CPRT - Copart: Understanding The Reasons Behind Its Valuation

2023-11-19 11:52:11 ET

Summary

- Copart has experienced significant growth in the last decade, with more than a 1000% increase in stock returns and a 300% expansion in topline.

- The company's moat, built through its online and physical presence, and the services it offers its customers are difficult to replicate and provide a big competitive advantage.

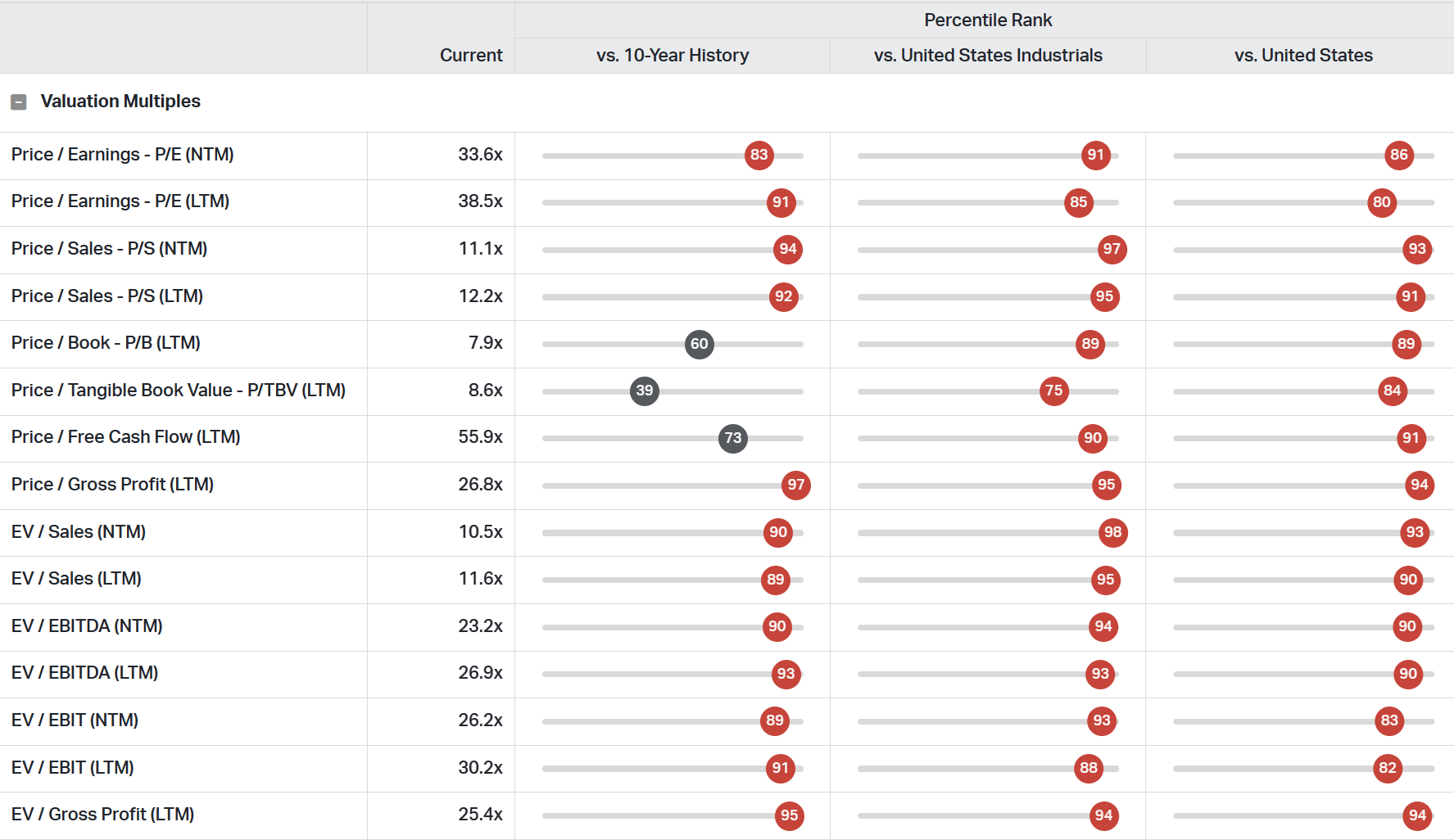

- Copart's consistent growth, high return on invested capital, and strong financial position along with a bright future that comes with EV dominated world could be the justifications behind its valuation.

On the surface, Copart ( CPRT ) did not seem like a particularly enticing business to me. It operates around the Auto sector and serves a very niche segment. Auto companies themselves haven't done too well for investors and my first guess was not to hope too much from the companies tied to this sector. But boy was I proven wrong! In the last decade alone the stock has returned 1000% and the topline has expanded by almost 300%. Digging further, I saw that its valuation multiples have also expanded rapidly.

Nearly all price ratios for the company, both forward and lagging, against its history and the industrial sector are close to the higher end for the stock.

{kind=link}

Naturally, I wanted to understand what is driving the sentiment for this stock. This company is in a cyclical industry and I wanted to understand why investors are willing to pay a premium to own this company in the current environment. I realized it could be more than one reason.

The moat

I believe investors have become aware of the moat developed by this business and more investors are flocking to the same realization.

Copart, Inc. is a company that specializes in online automotive auction services. Its business model is primarily centered around providing a platform for the buying and selling of used and salvage vehicles. Its business model could be summarized as follows -

-

Vehicle Auctions (Selling Side) : Copart operates an online auction platform where various parties, such as insurance companies, car dealerships, rental companies, and individual sellers, can list vehicles for sale. These vehicles may include damaged, salvage, or non-operational cars, trucks, motorcycles, and other types of vehicles.

-

Bidding Process (Buying Side) : Registered buyers, which can include automotive rebuilders, scrap yards, exporters, and individual consumers, can place bids on the listed vehicles. The auction process is competitive, and as auctions go, the highest bidder at the end of the auction wins the vehicle.

-

Logistics and Transportation (Connecting) : Copart manages the logistics of moving purchased vehicles from the seller's location to the buyer. This includes vehicle transport, storage, and handling services.

-

Title Processing : Copart assists with the transfer of titles and relevant paperwork for the sold vehicles.

If I have to say it in one sentence, the company provides end-to-end management of end-of-life or close-to-end-of-life vehicles!

The moat of the company has been built in the following ways -

Network Effect (Physical and Digital):

Copart's online and physical presence work in conjunction with each other and is incredibly hard to replicate. Online presence means having a big pool of buyers and sellers using the platform for their services, which in effect means a virtuous cycle of more buyers and sellers flocking to the platform (network effects are one of the strongest moats and are also one of the hardest to crack). What is interesting here is the fact that this is greatly supplemented by a physical network that provides storage, logistics, and transportation. The physical network is tough to replicate due to permits around obtaining operating salvage lots. Its yard footprint has been built over a long period aided by acquisitions and a new entrant cannot replicate this within any small timeframe.

Value Added Services

The company offers a suite of value-added services designed to enhance the overall customer experience and create lasting engagement. These services not only streamline the competitive bidding process but also make the platform inherently sticky for its users:

-

Advanced Bidding Features : The inclusion of internet bidding, internet proxy bidding, and virtual sales powered by their platform VB3 elevates the competitive bidding process, providing users with a sophisticated and efficient platform.

-

Mobile Accessibility : The company's mobile applications empower members to engage in auctions, search for vehicles, create watch lists, and bid in multiple languages from any location, ensuring a seamless and convenient experience.

-

Tailored User Experience : Leveraging predictive analytics through collaborative filtering, the Recommendations Engine feature suggests similar makes and models based on individual member behavior, delivering a personalized and engaging browsing experience.

-

Instant Purchase Options : The Buy It Now feature offers members the flexibility to immediately purchase pre-qualified vehicles at a set price before the live auction, enhancing convenience and efficiency.

-

Negotiation Opportunities : The Make An Offer option allows members to submit offer amounts on selected vehicles, providing a negotiation avenue and the possibility of securing a purchase before the live auction.

-

Multilingual Notifications : Email and text notifications, available in numerous languages, keep potential buyers informed about vehicles matching their preferences, contributing to a more inclusive and responsive service.

-

Comprehensive Vehicle Information : The company ensures transparency and accessibility by providing digital imaging of each vehicle and scanning essential documents, including titles and invoices, all accessible online.

-

Interactive Counter-Bidding : The platform's interactive online counter-bidding feature empowers sellers to directly counter-bid the current high bidder, adding a layer of engagement and negotiation to the auction process.

The compounder

The second big reason for its valuation could be due to how consistent the company is in terms of growth and how efficient it is in using capital to generate returns, leading to high ROIC.

The company has been logging double-digit growth both in terms of top and bottom line for most of the last decade. It has also been able to convert this to consistent growth in operational cash flows which have also mostly logged double-digit growth.

Consistent Double-Digit ROIC

Consistently achieving a double-digit Return on Invested Capital is a positive indicator for a company as it signifies the efficient utilization of capital to generate returns i.e. it suggests that the company is adept at deploying its financial resources in a manner that yields substantial profits relative to the amount of capital invested. This efficiency is crucial for sustaining long-term growth and creating value for shareholders often indicative of a company's competitive advantage and operational excellence.

What is most impressive about this business is the fact that the company has been able to achieve all this growth and return value to shareholders while maintaining a spotless balance sheet. It paid down most of its debt in 2022 and currently has a cash position alone of $2.3B.

Growth that isn't slowing down

The third and final reason for its valuation is that recent quarters have further proved that this company is not slowing down. For the latest quarter, the company reported revenues, gross profit, and net income of approximately $1B, $457M, and $348M, correspondingly. These figures reflect a revenue upswing of $114M, equivalent to a 12.9% increase; a gross profit surge of $76.0M, representing a 19.9% rise; and a net income growth of $84.1M, reflecting a substantial 31.9% increase, all compared to the corresponding period in the previous year. The fully diluted earnings per share for the same period in 2023 were $0.36, showcasing a notable increase of 33.3% compared to the $0.27 reported last year.

I believe the future will continue this trend as we are increasingly transitioning into a world of EV-dominated vehicles and some indicators indicate salvage could benefit from this shift. While the rise of electric vehicles may bring challenges for traditional auto salvage, it also presents opportunities for salvage yards to adapt and specialize in the growing market for salvaging electric vehicle components, especially for companies that already have enough footprint.

One of the first countries to have mass EV adoption is Norway and a lot can be learned from here. The understanding was that EVs would not break easily and undergo less wear and tear but salvage companies in Norway are seeing enough volume and are generating demand for salvaged parts, especially batteries. Battery recycling specialists face the challenge of securing a consistent supply, particularly as the primary source of electric vehicle batteries shifts to those sourced from retired vehicles rather than defective batteries from manufacturers' assembly lines. Companies already involved in processing decommissioned vehicles are strategically positioned to play a role in managing batteries.

At the end of the day, it’s going to be the people who have the ability to collect and distribute, and sell those cars. They physically have the yard space and the buyer network... The guys who are doing the actual grinding down and doing the refining of the component parts aren’t in the business of running 17,000 acres of auction yard like Copart is...

- Jefferies analyst Bret Jordan

Minor Risks

With the company benefitting well from the moat it has developed, the risks become less transparent. Fundamentally, the company is in a strong position but it may have to work harder for its future growth. The low-hanging fruit is pretty much gone in its home market, the U.S. and it is increasingly looking at international expansion to fuel its next wave of growth. Assimilating the challenges associated with each new market would take its course and this could start reflecting on its costs.

The other less apparent risk is related to climate change of which the company would have no control. Extreme events such as hurricanes can have an impact in two ways -

1. Drastically increase the amount of available supply for which the demand may not exist

2. Run into yard constraints and additional labor costs to process the volume of vehicles which will have an impact on operating results (which is precisely what occurred after Hurricane Ian)

Presently, I believe both of these risks are minor and does not pose a threat to the business model of the company.

Closing Thoughts

Even though the valuation looks expensive and over the short term the stock may be vulnerable in this regard, I believe it is a buy over the long term. The moat it has developed is hard to beat and it has demonstrated the power of its moat very well through its financial performance. With the ongoing EV revolution, it will again be one of the prime beneficiaries and its top line could expand even further. I will be adding a small position in my portfolio now and will look to add to my position when the valuation gets better.

For further details see:

Copart: Understanding The Reasons Behind Its Valuation