AIG - Corebridge Financial: Material Upside Even With The AIG Overhang

2023-12-13 03:28:45 ET

Summary

- Corebridge Financial shares have steadily recovered after a sharp decline during market turmoil in March and April.

- The company's shift from variable annuities to fixed and fixed-index annuities is boosting sales and making earnings more consistent.

- CRBG has a diverse investment portfolio and a solid capital position, with the potential for future special dividends and share repurchases.

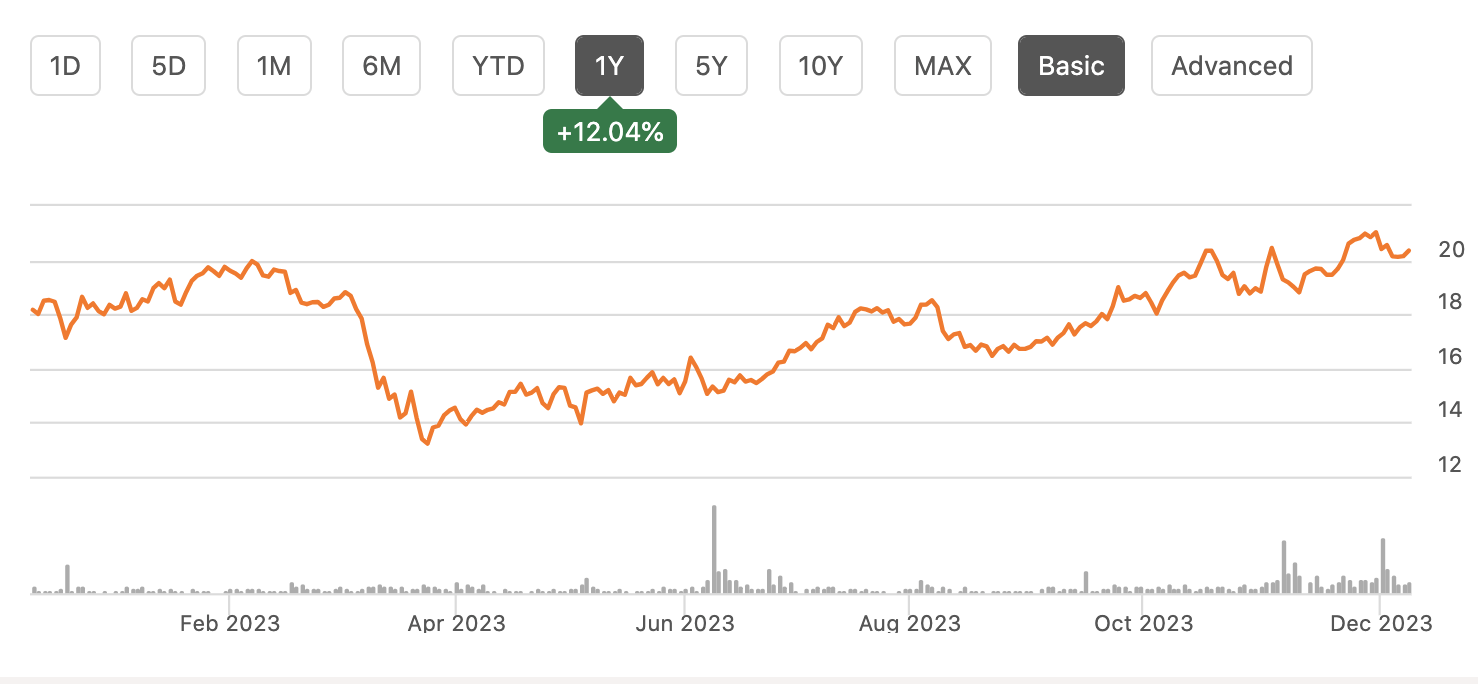

Shares of Corebridge Financial ( CRBG ) have been a solid performer over the past year, rising about 12%. They fell sharply during the market turmoil in March and April following Silicon Valley Bank's failure, but they have been steadily recovering. Because of its large variable annuity business and riskier (relative to insurance companies as a whole) investment portfolio, shares can react negatively to periods of significant market volatility. However, its hedges have worked as anticipated. At a steep discount to adjusted book value, I see shares as attractive.

{kind=link}

In the company's third quarter , its reported GAAP earnings of $3.28 roughly tripled estimates. Operating earnings, a better indicator of the company's underlying performance, were $1.05, vs the $$0.96 estimate. This was up about 25% from last year, thanks to increased investment income. There can be significant mark-to-market impacts of its hedges and market exposure, which over time cancel out, but do not necessarily do so one-for-one intra-quarter. This can cause GAAP income to move more dramatically and be inconsistent with the company's true economic performance.

Last quarter, premiums and deposits rose by 4% to $9.13 billion. Increased interest rates have made its insurance products more attractive to consumers, which has helped boost sales. Importantly, not only are sales rising, but they are shifting into less risky products. Fixed index annuity sales grew by 27%. For the third straight quarter , fixed index annuities had sales of over $2 billion. Corebridge was spun out from AIG ( AIG ), and it is that company's former retirement unit. This business had a significant variable annuities platform.

These annuities became increasingly complex in the lead-up to the financial crisis, and they frankly were sold at terms that proved to be too generous to investors. Because it is difficult to hedge all of the long-term market exposures in these policies, markets have viewed them skeptically. As these policies can last 30+ years, depending on when the policyholder passes away, even if you stop sales, they continue to impact financial results for years. While Corebridge is pivoting to fixed and fixed-index annuities, which are easier to hedge, variable annuities remain a significant chunk of assets.

In individual retirement, the company's shift from variable annuities is evident. As you can see below, over the past year, variable annuities balances are down by about 5% while fixed-index annuities are up nearly 25%. This shift is going to continue for many years, which in time will make earnings more consistent and reduce the uncertainty the market assigns to CRBG's fair value, which should lead to a higher multiple over time.

{kind=link}

Importantly, the company has completed its annual reserve assumptions, and it found $22 million of positive changes, an immaterial amount. This means policies are performing as expected. Because one cannot know when someone with a policy will die, for instance, earnings are based on modeled actuarial assumptions. Each year as more data is received, these assumptions can be revised.

This modest revision means policies are performing as expected, which should give the market some comfort about Corebridge's variable annuity exposure. Additionally, the company's net market risk benefit assets stand at $5.5 billion from $5.9 billion one year ago. That is roughly an 8% decline, slightly worse than the 5% decline in VA assets, partly due to timing. Even excluding timing, that represents just about $100 million of after-tax economic slippage during severe market volatility in both equities and interest rates. That solid hedging performance is a reason why shares have recovered their March/April losses.

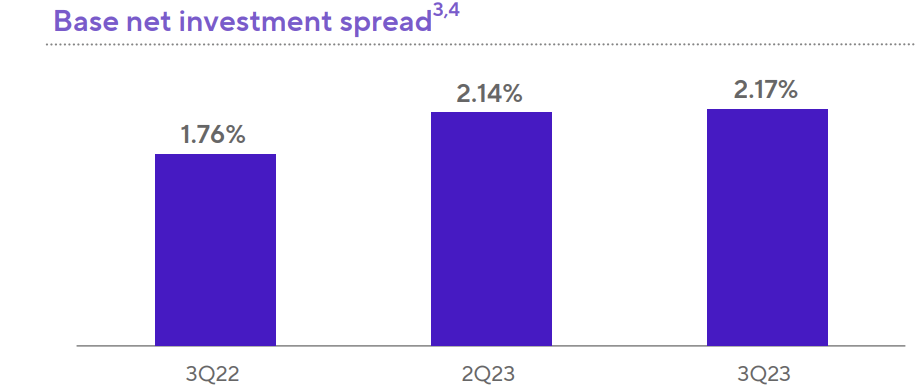

Corebridge has a diverse base of earnings. Investment spread generates about 50% of its income, excluding variable returns, 27% comes from investment management fees, and 23% from underwriting. Last quarter, base portfolio income rose from $2 billion to $2.4 billion. Spread income rose to $881 million from $668 million across its group and individual retirement units, with particular strength in individual (which generates half of the company's profits).

Essentially, the company has been able to take advantage of higher yields in the market without passing on the full amount to new policyholders, increasing the net interest margin it is earning on its $189 billion investment portfolio. Base yields rose 10bp sequentially to 4.7% and are now up 62bp from a year ago. This is because it is investing new money at 6.6% while securities rolling off have a 5.1% yield.

{kind=link}

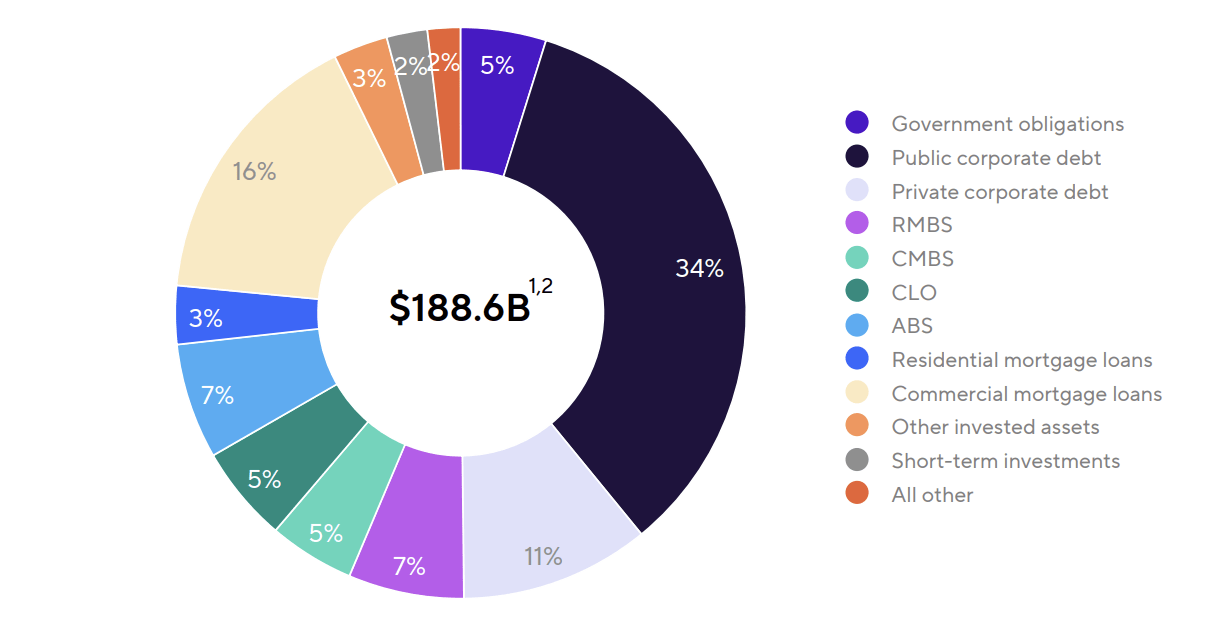

Now as you can see below, Corebridge has a fairly diverse investment portfolio. 97% of its portfolio is in fixed income or cash equivalents. 94% are rated investment grade. It has relatively large ABS and private debt exposures, at about 18%. This is because Blackstone ( BX ) manages $54.7 billion of assets. These assets have generated a yield of 6.6% since inception, 150bp over the portfolio's total yield. Blackstone also holds 9.9% of Corebridge stock, as part of a 2021 deal with AIG in which it will manage $93 billion of assets by 2027

{kind=link}

While these securities have an average A+ rating, they can be less liquid, leading to more meaningful mark-to-market volatility. Because its annuity liabilities are long-dated, Corebridge is able to hold these until maturity, riding through the volatility. There is also concern that in a recession some of these structured products could suffer more meaningful losses, given assets like collateralized loan obligations (CLOs) tend to lend to riskier companies and use structural protections (by having subordination and over-collateralization) to offset this risk and maintain higher credit ratings.

On the positive side, these assets earn higher yields given their complexity, but that complexity also causes caution on behalf of equity investors. Now, with the risk of a recession seeming to be declining, there is likely to be less concern about this exposure.

Corebridge also has $7.5 billion of office loans. The average loan-to-value is 64% with 1.96x debt service coverage. 77% are class A with an 84% occupancy. It has set aside 5.9% for losses here. There are currently no 90+ day delinquencies. Given traditional US office is just 2% of assets, I view this risk as manageable, though it could modestly weigh on investment returns.

Corebridge has a solid capital position with leverage at 27.2%, at the midpoint of the target. Its insurance companies have a risk-based capital ratio level north of 400%, consistent with solid financial strength. As a result, the operating companies have sent about $1.5 billion up to the holdco this year. The holding company has $1.7 billion of liquidity, more than fully covering its next 12 months of needs. It is this entity that pays dividends and does buybacks. This year, CRBG is running at a 55% payout ratio vs its 60-65% target.

On top of its 5.7% dividend yield, the company declared a special dividend of $1.16 to return the proceeds of its Laya Healthcare business. During the quarter, it also announced the sale of its UK business for about $580 million. This is likely to result in another special dividend over the next year of up to $1/share. Alongside that, it has done $246 million of repurchases through 9/30 with $102 million of open market purchases through October 31.

On December 1, AIG announced it would be selling 35 million shares (over 5% of the company). That follows a 50 million share sale in November . AIG still holds 330 million shares, giving it a roughly 52% stake. With its next share sale, it will likely cease to be the majority shareholder. Over time, Blackstone could also decide to reduce its stake. The stock has performed well despite the sales, but I expect them to continue as AIG seeks to gradually disinvest to repurchase its own shares. They do not want to distort the market, and so I expect an ongoing wave of sales for multiple quarters, rather than one large block.

This can be a headwind for performance, though I would expect to see CRBG increasingly offset these sales with repurchases, perhaps even buying shares directly from AIG again, as it did this summer .

With the holding company holding sufficient liquidity, all future operating company dividends should support shareholder returns. I would expect to see intracompany dividends of $1.5-$1.8 billion or $1.2-$1.5 billion after taxes. After its dividend, that leaves about $700 million in annual repurchase capacity, or about 6% of shares per year, for an 11+% capital return yield. If we assume AIG seeks to eliminate all holdings within three years, about 1/3 can be offset by buybacks and 2/3 would need to be absorbed by the market.

Now once AIG ceases to be a majority shareholder, we could see Corebridge gain entrance to indices like the S&P 500, increasing its ownership by index funds as well as by active funds benchmarked to that index. That buying could be 10-15% of its shares, further reducing the impact of AIG's sales. It is also in AIG's interest to be prudent in its selling patterns as it will want to maximize its average sales prices. I view this risk as manageable.

This overhang is likely reflected in its current valuation. Given my view there is unlikely to be a recession, and the lower-risk of its new products, CRBG should be able to sustain operating earnings in the $4/share area. While its reported book value is $13.21, this is distorted by $19.3 billion of losses in accumulated other comprehensive income (AOCI). These investments are duration matched against its liabilities, a factor not included in GAAP calculations. As such, it is more appropriate to look adjusted book value of $38.23.

Given its VA risk and the BX-managed assets, I would not expect shares to trade to book value. But I see fair value towards 0.75x book or $28-30, also about 7-7.5x earnings. Given a ~11.5-12% return on adjusted equity, this is a pro-forma annual return for investors of 16%, to reflect these risk factors. As VA assets decline, I would expect shares to move closer to book, but this will take many years.

This target still represents 40% upside as CRBG benefits from the higher investment yields it is locking in. This valuation disconnect makes its growing buyback program even more accretive. While shares will likely exhibit downside momentum during sell-offs, its hedges have been working, and investment yields have been rising. I would be a buyer. As the AIG overhang gradually diminishes, shares can move materially higher.

Editor's Note : This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Corebridge Financial: Material Upside Even With The AIG Overhang