CPRT - Copart: A Top-Tier Compounder I'm Buying On Weakness

2023-10-03 17:32:44 ET

Summary

- Markets are in turmoil with rising rates and weakening economic growth, causing the underlying economy to suffer.

- Copart, an industrial stock, offers attractive buying opportunities with its double-digit EPS and sales growth, unique business model, and strong flow of new customers.

- CPRT has a history of impressive revenue growth, a healthy balance sheet, and has outperformed the S&P 500 with a return of over 953% in the last decade.

Introduction

Markets are in turmoil. Rates are rising, economic growth is weakening, and the Fed remains hawkish. That's a horrible mix for investors. So far, the market is still up 11.5% year-to-date, which means the average investor should still be doing all right this year.

The problem is that the mix of headwinds I just listed is causing the underlying economy to suffer.

For example, credit, the core of our capitalist economies, is showing cracks.

Not only are big banks increasing loan loss reserves, we're also seeing increasing delinquencies. Credit card and auto loan delinquencies are at multi-decade highs. Mortgage default rates are creeping up as well.

Bloomberg

In light of these challenges, I'm currently working on my watchlist and portfolio to assess which investments I want to expand on weakness and which investments I might add.

This includes a few compounders that - I hope - may offer us attractive buying opportunities over the next few months and quarters.

One of these stocks is Copart ( CPRT ) , an industrial stock I found in 2018 .

Going forward, I expect Copart to further show double-digit EPS and sales growth, as economic growth supports overall demand for cars, while second-hand car prices are likely going to improve further. On top of that, I think the company will remain a winner with a unique business model that still has a strong flow of new customers.

Since then, CPRT has returned more than 210%.

In this article, I'll explain why I'm looking to buy CPRT on weakness if I get the opportunity.

So, let's get to it!

What's Copart?

Copart originated in California in 1982, went public in 1994, and later reincorporated in Delaware in 2012.

Presently headquartered in Dallas, Texas, the company operates globally across the United States, Canada, the United Kingdom, Brazil, Ireland, Germany, Finland, the United Arab Emirates, Oman, Bahrain, and Spain.

Although the biggest chunk of its revenue is generated in the United States.

| USD in Million | 2022 | Weight | 2023 | Weight |

|---|---|---|---|---|

| Service | ||||

| 2,853 | ||||

| 81.5 % | ||||

| 3,198 | ||||

| 82.6 % | ||||

| Vehicle | ||||

| 648 | ||||

| 18.5 % | ||||

| 671 | ||||

| 17.4 % |

In other words, CPRT offers a very differentiated way to benefit from the automotive industry and its ever-increasing installed base. I prefer CPRT over buying automotive manufacturers, as I don't like the risk/reward of almost every single one of these manufacturers.

Essentially, Copart's growth strategy revolves around expanding its network of vehicle storage facilities, pursuing global, national, and regional vehicle seller agreements, enhancing service offerings, and furthering the application of its VB3 platform in new markets.

{kind=link}

They actively seek acquisitions to integrate into their network, optimizing operational efficiency and cost-effectiveness.

Additionally, they focus on service augmentation, leveraging technology to provide real-time data, predictive analytics, and an enhanced bidding experience for their members.

{kind=link}

This business model has turned into a mind-blowing success. The company has found an asset-light way to benefit from an expanding installed base of autos without being dependent on new car sales.

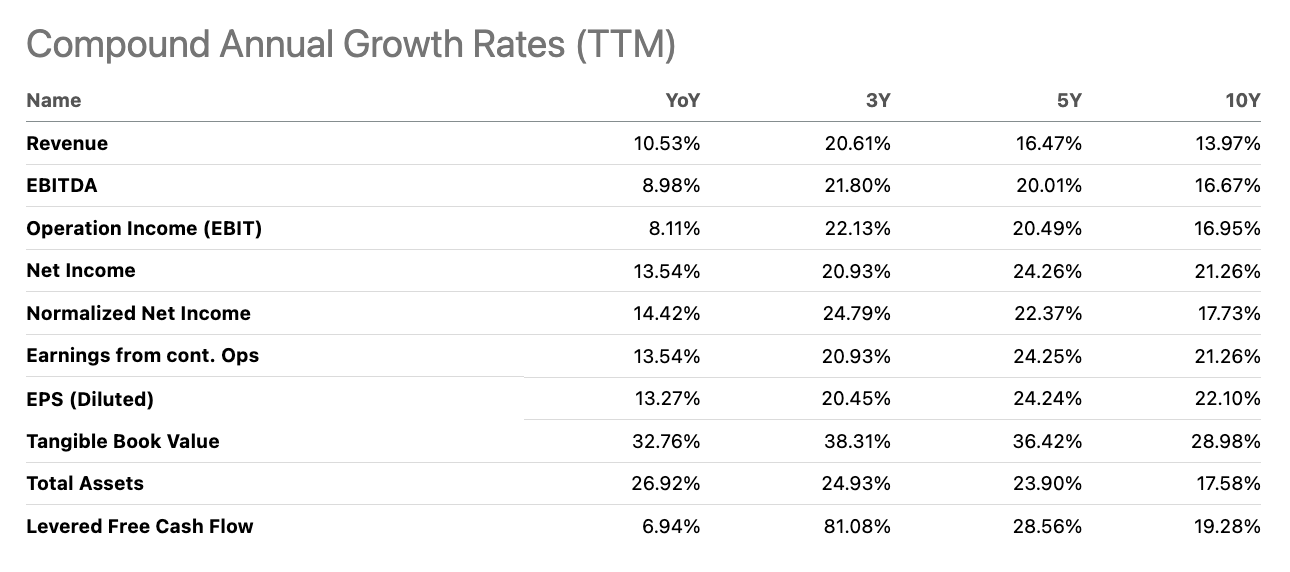

Using Seeking Alpha data, we see that the company has grown its revenue by 14.0% per year over the past ten years. Thanks to increasing margins, it turned this already impressive growth rate into 16.7% annual compounding EBITDA growth and 22.1% compounding earnings per share growth.

{kind=link}

It also helps that the company has a very healthy balance sheet.

As of July 31, 2023, the company has $6.7 billion in assets. Roughly $2.3 billion of this is cash and investments in held-to-maturity securities.

It has just $10.9 million in long-term debt.

The company is expected to end the 2024 fiscal year with $1.7 billion in net cash.

As one can imagine, the mix of strong secular growth and capabilities to capture growth has led to tremendous capital gains.

Over the past ten years, CPRT shares have returned 953%, beating the already impressive 203% return of the S&P 500 by a wide margin.

Now, the question is: how attractive is CPRT at these levels?

The CPRT Risk/Reward

In light of a challenging economy, it needs to be said that CPRT continues to fire on all cylinders.

Last month, the company presented the results for its 2023 fiscal year, which ended in July.

{kind=link}

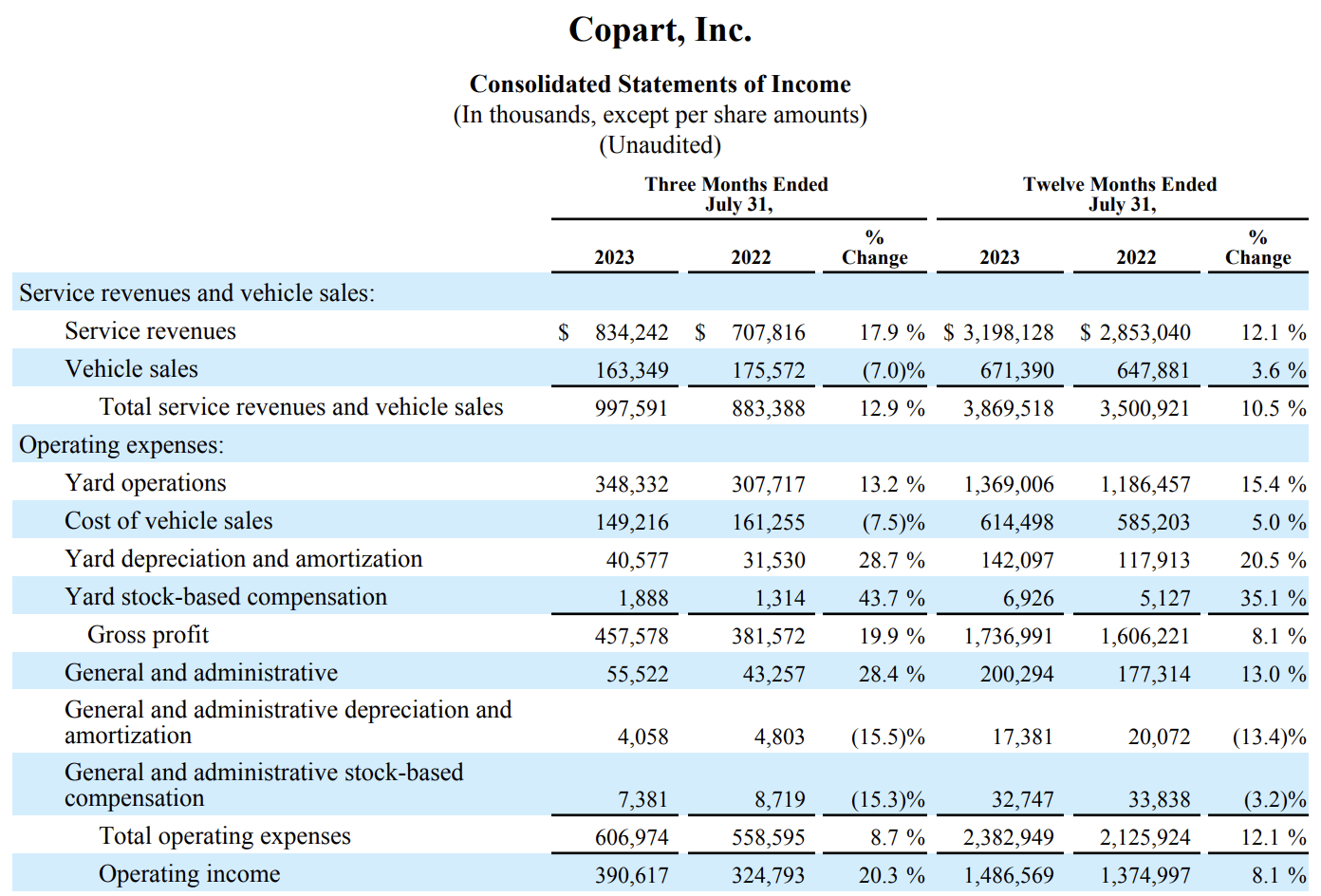

As the overview above shows, global revenue for the fourth quarter increased by $114 million, representing growth of nearly 13%, with a 1% tailwind due to currency fluctuations.

For fiscal year 2023, global revenue grew by $369 million, surpassing a 10% increase, although it faced a 1% headwind due to currency changes.

- Global service revenue saw significant growth, increasing by $126 million (nearly 18%) for the fourth quarter and $345 million (12%) for the year. This increase was primarily attributed to higher average revenue per unit and increased volume.

- In the U.S., service revenue showed a growth rate of almost 16% for the quarter and over 12% for the year, while international service revenue exhibited remarkable growth, exceeding 36% for the quarter and 11% for the year.

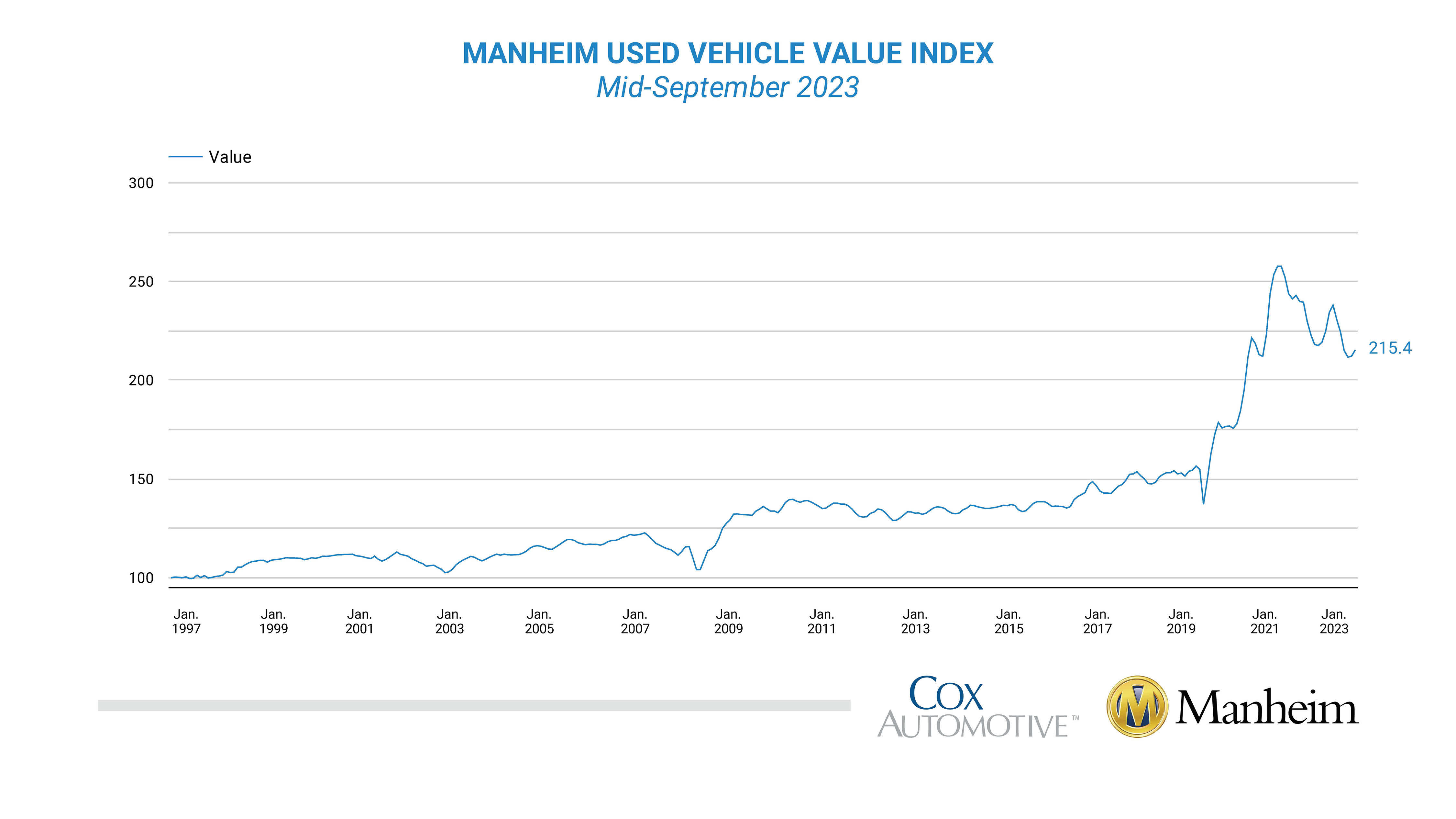

- Average sales prices slightly increased year-over-year for the quarter, with U.S. ASPs up by about 2%. This was noteworthy, especially considering the over 11% decrease in the Manheim Index, which can be seen below.

{kind=link}

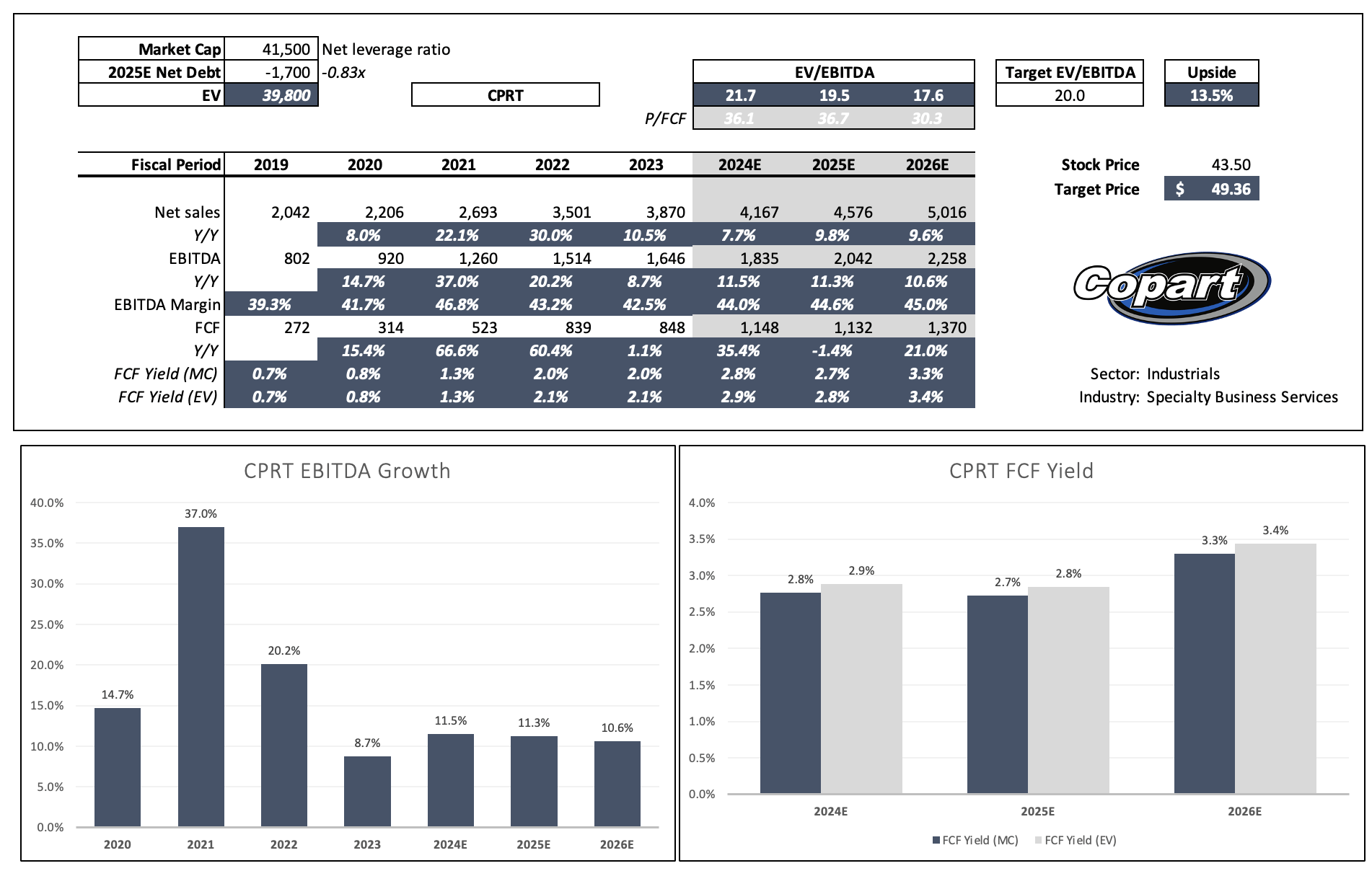

Looking at the data below, the market expects the company to maintain double-digit annual EBITDA growth and a free cash flow improvement to more than 3% of the company's market cap. This should help the company maintain a very healthy balance sheet and use M&A to expand its services - if it sees opportunities down the road.

Leo Nelissen (Based on analyst estimates)

{kind=link}

Having said that, the stock is trading at 21.7x 2023E EBITDA. That number drops to 17.6x using 2025E numbers.

Historically speaking, a 20x valuation multiple is fair, especially if the company is able to maintain double-digit annual EBITDA growth.

This would give the stock a fair price of roughly $49 per share.

The current consensus price target is $49. I cannot remember the last time these numbers matched exactly.

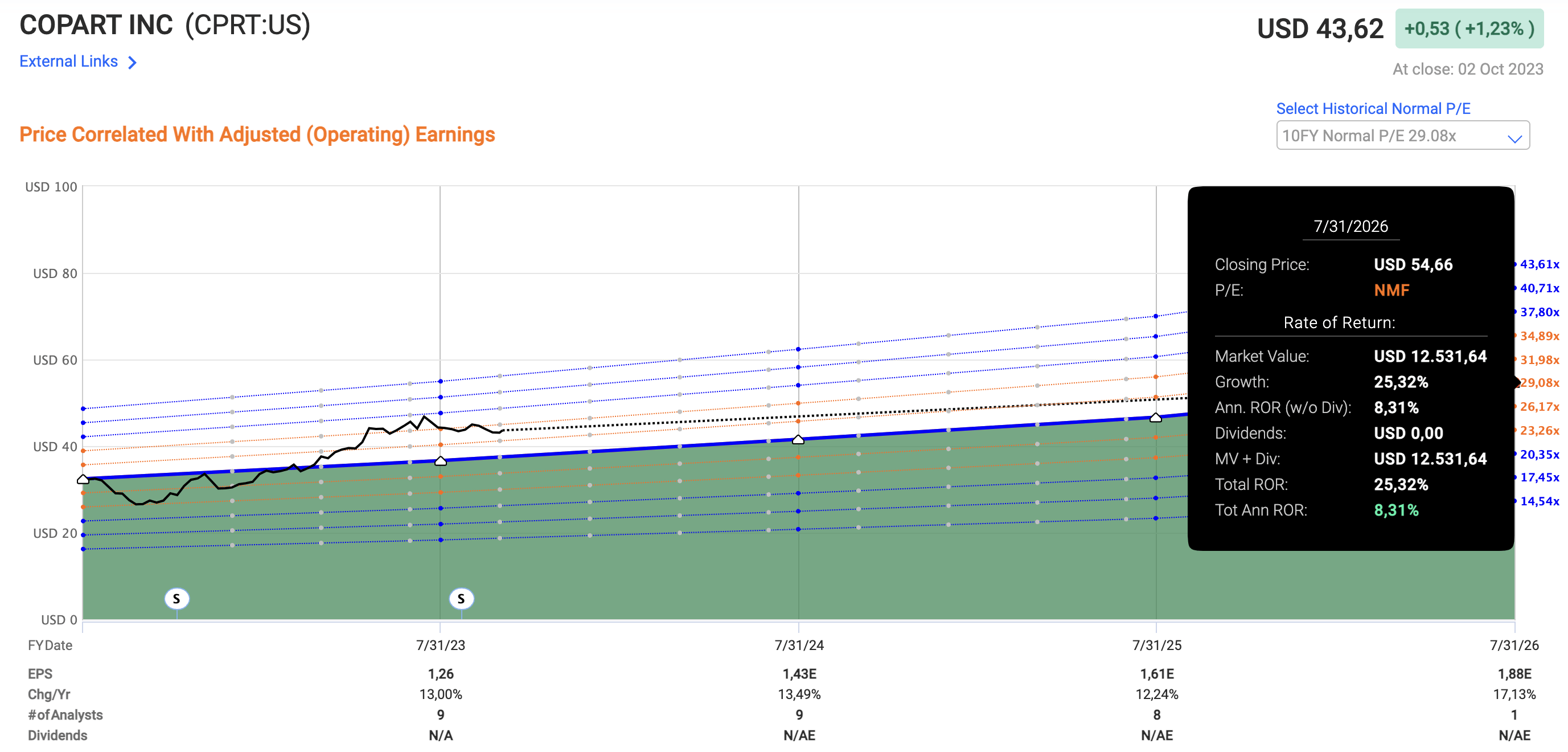

Over the past ten years, the company's P/E ratio averaged 29x. If the company maintains this valuation, it could return 8.3% annually through 2025. This is based on double-digit earnings growth expectations (shown in the overview below).

{kind=link}

Note that I'm not making the case that 8% annual compounding growth will happen. It just shows the risk/reward.

Based on everything said so far, I would not buy CPRT above $35.

As much as I love this business, I believe that $35 (and below) is a good entry point. Given the tremendous pressure on the economy, I think trying to buy at these levels is not that much of a long shot.

Takeaway

In today's turbulent market, with rising rates and economic challenges, finding resilient investments is crucial. Copart, an industrial gem I initially discovered in 2018, stands out.

Its unique business model in the online vehicle auctions and remarketing services industry positions it for growth, leveraging the increasing installed base of autos.

With a history of impressive revenue growth and a healthy balance sheet, CPRT has outperformed the S&P 500, returning over 953% in the last decade.

However, given its risk/reward, aiming for an entry point below $35 seems to be the best way to go.

For further details see:

Copart: A Top-Tier Compounder I'm Buying On Weakness