RBA - Copart: Fantastic Margins And Positive Trajectory

2023-06-20 09:56:06 ET

Summary

- Copart has a strong business model and has created a moat through technological development and increased scale.

- The company has a robust financial performance and potential for further expansion through infrastructure investment.

- Copart's conservative financing and strong cash generation can fund future growth and potential shareholder distributions.

- The company's current EBITDA-M is 42% and it is forecast to grow at a 9% rate.

Investment thesis

Our current investment thesis is:

- Copart has a high-quality business model that allows the business to carve out a niche in the car auction industry. Thus far, it has a strong pipeline of clients and vehicles, with a good monetization platform.

- Copart has developed a moat through a rapid expansion of scale, as well as the development of its technological capabilities to improve convenience for buyers and sellers.

- The used car market looks to be on a downward trend but this has not stopped Copart from growing, implying resilience.

- Copart's margins are extremely good and there is further scope for improvement.

- The company has no material debt and is accumulating cash, representing the potential for distributions or funding growth.

Company description

Copart, Inc. ( CPRT ) operates an online auction and vehicle remarketing platform that serves various countries including the United States, Canada, the United Kingdom, Brazil, and Spain.

The company offers a range of services to facilitate the buying and selling of vehicles online. Additionally, the company provides services like CashForCars.com for selling vehicles, Copart Recycling for purchasing parts from salvaged vehicles, Copart 360 for posting vehicle images, and membership tiers for buyers on their platform.

Share price

Copart's share price performance in the last decade has been astronomical, substantially outperforming the market. This has been driven by the development of a quality business model, allowing the business to grow well and generate impressive margins.

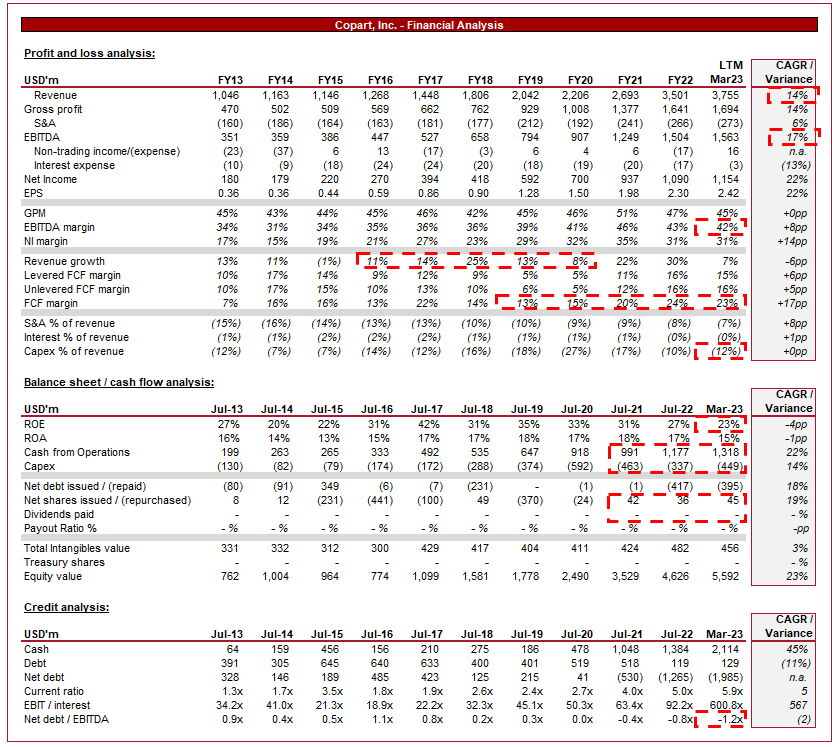

Financial analysis

Copart's financial performance (Tikr Terminal)

{kind=link}

Presented above is Copart's financial performance for the last decade.

Revenue & Commercial Factors

Copart's revenue has grown at a CAGR of 14% in the last 10 years, with only a single year of growth below 8%. This is a reflection of what is an incredibly robust business model, allowing scale investment to proportionately generate increased revenue.

Business model

The auction and vehicle remarketing industry provide a platform for sellers to sell vehicles to various buyers. Sellers consign vehicles for auction, paying a fee or percentage. Although Copart sources its vehicles from a range of customers (Banks, Charities, Dealers, etc), the vast majority are from Insurance businesses. Vehicles are processed and stored in multiple facilities, with the objective to sell the vehicles online. There is also a range of buyers, including Dealers and Consumers.

Copart's revenue is split into two primary streams, Service and Vehicle.

- Service Sales: Copart generates service revenue by charging fees for vehicle remarketing services, primarily through its online auctions. These services include vehicle purchasing fees, listing fees, selling fees, transportation fees, title processing fees, storage fees, bidding fees, and vehicle loading fees. Essentially, this is the revenue generated from monetizing the disposal process.

- Vehicle Sales: Copart also purchases and remarkets vehicles on its own behalf (as opposed to middleman operations). This revenue represents the gross revenue generated from an auction sale.

As of FY22, Copart's revenue is split as follows between the two streams.

Revenue split (Copart)

The large portion of Service revenue is critical for a high-quality operation as it means the company is not reliant on buying low and selling high. Further, earning revenue through fees allows the business to increase prices over time through inflationary increases while benefiting from scale benefits (marginal cost to provide a service). Overall, the revenue model is strong.

Moat/Differentiation

Vehicle auctions are fundamentally generic in nature. It is a market that most can enter following a reasonable capital outlay. Sellers will continue to seek the best prices and convenience, whereas buyers desire choice and ease of transacting. The focus on vehicle remarketing / salvage allows Copart to carve out a niche segment of the market within which to focus.

Copart has a significant geographic reach across multiple countries, such as the US and UK, enabling the business to benefit from enhanced scale and share expertise. Copart benefits from reduced administrative investment, lower transportation costs, convenient local facilities, a large number of repeat clients, and wider access to buyers.

Further, Copart has developed its operational capabilities. Copart utilizes technology for predictive analytics to suggest vehicles to consumers based on prior search history, it has developed an efficient process for vehicle transportation, and it has a high-quality online platform that allows for bidding/counter-bidding and payments online.

From a seller's perspective, Copart supports its clients, allowing them to access real-time data throughout the sales process in order to streamline their fleet management.

Additionally, Copart has enhanced its value proposition beyond many of the smaller, local players. This includes internet bidding, a mobile app, immediate purchase options, online payment capabilities, and multilingual notifications.

Copart has a good track record of acquiring facilities to enhance and expand its operations in domestic markets, as well as for the purpose of expanding its global presence. Many of these operations require a strategic overhaul in order to align their processes with that of Copart's, which it now is able to do efficiently.

The nature of the industry means Copart is unable to develop a traditional moat, such as patent protections, but the company has done a fantastic job of differentiating itself and building barriers around its current position. The company operates with tremendous scale (and earns the benefits that come with it) and has used this to develop technological capabilities that would require significant investment from peers in order to replicate.

Used car industry

The demand for used vehicles has substantially increased due in large part to the inability of automakers to meet demand as supply chain constraints restrict the industry. As the following used car index illustrates, demand-driven price is unlike anything seen in recent memory.

Used car price index (Autotrader)

{kind=link}

The concern is that following such a rapid demand/supply disparity, we will observe a slowdown as the market cools and market parity at a lower level is achieved. The nuance here is that this does not necessarily mean the salvage market will experience a parallel slowdown, and in theory, could see continued resilience following such a large increase in the purchase of vehicles in the last few years.

To continue driving growth, Copart should, and is, focusing on several key avenues.

The global used vehicle market offers significant growth opportunities for Copart. The industry is very much "copy-paste" across much of the developed world, with the only real difference being the potential market size. For this reason, we suspect Copart is positioned extremely well to continue its expansion. This will involve acquiring vehicle storage facilities and utilizing its existing online infrastructure. With the company operating in 11 countries, there is still a strong runway to develop further outside of its core markets. This can be enhanced through national and global agreements with vehicle sellers, allowing the business to rapidly accelerate its growth across regions simultaneously.

Finally, Copart continues to invest in its technological capabilities. This has allowed the business to develop thus far and continued investment is critical to maintaining its current trajectory (and competitive advantage). Copart has been developing its online selling platform, VB3, and intends to launch it into additional markets.

Economic & External Consideration

Current economic conditions represent a near-term headwind to the used car market. With elevated inflation and interest rates, consumers are struggling with living costs, likely contributing to a reduced desire to conduct large purchases. For this reason, we suspect a slowdown is ahead, exacerbating the slowdown we are already forecasting.

Looking ahead, we suspect rates will not begin to decline until 2024, implying a further year until economic conditions will start to improve.

This does not necessarily mean Copart will experience an end to growth, as it is (as stated previously) highly dependent on how the salvage market develops. This said, a slowdown looks reasonable to forecast compared to the last few years.

In the most recent quarter, Copart achieved a growth rate of 9%, which implies both resilience and also a slowdown.

Margins

Copart's margins are very good. The company has an EBITDA-M of 42% and a NIM of 31%.

Margin improvement has been fantastic since FY19, but does imply a portion of this is likely driven by the used car boom that occurred post-Covid. With margins reverting to within 3ppts. of FY19, we suspect Copart's is at a normalized level once factoring in scale benefits.

This profitability translates well into cash flow generating abilities, allowing the business to fund expansion and (potential) distributions.

Balance sheet

Copart is conservatively financed, with a ND/EBITDA ratio of (1.2)x. With a business such as this, where a large initial cash outlay is required alongside Capex spending, we find this unusual. This is a fantastic business with incredible margins, why not utilize debt? This could be because Management does not believe the total market size is large enough to warrant such an aggressive strategy, or it could just be pure conservatism.

The strong cash generation has thus far been utilized to fund capex, reduce debt, and fund acquisitions. Beyond this, Management has continued to accumulate cash, reaching a 10-year high relative to revenue. Thus far, shareholder distributions have been non-existent.

Outlook

Outlook (Tikr Terminal)

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts expect revenue growth to marginally slow, normalizing at a c.9% rate into FY25F. Our view is that this looks ambitious but is a reasonable forecast given how robust the business has been thus far and its continued investment in infrastructure expansion. Capex as a % of revenue remains high, illustrating this.

Margins are forecast to improve by several percentage points, which we believe is more unlikely. We suspect continued scale benefits and pricing uplifts will support improvement but not necessarily to the level expected above.

Peer analysis

Copart is not an unrivaled business but there is no company with a similar profile. RB Global ( RBA ) is comparable somewhat but is far less profitable (25% EBITDA-M) and is in the process of incorporating IAA. What this business will look like post-integration remains uncertain.

Valuation

Valuation (Tikr Terminal)

Copart is currently trading at 25.3x LTM EV/EBITDA and 21.9x NTM EV/EBITDA. This valuation is noticeably above the company's historical average.

The premium looks justified in our view, primarily due to the following summarized factors:

- An attractive business model alongside the development of barriers to entry, protecting the company's position.

- Increased scale generating improved margins.

- Successful expansion of the business model overseas, with further runway available.

- Deleveraging and cash accumulation contributing to increased potential for distributions or M&A-led growth.

Insiders

Many consider insider trading a key forward indicator for financial performance. The logic is simple. If Management is aware of factors that could contribute to a reduction in the share price, it is usually a good time to sell shares.

In the last 6 months, there were c.$40.5m in shares sold by insiders, with no buys.

Insider transaction (Dataroma)

Key risks with our thesis

The risks to our current thesis are:

- A slowdown in revenue growth as a result of current economic conditions, or a weakness in the used car market, as this would suggest a weakness in the business which has yet to be seen.

- Management's continued reluctance to utilize cash and debt in the long term, restricting the value of cash flows.

- Potential near-term weakness that has encouraged insiders to sell shares.

Final thoughts

Copart is a fantastic business. It has a strong business model with high monetization value, it has created a moat through technological development and increased scale, and its growth trajectory looks positive (with resilience against economic conditions). With strong margins and cash conversion, we see a fruitful financial future ahead for the business.

For further details see:

Copart: Fantastic Margins And Positive Trajectory