RBA:CC - Copart Deep Dive: Impenetrable Moat And Growth

Summary

- Copart is insulated from the short-term negative headlines in the automotive sector with long-term tailwinds in the insurance salvage business.

- Domestic dominance will be translated internationally as demonstrated by the insurer receptiveness and growth in Germany and the UK.

- Several lasting, structural advantages over the company's only sizable domestic competitor are leading to accelerating market share gains.

- Insurmountable and growing barriers to entry with significant insurer contract stickiness will contribute to setting Copart's dominance in stone.

Copart ( CPRT ) has a moat like no other that only becomes more impenetrable with time. Their only large domestic competitor, IAA ( IAA ), is only bound to lose market share, and so are smaller domestic players. International insurance salvage markets have not caught up to the new U.S. model Copart spearheaded, which creates an opportunity to repeat its domestic success.

Breaking Down the Breakdown Business

Copart operates online vehicle auction platforms primarily for salvage and whole vehicles. Salvage vehicles currently represent 80% of the total processed volume and are obtained through long-duration (and increasingly exclusive) contracts with insurers.

The company's insurance segment operates under two distinct revenue models: Under the principal model, it purchases vehicles directly from insurers and sells them on its own account retaining all of the selling profit. Under the agency model, vehicle ownership remains with the insurer, but Copart receives a percentage of its selling price. Both of these models (and non-insurance services) are supplemented by processing, marketing and listing fees as well as buyer fees.

Business Drivers

Copart deals on volume: The more vehicles that are processed, the more bidding, listing, and sales fees that are generated. I will focus on the volume drivers only for their dominant insurance segment.

The total loss rate ((TLR)) is the percentage of reported accidents determined as total losses by insurers. This rate matters to Copart as these are the vehicles their retrieve, process, and sell. Skipping the calculation details of the insurer's determination, and while the thresholds and details vary by state , we can think of the TLR as influenced by three variables:

- Actual cash value (pre-accident vehicle value less depreciation)

- Salvage value (post-crash estimated vehicle value)

- Repair costs (costs to remit vehicle to pre-accident state)

Here are their correlations with TLR:

{kind=link}

As can be seen in the graph below, the TLR has been increasing significantly over the past decade.

TLR Trend (2010-2020) (CCC 2022 Report)

The next section discusses why I believe TLR will sustain its increase in both the short and long term.

Promising Long-Term Trends for Salvage

Repair Costs

Over the past decade, the average repair costs for insurance claims rose by 41%. I expect this trend to continue in the future, first due to vehicle complexity; with expensive integrated tech and more complex crash structures, the number of parts repaired per insurance claim increased by 42% between 2010 and 2020 and labor hours per claim by 8%. Vehicle-technology integration is a secular trend for which I do not expect a reversal. As higher repair costs imply higher TLR, I expect this trend to provide more insurance volume to CPRT in the long term.

Parts

Design patents, valid for 14 years (beyond most vehicles' useful life), increased from 4% to 25% of all automotive patents filed over the past decade, with between 50% and 93% of these being for crash parts. Since OEM parts are, on average, between 60% and 70% more expensive than aftermarket parts, a limited non-OEM parts market is bound to further increase parts costs. As lawmakers in the U.S. have unsuccessfully tried for more than 10 years to limit OEM patenting rights for crash parts through acts such as PARTS and SMART , I believe higher parts cost related to patenting will be sustained and a long-term positive volume driver for Copart.

Labor

Labor costs have also been rising and will continue to rise. They will be more downward sticky than vehicles' pre-crash values in the current auto deflation environment (good for TLR). Between 2010 and 2020, the auto body shop labor rate went up 17%, but workers' productivity (labor hours per day) has decreased by 25% just since 2017. With many shops having trouble hiring qualified mechanics, training them to work on more complex and technological vehicles, or affording equipment necessary for certain repairs (especially sensor calibration, more ubiquitous than ever in all vehicle classes), the number of shops able to repair certain vehicles can be limited, a trend set to accelerate significantly as EVs gain traction.

With 30% of auto body shop owners reportedly thinking of leaving the industry in the next two years, 50% of them being over 50 years old, we should expect further consolidation of competition by multi-shop owners (MSOs). As such, between 2019 and 2021 the average number of cars per auto body shop in the U.S. shop went from 225 to 246, with 96% of shops facing delays of, on average, 3.4 weeks in 2021 (up from 1.7 weeks in 2019).

With higher parts costs, higher labor costs and auto body shop consolidation, I expect the average repair cost to continue to outpace vehicle ACV growth and increase TLR.

Salvage Value

Copart, IAA, or third parties do not compile or report salvage prices and trends. However, we can work around this and form a reasonable assumption with available statistics.

Given that buyers of salvage vehicles are mostly dismantlers for parts or scrap, we will take the assumption that the parts cost growth will at least partly translate into salvage prices. Between 2010 and 2020, the cost of parts increased by 48%, whereas according to the Mannheim Index, used vehicle values increased by 25% . Taking the resale value of parts as one of the main determinants of a salvage vehicle's value and that used vehicle prices are mostly not subject (or at least not so predominantly) to this driver, I assume that the difference in growth for parts prices and used vehicles has resulted in a shrinking average value difference between salvage and used vehicles.

Since I expect the cost of new parts to continue increasing for reasons discussed in the section above, I expect this gap to shrink further at the benefit of total loss rates.

Insulated From Short-Term Automotive Demand Trends

In the near term, used auto prices remain ~41% above mid-2020 prices after falling ~15% from peak prices. I expect, as do most, that given the sector's economics, they will fall further . Yet I believe the effect of this fall in prices will not be significant on Copart's bottom line.

{kind=link}

Effects of Falling Used Vehicle Prices

While lower whole (used/new drivable) vehicle demand is naturally correlated to that of salvage vehicles, I expect the prices of salvage vehicles to fall but be more downward sticky than that of whole vehicles.

For the reasons mentioned above, I expect parts prices to remain elevated and contribute to the higher realized value of salvage vehicles in the long term. In the shorter term, deferred vehicle purchases would increase the average vehicle age and repair frequency given the assumed unaffordability of newer vehicles. The rising demand for now scarcer parts could lead to further salvage price increases as the aforementioned OEM parts patenting will allow only manufacturers to legally fill parts demand.

In any case, increased parts prices should be met with consumers' inelastic demand; given the economic assumptions, repairs will remain cheaper than purchasing a newer vehicle. Since many salvage buyers are dismantlers, it should be partially translated into salvage prices and yield stickier ASP than for whole cars in the shorter term.

While this conclusion contains many assumptions, I though it worth mentioning as a possibility. Even constant parts prices will not matter as the falling vehicle prices will be offset by the following effect.

Higher Vehicle Processing Volumes

The lower prices due to lower demand imply deferred personal vehicle replacements, higher average vehicle age, and lower pre-crash value ((ACV)). Because ACV factors into total loss determination, ACV reduction will increase the TLR, increasing the insurance vehicle volume for Copart. In fact, this is a well-known effect discussed in Copart's latest earnings call (see below).

Uncertain Net Effect on Bottom Line

During the Q4 2022 earnings call , Copart Co-CEO Jeff Liaw said that they "don't know precisely which is 'better' for the bottom line" when comparing higher ASP vs. higher sale volumes. Based on the above, I believe the combined effect of higher processing volume and lower realized auction prices to be negligible on Copart's bottom line.

However, as Copart's principal model vehicle purchases are at a fixed, contracted price, we should expect temporary negative gross margin pressure until these contracts are renegotiated to reflect the fair market price of salvage.

IAA Doesn't Measure Up

The U.S. insurance salvage auction business is a duopoly; Copart claims 43%, IAA 40%, and smaller players 17%, with the closest one representing only 3% of the total market. I expect Copart to continue taking market share away from IAA and smaller domestic competitors due to its:

- larger buyer networks,

- stronger insurer relationships,

- broader customer base,

- better yard design,

- better financial position, and

- solid governance.

Larger Buyer Networks

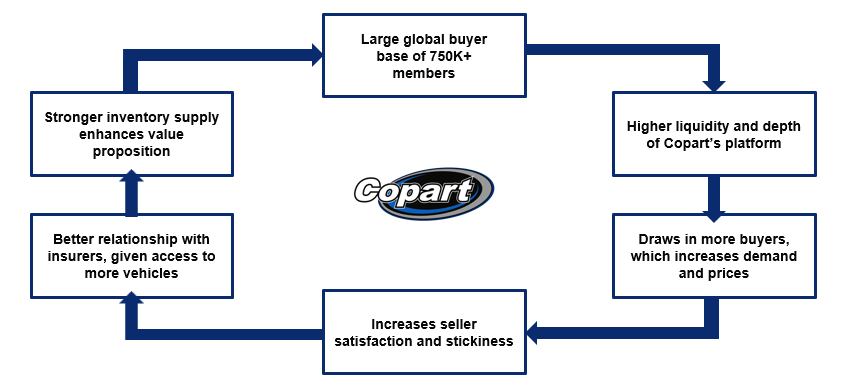

Copart's online auction platform benefits from strong network and buyer/seller flywheel dynamics. While Copart's online platform has over 750k buyers, IAA has only around 300k. Consider the below:

Copart's Buyer/Seller Flywheel (Author)

{kind=link}

I expect Copart to continue extending its online buyer base advantage; IAA started moving aggressively from in-person to online auctions faster than ever in 2019, whereas Copart has been online for over 20 years.

As depicted in the figure above, the more buyers there are on Copart's auction platform, the more competitive the bidding process is and the higher the final ASP (which insurers care about under the dominant agency model). This in turn which drives more insurance business to the platform, increases the inventory breadth and depth, and attracts even more buyers. Therefore, if we assume insurance market share capture (which leads to inventory growth), we should also assume buyer base growth.

Copart also markets and sells vehicles online for mostly local dealers of used whole cars through Copart Dealer Services (CDS). This segment accounts for most of Copart's non-insurance vehicle volume (20% of total), while IAA is legally prohibited from expanding into a dealer business for five years post-spinoff due to a non-compete with KAR. That's another advantage in attracting customers and inching its online platform dominance further ahead.

Stronger Insurer Relationships

Copart currently has 35 contracts with separate large insurers, whereas IAA has 10, and the trend has been increasingly concentrated auctioneer contracts with fewer or a single partner.

Copart moved to fully online auctions more than two decades ahead of IAA (2003 vs. 2020), allowing them to capture and develop a much stronger domestic and international buyer base online. Due to the dynamics of the flywheel discussed above, this more extensive buyer base provides insurers with a more competitive bidding process and higher realized sales prices (estimated ASP of $6,000 vs. IAA's $5,250), and lower turnaround times (30 days for Copart vs. 70 for IAA). Insurers see the benefits of this higher ASP directly through the dominant agency model where they receive a large percentage of the selling price.

Copart's integrated critical services, such as vehicle title processing, also make insurers dependent on them for essential processes of vehicle disposals, further increasing switching costs and barriers (the importance of which be further discussed in the international expansion section).

Copart signed on GEICO and American Family in 2019, two of the top 10 largest U.S. insurers. According to Copart's former VP of sales and accounts management, insurers grant increasingly exclusive salvage auction contracts of about five to seven years. Reliable service in all events then becomes very important if insurers depend on a single auctioneer. As such, GEICO's judgement of IAA as inefficient during Hurricane Harvey was the straw that broke the camel's back. I'll let Copart's former director of sales and accounts management describe why this pushed them to leave IAA for Copart:

It was kind of just like IAA has GEICO. And what happened is GEICO became very frustrated with the catastrophe performance of IAA. IAA did not plan for nor handle catastrophe volume efficiently like Copart did. Copart proactively bought land. They proactively put tow trucks and had agreements in place in municipalities where they could come right in and start getting cars. IAA missed the boat there. Right around Hurricane Harvey in Texas is when GEICO finally got pretty darn mad at IAA. They said, OK, I think it's about time we talk to you guys.

Catastrophic ((CAT)) events engender an irregularly high number of total losses for insurers. While they always care how fast these totaled vehicles can be moved, processed and sold to limit their storage expense, cycle times, and maximize the insured's satisfaction, this is particularly true during such events. In the normal course of business, before Copart or any towing partner picks up a crashed vehicle, it sits in storage at fees charged to the insurer of between $75 and $300 per day. This doesn't change after CAT events. The auctioneer's inability to respond and collect the surging volume of vehicles will be a direct (large) cost to the insurer. Copart plans ahead by owning idle land around CAT-prone areas, part of its towing fleet, and mobile divisions/personnel, all of which exacerbated the "normal" difference in operational efficiency between the two companies and pushed GEICO over the edge. IAA couldn't keep up.

Interestingly, despite Copart's decades-long contracts with most of the U.S.'s largest insurers, GEICO initiated their contract through pilot tests to ensure its salvage volume was handled efficiently. This only shows how insurers are incredibly slow movers and explains the low churn. Not only are internal logistics complex to change, but there is no guarantee that another auctioneer will be able to match your needs in short order. This is especially true if the insurer needs sizable geographical coverage with a single partner; only IAA and Copart can offer such a service.

Reputation and track record should play a big role for insurers, so I don't expect any of the "switchers" like GEICO to return to IAA any time soon.

Broader Customer Base

I have already briefly touched on the size difference in both companies' buyer bases, but the difference in their composition is also to Copart's advantage. Sixteen percent of the buyers on Copart's platform are international, compared to only 8% for IAA, the advantage likely catalyzed by Copart's much earlier transition to online, also discussed earlier.

Their inventory is also not as concentrated in insurance salvage; while 20% of their vehicles processed and sold are not from insurers, only 8% of IAA's are. Once again, I do not expect this number to rise much as they are prevented from expanding into the used/dealer side of the vehicle auction market for five years due to a non-compete with KAR. Most importantly, IAA has dangerously elevated contract concentration; their top three insurance contracts account for 40% of their revenue, while no single insurance partner represents more than 10% of Copart's.

Better Yard Design

Copart owns over 90% of its yards and IAA leases approximately 90% of its own (Copart operates on 16,000 acres and IAA 9,550). Around 50% of Copart's total capex of $1.8B over the last six years was spent on land acquisitions. Here is why land ownership matters:

- Protection from costs inflation

- Superior vehicle handling capacity (see CAT events)

- Lessee has weak bargaining power relative to the lessor

- Land only becomes more unaffordable with time

- Zoning limits land acquisition opportunities

A yard's urban proximity is essential to reduce pickup times, but also because Copart and other insurers pay the towing fees. The more centrally located and optimally densified the yards are (to limit travel distance to/from yards to fetch vehicles), the better it is from both unit economics and insurer relationship standpoints.

However, due to costs and zoning laws, urban proximity becomes increasingly difficult to attain through land ownership and yard construction. In the event IAA loses out on leases in strategic, highly competitive locations, its ability to secure other leases nearby or purchase new land is seriously questionable: Strict land use regulations have led to industrial land parcels being zoned to city outskirts. A great example of zoning difficulties is Copart having to wait for more than 20 years to obtain a permit to operate a yard on a piece of land it owned in California. While IAA would face countless such roadblocks if it decided to suddenly embark on an ownership strategy, Copart's owned and zoned lots are already grandfathered in.

Furthermore, environmental hazard risks (leakage of oil/antifreeze, noise pollution, etc.) have necessitated the need for appropriate licenses and ecological clearances, a bureaucratic barrier to entry which can delay or prevent expansions.

On costs, consider the land Copart bought around Los Angeles around 10 years ago. Now worth 10 times the price paid, its market value will only continue to increase. Copart gains twice on this trend - its assets appreciate and its competition's finances only become more squeezed with time as their lease costs increase and land acquisition options deteriorate. The longer IAA takes to realize the corner it is painting itself into the better for Copart; they only need to maintain their land and any pricing increases beyond that accretes directly to its bottom-line (all else equal). For IAA, price increases may only serve to fund rising lease costs.

Better Financial Position

Both companies' operations are mostly insurance salvage (80% for CPRT and 92% for IAA), and despite continuing to extend its lead over IAA, both share a similar domestic market share in insurance salvage (43% for CPRT vs. 40% for IAA). However, IAA is much more financially vulnerable than Copart.

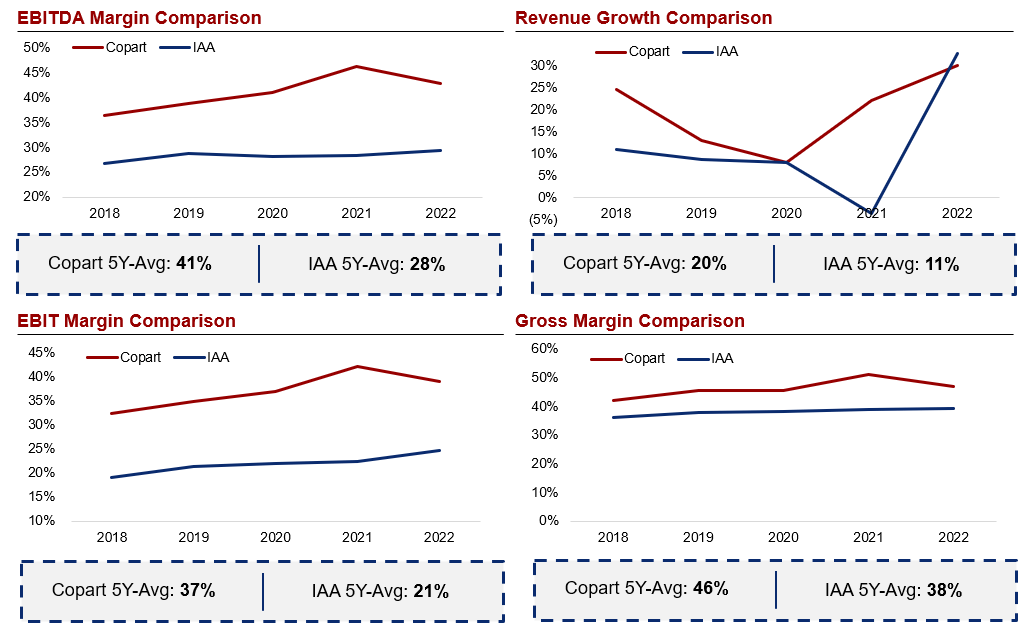

In the LTM, Copart generated revenue of $3,700mm vs. IAA's $2,098mm. Copart's revenue has been growing at higher rates (further extending its lead), with better Gross, EBITDA and EBIT margins (see the figure below).

Compiled and Formatted by Author (from S&P Capital IQ)

{kind=link}

The advantage or financial payoff of land acquisitions can be visible in Copart's significantly higher EBIT margin. While it only depreciates its land with UCC at historical cost, IAA continually amortizes leases at prices more likely to reflect the land's market value and with no end in sight. While costs associated with a yard end once Copart depreciates its acquisition costs, once IAA fully amortizes its lease it must renew it and begin its amortization anew at presumably higher prices following land appreciation.

This difference can also help explain Copart's larger lead in EBIT than EBITDA margin as it is solely attributable to the D&A (depreciation and amortization) factor. It implies that over the past five years, D&A represented on average 7% of IAA's revenue vs. 4% for Copart, which likely circles back to the fact that IAA's land-related expenses are likely closer to the land's market value.

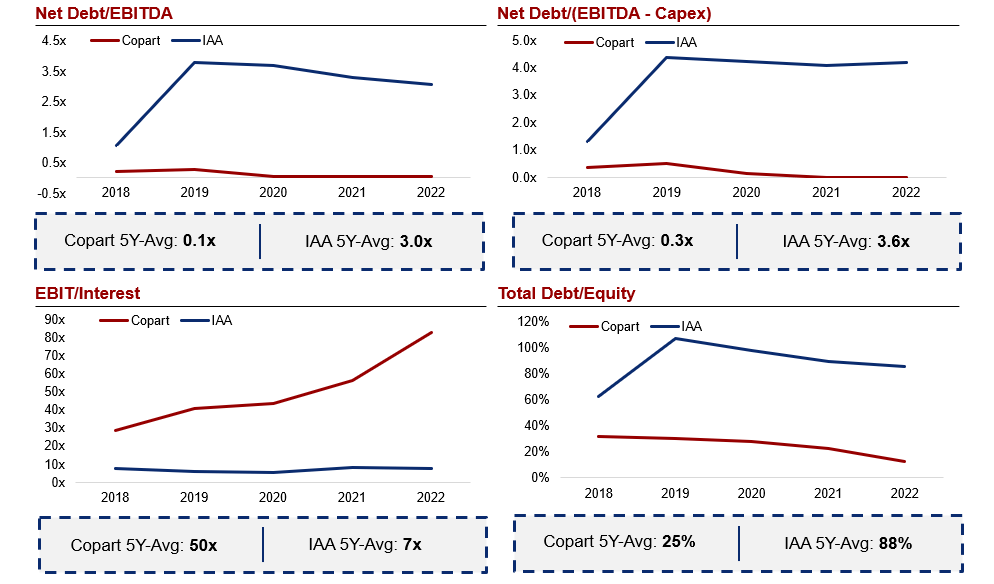

Related to the above but referring to the graphs below, Copart's management is much more disciplined with debt than IAA. Importantly, IAA's long-term debt multiples do not include operating leases, even though as of the latest quarterly filings, long-term obligations related to leases are as large as the carrying value of long-term debt. Copart's strategy provides it much operational flexibility, financial resiliency, and acquisition financing options:

Author (Data from Company Filings)

{kind=link}

IAA's financial vulnerability could also swell its market share loss troubles. As mentioned above, IAA's insurance segment is dangerously concentrated as their top three insurance partners account for 40% of their revenue, while no such partner represents more than 10% of Copart's revenue.

Pair the risk of market share loss with the fact that IAA cannot legally diversify into used vehicle auctions and the loss of one of these contracts would be catastrophic. According to SimilarWeb, the traffic to Copart's platform has been more resilient than that of IAA, falling 12% in the last 12 months whereas IAA's fell 25%. This only confirms and amplifies my lack of confidence in IAA's buyer base development and retainment; Copart's website now has 72% more global traffic.

Solid Governance

Since founder Willis Johnson stepped away from his CEO position in 2010 (he's currently chairman of the board), Jay Adair has led the company with now more than 30 years at Copart. What displays management's shareholder alignment and business-first mindset is Adair's compensation plan: $1 a year salary, $0 annual bonus and 3.35% ownership of Copart.

Innovation has always been a focus for Copart. When it created the profit-sharing (agency) model with insurers, IAA stuck with its buy-and-flip (principal) model and only followed Copart's lead in the 90s. While Copart developed an online auction system in 1998 and moved 100% of its auctions online by 2003 after realizing its advantages for both Copart and buyers, IAA took until 2020 to transfer its own auctions fully online after initiating online auctions just a few years prior. Copart is again pioneering the consignment model in the UK and Germany (more on this in the international section) and solving used vehicle market inefficiencies with its CDS segment (discussed above).

Internally, Copart kicked off the "Copart Identity Campaign" in 2003. Management (including CEO Willis Johnson) toured every yard in the U.S. to emphasize, revive, and reinforce their family-business culture, employees' sense of belonging, and commitment to outstanding service to buyers and sellers. Interviews with former employees show that mid-level management at Copart is held accountable to specific metrics of operation efficiency; the process timelines and spreads are stricter and have been broken down to the number of hours. While Copart has had two chief executives since 1982, IAA has had five. This stability enables corporate culture continuity.

Ritchie Bros. Is Not a Concern

In early November, Ritchie Bros. ( RBA ), an industrial and construction equipment auctioneer, announced having entered into a definitive agreement to acquire IAA for ~$7.3B. I do not believe this news changes my competitive assessment above.

RBA's buyer base is non-transferable to IAA's insurance salvage business; they have no existing relationship with consumer insurers that IAA could leverage. Ritchie Bros.'s yards will also not materially improve IAA's competitive positioning. These yards are already used for RBA's industrial equipment storage and auctions and the yards' systems for storage, processing, and marketing are not optimized for the distinct volume-heavy insurance salvage operations. I also discussed the importance of location and optimal density for insurance salvage yards, and I do not expect Ritchie's yards to have been built with similar strategic locations. RBA and IAA together would only have 13,600 acres (still 2,400 acres fewer than Copart), and that's assuming that all of Ritchie's land would be converted as insurance-ready for IAA.

If anything, I expect the deal to be voted against by shareholders; the 19% premium paid on IAA shares was essentially wiped out to 2% upon announcement, implying that investors either believe the deal will destroy value or that it revealed management believes its stock price is overvalued. Regardless, given that over 85% of RBA shareholders are institutions, I don't expect a voter turnout problem, and I believe the response that management will receive from shareholders will echo Ancora Holdings Group's (4% RBA shareholder) disapproving letter to the board .

An even more detailed letter from Luxor Capital to Ritchie Bros. contains insights and data echoing some points discussed above. Luxor provides several data points demonstrating IAA's domestic market share loss to Copart (and its acceleration), disputes the claims of synergies between RBA and IAA and reiterates my thoughts as to the market's reaction to the announcement. I recommend this letter for further reading. Even if the deal goes through, I do not believe it will lift IAA out of its negative momentum.

Significant International Opportunities

Copart is currently pursuing primarily European expansion. TAM-wise, the number of vehicles in the U.S. has grown at a 0.65% CAGR over the past five years compared to Europe's 1.5% CAGR. European vehicles are also aging faster; their average age has grown at a CAGR of 1.8% between 2016 and 2020 compared to 0.85% in the U.S. (beneficial to the TLR as pre-crash values are bound to be lower). Copart has its largest European operations in the UK and Germany, whose combined automobile market size is equivalent to that of the U.S. The chart below shows Copart's international revenue growth by segment, both with a ~12.5% CAGR since 2015.

Author (Data gathered from Company Filings)

Highly Inefficient Markets

While the fragmented mom-and-pop salvage auction market in the U.S. has been disrupted over the past decades, many countries' salvage disposal process remains even more inefficient than the U.S.'s was 50 years ago.

Take the example of Germany. Until Copart entered in 2016, salvage vehicles were kept by the owner and it was their legal responsibility to sell them to recuperate their salvage value. It was illegal for an insurance company to net direct settle and take possession of a vehicle. The insurance company only paid the policyholder for its estimate of the difference between the vehicle's pre- and post-accident values. Selling this vehicle was a lengthy and painful process; on German vehicle auction sites, buyers are obligated to honor their bids for a full 21 days after bidding, but the owners do not have an obligation to sell which creates an adverse selection problem. Only up to 33% of auctioned vehicles were awarded to buyers.

After more than a year of legal procedures and analyses, Copart began operating on what is called the V ermittler model in Germany, managing to independently create legal documentation that could be signed by the insurer and insured to circumvent the legislation which prevented insurers from selling vehicles. In my opinion, the legal process to get to this stage demonstrates how smaller competitors would struggle to enter or disrupt these high-friction markets.

Many more countries in which Copart has expanded operations into share Germany's process of customer retained salvage (see figure below). The value-add of Copart's services will be even more significant there than in the U.S. or UK.

Author (Company Filings & Statista)

Encouraging Growth

Since entering Germany, some of the country's largest insurers have been cautious but eager to do business with Copart. The company often mentions that initiating international contracts under the principal model can be necessary since insurers buying into the agency model straight away risk bearing the cost of an inefficient auctioneer.

Carlos Sabugueiro, Copart's former CEO of India, the Middle East and Africa, mentioned that as he left in mid-2020 , German insurance companies were shown a year's worth of data demonstrating that vehicles listed on Copart could fetch 33% higher resale values than those of a leading German platform (WOM). At the time, seven of the top 10 insurance companies in Germany were involved in pilot testing with Copart.

According to Sabugueiro, eager insurers will not look to switch in a piecemeal way; they are looking for a streamlined, cohesive and consolidated process, and it makes sense to consolidate it with the auctioneer offering the largest ROI. This approach mirrors the contract consolidation trend among U.S. insurers which we've discussed.

Copart has been working on "cracking" international insurers as it has done in the UK, its first non-American expansion, initiated in 2007. In the three years that followed, Copart successfully converted most insurance contracts it had in the UK from principal to agency. As further proof of its unrivaled value offering, Aviva, the UK's largest general insurer, closed their own salvage auction subsidiary in 2013 to award their business to Copart. While it took Copart five years to reach 1 million cars sold in the UK, it only took two to get a million more.

Business Model Transition

I mentioned that Copart is continuously looking to onboard international insurers onto the agency model by proving that they're giving away some of the salvage's realizable value to Copart by selling at a fixed price under a principal arrangement. Why would Copart do this? Because of agency's higher revenue and principal's higher margins, management claims that the differences offset each other such that the bottom-line results are not materially different between the two.

What instead motivates Copart's preference for the agency model is that insurers adopting it align their interests with Copart's. If Copart buys salvage from insurers, it is in their best interest to negotiate salvage prices as low as possible whereas insurers want to raise them ever higher. This business model generates too much friction given that Copart aims to retain these insurance clients for decades.

With the agency model instead, Copart and the insurer share the goal of selling the vehicles as fast as possible for as much as possible.

Looking Ahead

Again according to Sabugueiro, the professional relationships Copart has developed there will benefit their expansion into other European countries:

We've got tremendous working relationship with Zurich in the UK. Zurich has a team of forensic examiners that are based at one of Copart's yards. So that's how entrenched Copart has got in the UK in its relationships with its customers, and the same in the U.S., is the Copart's model with its land, with its process, with its system, with its added value services. It's now really difficult to ever get out. Once you're in and you buy in, which you do pretty quickly because you start to see that Copart derives the right price for your vehicle, it's quite difficult to extricate yourself.

This will only further catalyze Copart's market share dominance internationally. Can IAA convince insurers to sign with them and take a risk with them in let's say Germany when they have long-standing and smooth-running operations with Copart in the UK? Given most insurers' low churn and risk-averseness discussed earlier, I don't see why they would, especially given Copart's numerous structural advantages that were described above.

Unit economics are also bound to significantly improve as operations scale in specific international markets. As discussed in the IAA section regarding Copart's superior yard design, higher urban yard density increases margins due to lower towing costs. Here's a concrete example:

Author

The above simply demonstrates the lower unit costs brought about by yard proximity to pickup location. With more yard concentration in urban centers, the average towing distance and towing unit costs decrease. Therefore, not only will revenues naturally improve as international operations are scaled, but with time, so will margins and operational efficiency.

Conclusion

Copart will not be affected by short-term automotive market weakness in demand and prices like a purely used vehicle sales platform would be. Beyond the short term, I expect Copart to keep capturing market share as it takes advantage of its buyer-seller flywheel and structural advantages over competitors.

While still in the early stages of its international expansion on a relative basis, given the high frictions of foreign auction salvage markets, I believe Copart will have an even easier runway for growth by streamlining the salvage auction processes as it has domestically.

For further details see:

Copart Deep Dive: Impenetrable Moat And Growth