CPA - Copa Holdings: Streamlined Strategy Strengthening Its Industry Position

2023-10-24 04:43:31 ET

Summary

- Copa Holdings' strategy of fleet modernization, destination expansion, and hub enhancement for Copa Airlines aligns with industry growth trends.

- Copa Holdings' single aircraft type and hub strategy significantly boost operational efficiency and reduce costs.

- Copa Holdings' streamlined operations yield high operating margins, reflecting financial stability and competitive advantage in the industry.

- Discounted cash flow analysis forecasts a steady growth for Copa Holdings, with a potential return of around 12% per year over five years.

Investment Thesis

I believe Copa Holdings (CPA) stock is a hold. Copa Holdings, through its key subsidiary, Copa Airlines, has strategically positioned itself for substantial growth and financial stability by aligning its operations with the prevailing industry growth trends. The cornerstone of its strategy hinges on fleet modernization, destination expansion, and hub enhancement, which not only resonates with the broader market dynamics but also sets a trajectory for sustainable growth. A notable facet of this strategy is the airline's singular focus on operating a single type of aircraft and centralizing operations around a major hub. This operational model significantly enhances efficiency, trims operational costs, and propels the profitability of each flight, as reflected in the robust operating margins of 24% and 22% in consecutive quarters of 2023. Such margins are a testament to the airline's financial prowess, giving it a competitive edge in the fiercely competitive aviation industry. Moreover, a Discounted Cash Flow [DCF] analysis foresees a steady growth trajectory for Copa Holdings, projecting a potential Compound Annual Growth Rate [CAGR] of around 12% over the next five years. This reflects a promising outlook for Copa Holdings, underlining the efficacy of its streamlined operational model in navigating the intricacies of the aviation sector.

Company Overview

Founded in 1947 in Panama City, Copa Holdings, S.A., through its primary subsidiary Copa Airlines, has emerged as a leader in the Latin American aviation landscape. The acquisition by Corporación de Inversiones Aéreas, S.A. [CIASA] in 1986 and the subsequent formation of Copa Holdings in 1998 marked significant milestones in the company’s journey. By 2005, the company strategically acquired AeroRepública, a leading Colombian carrier, and introduced Wingo, a low-cost flight model. This commitment to growth and customer service was further underscored in 2015 with the launch of its loyalty program, ConnectMiles, and a joint business agreement with United Airlines (UAL) and Avianca (AVH).

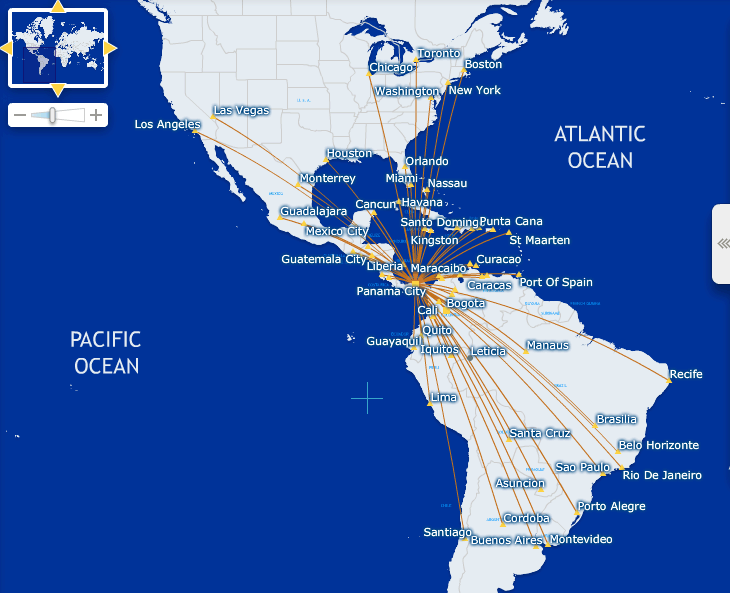

Today, Copa boasts a fleet of 101 aircraft, with plans to add 66 Boeing 737 MAX aircraft by 2028. Operating from its strategically located "Hub of the Americas" in Panama City, the airline connects 81 destinations across 33 countries, offering around 327 daily flights. Its alliance with Star Alliance and a partnership with UAL further enhances its market position. Renowned for its cost efficiency, modern fleet, and an impressive on-time performance rate of 87.5%, Copa's ethos revolve around teamwork, customer-centricity, and continuous improvement. Despite fierce competition from airlines such as LATAM Airlines Group (LTMAY) and Aeromexico, Copa's commitment to excellence has ensured its prominent place in the Latin American aviation sector.

Committed to Expansion to Maximize Industry Tailwinds

Copa Holdings, through its primary subsidiary Copa Airlines, is ambitiously advancing its operations across the Americas, aligning its strategy with the notable industry growth and demographic shifts observed in the region. This strategy is anchored on three main pillars: modernizing the fleet through acquiring new aircraft, expanding the destination roster, and enhancing the central hub facilities at Tocumen International Airport.

As part of this robust strategy, Copa Airlines has invested significantly in modernizing its fleet, epitomized by the $2.1 billion investment in 15 Boeing 737 MAX aircraft . This acquisition not only symbolizes the airline's resilience in bouncing back from the COVID-19 pandemic-induced challenges but also its foresight in capitalizing on the opportunities presented in the post-pandemic recovery phase. The modernized fleet, currently with 101 aircraft , is designed to drive greater operational efficiency, reduce operational costs, and potentially unlock new routes that were previously unfeasible due to aircraft limitations.

{kind=link}

When it comes to geographical expansion, Copa Airlines has been proactive in broadening its network to meet the evolving market demands. In the first quarter of 2023 alone, the airline added three new destinations: Baltimore, Austin, and Manta in Ecuador, followed by announcing the commencement of a new service to Barquisimeto, Venezuela in Q2, extending its network to an impressive 81 destinations across 33 countries in the Americas. This expansion strategy significantly strengthens Panama's 'Hub of the Americas,' providing travelers with a wider range of flight options and connections, thereby solidifying its position as a premier choice among its regional counterparts.

{kind=link}

At the heart of its operations, significant upgrades at Tocumen International Airport are underway. Investments in a new terminal to increase capacity and improved facilities like the Copa Club lounge are aimed at elevating the overall passenger experience. These enhancements are not merely about immediate passenger satisfaction but are a long-term strategy to position the company favorably to harness the favorable industry and demographic trends, particularly in the medium to long term as the market recovers post-pandemic.

The broader Latin American aviation market outlook further complements Copa Airlines' ambitious expansion plans. The market is on a promising recovery trajectory, with passenger traffic levels returning to pre-pandemic numbers as of December 2022. The year 2023 is expected to witness a 9.3% growth in passenger demand, and the market size is projected to burgeon from $38.93 billion to $45.20 billion by 2028 . Furthermore, the International Air Transport Association [IATA] has forecasted that passenger numbers in 2023 will surpass those from 2019, particularly with a 102% surge in Central America, which underscores the resurgence of international tourism.

However, despite these promising trends, I think it is important to consider that challenges such as the political landscapes in countries like Chile and Colombia, rising fuel prices, and global inflation remain as short-term hurdles. Yet, the overarching growth trajectory across the North and South American aviation market continues, offering a favorable backdrop for Copa Airlines to leverage these industry tailwinds.

The demographic shifts, characterized by increased movement between North and South America, further underline the strategic importance of Copa Airlines' market adaptation. The airline's expansive network and partnerships with other airlines are well-poised to tap into the increasing travel demand, thereby enhancing its connectivity across the continents.

Streamlined Operations which Maximize Efficiency

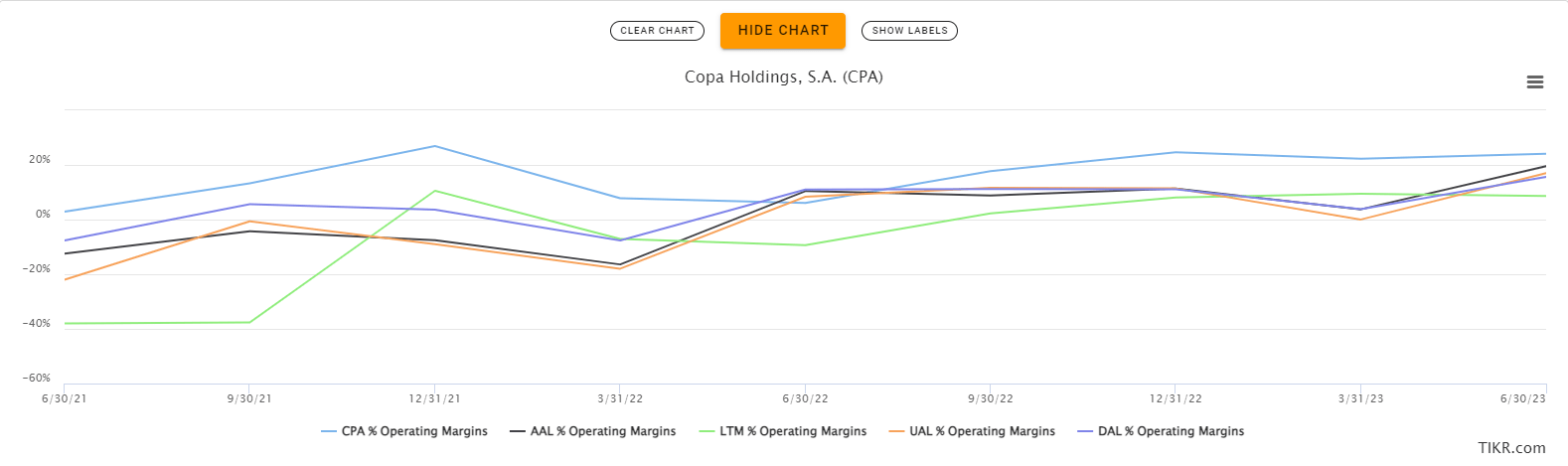

In my recent American Airlines (AAL) article , I stated that the stock was a sell, mentioning how the company has substantial fixed expenses such as aircraft financing, crew salaries, and airport fees that remain constant, regardless of how many passengers they serve. I believe in the case of AAL, it's particularly pronounced due to the size of their operations but also because the company operates out of many airports and operates many different aircraft types. In my opinion, the approach of Copa Holdings, through Copa Airlines, mitigates many of the factors affecting major airlines such as American Airlines and LATAM by streamlining operations to a single aircraft type and one major hub.

In my opinion, the strategy employed by Copa Airlines of operating with a single type of aircraft, the Boeing 737, and consolidating operations around a singular hub significantly drives operational efficiency and cost reduction, setting a commendable example in the aviation industry. The essence of utilizing a single type of aircraft lies in the simplification it brings to both maintenance operations and the management of airport turnaround times. As ground staff become adept with routine tasks due to the uniformity of the aircraft, operational efficiency is naturally bolstered. Furthermore, the streamlined nature of maintenance operations, devoid of the need for stocking diverse parts or training personnel for multiple aircraft types, not only curtails time consumption but also slashes operational expenses substantially. Alongside, the hub-and-spoke system, characterized by a central hub, minimizes the number of routes and aircraft in operation, thus optimizing resource utilization. This system inherently requires fewer routes compared to the point-to-point model, hence reducing the operational complexities that come with managing multiple hubs and diverse routes.

The cost reduction achieved through this operational model directly propels the profitability of each flight operated by Copa Airlines. This cost-saving strategy is markedly reflected in the airline's robust operating margins, which are impressive for an airline business. For instance, the exceptional operating margins of 24% and 22% reported in the second and first quarters of 2023 respectively, the highest of any airline , serve as a testament to the financial prowess and stability emanating from such a streamlined operational model. These figures not only eclipse many global counterparts but also underscore the competitive advantage Copa Airlines holds over peers, particularly in a fiercely competitive industry.

{kind=link}

The exemplary operating margins are a direct reflection of the financial stability and efficiency that Copa Airlines enjoys, largely attributable to its streamlined operations and cost-saving strategies. In a nutshell, by adhering to a business model underscored by operational simplicity, Copa Airlines has not only navigated the intricate operational and financial challenges prevalent in the aviation industry but has also positioned itself for greater financial performance.

Financial Analysis

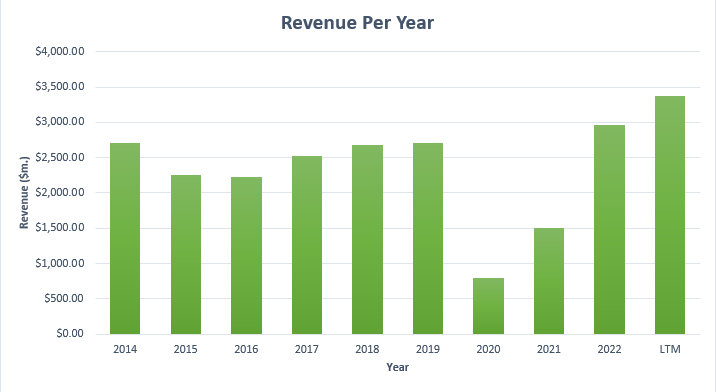

As of 2023, Copa Holdings has demonstrated a solid financial performance. In my opinion, the growth in revenue from $2.68 billion in 2018 to $3.38 billion in the last twelve months [LTM] has been solid, despite the obvious decline it experienced during the COVID years and the cyclical nature of the airline industry. This growth corresponds to a CAGR of approximately 4.8%.

{kind=link}

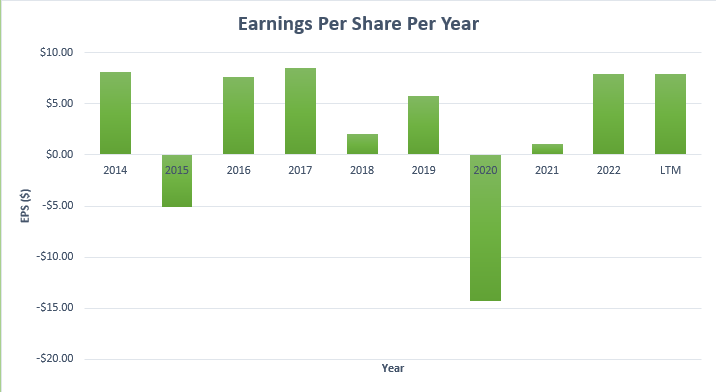

The Earnings Per Share [EPS] has also been rather impressive considering the adversity the airline industry has experienced over the past few years. The EPS has reached $7.93 LTM up from $2.08 and -$14.28 in 2018 and 2020 respectively.

{kind=link}

While the company's Book Value Per Share [BVPS] has declined compared to $42.30 in 2018, it has seen steady growth since 2020 where it collapsed to $30.19 and now stands at $39.42 LTM. This trend suggests to me that Copa Holdings has been effective in augmenting its intrinsic value since the pandemic collapse and I hope to see this continue.

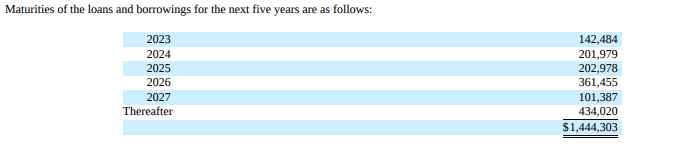

On the liquidity front, the company has cash and cash equivalents amounting to $281 million; however, it currently holds debt of approximately $1.81 billion. It is worth noting, however, that this debt is reasonably distributed across the coming years with most of the company’s debt not due until 2026 or later. I believe that based on current income levels, CPA should have sufficient capital to comfortably service this debt.

{kind=link}

Looking forward, as long as the global economy remains robust and travel demand remains, I believe CPA will continue to post strong growth. In the event of economic downturn, I anticipate travel demand will plummet as it has done it the past which will significantly impact the business of Copa Holdings. That being said, I believe that, in the event of a downturn, CPA will be able to better manage the headwinds due to their lower operating costs and superior operating efficiency and will likely come out of any crisis stronger than most of their competitors.

Valuation

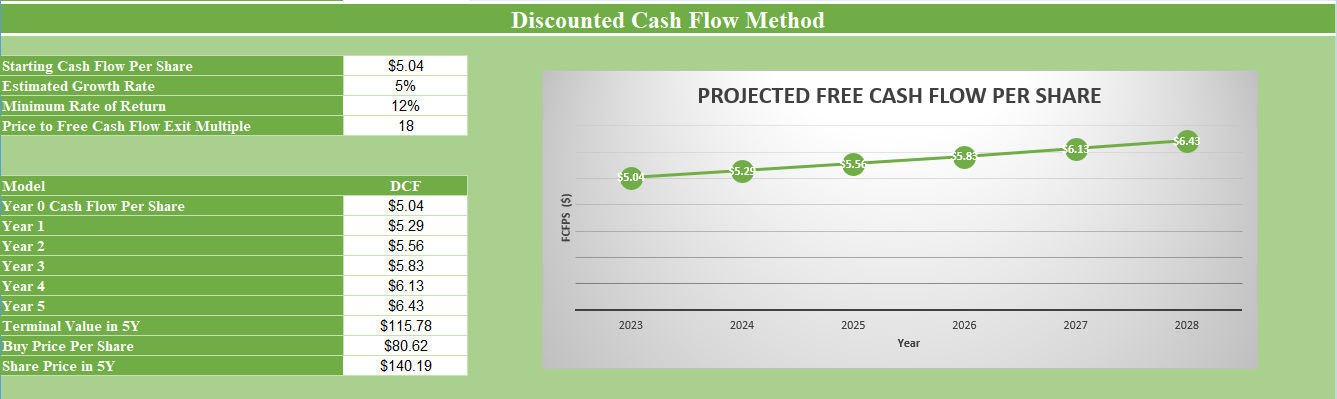

For my valuation of CPA, I have opted to use a DCF analysis as I believe valuation should encompass a comparison between the market capitalization and the foundational business metrics, inclusive of future earnings projections. As of now, the LTM Copa Holdings’ free cash flow [FCF] per share stands at $5.05. I project an annual growth rate of 5% for Copa Holdings' FCF per share over the forthcoming five-year span. Factoring in this growth, the anticipated cash flow per share for Copa Holdings by Q2 2028 is forecasted to be $6.43.

Employing an exit multiple of 18, predicated on what has been reasonable for Copa Holdings amid a stable economic backdrop and FCF generation over the preceding decade, the price target for the stock in five years aggregates to $140.19. Therefore, should you invest in Copa Holdings at its present share price, the anticipated CAGR would be around 12% over the ensuing five years. While a reasonably attractive return, in alignment with my individual investment principles, I aim for a minimum anticipated rate of return of 15%. This threshold is pivotal as it makes the intrinsic risks tied to investing in individual stocks more tolerable, particularly when contrasted with the broader market exposure provided by index investments.

{kind=link}

Conclusion

Copa Holdings has strategically positioned itself for substantial growth and financial stability by aligning its operations with the prevailing industry growth trends. The cornerstone of its strategy hinges on fleet modernization, destination expansion, and hub enhancement, which not only resonates with the broader market dynamics but also sets a trajectory for sustainable growth. A notable facet of this strategy is the airline's singular focus on operating a single type of aircraft and centralizing operations around a major hub. This operational model significantly enhances efficiency, trims operational costs, and propels the profitability of each flight, as reflected in the robust operating margins of 24% and 22% in consecutive quarters of 2023. Such margins are a testament to the airline's financial prowess, giving it a competitive edge in the fiercely competitive aviation industry. Moreover, a Discounted Cash Flow [DCF] analysis foresees a steady growth trajectory for Copa Holdings, projecting a potential CAGR of around 12% over the next five years. This reflects a promising outlook for Copa Holdings, underlining the efficacy of its streamlined operational model in navigating the intricacies of the aviation sector.

For further details see:

Copa Holdings: Streamlined Strategy Strengthening Its Industry Position