AZO - Copart: High ROC Suggests A Quality Company Questionable Entry Price

2023-11-06 17:03:54 ET

Summary

- Copart is a high-quality compounder with a great management team.

- The founder is the board chairman, and the CEO has a great compensation plan.

- Copart has impressive revenue growth, high returns on capital, and strong solvency.

- But current prices do not give us an opportunity.

My Thesis

Copart ( CPRT ) has a unique business model that is not easy to understand. It operates in a relatively small market but is estimated to hold about 40% of the market share. The company possesses high-quality attributes, including high and stable ROCs, steady margins, and robust FCF per share growth , averaging 17% CAGR since 2014.

I believe that Copart has significant growth potential and formidable barriers to entry. However, despite its strong business fundamentals, and while I am usually willing to pay a premium for such qualities, I currently consider the stock to be overvalued as it appears to be priced for perfection.

The Business

Copart operates as an online auction-style marketplace for vehicles or vehicle parts taken off the road due to accidents or being too old. They play a crucial role in the end-of-life cycle for vehicles. Copart forms connections with insurance companies, and when the insurance company decides it's not cost-effective to repair a damaged vehicle, Copart steps in. They take the vehicle to one of their 200 junkyards and list it for auction on their website. In most cases, Copart doesn't purchase the vehicle; they provide the service.

Consequently, the primary sellers are insurance companies, making up 80% of the total, with the remaining portion consisting of banks and other parties selling their vehicles through the Copart platform. Buyers come from all over the world, including dismantlers like LKQ, the largest in America, and private individuals. Developing countries often have a high demand for these vehicles because they offer affordable options.

Copart generates its profits quite effectively, primarily through fees charged to buyers. These fees are calculated as a percentage of the transaction price, and as the transaction price increases, the percentage fee decreases. Additionally, buyers are required to have an annual membership to purchase through Copart, which is usually not an issue for companies.

Copart is estimated to hold a 43% market share in a relatively small yet growing market.

Several key drivers impact this market. Firstly, the total miles driven are increasing, leading to more damage. Secondly, as vehicles age, the likelihood of damage rises, and sometimes it becomes uneconomical to repair them. Moreover, advancements in car technology result in more sophisticated and expensive vehicles, increasing selling prices and the fees that Copart collects.

{kind=link}

One significant metric to gauge Copart's flow of cars is the "total loss frequency."

In the management's view, the long-term drivers, as highlighted in the last confe rence call , are as follows:

" The long-term drivers of total loss frequency, of course, remain unchanged. First, repairs are more expensive and less attractive due to increasing accident severity, vehicle complexity, labor costs and rental car costs; and two, salvage economics are more attractive because the growing economies in Central and South America, Africa and Eastern Europe depend on our damaged vehicles to provide the mobility they need. "

The value that Copart provides to its clients is significant, as it effectively manages the entire process of handling total loss vehicles.

" As we've noted in the past, for a vehicle that will ultimately be totaled, insurance companies often nevertheless incurred literally thousands of dollars in towing, storage estimating teardown costs and appraiser labor, much of which could have been mitigated with streamlined decision-making. "

Management

The founder of Copart is Willis Johnson, a highly respected and ambitious entrepreneur who built Copart from the ground up. The good news is that he currently serves as the Chairman of the Board. Copart operates with a co-CEO model, with Jay Adair serving as the CEO, responsible for the significant success of the company's operational aspects and the stock price. He has a strong operational background, having joined Copart at the age of 19 and learned the business from Willis Johnson in all its forms. The other CEO, Jeff Liaw, has a more financial-oriented role, having served as the CFO in the past.

The management team is known for making decisions that benefit the business in the long term. For instance, they choose to buy their junkyard land instead of leasing it, understanding that this will be more advantageous in the future, as rising lease prices won't erode their profits. They are often candid with analysts, admitting when they don't track certain metrics.

Willis Johnson was known for taking risks with technology ventures and investing heavily in them. This aligns with Copart's plans to grow its FCF through the acquisition of tech ventures.

Jay Adair shows a strong commitment to the shareholders, as his cash salary is only $1 per year. He primarily receives his rewards through stock ownership, which is something investors appreciate. His interests are directly tied to the shareholders' interests, and he has "skin in the game" with 3.71% ownership of the total Copart stocks. This commitment is evident in the proxy statement:

" If the stock price does not increase, Mr. Adair realizes nothing. If the stock price appreciates only modestly, Mr. Adair realizes only modest compensation. On the other hand, outsized gains in stock price appreciation for the benefit of all our stockholders will accrue as well to Mr. Adair. "

Jeff Liaw's compensation follows a similar pattern, with a significant portion of it being tied to stock option awards, which accounted for approximately 74% of his executive compensation package's value in fiscal 2022. This alignment of their interests with the shareholders' interests demonstrates their commitment to the company's success.

Growth & Profitability

Copart achieved an impressive revenue growth of 13% CAGR over the last decade, which is a remarkable accomplishment. Moreover, the long-term drivers for the market remain intact. The expansion of their current yards will not only help in reducing operational costs, especially related to towing but also contribute to improving margins, which, in turn, leads to exceptional operational leverage. It's worth noting that they managed to grow their FCF by more than double the rate of revenue growth over the last decade. While constructing the DCF model, I won't employ the same growth metrics since the company has grown in size, and I aim to take a slightly more conservative approach.

In fiscal year 2023, Copart experienced somewhat slower top-line growth at 10%, while net income grew by an impressive 13.5%. Analysts have set more conservative expectations for the next three years, with a projected 10% CAGR. However, it's important to note that Copart has a history of surpassing these expectations, so there is potential for higher growth than analysts currently anticipate.

I appreciate Copart's high and stable margins, as they provide the business with the flexibility to avoid cutting its capital expenditure for future investments or reducing shareholder compensation, which, in Copart's case, takes the form of buybacks. Additionally, these margins are on an upward trajectory, which is a significant driver of long-term FCF per share growth, alongside the impact of buybacks. Furthermore, Copart boasts higher margins than its primary competitor.

{kind=link}

These higher margins contribute to what I consider the most important indicator for long-term success, alongside top-line growth: returns on capital. High and growing returns on capital, which create a significant spread between the WACC, indicate future compounders, as research by Morgan Stanley has shown.

Furthermore, from time to time, Copart's management decides to return capital to shareholders rather than seeking additional future growth. This approach involves reducing a substantial portion of outstanding shares, which significantly contributes to FCF per share growth. In recent article s, I discussed two other companies, AutoZone ( AZO ) and Sprouts Farmers Market ( SFM ), which consistently reduce their share counts, and I anticipate that this will be a substantial driver of value. Copart is not paying dividends, but I'm comfortable with this, knowing that their excellent management can deliver exceptional investments or acquisitions with their cash.

Solvency

Copart essentially has no debt (just $10 million), holds almost a billion dollars in cash, maintains an outstanding current ratio, boasts an Altman Z-Score suggesting no financial distress, and carries a very low debt-to-equity ratio. It's a highly solvent company.

Valuation

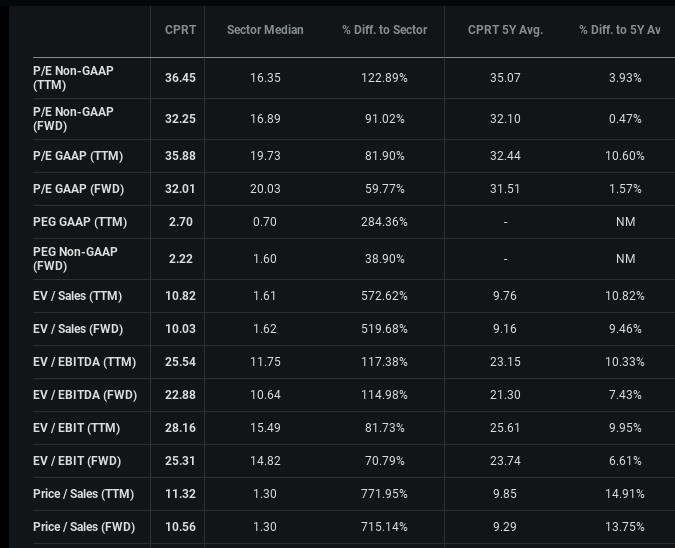

I prefer to purchase companies when they are trading below their historical average multiples. However, this isn't the case with Copart, and it's becoming increasingly challenging to find quality companies at affordable prices. Additionally, the FCF yield for Copart is relatively low at 1.9%, and I typically look for it to be above 3%. There are many quality companies currently available with FCF yields exceeding 4%.

{kind=link}

For the DCF analysis, I'll employ two scenarios: one based on past growth rates and a more conservative approach.

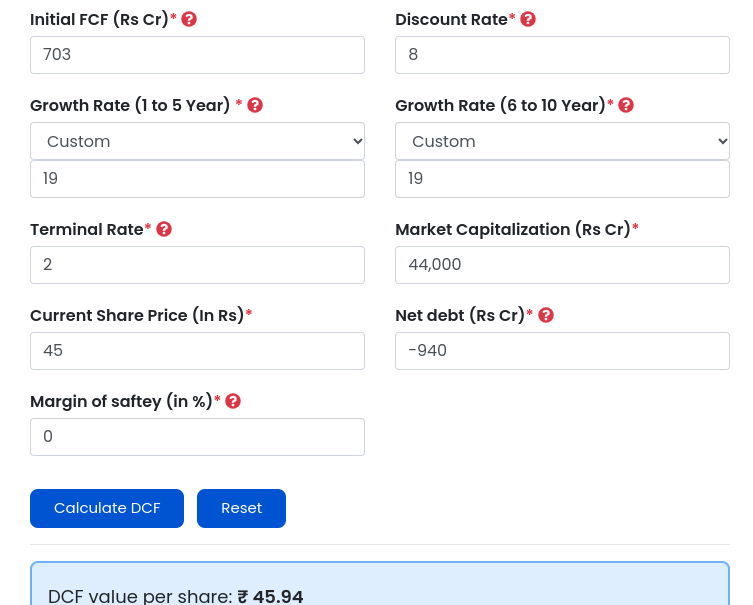

In the "past growth" case, I'm using a 2% terminal growth rate, an 8% WACC , a 22% FCF margin, and FY23's revenue. The growth rate is set at 19%, reflecting the 10-year FCF CAGR . The resulting intrinsic value is $45, indicating a well-valued company. However, this is an optimistic scenario, given that the company's last year growth and analyst consensus typically lean toward the low teens.

{kind=link}

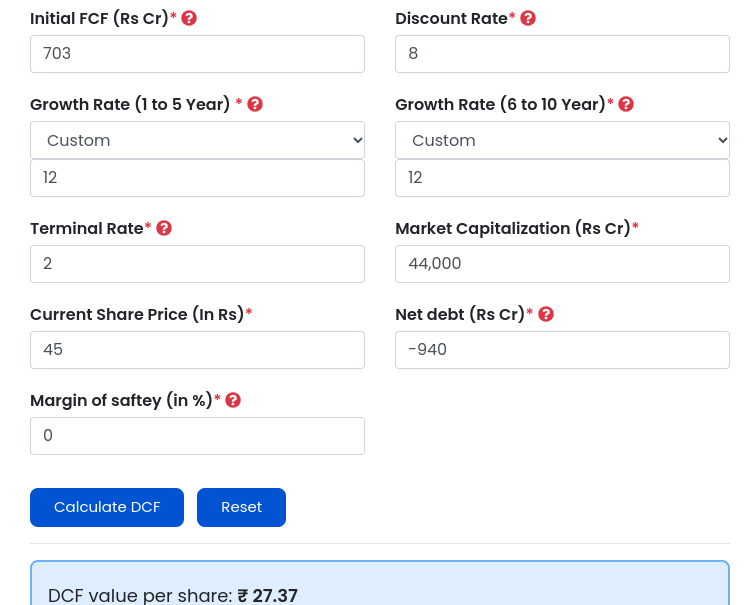

In the more conservative case, I'll use the same inputs except for the FCF growth rate, which will align with the anticipated EPS growth of around 12% for the next 3 years. In this scenario, the derived result suggests an overvaluation of more than 60%, with an intrinsic value of $27. While I don't believe this will be the case, I do consider the bullish past growth scenario to be too optimistic.

It's worth noting that in many instances, quality companies like this one may not fit neatly within the DCF model, as their unique qualities may not align perfectly with the model's assumptions. However, I'm not entirely certain if this is the case here.

{kind=link}

Risks

There are several potential risks to consider:

1. Autonomous Vehicles: The advent of autonomous vehicles could reduce accidents on the road, impacting the salvage vehicle market. However, it's worth noting that widespread adoption of autonomous vehicles may still be quite some time away.

2. Fuel and Wage Prices: Fluctuations in fuel and wage costs could affect Copart's main operational expenses, potentially impacting profitability.

3. Vehicle Safety Technology: As cars become safer with more advanced technologies to prevent accidents, there might be a decrease in salvageable vehicles, which could affect Copart's supply.

4. Valuation: The current stock price suggests extensive future growth, which may be achievable but could also be somewhat optimistic. It's important to carefully assess the valuation and consider other investment opportunities in the market.

Conclusions

I view Copart as a high-quality company with a reasonably wide moat, high ROCs, promising future growth prospects, and excellent management, which includes significant skin in the game. Furthermore, I perceive it to have relatively low risks.

However, given the current stock prices, I find it to be on the optimistic side, and I would rate Copart as a HOLD. It's certainly worth keeping an eye on, and I will add it to my watchlist.

I appreciate your thoughts on this, and it's always valuable to assess investments carefully, especially when they appear to be trading at a premium.

For further details see:

Copart: High ROC Suggests A Quality Company, Questionable Entry Price