CNM - Core & Main: Upgrading To Buy As End-Market Improves

2023-12-10 22:24:32 ET

Summary

- Core & Main, Inc. has seen improvements in its non-residential market, offsetting weakness in multifamily housing and warehouse-related work.

- The company is well-positioned to benefit from growth in highway and street projects and the trend of mega projects in its non-residential end market.

- The revenue outlook is positive, with stabilization in non-residential orders, solid demand in the municipal end market, and potential recovery in the residential market.

Investment Thesis

I last covered Core & Main, Inc. ( CNM ) in September. While I liked the company’s cheap valuation at the time, I was concerned about the slowdown in the non-residential market, especially warehouses and multifamily construction. However, the situation has meaningfully improved for the company in recent months and management noted stabilization in non-residential orders on its earnings call last week.

Moving forward, Core & Main, Inc. is well-positioned to benefit from growth in highway and street projects as well as the growing trend of mega projects in its non-residential end market, which should offset the weakness in multifamily housing and warehouse-related work. In addition, the multiyear tailwind from CHIPS and Science Act and IRA in the non-residential end market and water infrastructure funding under IIJA in the municipal end market should drive the company’s revenue growth in the medium to long term. While there is near-term pressure on the residential end market due to the high-interest rate environment, comparisons are getting easier and the medium to long-term outlook is favorable for CNM with a potential reversal in the interest rate cycle next year and pent-up demand due to over a decade of underbuilding of new homes.

On the margin front, the gross margins should improve in the coming quarters with most of its high-cost inventory being used by Q4 2023 and the company cycling through lost-cost inventory in FY24. The longer-term outlook also looks favorable with benefits from initiatives like pricing analytics, sourcing optimization, increasing private labels, leveraging technology, and process improvements. Further, the stock is trading at a discount compared to other distributors like W.W. Grainger, Inc. ( GWW ) and Fastenal Company ( FAST ). Given the good medium to long-term growth prospects and an attractive valuation, I am upgrading my rating on CNM stock to a buy.

Revenue Analysis and Outlook

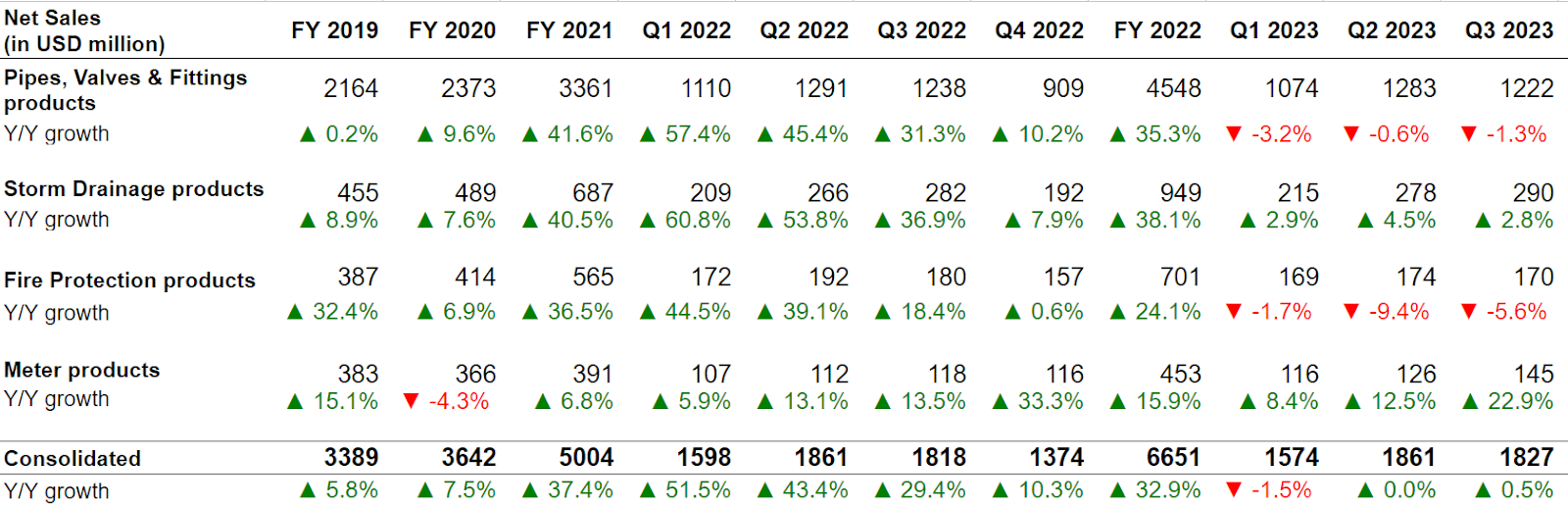

After seeing strong growth in FY21 and FY22, the company’s growth has meaningfully slowed as high interest rates started impacting its residential and non-residential end markets. In the third quarter of 2023, CNM reported a 0.5% Y/Y increase in net sales to $1.827 billion, mainly due to contributions from acquisitions, partially offset by a low single-digit decline in organic sales. Organic volume was down Y/Y while the price contribution to net sales was flat in the quarter. Product category-wise, net sales declined 1.3% Y/Y for pipes, valves, & fittings as lower end-market volumes more than offset the contributions from acquisitions. Net sales of fire protection products decreased 5.6% Y/Y due to lower selling prices and lower steel pipe volumes. On the other hand, acquisitions drove a 2.8% Y/Y increase in net sales of storm drainage products. Meter products net sales grew 22.9% Y/Y, benefiting from acquisitions and increased volumes attributed to the increasing adoption of smart meter technology.

CNM’s Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

Looking forward, the company’s revenue outlook looks positive. In my previous article , I shared my concerns about the slowing non-residential market especially multifamily housing (which the company includes in non-residential) and warehouse-related work. However, there has been an incremental positive development in this regard and management noted that they have begun to see non-residential volumes stabilize late in the third quarter with growth in highway and street projects and an increasing trend of mega projects across the country (thanks to the recent reshoring trend catalyzed by CHIPS and Science Act and IRA) offsetting some of the softness in the multifamily and warehouse work. This is a big positive as the non-residential end market accounts for ~40% of the company’s revenues. Further, most of the megaproject-related work is multiyear in nature, and with increasing deployment of funds under CHIPS and Science Act and IRA, I expect continued acceleration for these kinds of projects which makes the company well positioned for growth in FY24 and beyond.

The demand environment in the municipal end-market, which is another major end-market for the company, also remains solid. This market is expected to benefit from the funding for Water Infrastructure under the Infrastructure Investments and Jobs Act (IIJA). While the deployment of these funds has been a bit slower than anticipated, the company has started to see some green shoots and as the fund deployment accelerates in 2024, this should be a nice tailwind for the company.

Lastly, in the residential market, which has been facing headwinds due to a high interest-rate environment, the company will lap easier comparisons in the first half of 2024 which should help Y/Y sales. Further, we are likely near the peak of the current interest rate cycle and there have been some positive developments with some easing of inflationary pressures which can catalyze rate cuts starting mid-2024 driving a meaningful recovery in this market as well. There continues to be a shortage of existing homes for sale thanks to over a decade of under construction of homes post the great housing recession of 2008. This is driving the need for new lot development and new home construction which should help the company’s sales.

Overall, I am optimistic about the company’s revenue growth prospects in all of its end markets going into FY24.

Margin Analysis and Outlook

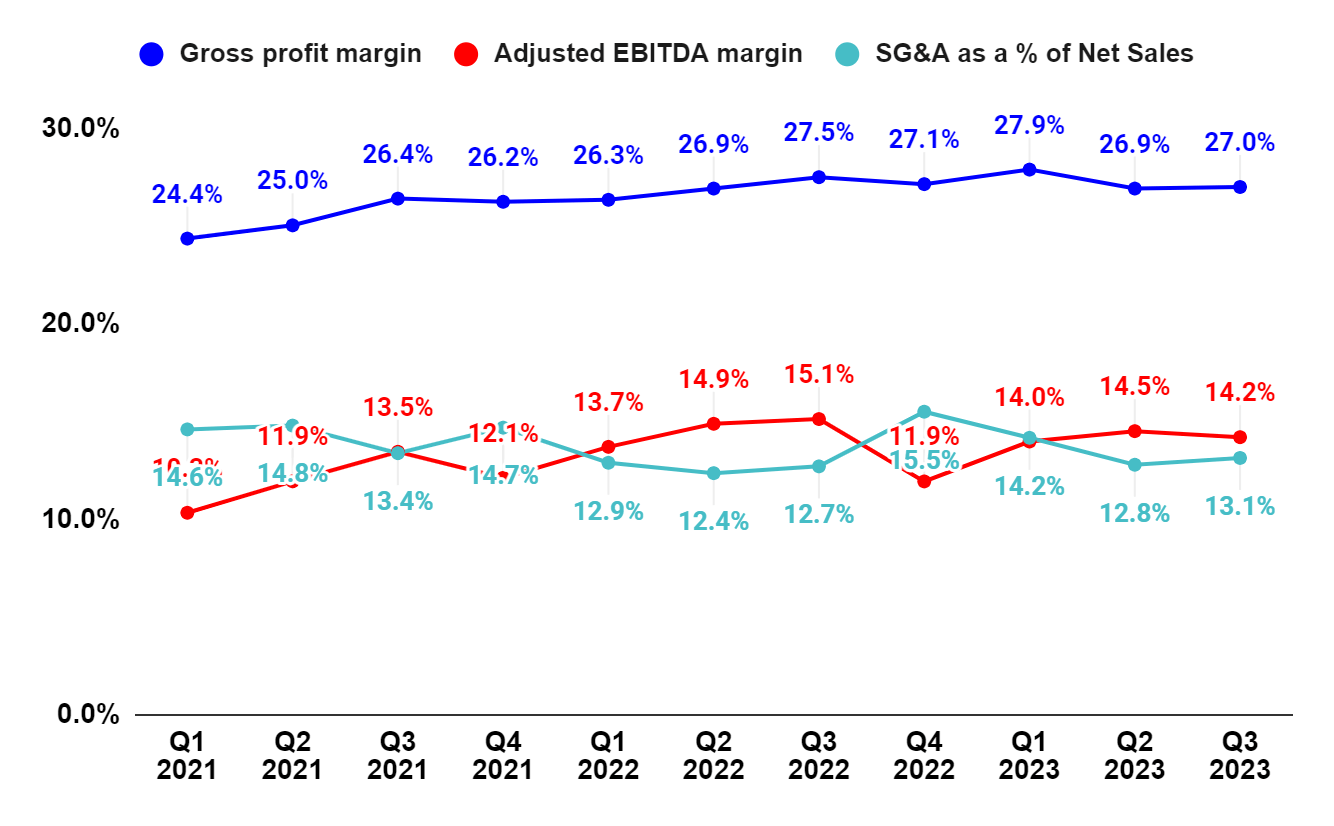

In Q3 2023, the company’s gross margin contracted by 50 bps Y/Y to 27%. The Y/Y decline was due to gross margin normalization as inventory costs continued to catch up with current market prices. However, a favorable impact from the execution of gross margin initiatives somewhat offset the Y/Y gross margin contraction. SG&A as a percentage of net sales increased 40 bps Y/Y driven by increased personnel expenses and higher facility and other distribution costs associated with inflation and acquisitions. The contraction in gross margin and higher SG&A as a percentage of net sales resulted in a 90 bps Y/Y decline in adjusted EBITDA margin to 14.2%.

CNM’s Gross Margin, Adjusted EBITDA Margin, and SG&A as a percentage of Net Sales (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I am optimistic about the company’s margin growth prospects. Going into the earnings, I was concerned about the company’s gross margins as it was burning high-cost inventory acquired in the prior period and I have discussed this in my previous article . While the company did post a 50 bps Y/Y decline in gross margins, its gross margins sequentially improved from 26.9% in Q2 2023 to 27% in Q3 2023.

This indicates the worst is behind us and points towards excellent execution in terms of pricing and cost control by management. With most of the remaining high-cost inventory expected to be used by Q4 2023 and the company cycling through its low-cost inventory post that, I expect the margins to improve in FY24.

Management has shared a target of achieving ~15% annual adjusted EBITDA margin by FY2028 through initiatives like pricing analytics, sourcing optimization, increasing private labels, leveraging technology and process improvements to leverage branch efficiency, etc., and given good execution in terms of cost control so far, I am optimistic that the company can see a good improvement in the coming years.

Valuation and Conclusion

CNM is currently trading at a 16.18x next year (FY25 ending Jan) consensus EPS estimate of $2.35, which is at a discount compared to its peer distributors like W.W. Grainger, Inc. trading at 20.83x next year consensus EPS estimates and Fastenal Company trading at 29.22x next year consensus EPS estimates.

I like the company’s medium to long-term growth prospects supported by multiyear tailwinds from CHIPS and Science Act and IRA in the non-residential end market, IIJA funding in the municipal end market, and a decade-plus of underbuilding of new homes in the residential end market. While the residential end market is under some pressure, the company will lap easier Y/Y comps in the first half of FY24, and once the interest rate cycle turns sometime next year, a sharp recovery in this market is likely which should fuel the company’s sales growth. The medium to long-term margin outlook is also favorable with benefits from low-cost inventory, pricing analytics, sourcing optimization, increasing private labels, etc. The company’s valuation also looks attractive when compared to its peers. Hence, I am upgrading my rating on CNM’s stock to a buy.

For further details see:

Core & Main: Upgrading To Buy As End-Market Improves