INVH - Copy The 'Smart Money' On Wall Street By Buying Invitation Homes Stock

2024-01-10 07:00:00 ET

Summary

- Wall Street is turning to building entire suburban neighborhoods for renting as a strategy in the competitive U.S. housing market.

- Institutional investors see single-family homes as a more attractive option than apartments due to stronger rent growth and longer tenant stays.

- Invitation Homes Inc., a major owner and operator of single-family homes for lease, is a top-tier landlord with a focus on build-to-rent communities and a standardized approach.

This article was coproduced with Leo Nelissen.

I’m not breaking any news when I say that it’s tough to buy a new home, as (potential) homebuyers are dealing with a toxic mix of headwinds, including elevated rates, high home prices, and general pressure on their finances caused by sticky inflation (core inflation is still at 4%!).

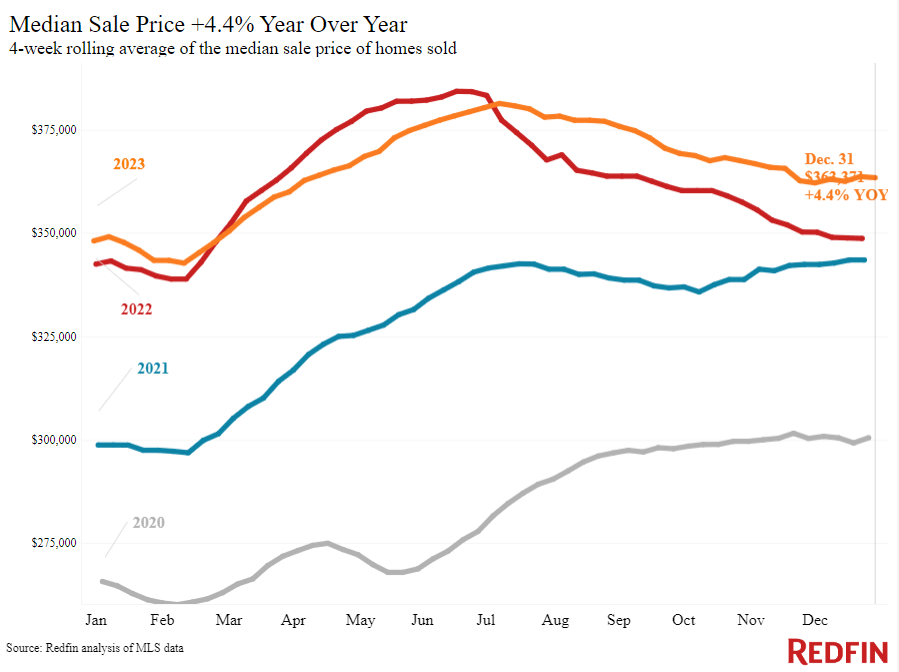

For example, Redfin reported that the median home sales price in the United States ended the year 4.4% higher compared to the prior year at roughly $363 thousand.

{kind=link}

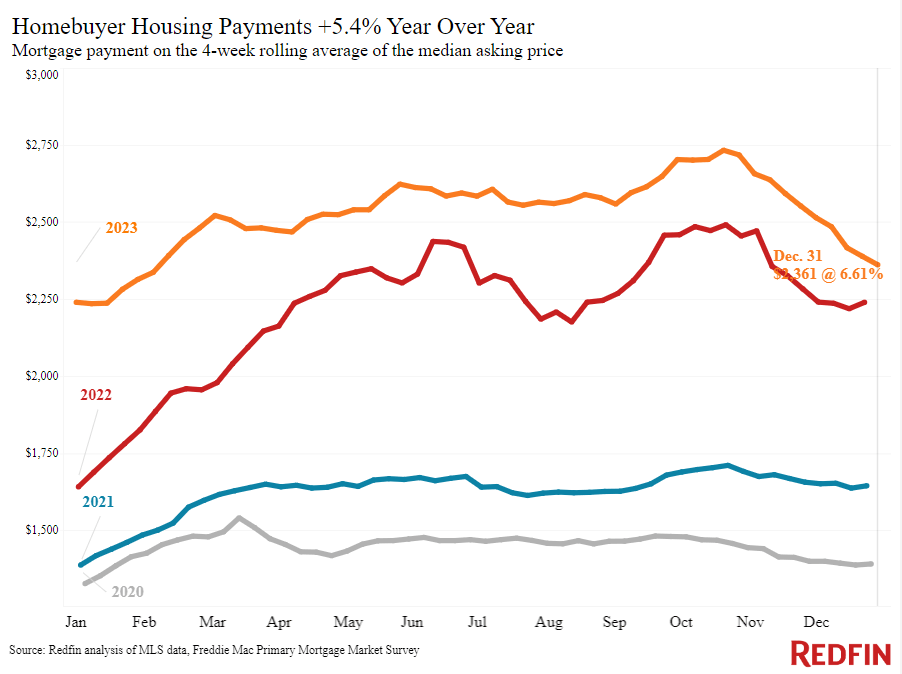

At a 6.6% rate, homebuyers need roughly $3,400 per month to service the mortgage payment on a median home.

In 2020, that number was consistently below $1,500, which explains why housing supply is so poor, as people who have locked in low rates aren’t looking to take on more expensive debt.

Hence, they stay put.

{kind=link}

That said, do you know what’s even worse?

Wall Street is now competing for single-family homes.

The Wall Street Journal just ran the headline “Wall Street Moves Into The Neighborhood.”

{kind=link}

According to the report , in the increasingly competitive U.S. housing market, big investors are turning to a new strategy: building entire suburban neighborhoods for renting.

With interest rates high, housing prices soaring, and traditional channels limited, institutional investors find it challenging to meet return goals.

While institutional investors already own 55% of U.S. apartments, a trend we have often discussed in our Investing Group, they now see single-family homes as a more attractive option due to stronger rent growth and longer tenant stays.

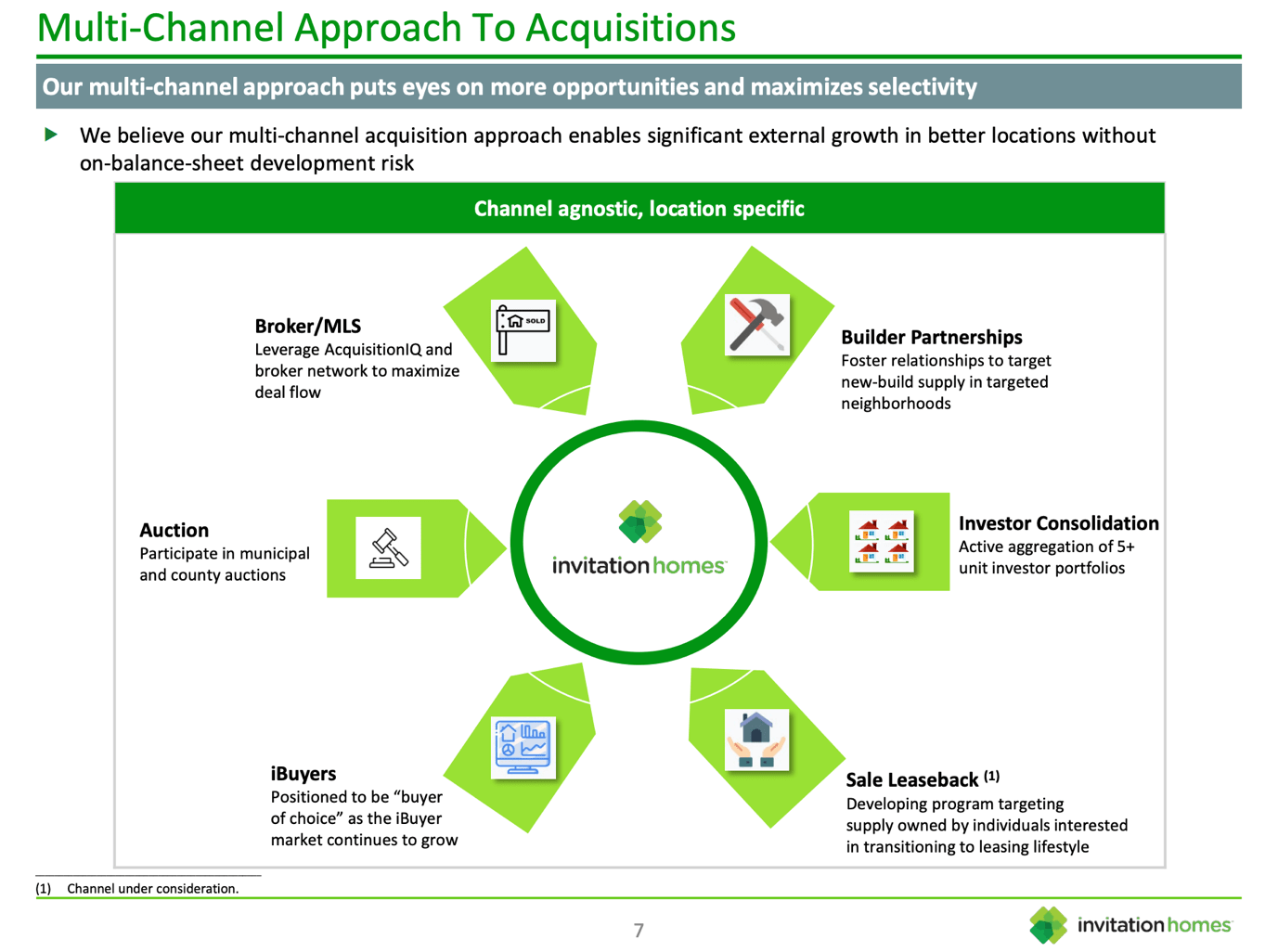

However, the traditional method of acquiring individual houses is becoming inefficient.

Additionally, it's harder for investors to bulk-buy newly constructed houses as the limited housing inventory leads to immediate purchases by regular buyers.

To overcome these challenges, Wall Street investors are increasingly focusing on constructing new neighborhoods exclusively for renting, known as "build-to-rent" communities.

This model, while not entirely new, is gaining traction.

Approximately 10% of new housing construction is now dedicated to build-to-rent, with 900 such neighborhoods nationwide. This approach allows investors to consolidate rental properties, making maintenance more cost-effective.

Some companies, like American Homes 4 Rent ( AMH ), are independently constructing thousands of new family homes, while others, like Invitation Homes ( INVH ), form partnerships with housebuilders, albeit at a higher cost.

This brings me to Invitation Homes, which is my favorite way to copy the smart guys on Wall Street.

What Makes Invitation Homes So Special?

Let’s start at the top for the people who are new to the INVH ticker.

Invitation Homes is a major owner and operator of single-family homes for lease, owning over 80,000 homes across 16 markets in the United States going into 2023.

Positioned in sought-after neighborhoods, the company makes the case that it addresses the growing demand for leasing lifestyles, offering quality residences with proximity to jobs and good schools.

{kind=link}

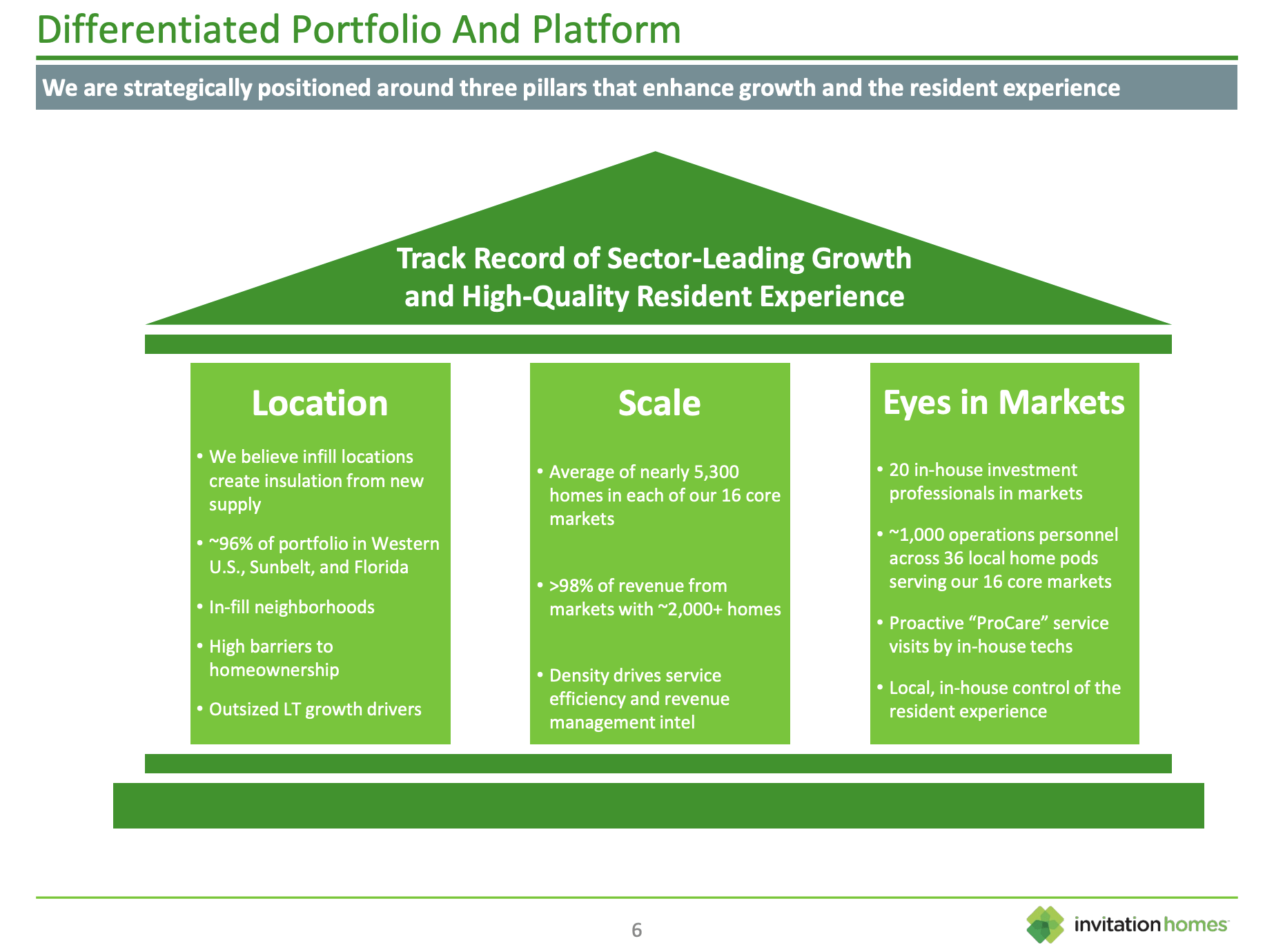

Operating in markets with strong demand, high entry barriers, and rent growth potential, primarily in the Western United States, Florida, and the Southeast, Invitation Homes focuses on strategic mergers and acquisitions for efficient market and asset selection.

Essentially, the company’s portfolio captures the benefits of local density and economies of scale, creating a vertically integrated platform.

{kind=link}

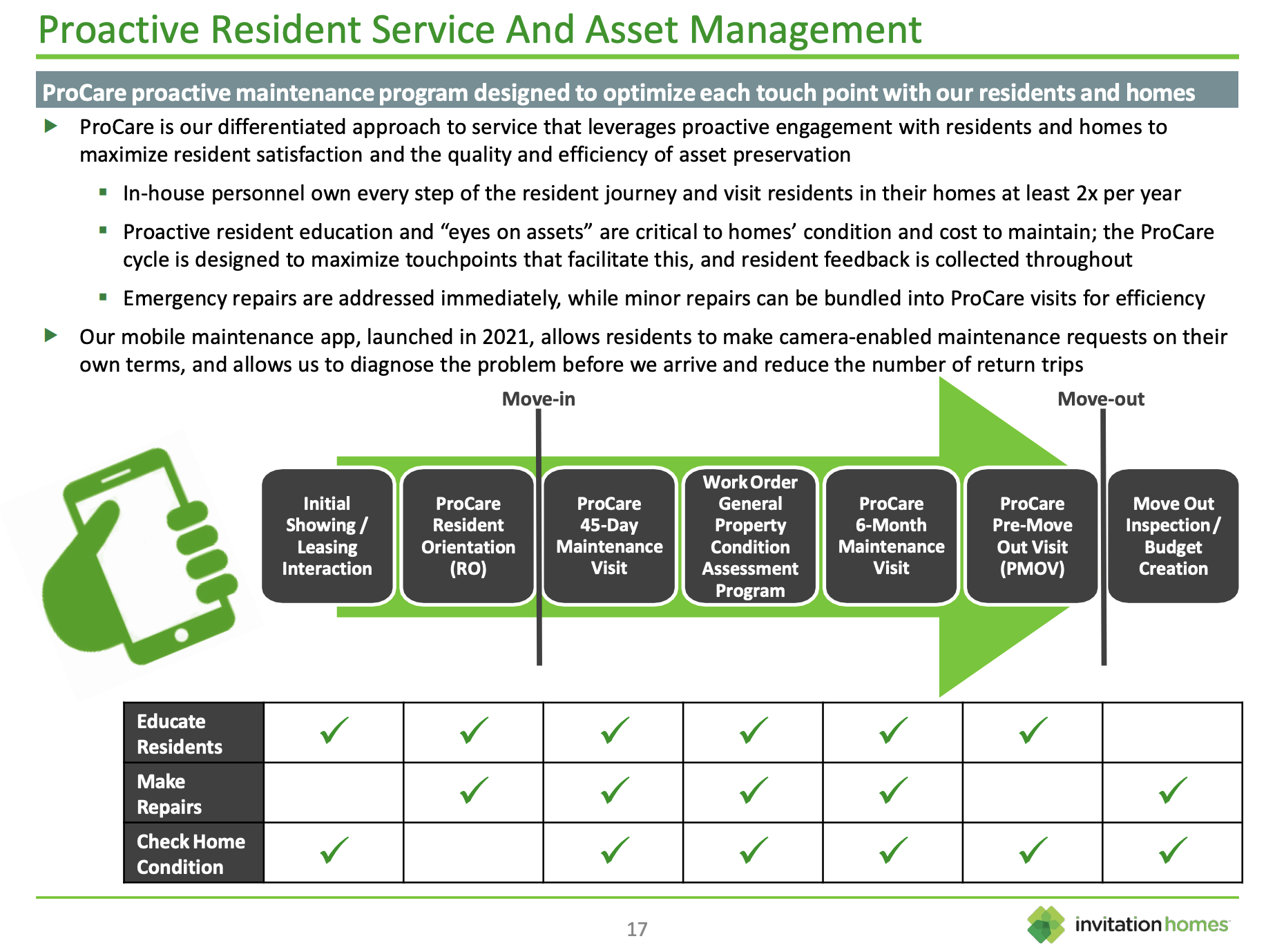

In other words, to effectively and efficiently manage its massive portfolio, the company engages with residents through digital platforms.

This digital marketing approach, coupled with initiatives like Resident Appreciation Month, sets them apart in creating a sense of community and connectivity among residents, which is a win-win.

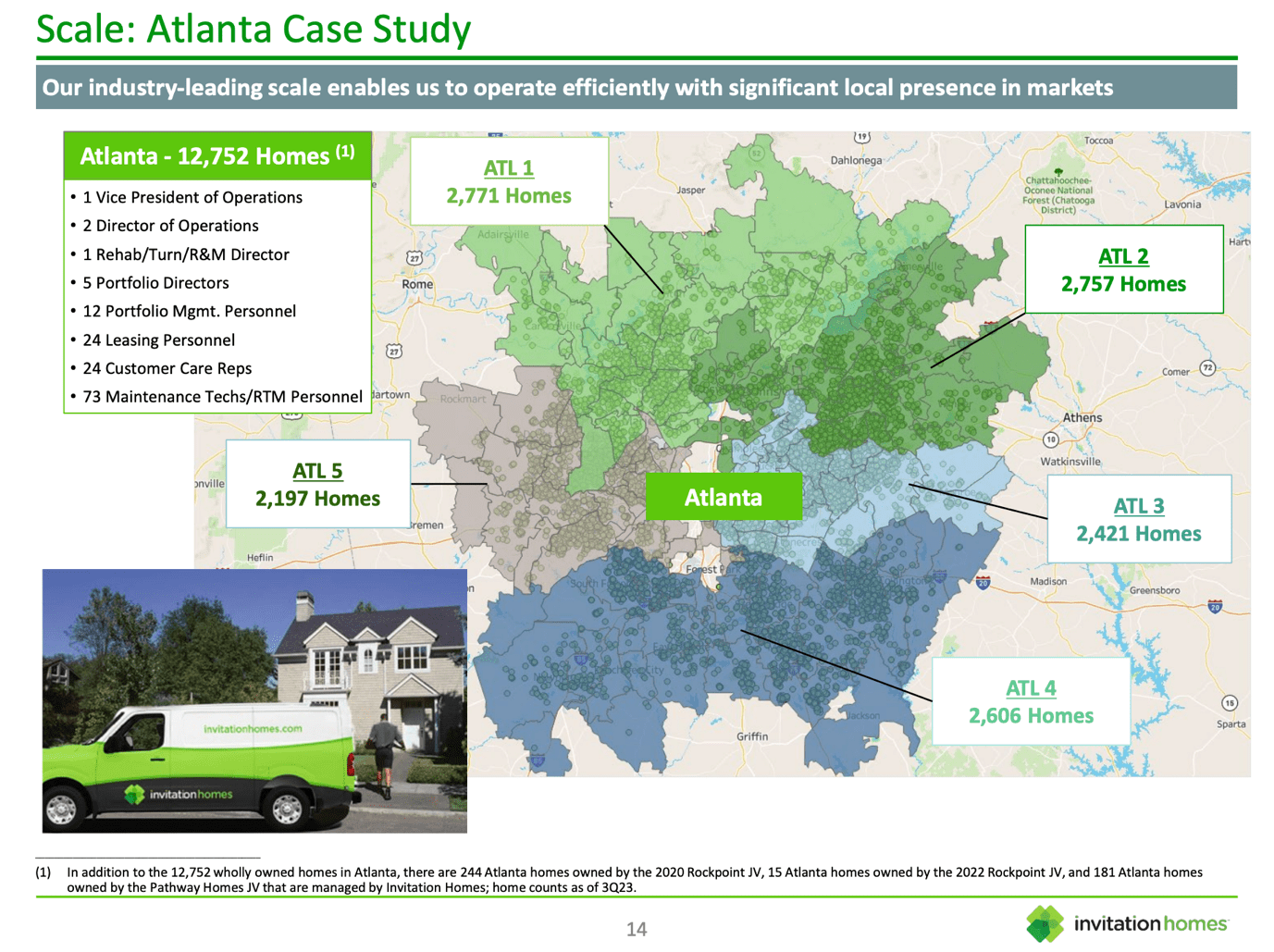

To give you an example, in Atlanta, the company owns roughly 12,800 homes. These homes are managed by one VP of Operations, 2 Directors of Operations, and a number of supporting employees like Portfolio Directors, leasing personnel, and maintenance people.

As we can see below, the company has just 73 maintenance employees in this region, which is truly impressive.

{kind=link}

Adding to that, the overview below shows the company’s highly standardized approach, which minimizes employment and maintenance costs while streamlining operations and renter comfort.

{kind=link}

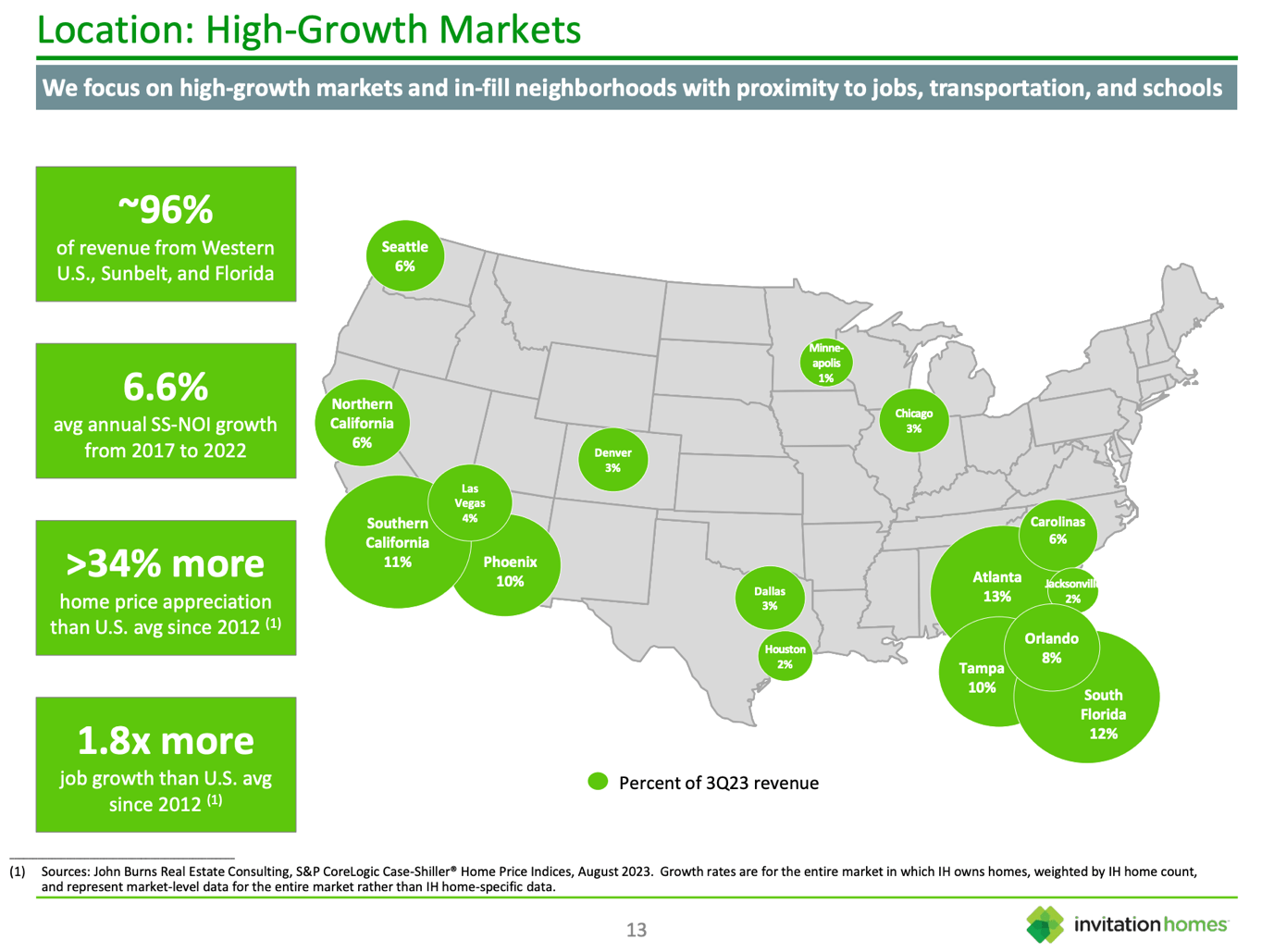

Furthermore, its most recent numbers show that the company owns most of its assets in highly attractive regions.

As I already briefly mentioned, the Western U.S., Sunbelt, and Florida account for almost all of its revenue.

Between 2017 and 2022, the company has grown its same-store net operating income (“NOI”) by 6.6% per year, benefiting from more than 34% home price appreciation on top of the U.S. average since 2012.

The markets it serves have had 1.8x higher job growth since 2012.

{kind=link}

It also has an attractive dividend.

After hiking its dividend by 7.7% on December 8 , the company currently pays $0.28 per share per quarter. This translates to a yield of 3.3% .

The five-year dividend CAGR is 25% , which is skewed by aggressive dividend growth after the company went public.

Back in 2017, the company initiated a $0.06 per share quarterly dividend, which it hiked by 33.3% on August 4, 2017.

Seeking Alpha

The good news is that analysts expect the company to generate $1.49 in 2023 adjusted funds from operations (“AFFO”), which translates to a 75% payout ratio .

This means the dividend is well-protected with room for consistent longer-term growth, as these are the AFFO growth expectations from analysts:

- 2023: +6%

- 2024: +4%

- 2025: -5% (This number is based on just one analyst estimate and needs to be taken with a grain of salt.)

The company also comes with a BBB credit rating , which is an investment-grade rating.

At the end of the third quarter , the company had $1.8 billion in available liquidity , consisting of unrestricted cash and undrawn capacity on its revolving credit facility.

The net debt-to-EBITDA ratio stood at 5.5x, aligning with the lower end of the targeted 5.5x to 6x range.

The outstanding borrowings carried a weighted average interest rate of 3.8% , while the majority of its debt had a fixed rate or was swapped to a fixed rate.

Speaking of the third quarter, let’s take a closer look at its environment and financial performance.

INVH Thrives In This Market

Like the Wall Street professionals, INVH is betting big on the U.S. housing market.

During the third quarter of 2023, Invitation Homes capitalized on unique external growth opportunities.

This included a significant portfolio acquisition of 1,870 wholly-owned homes for $650 million.

The company disclosed a year-one yield in the mid-5%s, with expectations for it to grow into the 6%s within the next year.

One reason for its aggressive buying is shortages, which I discussed at the start of this article.

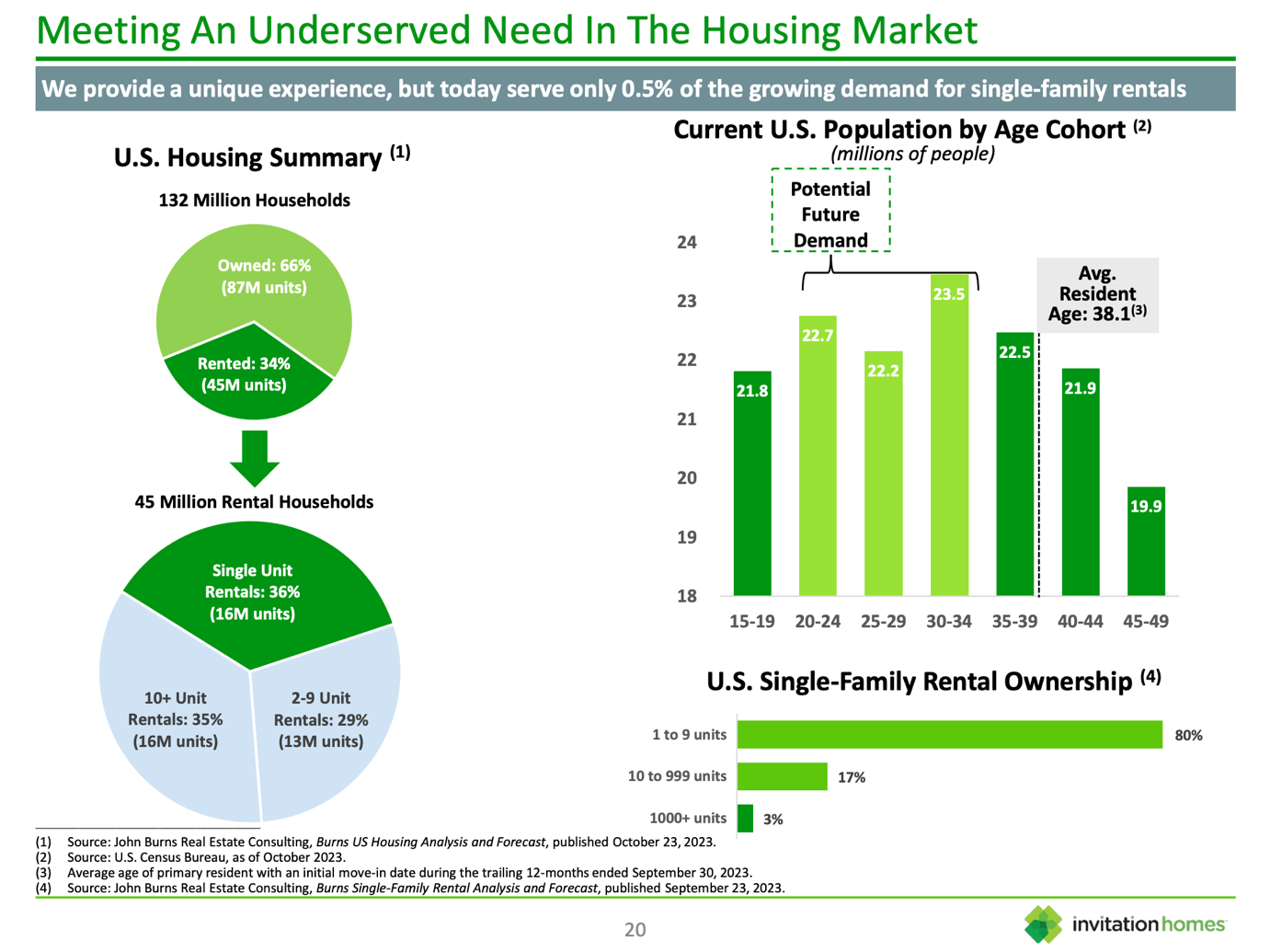

According to INVH, it operates in the context of a significant housing shortage in the United States, estimated to be several million units.

This imbalance in supply and demand continues to be a driving force behind the company's positive performance. The demand for single-family homes for lease remains robust, fueled by various factors.

{kind=link}

One key driver is the changing landscape of homeownership costs. According to the company, leasing a home through Invitation Homes is now over $1,100 a month cheaper than owning, on average, in the company's markets.

This cost advantage, combined with the flexibility and convenience of leasing, positions Invitation Homes favorably in the market.

Furthermore, Invitation Homes has strategically positioned itself to meet the growing demand for single-family homes for lease.

This demand is attributed to favorable demographics, including a desire for flexibility and convenience, coupled with rising mortgage rates, making leasing a more attractive and affordable option compared to owning similar homes.

{kind=link}

These developments also translate to strong earnings.

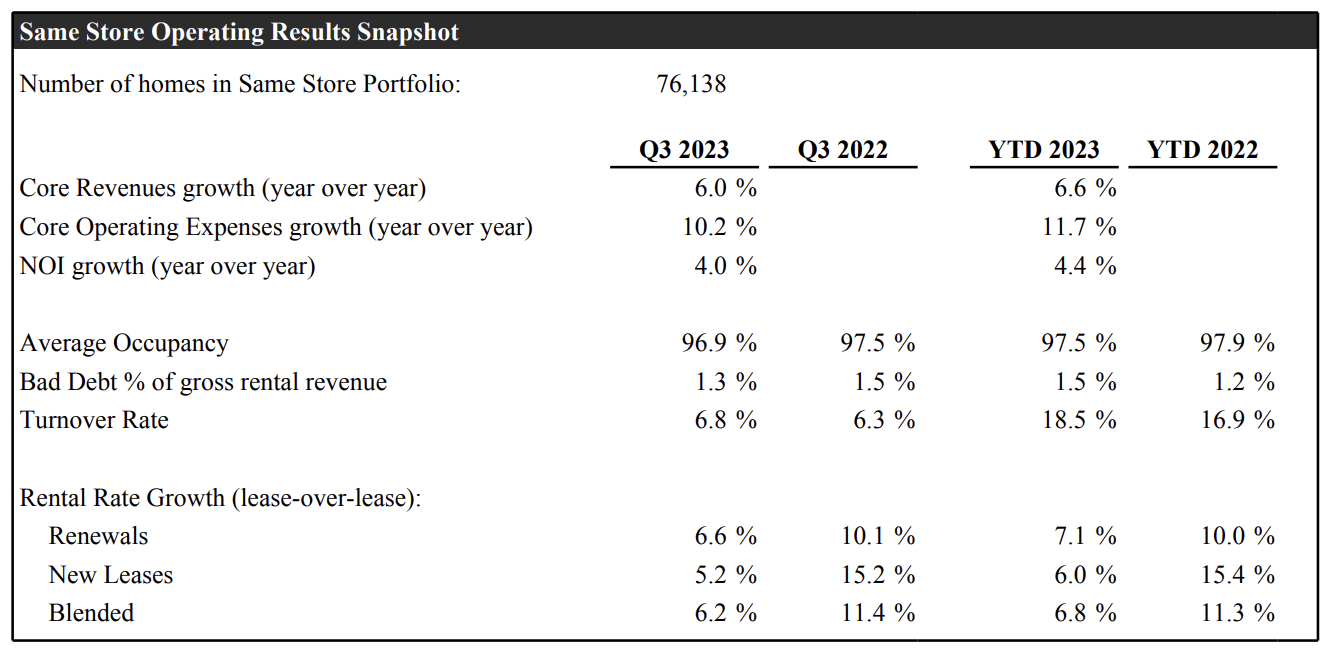

During the third quarter, the company’s same-store NOI grew by 4% year-over-year, which was in line with expectations.

This growth was supported by a 6% year-over-year increase in same-store core revenues.

The key drivers included a 6.2% growth in average monthly rental rates and a 20-basis point improvement in bad debt, meaning its tenant health has improved.

In general, Invitation Homes continues to attract high-quality residents, with new residents having a combined household income of over $142,000 per year.

On top of that, the company's partnership with Esusu, announced in July, has enrolled over 160,000 residents in a free credit reporting program.

Approximately half of these residents have seen an improvement in their credit scores, with an average increase of over 20 points.

- The occupancy rate for the third quarter was 96.9% , surpassing pre-pandemic norms by 120 basis points.

- Blended rent growth for the same period was 6.2%, consisting of renewal rent growth of 6.6% and new lease rent growth of 5.2%.

{kind=link}

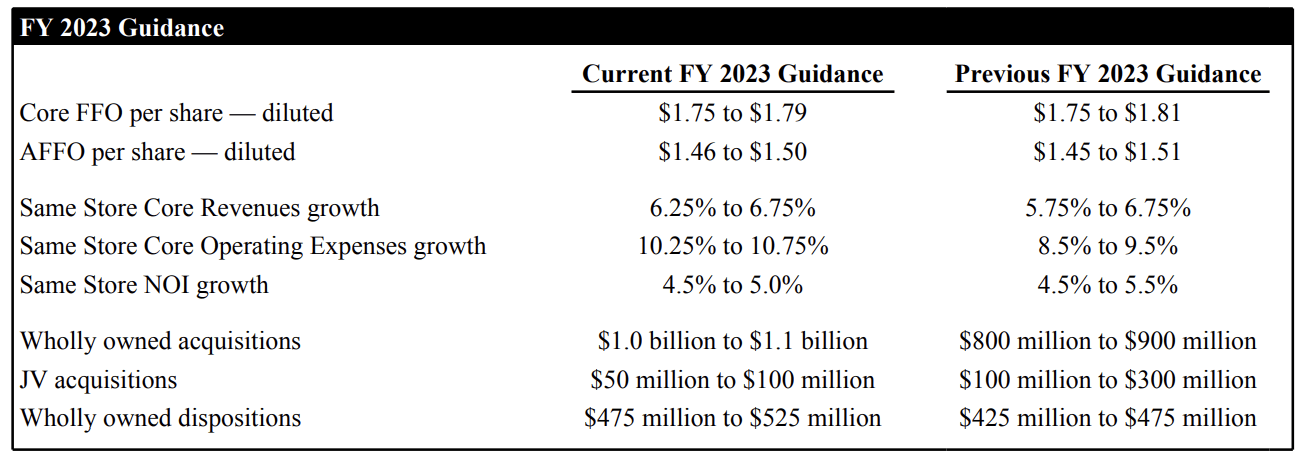

Furthermore, the company updated its full-year guidance.

The same-store NOI growth range for 2023 was narrowed to a new range of 4.5% to 5%.

This adjustment was based on a refined range for same-store core revenue growth (6.25% to 6.75%) and revised same-store core expense growth (10.25% to 10.75%).

During the earnings call , the company explained that the increase in same-store core expense growth was primarily due to higher property tax expenses in Florida and Georgia.

The expected growth in same-store property tax expenses for the full year was revised to approximately 10% to 10.5%.

The guidance also tightened the ranges for expected core FFO per share and AFFO per share for the full year 2023, with anticipated growth of 6% at the midpoint for core FFO per share.

{kind=link}

So, what about the valuation?

Valuation

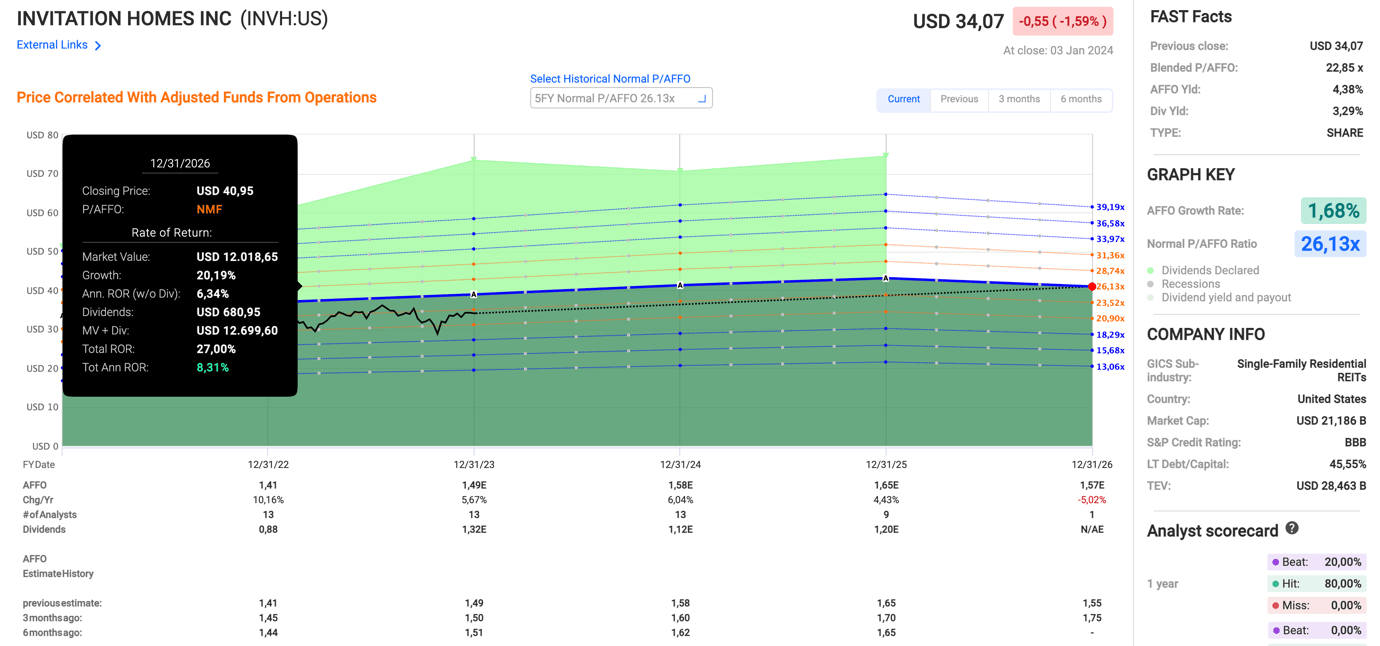

INVH is currently trading at a blended P/AFFO ratio of 22.9x, which is below its five-year normalized valuation multiple of 26.1x.

Furthermore, in light of the aforementioned expected AFFO growth rates (these are also visible in the chart below), the company could return 8.3% per year through 2025 – including its 3.4% dividend . It has returned 9.1% per year since it went public.

{kind=link}

However, although I am bullish on the stock and believe that it will be able to outperform its peers on a prolonged basis, I have put INVH on my watchlist instead of my portfolio for a few reasons:

- The market has priced in six rate cuts over the past two months, which means that any sign of sticky inflation could cause rates to rise again, which is bearish for real estate stocks.

- A normalized valuation of 26.1x is only warranted if the company is able to maintain elevated annual growth. Although its growth rates are strong, they are below the five-year average.

In October, INVH was trading below $29. It is trading at $34 now.

I would like to see it come down a bit before jumping in.

Nonetheless, the main message here is that INVH is a terrific stock that allows long-term investors to copy Wall Street investors by buying a top-tier landlord capable of long-term dividend growth with some of the best assets in the real estate sector.

Takeaway

Investing in Invitation Homes provides a strategic opportunity to copy Wall Street professionals.

As the housing market faces challenges, INVH stands out with over 80,000 single-family homes strategically located in high-demand areas.

The company's focus on build-to-rent communities, digital engagement, and a standardized approach ensures operational efficiency and resident satisfaction.

INVH's strong financial performance, attractive dividend yield of 3.3%, and projected AFFO growth affirm its position as a top-tier landlord.

Despite current valuation considerations, INVH remains a compelling long-term investment , offering a chance to align with Wall Street's new investment choices.

iREIT®-MarketVector™ Quality REIT Index (Quality and Value Scores)

{kind=link}

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Copy The 'Smart Money' On Wall Street By Buying Invitation Homes Stock