CORR - CorEnergy: Common And Preferred Distributions Cut What's Next?

Summary

- Each round of successive results had forced us to dial up the caution on CorEnergy.

- On our last call, we took the controversial stance that the investors hiding in preferred shares are likely to face a cut at the same time as the common shares.

- That has come to pass.

- Let's look at what is next.

Your job as an investor is to focus on risk management. That means the primary question you should ask is what can go wrong. You do this by first ignoring the "yield" and looking at how the company manages its debt structure. An extension of risk management is to also evaluate company management. We did all of that for CorEnergy Infrastructure Trust, Inc. ( CORR ) and its preferred shares ( CORR.PA ). Against the grain, we suggested that things were getting worse for the company. In fact, we dialed up the negativity, as more and more data suggested that anyone holding for yield, would regret it.

Seeking Alpha

On our last note, we did not believe discretion was the better part of valor and instead told you to run like the wind.

Of course preferred distributions can only be cut when common distributions are moved to zero. We get that. But in this case, it's totally warranted and likely the only thing that keeps the firm on a good footing going into 2024. For those bullish on the firm the 19.263% yielding bonds make 100 times more sense than the preferred shares yielding 10%. Sell the common shares, sell the preferred shares and perhaps consider the bonds if you are bullish.

Source: Common And Preferred Distributions Likely Get Cut

Time, Tide and Distribution Cuts wait for no man. CorEnergy dropped the hammer this morning.

KANSAS CITY, Mo.--(BUSINESS WIRE)-- CorEnergy Infrastructure Trust, Inc. announced today that its Board of Directors has determined the Company will suspend dividend payments on its 7.375% Series A Cumulative Redeemable Preferred Stock and the Company’s common stock.

“After careful consideration, the Board agreed with management’s recommendation to suspend dividends due to a combination of declining volumes and increased costs in our California systems. As a result, we filed for a 36% rate increase on our SPB line in California based on the regulated cost-of-service tariff structure,” said Dave Schulte, Chairman and Chief Executive Officer.

“Additionally, near-term debt maturities provide a transitory challenge, which will be addressed with a focus on monetizing assets and reducing total leverage. Pending the resumption of dividends, we believe that retained capital best benefits stockholders through the reduction of debt. The Board will continue to evaluate future dividend payments on a quarterly basis,” Schulte concluded.

Source: CorEnergy

Outlook

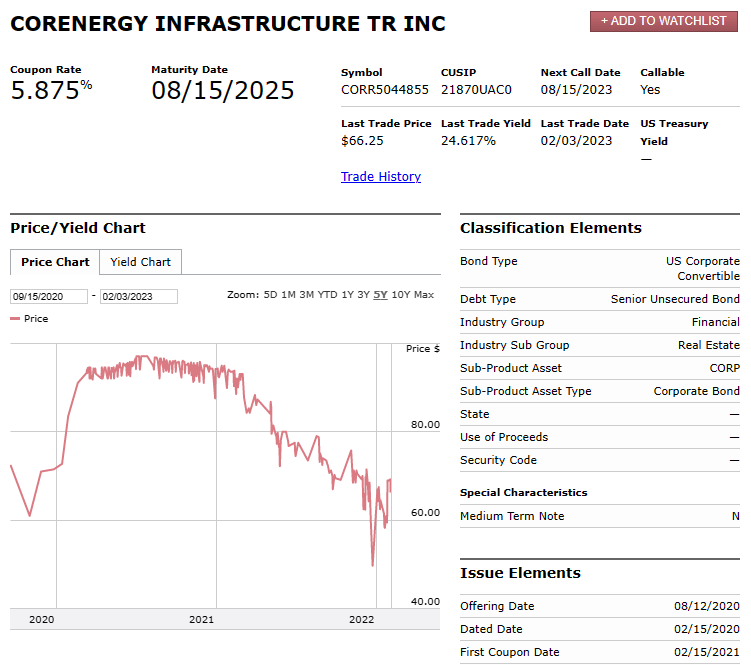

There are a few things to dissect here so let's get started. Our thesis was always that the near-term debt maturities were screaming that the organization is not viable. That distress has increased. In September, those bonds yielded 19% and they now are now with a 24.6% yield to maturity.

{kind=link}

FINRA

Remarkably, this happened at the same time as when junk bonds have rallied and CCC spreads have compressed.

In other words the entire market was screaming "risk-on" but CorEnergy bonds were refusing to drink the Kool-Aid. This is the "dog that did not bark."

Silver Blaze

When company specific fundamentals are so bad that even the madness of crowds cannot move things up, you have to be worried.

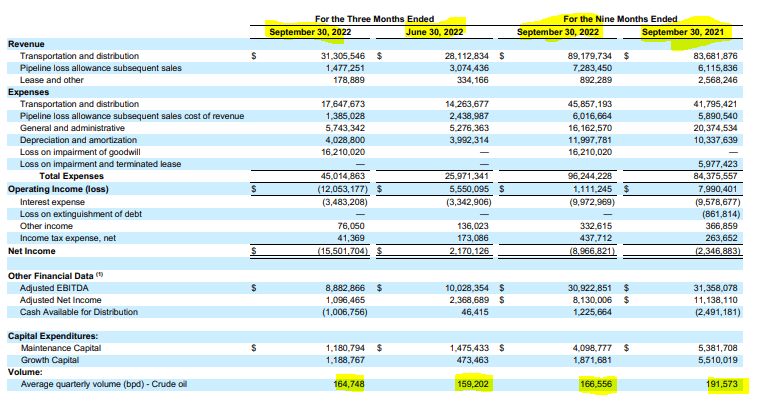

What's driving this is exceptionally poor cash flow from the company. Over the last six reported months, cash available for distribution has been negative $1.05 million.

Q3-2022 Press Release

This has been driven by extremely poor operational performance and an increase in interest rates. On the first front, CorEnergy 's volumes paint a distressed picture.

{kind=link}

10-Q Link Below

On the interest rate front, the variable debt is a big albatross.

Under the Crimson Credit Facility, a 100 basis point increase or decrease in the current SOFR rate would have resulted in an approximately $738 thousand increase or decrease in interest expense for the nine months ended September 30, 2022.

Source: 10-Q

There's a lag with which these rates reset for CorEnergy and this underpinned our thesis. Anyone doing the math would know instantly that the company's cash flow would go deeply negative by the time all these rates moved through to the system. The base case would be close to negative $2 million a quarter of cash available for distribution once these resets were through. So the common dividend was toast and that was engraved in stone. But why the preferreds?

Here, it's an extension of the same math. Suspending the common dividend barely helps the company. With 15.86 million shares, the common dividend of 5 cents a quarter is peanuts.

The bulk of the dividend payments are the preferred shares. So if you examined the financial statements, you would know with a high degree of certainty that a dividend cut would have to be at both the common and preferred levels to make any sort of difference to the company.

With the distribution cuts behind us, what lies ahead? CorEnergy has about $220 million of debt with an EBITDA run-rate of close to $40 million.

{kind=link}

10-Q Link Below

Generally speaking, major midstream companies with a diversified base of assets tend to stay at a debt to EBITDA under 4.0X for safety reasons. CorEnergy is at 5.5X and we might add with a more tarnished history than most other midstream companies. That debt to EBITDA ratio does not count to the preferred shares. Practically speaking if any other midstream company had preferred equity equivalent to 5X the common equity market capitalization, no credit agency would count that as equity. It would be counted as debt. So in essence we see the debt to EBITDA ratio as 8.625X. To this we have to add the fact that at least $10 million a year will be spent maintaining the infrastructure. So you have $30 million of cash to service $344 million of debt plus par value of preferred shares.

Interest rates will move up on the variable portion and if CorEnergy makes it to the 2025 maturities, we think they will reset there at least 5% higher. There was nothing left for common shareholders (cash available for distribution) when CorEnergy was paying $14 million of interest annually. So when it pays $25 million annually down the line (by 2025), we cannot imagine there will be anything for common or preferred shareholders.

Verdict

The one hope here is the massive tariff hike requested by CorEnergy. That 36% hike is extraordinary and likely to get rejected in our opinion. But that also offers the only hope to the bulls. 36% increase in revenues would likely prevent a wipeout and the company could make it. Even in that scenario the common equity would be close to worthless in our opinion. The preferred shares won't get a distribution paid until the 2025 debt maturities are refinanced. You can take that to the bank. Which also brings us to our only viable play here. Those 2025 bonds with a 25% yield to maturity are still your best and only bet that bulls should make. For our part, we are not even interested in those. We are changing our ratings as follow.

CORR-Common Shares-Maintaining Strong Sell as terminal value is zero.

CORR.PA-Preferred Shares-Upgrade! We had a Strong Sell on this and as we are writing this, the preferred shares have been acquainted with reality.

{kind=link}

Interactive Brokers Feb 6, 2022

At a price of $7.00 we are upgrading this to a "Hold."

Unsecured Bonds: We are maintaining this at a Hold and might get interested if we see fundamentals improve.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

CorEnergy: Common And Preferred Distributions Cut, What's Next?