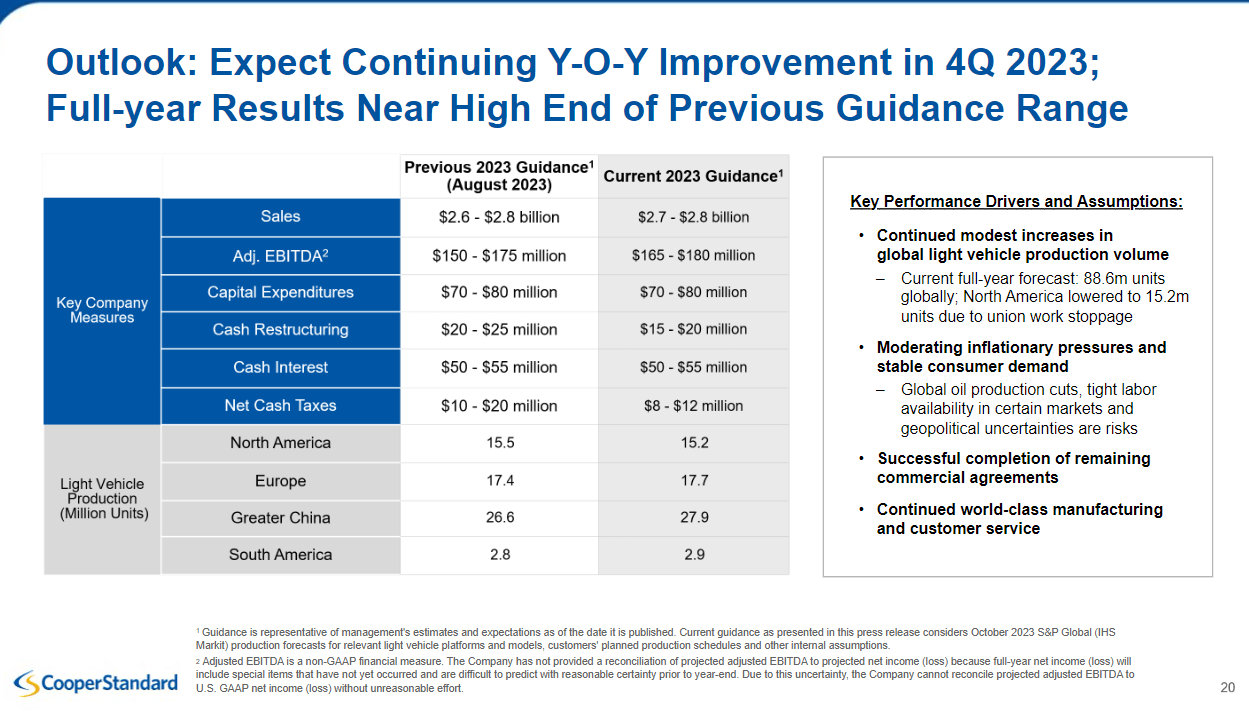

Guidance

Though it appears that the UAW strike will impact Q4 results, the company's financial guidance was raised across the board.

Cooper-Standard Q3 2023 Earnings Presentation

{kind=link}

In this updated slide from the call, we can see that the revenue guidance range has been tightened upward, and the company's expected FY 2023 adjusted EBITDA has been revised upwards. Furthermore, cash restructuring and net cash tax expectations have been revised downwards. This positive news comes with the expected impacts of the UAW strike already accounted for in the updated numbers. Even when faced with short-term headwinds, the company's recovery appears to be unstoppable, in my view.

The company's light vehicle production expectations were also revised upwards in all regions except North America, which was impacted by the UAW strike. I believe this is further evidence that global light vehicle production is well on its way to returning to pre-COVID levels.

Risks

There are risks and uncertainties associated with owning Cooper-Standard stock. Risks that would challenge my bullish thesis on Cooper-Standard include but are not limited to:

Automotive Sector Risk: Delayed automotive production schedules or a slowing of the production rate recovery as a whole could materially impact Cooper-Standard's revenues and cash flows.

Commercial Agreements: Delays or the inability of management to continue securing the remainder of their sustainable pricing agreements with customers could pose a threat to the company's bottom line, cashflows, and liquidity.

Stock Volatility: Shares of Cooper-Standard could experience short- to medium-term volatility. Negative news related to the automotive industry could act as a temporary adverse catalyst. With the stock now up ~40% since the company's Q3 earnings report, negative catalysts like weaker Q4 production in North America due to the UAW strikes may put pressure on the stock.

These risks should be monitored diligently, as they can affect Cooper-Standard's performance materially.

Conclusion

Cooper-Standard continues to impress investors by delivering "blow-out" quarterly results in Q3. The convergence of the company's remarkable commercial turnaround and the immense operational leverage gained from recovering global auto production rates continues to validate the bullish thesis surrounding the company. In my view, there is a very clear path forward for the company; therefore, I welcome the volatility that may present itself in the coming quarters, giving investors an opportunity to buy a stock that's valued at a significant discount compared to what I believe it will be earning on a per-share basis in the next 1-3 years. Thank you for reading.

For further details see:

Cooper-Standard Wows: Beats EPS, Issues Strong Guidance Despite UAW Concerns