TEVJF - Corcept Therapeutics: Korlym Overhang Appears To Be A Drag On Valuation Upside

Summary

- Despite settling one of its disputes surrounding the Korlym label, investors were major sellers of Corcept equity in Q4 FY22.

- Question is, does the selloff represent a value proposition, and do current valuations make sense.

- On close inspection, we believe that paying 21x forward earnings and 4.7x book value isn't justified in this instance.

- Net-net, we rate CORT a hold.

Investment Summary

The substantial repricing of equities across 2022 has widened the list of potential opportunities to allocate risk capital towards in the new year. Noting the selloff in Corcept Therapeutics ( CORT ) at the back end of FY22', following a recent settlement with its Korlym label, we were immediately drawn to the prospects of any upside capture that could be on the table.

After rigorously analyzing all of the contributing factors to the investment debate, we believe there are more selective opportunities elsewhere for now, and rate CORT a hold. Here I'll run through our investment findings in greater detail.

Korlym overhang appears to be a resounding factor for CORT

Korlym [drug name: mifepristone], is CORT's main revenue driver, since being approved in 2012. The label is indicated to treat hyperglycemia due to hypercortisolism in adults diagnosed with endogenous Cushing’s syndrome. For reference, endogenous Cushing's syndrome is a rare disorder that is caused by excessive production of the hormone cortisol by the adrenal glands. Cortisol being the hormone that helps regulate the stress and immune response in the body. Symptoms are broad and generally quite inhibiting on the affected individual.

The Korlym journey has been fraught with challenges over the last 2-3 years, namely due to the challenges to CORT's patent on the drug, starting with Teva Pharmaceutical ( TEVA ) in 2020. Back in November FY20', the U.S. Patent Trial and Appeal Board upheld the validity CORT's patent claim , saying TEVA " has not shown by a preponderance of the evidence that claims 1-13 of the '214 patent would have been obvious over the combination of the Korlym Label and Lee ", and, that " [i]n consideration of the foregoing, it is hereby ordered that [Teva] not proven by a preponderance of the evidence that claims 1–13 are unpatentable;.... "

In December 2021. the U.S. Court of Appeals for the Federal Circuit upheld the original decision and denied TEVA's attempt to invalidate the Korlym patent once again. The case is still in arbitration, however management noted on the Q3 earnings call that should the court rule CORT's favour, TEVA would be "barred from marketing generic Korlym until 2037 when the 214 patent expires". On the other hand, if it rules in TEVA's favour, it will head to trial to argue or a favourable judgement.

Aside from that, in 2021, CORT also sued Hikma Pharmaceuticals USA Inc. ("Hikma") after Hikma attempted to file an abbreviated new drug application ("ANDA") to sell a generic version of Korlym in the marketplace. CORT reached a settlement with Hikma in December 2022, with the terms allowing it to market a generic version of Korlym not until October 1st, 2034.

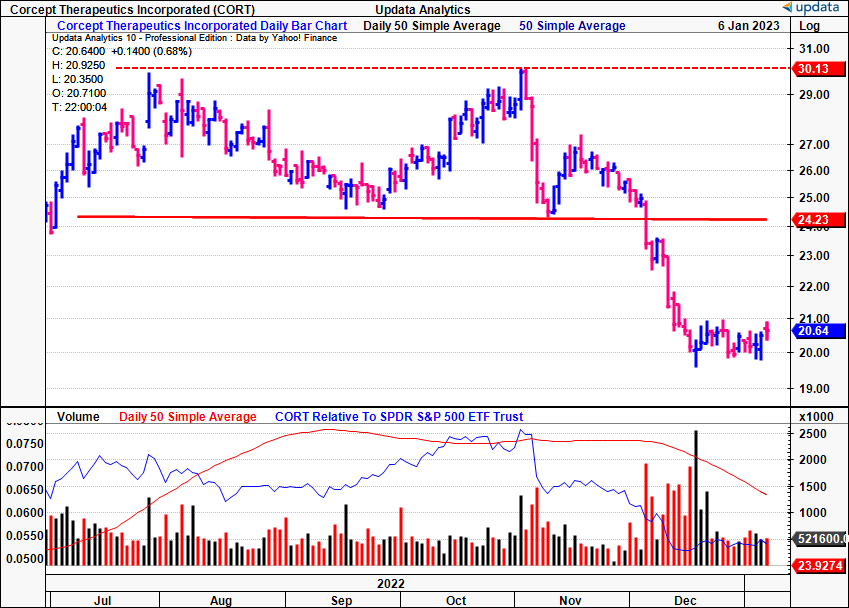

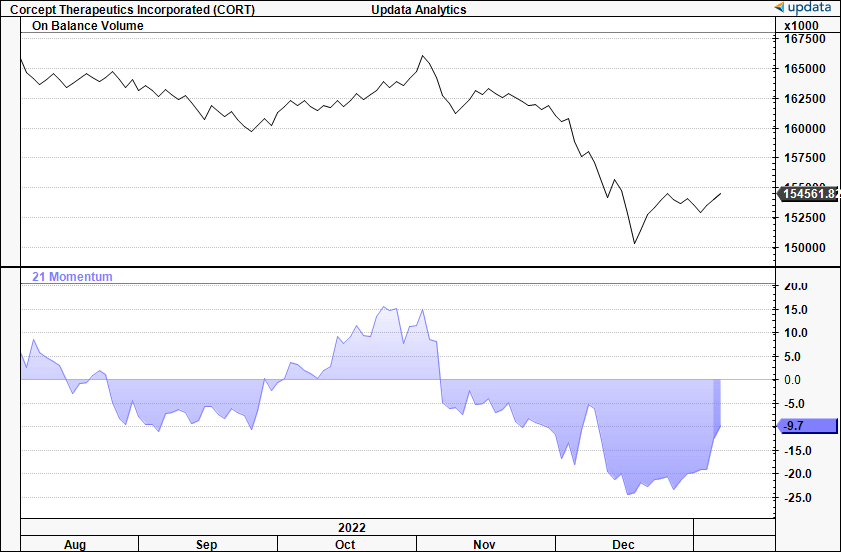

One might presume this provides clarity for CORT investors on a forward-looking basis, and shores up revenue protection for Korlym into the next decade. However, the price response from the market was incredibly poor [Exhibit 1] and investors sold off CORT shares en masse to close out the year. This is further exemplified in Exhibit 2 where we noted the level of on-balance volume and momentum drive to new lows, demonstrating the lack of buyers to make a market for CORT.

Exhibit 1. Price response to Hikma decision poor with rapid selloff in CORT equity

{kind=link}

Exhibit 2. On-balance volume and momentum studies demonstrate lack of buyers for CORT

{kind=link}

Deeper look at CORT fundamentals

The underlying question in the CORT investment debate really stems back to what kind of growth potential are we buying, and does this represent value – especially with the recent selloff. Here I'll take a hard data approach and run through several measures to underline where the evidence of corporate value for CORT may or may not be.

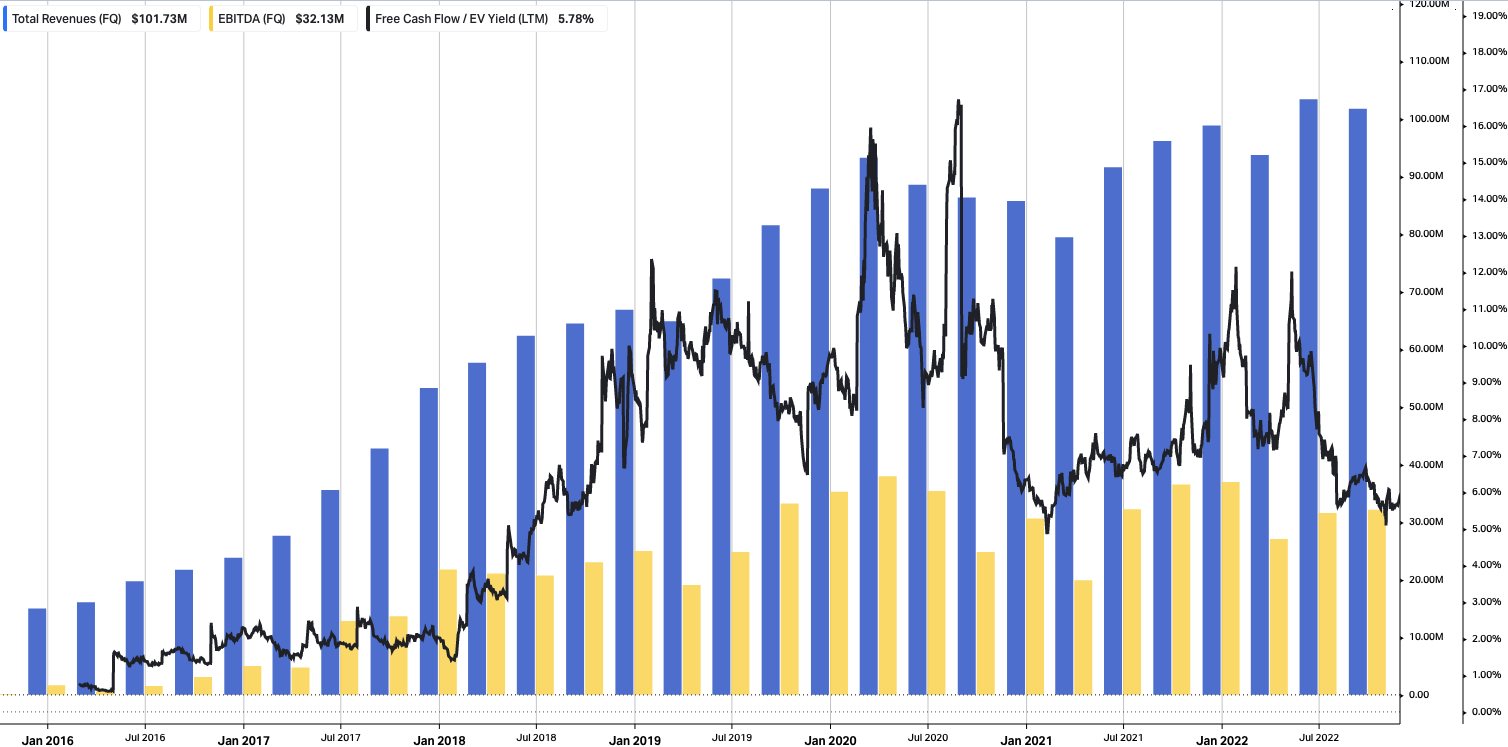

First, at a high level, it's worth noting CORT's sequential revenue growth since FY16', demonstrating cyclical upsides over this time [Exhibit 3]. More recently, growth percentages have slowed, whilst core EBITDA hasn't exhibited a reasonable growth pattern since FY20'.

However, investors can still buy CORT at a 5.8% trailing FCF yield, which represents reasonable value on absolute terms in our opinion. Moreover, it also has a 98% gross profit margin to produce its quarterly revenues, which is also very attractive.

Exhibit 3. CORT sequential revenue, core EBITDA and FCF yield, FY16'–date

{kind=link}

Delving a little deeper, we investigated how and where CORT is investing its capital, and what kind of returns it is seeing on this.

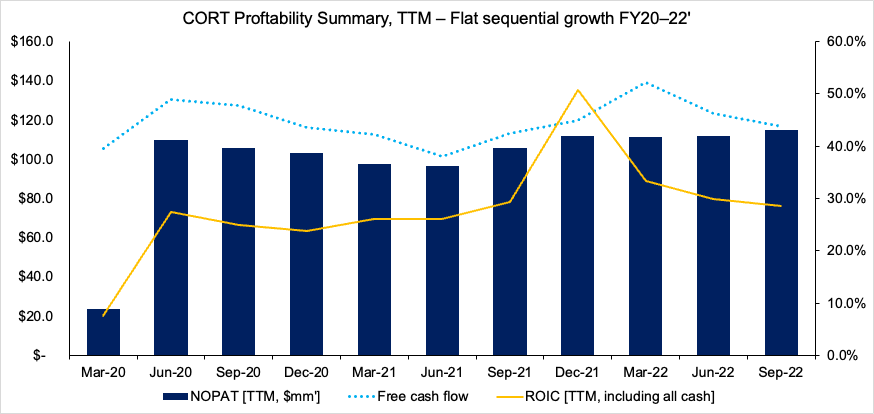

For those observing Exhibit 4, you'll note the company has held a steady line on the trailing return on its invested capital ("ROIC") these past 2 years. It realized a 28.6% TTM ROIC in Q3, an upside from 27.8% the same time in FY20'.

At the same time, it's printed a steady stream of free cash inflows over this time, and recorded $116mm in TTM FCF last quarter. However, you'll also notice that the degree of NOPAT growth the company's generated has stalled over the testing period.

Question is, why, and what's actually driving the strong trailing ROIC each period?

Exhibit 4. CORT's maintained a strong ROIC and FCF conversion these past two years, but NOPAT growth is stagnant

{kind=link}

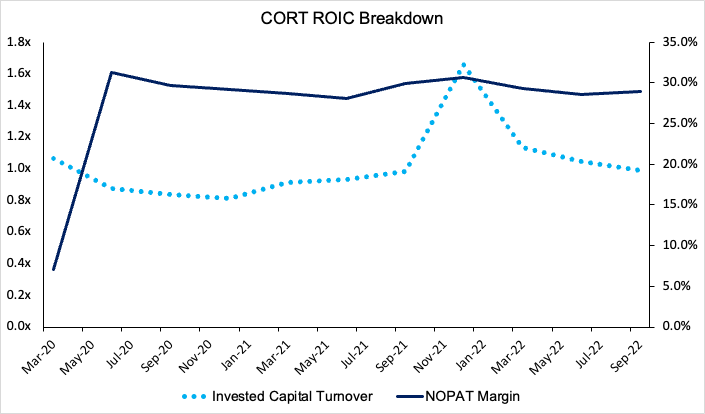

To examine this, we broke the drivers of the ROIC down into its subcomponents, NOPAT margin and invested capital turnover [Exhibit 5].

As you can see in the chart below, NOPAT margin has been a flat 28–30% of revenue in our testing period, whereas invested capital turnover has curled up very gradually over time. What this tells us is that the bulk of the ROIC during the past 2 years has stemmed from CORT investing more capital, more often each period, and not necessarily a greater level of NOPAT.

This is especially true in the Q1 FY22' period, where ROIC leapt to ~51%, providing a misleading measure of corporate value creation. Moreover, this, as revenue has crept up from $301mm in FY19' to $392mm on a TTM basis.

Therefore, CORT's capital intensity has increased since then, without the pull-through to profitability. In terms of capital budgeting, this is an unfavourable outcome in our opinion.

Exhibit 5. Despite strong ROIC numbers, this has stemmed from higher turnover of invested capital, not greater NOPAT margin

{kind=link}

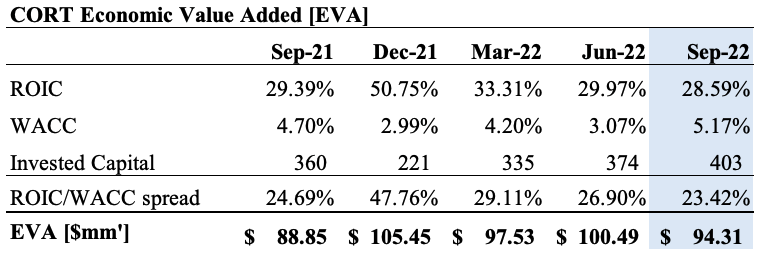

Adding some balance to the risk/reward calculus, we'd also illustrate that management have generated positive economic value added ("EVA") over the past year to date. It generated $94mm in EVA last quarter, using TTM numbers.

Moreover, CORT's cost of capital is attractive and sits in a favourable range of ~500bps, meaning it comfortably covers its hurdle rate from ROIC. This data should be factored into the investment debate in our opinion.

Exhibit 6. CORT management generating EVA above cost of capital on TTM basis

{kind=link}

Valuation and conclusion

At first glance, there's various attractive features that make CORT a potential standout in the current macro-landscape.

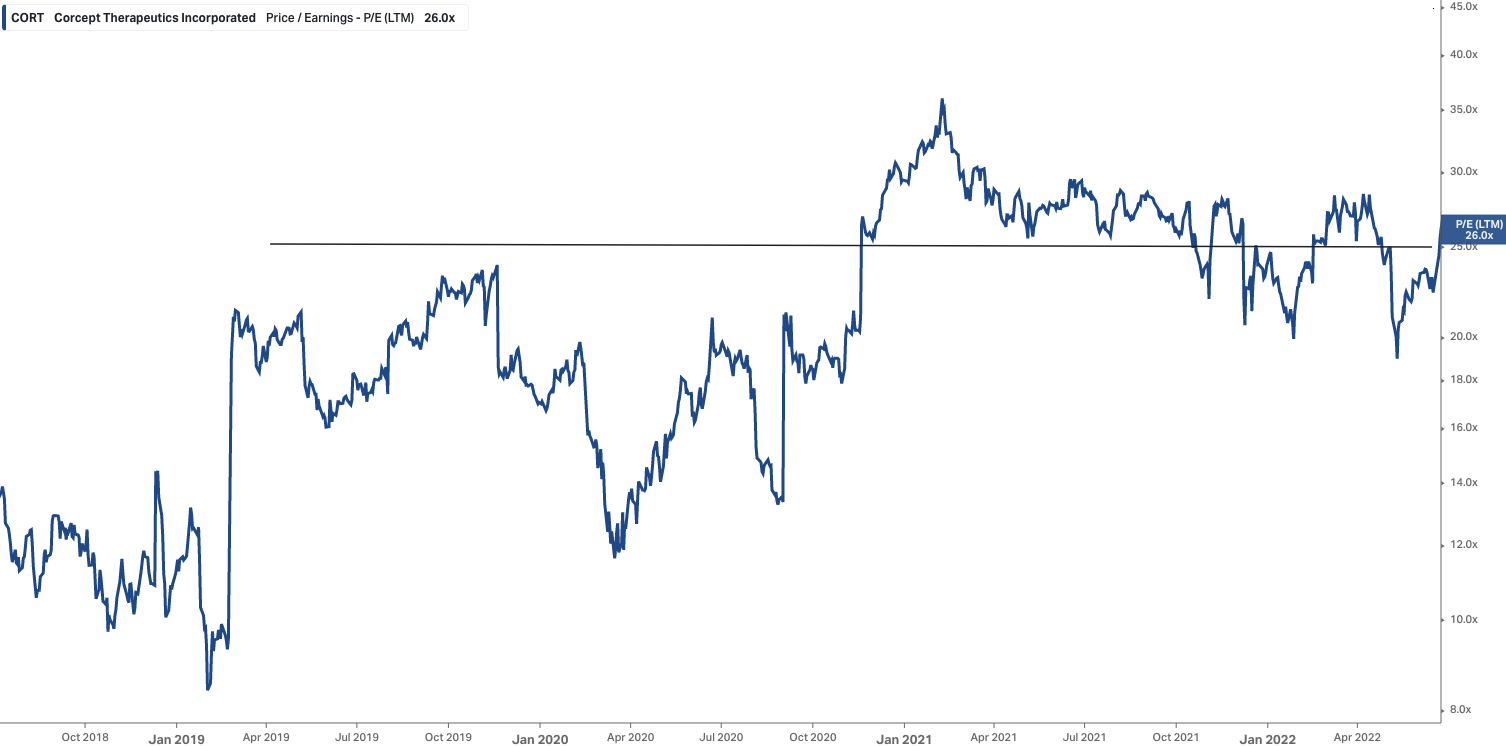

However, we've already shown these mightn't be as attractive as on face value, and, paying 21x forward earnings for this adds to this sentiment. This is also well above its historical averages.

Exhibit 7. CORT historical trailing P/E, FY18'-date

{kind=link}

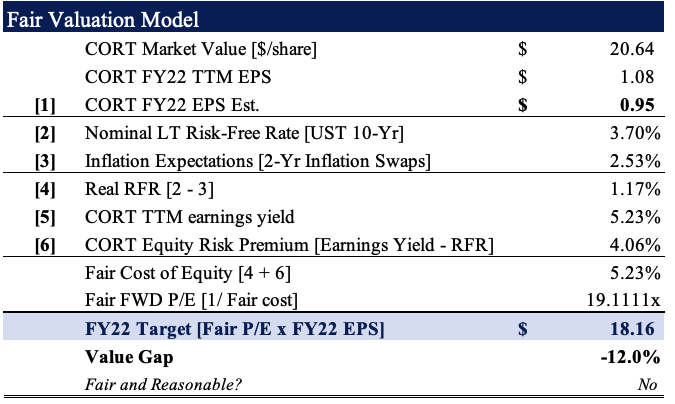

Moreover, CORT is also trading at 4.7x book value, the trailing ROE of 23% tightens to just 4.9% for the investor ROE. Hence, not growing corporate value [NOPAT, NOPAT margin] and trading at high multiples challenges the bullish view in our estimate. Only thing left is EPS upsides and the potential for valuation upside looking ahead.

Factoring in FY22 consensus EPS estimates of $0.95 [to which we are aligned], we believe the stock is fairly priced at ~19x forward earnings. Based on these figures, the stock still looks expensive and we price it at $18.16 [Exhibit 8]. This confirms our hold thesis.

Exhibit 8. Fair valuation of $18.17 demonstrating lack of valuation upside.

{kind=link}

Based on the culmination of data points discussed in this report, the CORT investment debate is balance in our opinion. There's corroborative and mitigating factors on both sides of the risk/reward equation. Most importantly, however, is that there appears to be a lack of valuation upside on offer, which advocates against entry at this point. We were keen to understand if the recent selloff in CORT's equity warranted a proposition of value, however, based on these findings, we believe this mightn't be on the table right now. Net-net, we rate CORT a hold.

For further details see:

Corcept Therapeutics: Korlym Overhang Appears To Be A Drag On Valuation Upside