CPA - Copa Holdings: Achieving Stable Annual Return With Potential For Further Expansion

2023-06-06 13:29:48 ET

Summary

- Copa Airlines is projected to double its revenue by 2028 through an expansion plan involving the addition of 66 more airplanes to its fleet.

- The intrinsic value of the stock indicates a price target of $159 by 2028, with potential to reach as high as $209 if forward multiples are considered.

- Despite potential risks such as a recession, Copa's strong financial position, conservative fiscal policy, and exceptional management make it a promising long-term investment.

Thesis

Copa Holdings, S.A. ( CPA ), as a highly liquid and well-managed top Latin American company, is poised to benefit from the recovery in travel. I project that Copa will be able to double its revenue by 2028, which involves adding 66 more airplanes to its fleet, resulting in a total fleet of 155 planes. Through a Discounted Cash Flow Model, I have calculated the intrinsic value of the stock, indicating a price target of $159 by 2028. This estimation assumes a secure annual growth rate of 10% and does not account for the potential impact of forward multiples such as P/E. If we include such factors, the stock could potentially reach as high as $209 by 2028.

Company Overview

History

Copa Airlines was founded in 1947, and initially operated domestic flights in Panama and gradually expanded to international destinations. In the 1960s, it introduced flights to cities such as San José, Kingston, Barranquilla, and Medellín. By the 1980s, Copa Airlines had acquired Boeing 737 aircraft and expanded its network to include various destinations in the Americas. In 1992, it established a hub at Panama's Tocumen International Airport, connecting flights within Latin America. In 1998, Copa Airlines modernized its fleet and formed a strategic alliance with Continental Airlines (today, United Airlines). Subsequent years witnessed further expansion, acquisitions, and membership in alliances such as SkyTeam in 2007 and Star Alliance in 2012.

However, in 2020, Copa, like many other leisure companies, faced challenges as its customers stayed at home and international travel came to a halt. Its revenue slumped by over 70%, causing difficulties as maintaining planes is expensive.

Nevertheless, thanks to its strong financial position and conservative fiscal policy, Copa managed to recover and maintained considerably lower leverage compared to its competitors.

At the start of 2023, Copa's pilots were on the verge of a strike due to the loss of purchasing power during the pandemic. However, on February 2, just hours before the strike was scheduled to take place, Copa reached a deal with its pilots, offering them increased compensation and bonuses, leading to the cancellation of the strike .

Copa's plan is to continue expanding, and they are currently working on adding 66 Boeing 737-MAX aircraft to their fleet, bringing the total to 155. You may wonder about retiring planes. Based on my calculations, the retirement of planes is expected to commence in 2033, as their Boeing 737 Next Generation aircraft (launched in 1998) reach their lifespan of 35 years. Therefore, it is safe to predict that Copa will achieve impressive numbers until 2033. However, after 2033, I predict that the decline in passenger revenue may occur as their older generation planes begin to retire.

We operate a modern fleet. Our fleet consists of Boeing 737-MAX and Boeing 737-Next Generation aircraft equipped with winglets and other modern cost-saving and safety features. Over the next several years, we intend to enhance our modern fleet through the addition of 66 Boeing 737 MAX aircraft to be delivered between 2023 and 2028.

- 2022 Annual Report

Market

Copa Airlines is the sole Panamanian airline that operates international routes, including destinations in the USA, Canada, all of Central America, all countries in South America except for the Guianas, and the Caribbean. Within the Americas, Copa enjoys a highly favorable market position due to its membership in the Star Alliance. This affiliation shields Copa from detrimental competition posed by United Airlines Holdings ( UAL ) and Avianca Holdings S.A. (Recently emerged from bankruptcy ), which I would consider as their two most significant threats should this alliance be disrupted. Consequently, with every route from Panama to other parts of the Americas requiring a connection through Copa, American Airlines Group ( AAL ) remains the sole formidable competitor to Copa, since other airlines such as AeroMexico , and Latam Airlines filed for bankruptcy during the Pandemic, meaning they are in poor financial position to compete with Copa. As additional information, you can see which markets are the most important for Copa in relation to their revenue:

Weight of Regions in Copa's Revenue (Anual Report 2022)

{kind=link}

Ecosystem Inside Panama

Copa Holdings, is connected to a group of businesses founded by the same entrepreneurs who established Banco General S.A., the largest bank in the country. This group includes other companies like Empresa General de Inversiones S.A., which owns Empresa General de Petróleos, and Empresa General de Capital. The latter is responsible for importing hydrocarbons for Empresa General de Petróleos.

These companies share common ownership and represent just a few examples of the extensive business portfolio established by the founders. They have also ventured into shopping malls, media companies like TVN, liquor stores under Felipe Motta, an import company called Motta International, and online stores like iShop, which serves as an Apple distributor in Panama.

While Copa Holdings does not necessarily own these businesses, it can be considered as "part of a conglomerate" because it was founded by the same individuals who established these diverse enterprises. This situation provides Copa Holdings with significant advantages in Panama. For example, it can access financing through Banco General, import fuel through Empresa General de Capital, run TV advertisements through TVN, and so on.

Given this close relationship, it is not unlikely that Copa Holdings may enjoy special advantages or preferential treatment, which by itself is an economic moat in Copa's home country. It is natural for business owners to leverage their other enterprises to benefit their own company.

Financials (In Millions)

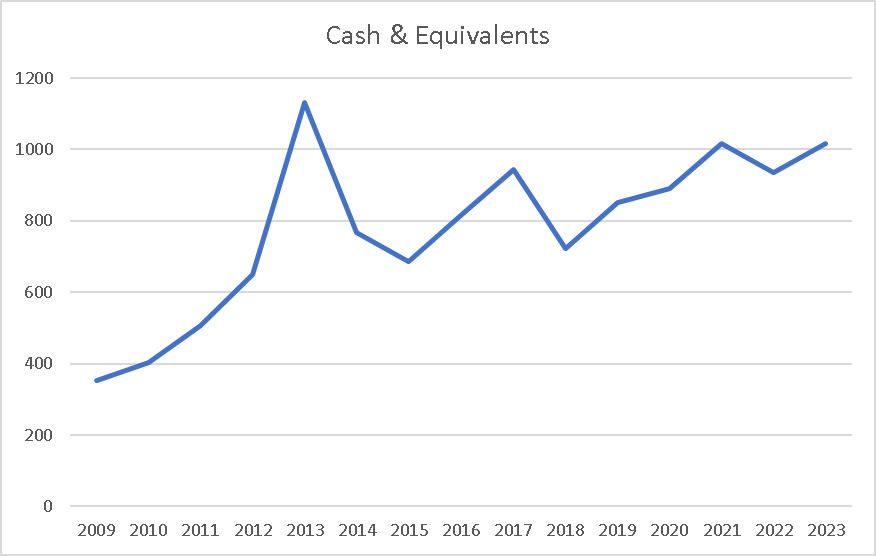

Copa not only is a growth company, but it offers a nice 3% dividend, therefore I would like to highlight Copa's remarkable achievement in growing its cash balance, which has shown minimal decrease even during the pandemic. Since 2009, Copa has achieved an annual cash balance increase of 12.5%. This aspect is vital to define Copa's dividend payment capacity.

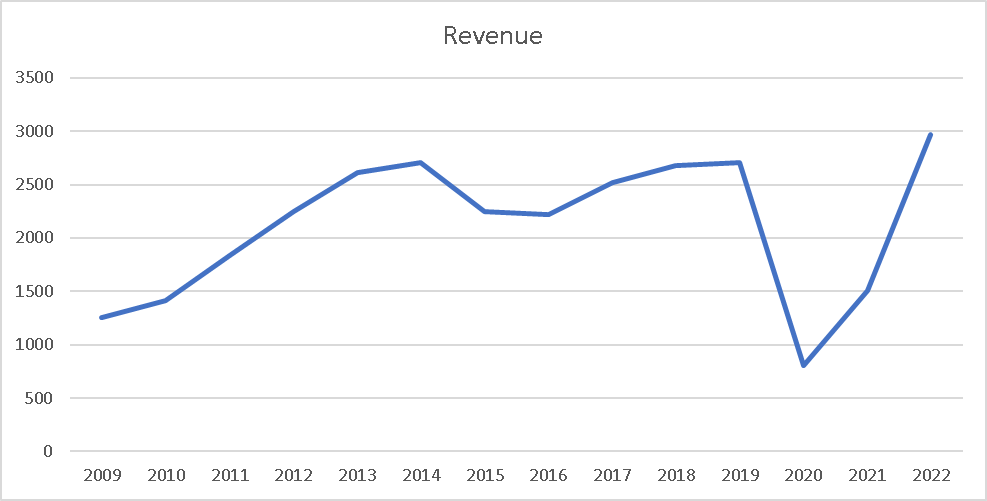

Cash & Equivalents Evolution (Author's Calculation) Revenue Evolution (Author's Calculation)

{kind=link}

{kind=link}

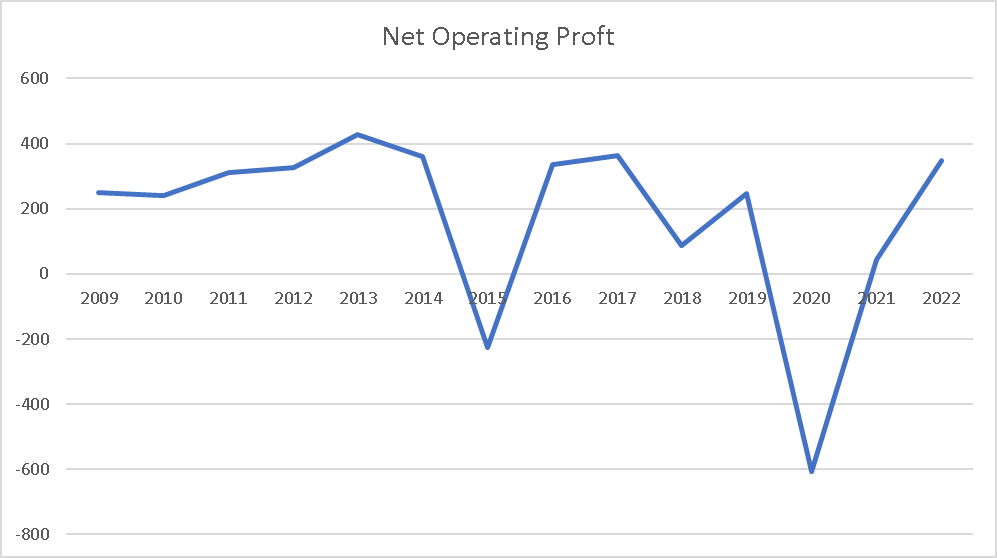

The revenue has experienced substantial growth, but most growth occurred between 2009 and 2013, after which revenue growth stagnated. As a result, the stock price began to decline after 2014. In contrast to stability observed in revenue, the Net Operating Profit has never surpassed the $500 million mark. In my opinion, this indicates the threshold at which Copa will start utilizing its profits for reinvestment purposes. It doesn't take much time to understand why: Copa is an expanding business that remains focused on growth. Consequently, they often utilize their profits for reinvestment. However, I believe, they excel at avoiding excessive investment that could potentially jeopardize their financial stability, even when faced with minor challenges, such as what was previously said about Latam, Avianca, and AeroMexico. Overall, the key takeaway is that with a larger fleet and increased revenue, Copa has the potential to expand at a faster pace. This is because they would only utilize the amount exceeding $500 million for reinvestment. Additionally, having a larger pre-investment profit, thanks to the expanded fleet, provides them with more resources to support their growth initiatives.

Net Operating Profit Evolution (Author's Calculation)

{kind=link}

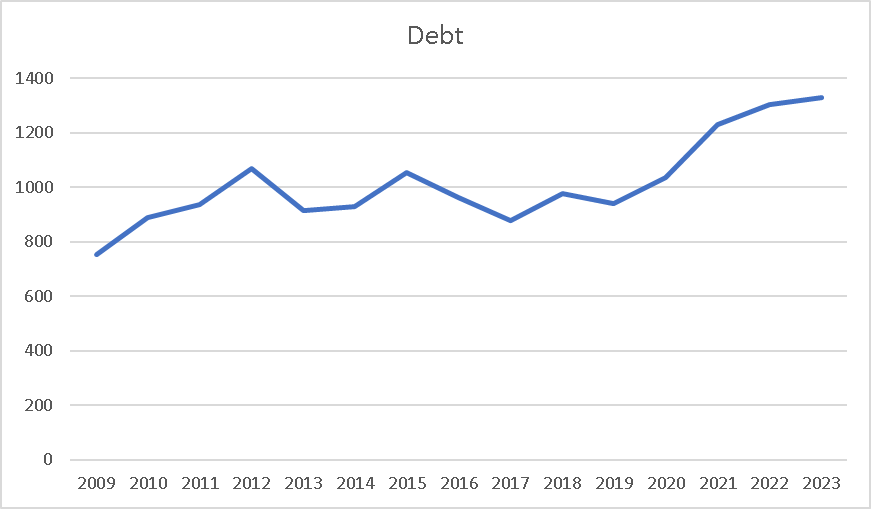

This expansion has brought a debt that began to increase after 2019 when the pandemic struck, and the 66 Boeing 737 Max aircraft started to be delivered. Prior to that, the debt remained relatively stable or flat, emphasizing the financial responsibility of the management team.

Debt Evolution (Author's Calculation)

{kind=link}

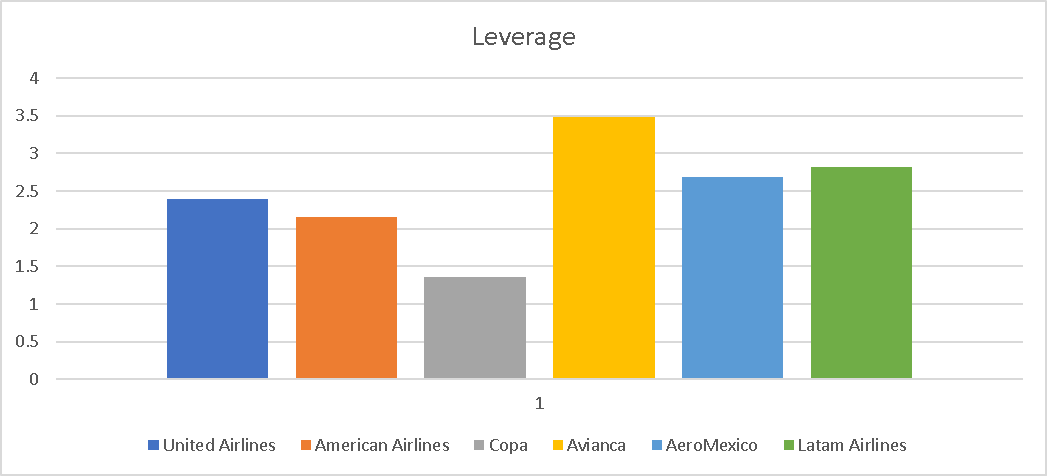

Furthermore, when it comes to debt, I have included a graph that compares Copa's leverage to that of other major airlines operating in the Americas. This graph highlights why Copa was able to recover faster than its counterparts and avoid bankruptcy, unlike AeroMexico, Avianca, and Latam, however I need to point out that this isn't new data, as Copa expands, the leverage could increase to that of United's, but with the current leverage of Copa, in my opinion, there is plenty of room for that and will not affect Copa's future viability.

Leverage (Author's Calculation)

{kind=link}

Overall, I see that Copa's financials do not offer anything particularly noteworthy. The company operates in a conservative manner, and as a result, its indicators do not reveal anything exceptional for a growing company.

Valuation (Every Number is Expressed as it is)

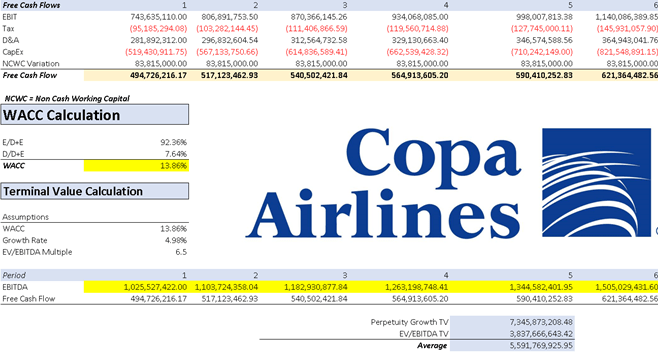

In order to value Copa Holdings, I utilized a DCF Model with a primary focus on predicting the impact of adding 66 new Boeing 737 Max planes to Copa's fleet, a process scheduled for completion in 2028, and this expansion is the one that, in my opinion, will double Copa's revenue.

To mitigate any potential inconveniences during the delivery of these new planes, I constructed the model assuming Copa will receive 9 planes annually from 2023 to 2028.

To determine the projected earnings for each airplane, I divided the operating revenue of $2.965 billion (from Copa's 2022 Annual Report) by the total fleet size of Copa Airlines as of 2023, which is 89 airplanes. This calculation yields a revenue of approximately $33.3 million per plane. Consequently, projecting the revenue until 2028 is straightforward since Copa's Statement of Income encompasses only Passenger Revenue, Cargo and Mail Revenue, and Other Operating Revenue.

Operating Revenue (Annual Report 2022)

{kind=link}

Then, to calculate the expenses, I employed a similar approach, dividing the total expenses by each airplane. Since Copa's revenue relies heavily on passenger revenue, their expenses are predominantly linked to the aircraft. Based on this analysis, I estimated expenses to be approximately $25 million per plane.

However, it's important to acknowledge a flaw in this rough calculation. It assumes that the exceptional fuel expenses incurred during the current period will persist in the future. We know that a fuel price of $100 per barrel is not likely to become the new normal. In fact, it is expected to decrease, either due to a recession or through political maneuvering, as high energy prices primarily benefit the producers. Nevertheless, this flaw acts as a cushion, accounting for potential errors in the DCF analysis.

Regarding depreciation and amortization (D&A) as well as interest expenses, I incorporated historical variations into the model. Specifically, I considered the average variation between 2009 and 2022, resulting in an average annual variation of 5.3% for D&A and 4.5% for interest expenses.

D&A, and Interest Expenses Projections (Author's Calculation)

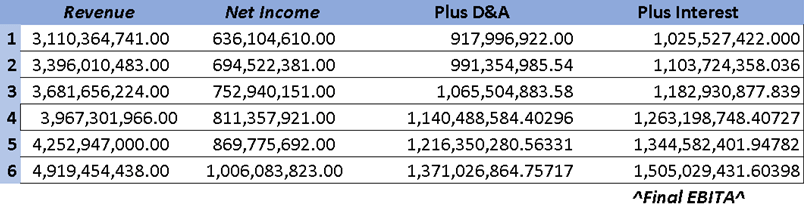

Below is a table presenting the complete projections. It is important to clarify that the net income is stated before taxes, hence there was no need to include a "plus taxes" column. Additionally, the revenue column is included solely for display purposes and was not factored into the EBITDA calculation.

Projections of EBITDA (Author's Calculation)

{kind=link}

Now, here is the table of variables for the DCF model. I believe there is no need for further explanation as it simply presents the data that anyone can extract from the 2022 Annual Report.

Table of Assumptions (Author's Calculations)

Then the complete DCF model:

DCF Part 1 (Author's Calculation)

{kind=link}

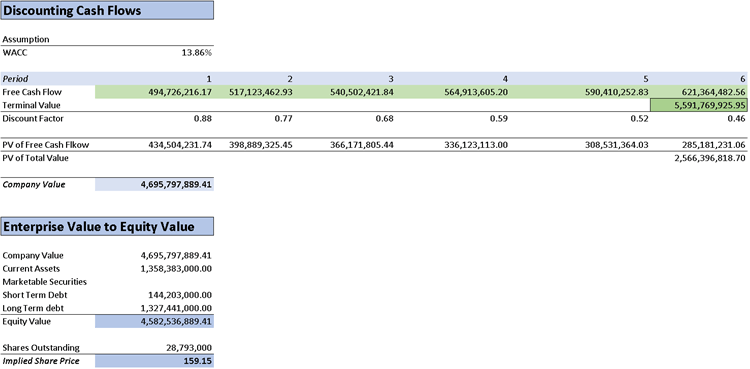

DCF Part 2 (Author's Calculation)

{kind=link}

Finally, the DCF analysis yields an implied stock price of $159, assuming a 10% annual return. However, it is important to note that this target does not account for the P/E ratio. To speculate further, I would suggest that in 2028, Copa's stock could be trading at a P/E ratio of 6. This would imply a stock price of $209, providing a potential 15% annual return.

Furthermore, considering that Copa currently operates with a fleet of 155 planes, there is still ample room for future expansion before reaching the size of United Airlines' fleet, which exceeds 800 aircraft.

Risk to Thesis

In my opinion, the primary risk for Copa in the near term lies in the potential occurrence of a recession, which could result in a decline in passenger revenue. This scenario presents challenges for Copa, especially concerning the fulfillment of their order for 9 planes. However, it is important to highlight that Copa has already demonstrated its ability to navigate through the challenges posed by the pandemic, showcasing resilience and adaptability. Thus, even in the face of a recession, Copa has proven its capacity to overcome adversity.

That being said, I must acknowledge that my optimistic view of Copa in the near term may require reevaluation if a recession occurs. Nevertheless, I maintain a highly positive long-term outlook for the company, as it continues to shine brightly within the industry.

It is also worth noting a crucial aspect about the airline industry. Operating aircraft is an expensive endeavor, and customer loyalty tends to be relatively low (hence the implementation of loyalty programs and miles). Moreover, the industry as a whole is capital-intensive.

Conclusion

Copa Holdings is distinguished by exceptional management, led by highly experienced Panamanian businesspeople. Under their guidance, Copa has emerged as one of Latin America's standout companies, reflecting its status within emerging markets.

With a solid financial foundation, Copa is well positioned for future growth. The forthcoming delivery of the 66 Boeing 737-MAX aircraft order will propel the company towards doubling its revenue by 2028. This growth trajectory is projected to elevate Copa's stock price to a range between $159 and $205, providing annual returns of 10% to 16% to shareholders. These targets are already conservative, and it would not be surprising if Copa surpasses these projections and achieves an even higher stock price by 2028. However, it is important to note that in the event of a recession, the near-term outlook may face challenges, but it is unlikely to significantly impact the long-term prospects.

Copa Airlines will continue to expand its network of destinations and enhance flight connections, further solidifying its position as a major player in the regional airline industry.

For further details see:

Copa Holdings: Achieving Stable Annual Return With Potential For Further Expansion