CPA - Copa Holdings: A Continuation Of Opportunity Reiterate Buy

2023-08-22 21:03:27 ET

Summary

- If Copa maintains its current pace of adding 2 airplanes per quarter, it could fall short of its expectations, potentially leading to a delay in expansion plans by approximately 2.25.

- While its operating margins experienced a modest increase in Q2, attributed to reduced fuel prices, the sustainability of this improvement could be jeopardized if OPEC enacts further production cuts.

- The pivotal juncture in Copa's growth trajectory could materialize around 2038, coinciding with the retirement of its older fleet.

- In the medium term, investors in Copa can anticipate annual return rates reaching up to 49%.

- The DCF analysis implies a stock price of $244, with future projections pointing toward a stock price of $382.

Thesis

In my earlier article about Copa Holdings, S.A. ( CPA ), I set a target stock price of $209 for Copa. However, as of now, the revenue projections for both 2023 and 2024 have already been achieved. Consequently, I found it necessary to revise the revenue expectations for the upcoming years, incorporating a roughly 9% increment to accurately align them.

This adjustment notably influences the 2028 target, which, under the most optimistic circumstances, now reaches approximately $382. Given the prevailing stock price of $95.64, this revised target implies an impressive upside potential of 299% or an annual growth rate of 49%.

Overview

Starting from Q1 2023, Copa has acquired an additional 2 airplanes. Consequently, the total airplanes received by the company in this year thus far amounts to 4. Assuming this acquisition pace remains constant and projecting that Copa will secure 4 more airplanes during the remaining two quarters of its fiscal year, it becomes evident that the company will fall short of the 11 airplanes required annually to integrate the targeted 66 airplanes into its fleet. In simpler terms, Copa is projected to require an additional 2.25 years to fulfill its complete order of 66 airplanes.

Furthermore, the stock has witnessed a decline of approximately 13% since the publication of my initial article about this stock. This decline can be attributed to the prevailing deterioration in market sentiment, resulting in an overarching market downtrend. Another factor influencing this decline is the looming risk of a recession in China. As a significant foreign investor in Latin America, China holds a position second only to the United States. The concern lies in the potential consequences of a Chinese economic crisis, which could cast a negative shadow over the global economy and potentially trigger recessions in the nations where China wields substantial economic influence.

Financials (In millions of USD, unless stated otherwise)

Copa's margins have experienced a nice upturn due to the surge in travel demand coupled with a notable reduction in fuel prices. This decline in fuel costs was propelled by the decrease in the price per oil barrel, which, between March and June, exhibited oscillations within the range of $65 to $72. However, following a trough at $67, the price of oil rebounded to a zenith of $84.29.

Crude Oil Price Evolution (CNBC)

{kind=link}

This increase was spurred by OPEC+'s decision to curtail production in response to the downward pressure on prices resulting from apprehensions of a global recession. Nevertheless, given the present decline in oil prices, OPEC+ will likely be compelled to enact further cuts. Without such measures, the downward trajectory will persist, particularly while the potential of a China recession remains a concern.

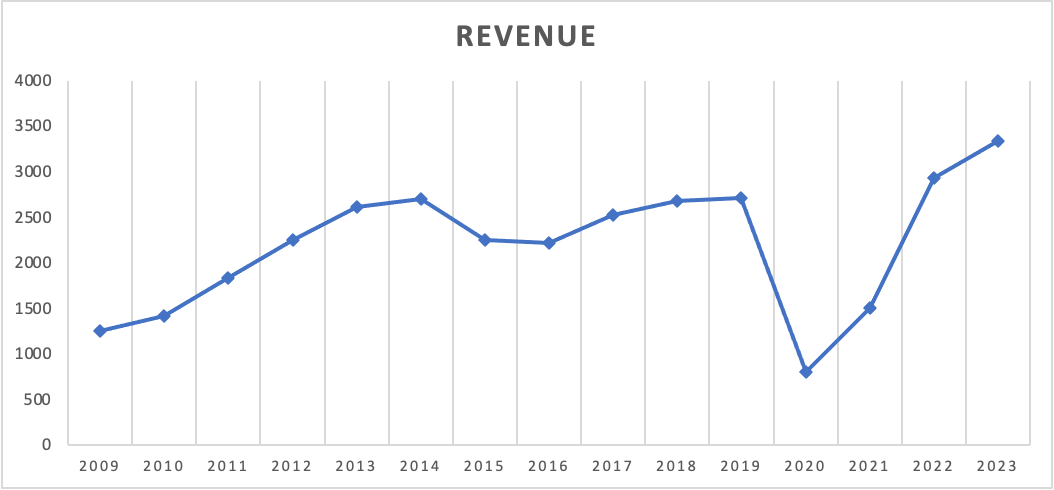

During the span from Q1 2023 to Q2 2023, minimal unexpected shifts were observed. The only significant alterations were in the realm of revenue, wherein the trailing twelve-month [TTM] revenue climbed from $3,219 in Q1 to $3,335 in Q2, representing a growth of 3.6%.

Revenue Evolution (Author's Calculations)

{kind=link}

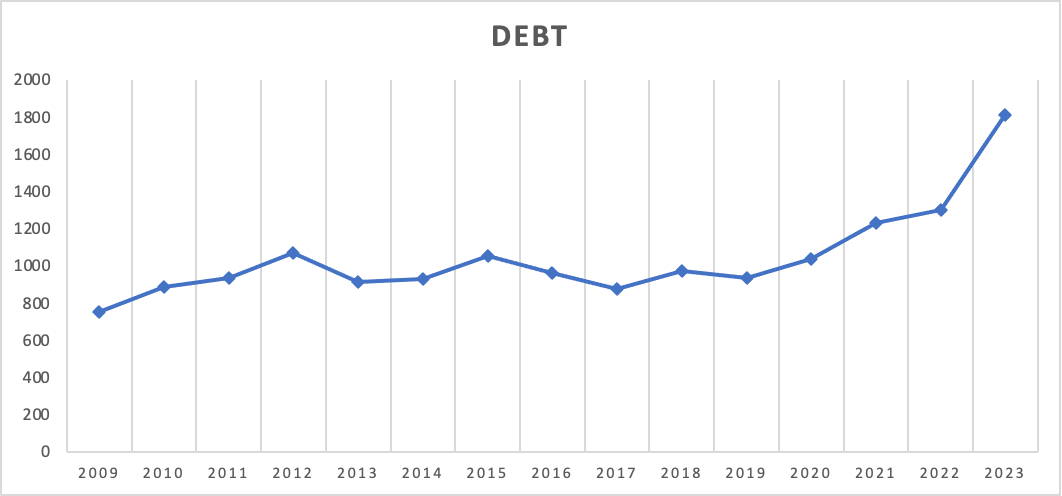

Additionally, there's the matter of debt, which predictably surged by 5.7% from Q1 to Q2. This escalation was, as anticipated, due to the likelihood of ongoing high capital expenditures [CAPEX] and extraordinary expenses until the completion of the aforementioned expansion in 2028.

{kind=link}

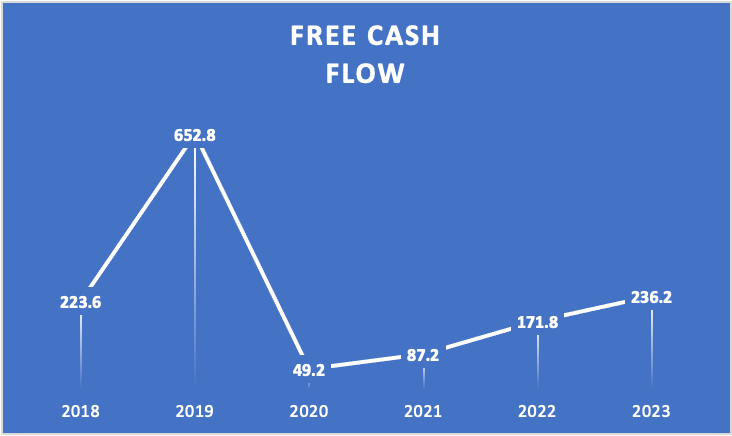

Its free cash flow margin stands remarkably high for an airline, at 7.1%. This figure becomes even more noteworthy when contrasted with the industry's average of approximately 2%. Notably, this metric witnessed a robust 7% increase from Q1 to Q2 2023.

Free Cash Flow components (Author's Calculations) Free Cash Flow Evolution (Author's Calculations)

{kind=link}

{kind=link}

The gross margin in Q1 stood at 38.6%, marking an ascent to 41% in Q2 2023, signaling a notable increase of 2.4%. These positive developments in operational margins on a quarterly basis are primarily attributed to the decline in fuel prices. However, it's prudent to anticipate a return to Q1 margins should oil prices once again fluctuate around the $81 per barrel mark—this possibility hinges on whether they have implemented effective hedging strategies or not.

Turning to the pivotal metrics that warrant everyone's attention: Is Copa Airlines overleveraged due to this expansion?

Currently, its current ratio stands at 0.73, indicating a less-than-optimal condition. However, to gain a comprehensive perspective, we must await the subsequent quarter's results to assess whether this ratio surpasses 1. In Q1 2023, this metric was a healthier 1.1. It's worth noting that in Q2, the need arose to address the $300.9 million long-term debt that reached its maturity and necessitated repayment.

The debt-to-equity ratio has risen to 1.16 from Q1's 1.06. Nevertheless, it remains comfortably below the threshold of 2.00, which distinguishes between manageable conditions and potential challenges. A case in point is United Airlines Holdings, Inc. ( UAL ), with a notably higher debt-to-equity ratio of 4.6 and a current ratio of 0.91. Comparatively, Copa's position is stronger. However, it's important to recognize that UAL's debt-to-equity metric in 2019 was 1.77—a considerably more favorable scenario than today's reality. Yet, it's crucial to consider the unique circumstances during the pandemic's onset, wherein airlines had to secure substantial debt to avert default due to grounded fleets—a situation analogous to the cruise industry's challenges.

In the grand scheme, Copa Airlines emerges as a relatively more promising contender when measured against its peers in the Americas. This favorable positioning is particularly significant, as it signifies that while many of its competitors are grappling with limitations on expansion, Copa is aptly equipped to pursue its growth ambitions.

Valuation (In USD)

To begin, I will present my previously established expectations, which are outlined below:

Previous Table of Expectations (Author's Calculations)

{kind=link}

However, it's crucial for me to address a pivotal aspect of this valuation that I inadvertently overlooked in my prior article: What if Copa were to retire certain airplanes? Would this not potentially lead to reduced future revenue compared to what is presented in this valuation?

The answer to this query lies in the fact that, to the best of my knowledge, Copa has not revealed any intentions regarding the retirement of future aircraft aside from the plan they disclosed in 2020 during the pandemic to retire 14 Boeing 737-700s , and so far they have retired 5 of these airplanes.

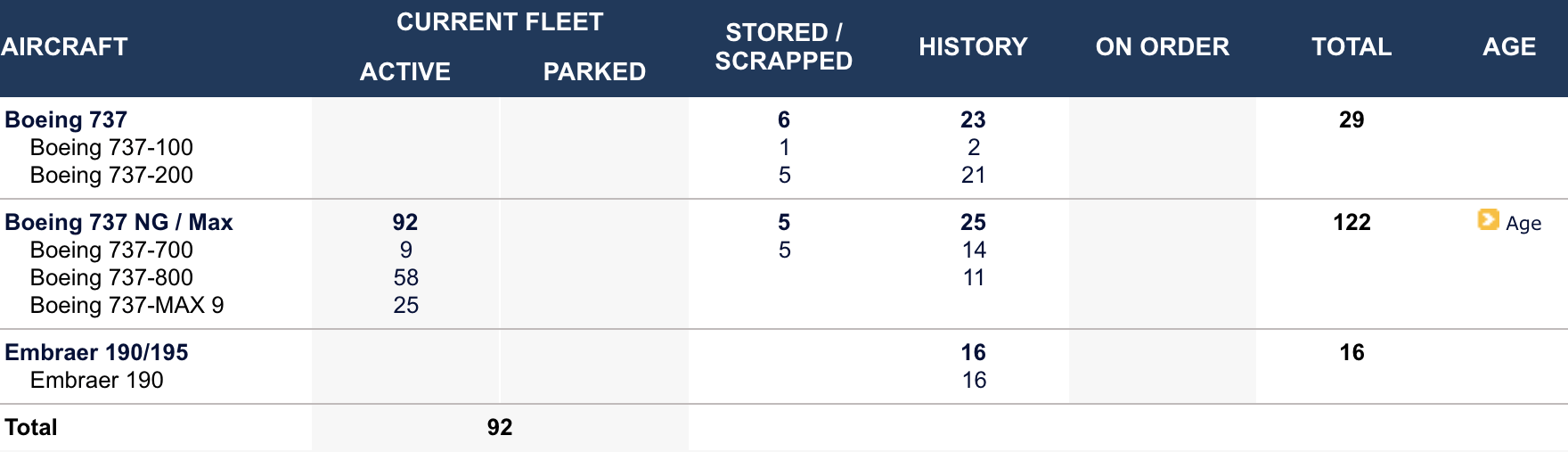

Composition of Copa's Fleet (airfleets.net)

{kind=link}

As of December 31, 2022, we operate a fleet of 97 aircraft , 77 Boeing 737-Next Generation aircraft, 20 Boeing 737 MAX 9 aircraft and one Boeing 737-800 BCF (Boeing Converted Freighter). As of December 31, 2022, the Company has firm orders to purchase 66 Boeing 737 MAX aircraft to be delivered between 2023 and 2028.

Presently, none of these Boeing aircraft remain within Copa's fleet. Additionally, considering that the average age of Copa's current fleet is 9.3 years, the airline still has approximately 15.76 years to capitalize on the opportunities stemming from the impending expansion. This projection assumes that Copa will retire its airplanes around the age of 25. It's worth noting that this retirement age could fluctuate, given that Copa primarily operates shorter-distance flights, thereby potentially preserving the condition of their airplanes more effectively compared to airlines operating longer-haul routes to Europe or Asia. Regardless, any potential downsides for Copa may materialize around 2038 as they initiate the retirement of their existing fleet of 97 airplanes. However, in the medium term, the prospects appear exceptionally promising.

{kind=link}

With this context established, let's delve into the new valuation, which is underpinned by the following updated projections:

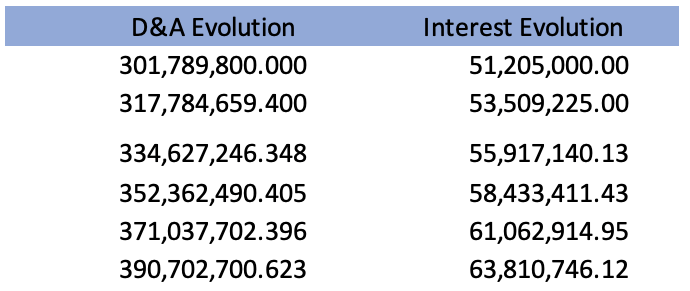

New Expectations (Author's Calculations) D&A and Interest Expenses Projections (Author's Calculations)

{kind=link}

{kind=link}

The revenue projections have been derived using a simple yet somewhat rudimentary method, which may be considered rustic by some. The initial step involves dividing Copa's total revenue by the number of airplanes under its operation. This approach exhibits a negligible margin of error, as Copa's revenue predominantly hinges on the sale of plane tickets. This calculation has yielded an estimated revenue per airplane amounting to $33.3 million, attained by dividing Copa's operational revenue for the year 2022 by the fleet's size of 89 aircraft.

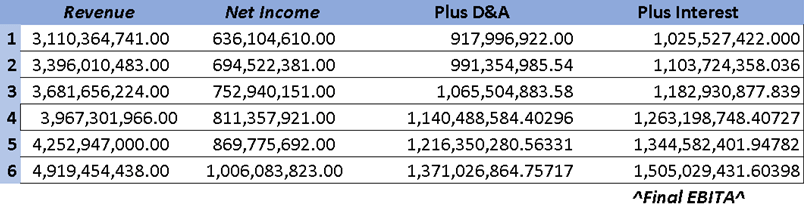

Incorporating the elements of depreciation and amortization (D&A) alongside interest expenses into the model, I have taken into account historical fluctuations. To be precise, I have factored in the average rate of variation spanning from 2009 to 2022. This has resulted in an average annual fluctuation of 5.3% for D&A and 4.5% for interest expenses.

As evident from the provided data, the revenue projections have been elevated. It's important to note that the projections for 2023 and 2024 are no longer based on my own estimates, as I have substituted them with the figures available on Seeking Alpha's "summary tab." This alteration, however, necessitated an overall increase of 9% to each projected revenue figure.

Presented below is the comprehensive DCF model, which incorporates these revised figures:

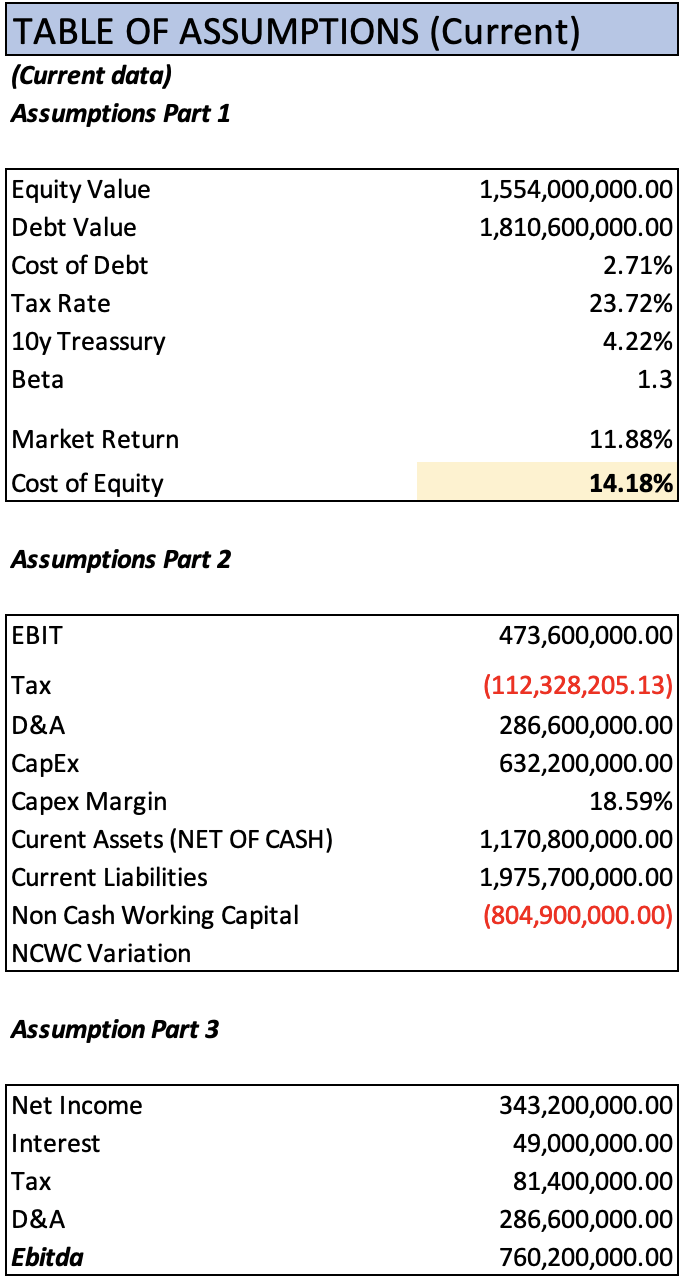

DCF part 1 (Author's Calculations)

{kind=link}

{kind=link}

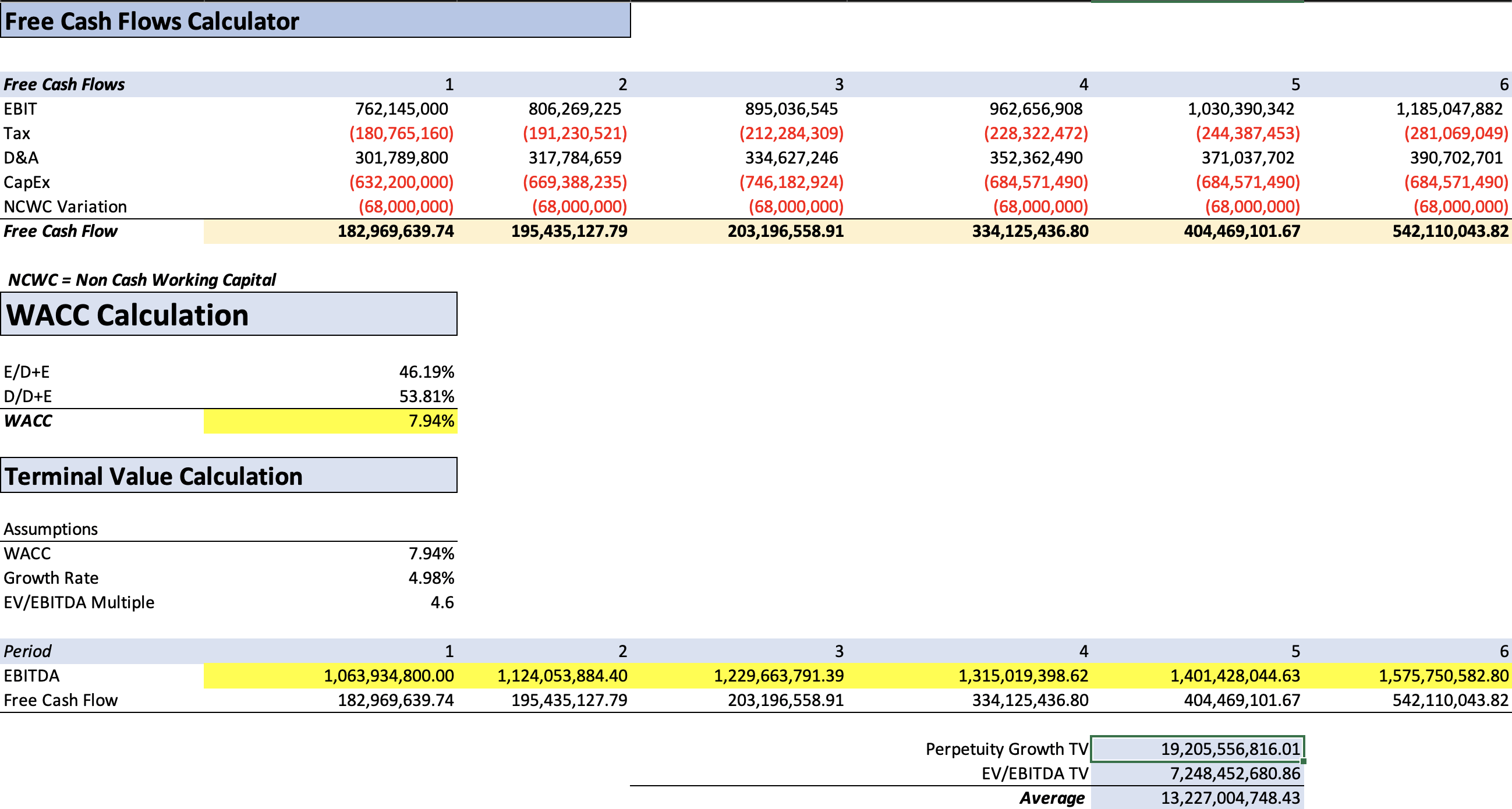

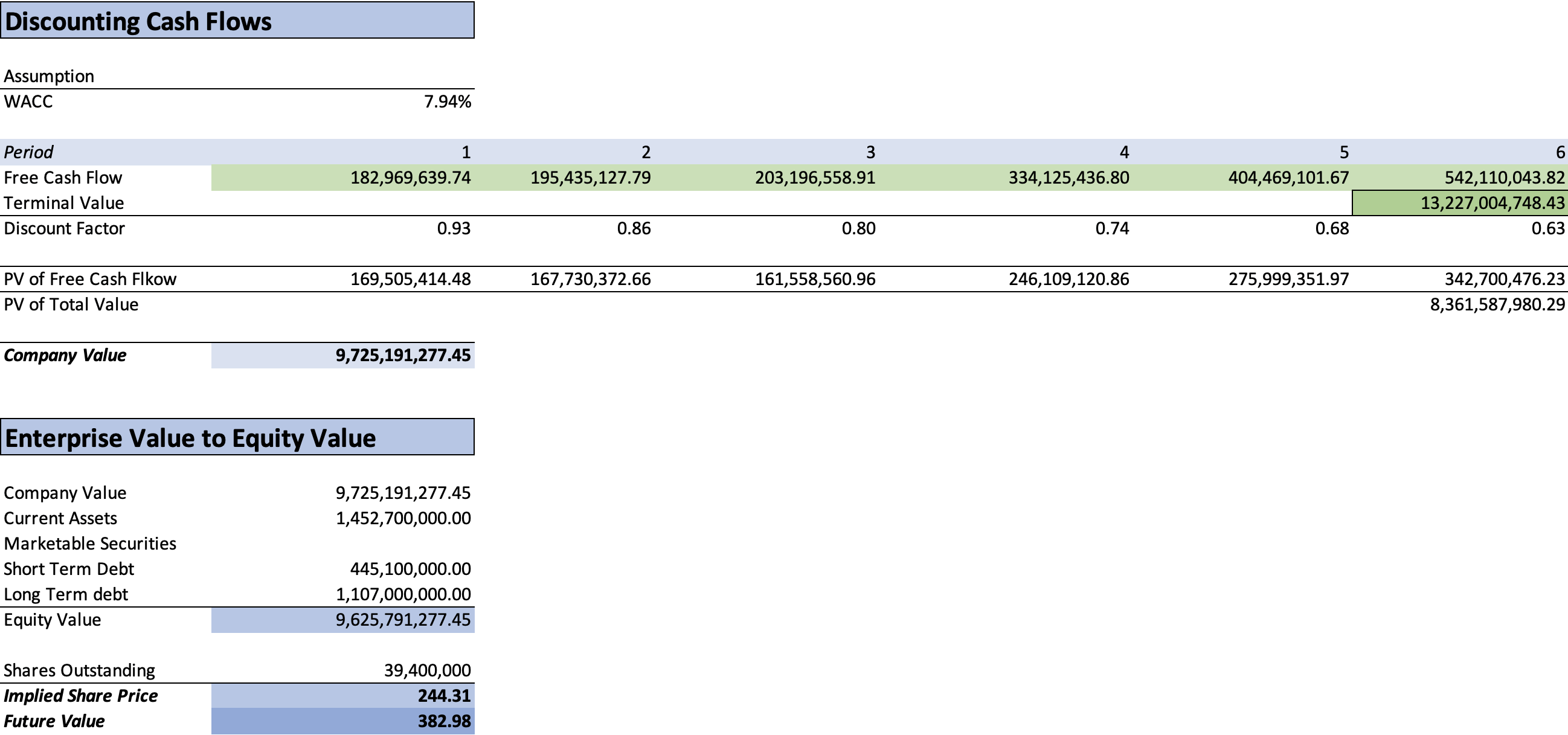

DCF part 2 (Author's Calculations)

{kind=link}

As you can observe, the implied share price stands at $244.31. You might find yourself contemplating a pertinent question: Is a 156% upside potential truly attainable? It's important to consider two factors that play into this assessment. Firstly, this DCF analysis spans a projection horizon of 6 years. Consequently, if we were to truncate this horizon by a year, the resultant price target would inevitably decrease. Secondly, it's crucial to recognize that Copa is still in the nascent stages of its expansion. Despite having placed an order for 66 Boeing 737-Max aircraft, they have received only 4 thus far. This signifies that investors are likely hesitant to assign such a valuation to Copa at this juncture. However, there lies an undeniable truth: if there's a high degree of certainty that Copa will indeed execute its expansion plans as envisioned, then the valuation implied by the DCF analysis undoubtedly merits consideration.

Risks to Thesis

The primary macro risk to this bullish thesis is the potential deterioration of the economic outlook. It's imperative to bear in mind that the feasibility of this fleet expansion hinges on robust travel demand, which provides a substantial economic incentive for Copa's acquisition of these airplanes. However, in the event of a global recession, travel demand is likely to experience a decline. Nevertheless, a closer examination reveals that Copa's primary clientele is situated in the Americas, as the airline does not operate flights in other regions around the world.

Sources of Copa's Revenue (2022 Annual Report)

{kind=link}

Shifting focus to business-related risks, one prominent concern is the potential for overleveraging of Copa's financial structure. This expansion endeavor comes with a considerable price tag, and a review of Copa's cash flow statement dating back to 2013 highlights that capital expenditures have reached an all-time high of $632.2 million. Notably, in 2021, Copa exceeded the milestone of $400 million in capital expenditures for the first time in its history. If the company begins to approach its financial capacity, it's plausible that the expansion could be put on hold. However, this underscores Copa's profound commitment to its long-term sustainability, a favorable trait. This proactive stance is especially commendable in light of the bankruptcy filings made by Aeromexico, Avianca, and LATAM Airlines in the aftermath of the COVID-19 pandemic.

What would be the impact on valuation in the scenario of not acquiring additional airplanes? If the expansion were to be indefinitely postponed, my projection is that the anticipated future revenue of $5.2 billion would decrease to $4.2 billion. Consequently, the projected future value would approximate $259, while the current implied value stands at $174.

This revenue projection is established upon the growth trajectory observed prior to the announcement of the expansion. This growth indicated an annual increase of approximately $100 million. The relatively favorable outcome stems from the fact that, in the event of expansion cancellation, a substantial portion of the present-day Capital Expenditures [CAPEX] would adjust downward from the existing levels of $600+ million to a range of $100-135 million.

Conclusion

In conclusion, our assessment of Copa Airlines reveals a dynamic landscape that intertwines ambitious growth prospects with pertinent risks. The airline's ongoing fleet expansion, driven by robust travel demand and favorable economic conditions, paints an encouraging trajectory for its future. The strategic acquisition of new aircraft is aligned with Copa's commitment to catering to its burgeoning client base in the Americas. However, amidst these favorable prospects, a number of critical considerations come to light.

On the macro level, the potential impact of a deteriorating economic outlook emerges as a significant risk. The viability of Copa's expansion largely relies on sustained travel demand, which could be vulnerable in the face of a global recession. Notably, the bulk of Copa's clients are situated within the Americas, a regional focus that could potentially mitigate some of the fallout from a broader economic downturn.

On the operational front, the prudent management of finances and capital is pivotal. The remarkable capital expenditures required for this expansion underscore the importance of maintaining a balanced financial structure. While the growth opportunities are compelling, the potential for overleveraging is a concern that Copa must navigate with diligence. The company's history of capital expenditures reaching unprecedented levels reflects its proactive approach to investing in its future.

Ultimately, Copa Airlines stands at a pivotal juncture, armed with both potential and prudence. The robust DCF model projections showcase the promising upside that lies ahead, but it's essential to acknowledge that this potential is not without its caveats. Copa's prudent financial management and regional focus, coupled with its dedication to sustainability, provide a solid foundation for its expansion strategy.

In light of the lessons learned from the recent challenges faced by other industry players, Copa's measured approach signifies an earnest effort to avoid the pitfalls that led others astray. As we navigate the intricate interplay of growth aspirations and potential risks, we find ourselves with an airline that has the ambition to soar, the adaptability to face headwinds, and a commitment to secure its place among the industry's leaders.

For further details see:

Copa Holdings: A Continuation Of Opportunity, Reiterate Buy