CNM - Core & Main: Leading Player That Is Well Positioned To Grow

2024-01-03 16:15:15 ET

Summary

- I see a 15% upside over the next 2 years.

- CNM is a leading player in the industry with a market share of around 25%.

- CNM is going to benefit from the ageing US water infrastructure as the government steps up in reinvestment.

Investment overview

I see a 15% upside for Core & Main ( CNM ) over the next 2 years as the business benefits from the reinvestment in US water infrastructure, a sector that has faced underinvestment for multiple years. CNM, being one of the leading players in the industry, has the capacity to meet the needs of the government; as such, I think it is well positioned to grow. I recommend a buy rating.

Business description

CNM specializes in distributing products and services related to water, wastewater, storm drainage, and fire protection. Its target market consists of professional contractors, private businesses, and municipalities. These are the four product categories offered by CNM:

- Pipes, valves, and fittings: Products include pipe, fittings, and restraints to connect pipe, hydrants, and valves. This segment represents around 68% of FY23 sales, and the products are used in the distribution, flow control, and service and repair of underground water, wastewater, and reclaimed water transmission networks.

- Storm drainage Products include corrugated piping systems, retention basins, manholes, grates, and other related products. This segment represents around 14% of FY23 sales.

- Fire protection: Products include fire protection piping and custom fabrication, as well as ancillary products such as sprinkler heads. This segment represents ~11% of FY23 sales.

- Meters: Products include meter products used for water volume measurement. This segment represents around 7% of FY23 sales.

Financial statement review

CNM revenue has grown through organic and inorganic measures, leading to doubling of revenue from $3.2 billion to $6.6 billion since 2019. The increased revenue base came with a major surge in profit on both absolute and margin. In FY19, EBITDA margin was 8% and EBIT was $260.7 million, that has improved significantly to $924 million over the last 12 months and 14% margin. As I discuss below, scale is a very important competitive advantage in this industry, and the CNM financial results clearly shows this. CNM also has a strong balance sheet with $1.5 billion in debt, or less than 2x net debt to EBITDA. Given that M&A is part of CNM’s growth strategy, having a strong balance sheet also suggest possible growth upside if more M&As are done.

Leading player in the field is competitive advantage

CNM is a leading player in the industry that holds a market share of around 25% as of LTM3Q24 (based on management estimates of $27 billion TAM). CNM did not have the leading position from the onset; it was through a series of acquisitions (18 since 2021) that helped drive CNM's revenue size from $3.6 billion to $6.6 billion today. The acquisitions also helped CNM expand its geographic footprint, add new products, and expand its current product offerings. As a result of these initiatives, CNM has risen to the position of one of the industry's leading national distributors. In this climate, where disruptions to the supply chain and inflation are having huge implications for multiple industries, I see CNM's scale as a significant competitive advantage. With more than 4,000 suppliers, many of whom have maintained exclusive relationships with CNM for many years, the company is in a very competitive position in the current market. In most cases, CNM is the biggest customer of those suppliers, which gave them a leg up when supplies were low. Specifically, it is able to get inventories when sub-scale players are not able to. In essence, the bigger CNM becomes, the stronger its competitive advantage in terms of inventory sourcing and distribution. Sub-scale players will not be able to compete effectively unless they burn through an immense amount of capital to acquire their way up. I see the likelihood of this happening as low in the near term, given that the cost of capital has risen dramatically since the Fed started increasing rates. I also think that it is unlikely for the world to revert back to the zero-interest-rate era. As such, CNM's competitive position seems to be fairly solid.

Municipal end-market has a strong growth tailwind

When looking at CNM's end market, the largest one is Municipal. To provide some context, related expenditure and an aging water and wastewater infrastructure are the primary drivers of demand in the municipal end market. Spending has increased by the low single digits over the last several decades, which I believe it due to investments to fix and replace outdated infrastructure. When it comes to funding, the main sources are water and wastewater funds, which come from water bills or general funds from local taxes. Additionally, there is access to the municipal bond market. Support is also provided by spending by the federal government.

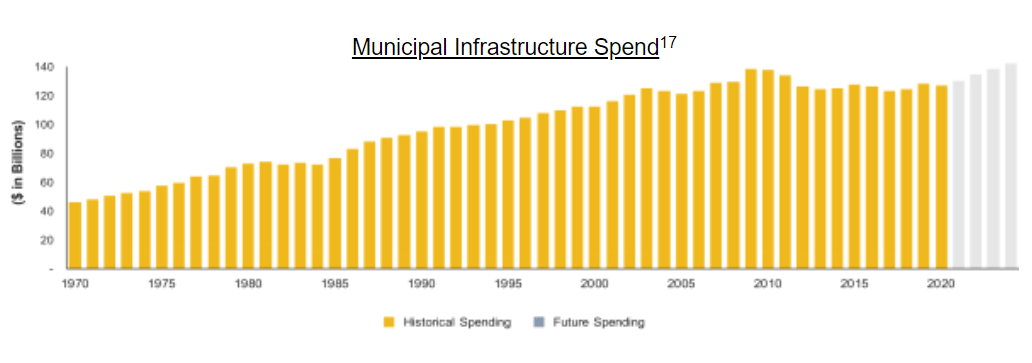

I expect growth to accelerate in the coming years, driven by aging pipe infrastructure investments, and the strongest growth driver in recent history is the Bipartisan Infrastructure Plan . The approved plan calls for an allocation of $55 billion for water infrastructure. $55 billion is the biggest investment in clean water infrastructure in the United States to date, with the primary goal of replacing outdated lead pipe systems and other related infrastructure. The following chart shows that municipal spending increased consistently year over year from the mid- to late-20th century into the early 2000s. The rising population and the ongoing need to fix and maintain the existing infrastructure were the main drivers of the growth. However, significant underinvestment occurred between 2010 and 2020 as a result of a slowdown in investment activity following the subprime crisis. From the peak of ~$140 billion spent, it has remained at ~$110 to $120 billion. In order to catch up, the US would have significantly increased its investments in the near future. The longer it delays, the more it has to catch up.

{kind=link}

Company S-1

Another way to view the situation (aside from the dollar amount) is that the US has a water pipe network of more than 2 million miles , with an average age of close to 50 years . The impact of the aging infrastructure is clear from the increasing number of water main breaks per year. This further proves my point that eventually the US has to step up on investment. The longer they delay, the worse the situation becomes, which is going to lead to more financial impact (both economic and social).

The average age of water and wastewater pipes in 2020 was 45 years, up 20 years 1970.1 More than 600 municipalities still use 200-year old cast iron pipe systems,2 and there are approximately 300,000 waterline breaks every year, representing the equivalent of a water line break every two minute. Company S1

In the midst of all these, CNM is well positioned to ride on this growth tailwind as I expect it to be the vendor of choice when the US government is finding the right party to see through the projects. In my opinion, meeting the demands of the municipal sector requires a focus on design from the outset and the ability to precisely source materials with adequate back-end support. These are strengths of CNM, where it has sufficient scale, financial strength (<2x net debt to EBITDA), and distribution capabilities, that can meet the needs of the government. Also, CNM recent share offering has further improved the liquidity position of CNM to fund further growth investments.

Strong FCF generation for growth and capital returns

Another attractive part of CNM that I like is that it operates an asset-light model due to its position as a distributor. The business is not as capital intensive as it sounds, given that CAPEX is typically less than 1% of sales, lower than peers in the industry. CNM also has a very high net income from FCF conversion, which supports the fact that this is not a capex-intensive business. It also indicates that CNM has very strong inventory management, which I believe is due to its scale, allowing it to procure and distribute inventory without the need to stock up large amounts of inventory.

May Investing Ideas

Valuation

May Investing Ideas

My financial model has a target price of $46.52 in FY25. As the CNM fiscal year ends in January (which means FY24 is ending soon), my projections are focused on FY25 and FY26. I used management FY24 guidance for my FY24 estimates. My belief is that growth will accelerate given the urgent need for infrastructure investments, and I expect growth to accelerate back to high single-digits. As for margins, my take is that they should improve with a higher revenue base given that incremental margins have been in the high teens range over the past few years. I don’t think there will be any upside from the valuation re-rating, as CNM is already trading at its historical average forward EBITDA of 11x. There might be a case for valuation to overshoot the historical average in the near term, but I am taking a more conservative approach. When comparing CNM’s valuation to peers, at 11x forward EBITDA, it is trading at a discount to Ferguson ( FERG ) which is trading at 13.6x. This discount is in line with recent trading history (post-covid) where CNM trades at a ~22% discount. Applying the 22% discount to 13.6x equates to ~11x forward EBITDA.

One thing to note about my model is that I have incorporated the recent share issuance to the cash and shares outstanding calculation.

Risk

CNM growth is essentially tied to how much the government wants to invest in water infrastructure. As such, a slowdown in municipal markets caused by budget shortfalls or delays in funding could delay the growth trajectory of CNM. M&A is part of CNM growth strategy, while the company has a pretty good track record of integrating acquired targets, the inherent risk is the next M&A might be mis-integrated, leading to friction in operation workflows and lower productivity as resources get pulled from productive functions to address any issues.

Conclusion

I recommend a buy rating for CNM with an estimated 15% upside over the next 2 years. Growth is going to be fueled by reinvestments in the US water infrastructure sector, and as a leading player, CNM is strategically positioned to capitalize on this growth. With a wide geographic presence and relationship to over 4,000 suppliers, CNM maintains a strong position in sourcing inventory, a key strength in the current market landscape. Moreover, the company's asset-light operational model, high free cash flow conversion, and efficient inventory management are all attractive aspects of the business.

For further details see:

Core & Main: Leading Player That Is Well Positioned To Grow