CORR - CorEnergy Infrastructure Trust: 16% Yield On Preferred Shares

Summary

- CorEnergy Infrastructure Trust is a REIT that owns pipeline assets for the transportation of crude oil and natural gas.

- The company's preferred shares are deeply discounted due to a number of risks.

- Based on an evaluation of these risks, I believe the preferred shares are still a good investment.

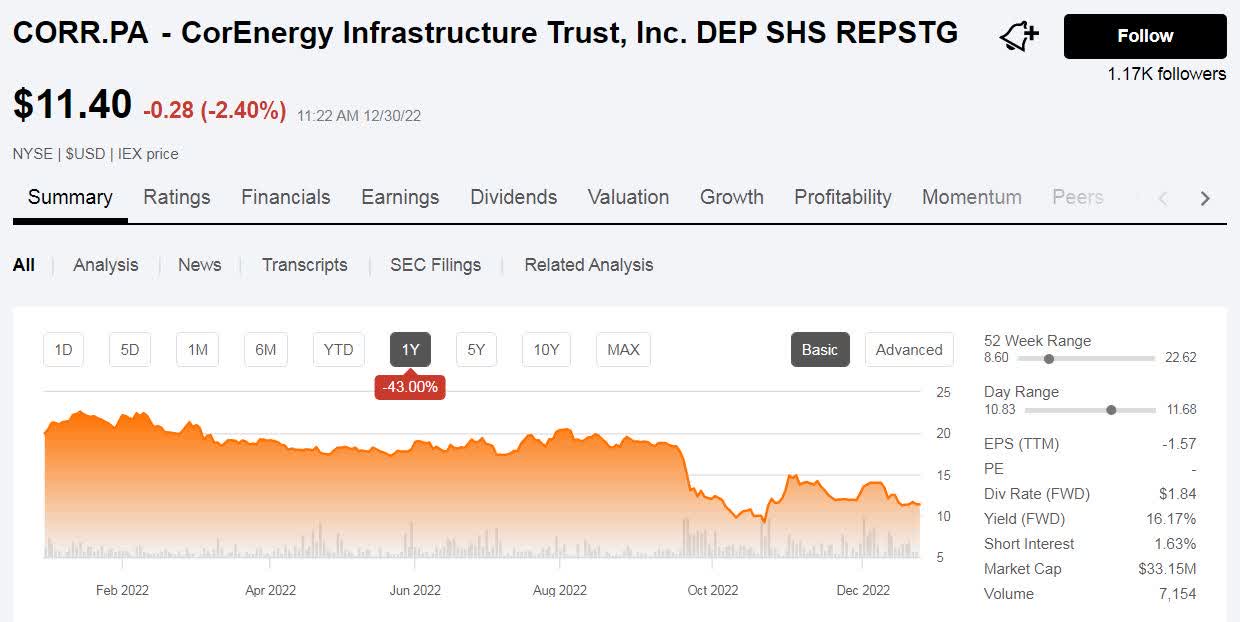

CorEnergy Infrastructure Trust ( CORR ) is a REIT that owns and leases pipeline assets for the transport of crude oil and natural gas on the west coast of the United States. The company has a Series A Cumulative Preferred share ( CORR.PA ) that is currently trading at 46% of par value ($11.40/$25) generating a dividend yield of over 16%. After weighing the risks involved in the business, I believe the preferred shares are still a good investment for income investors.

{kind=link}

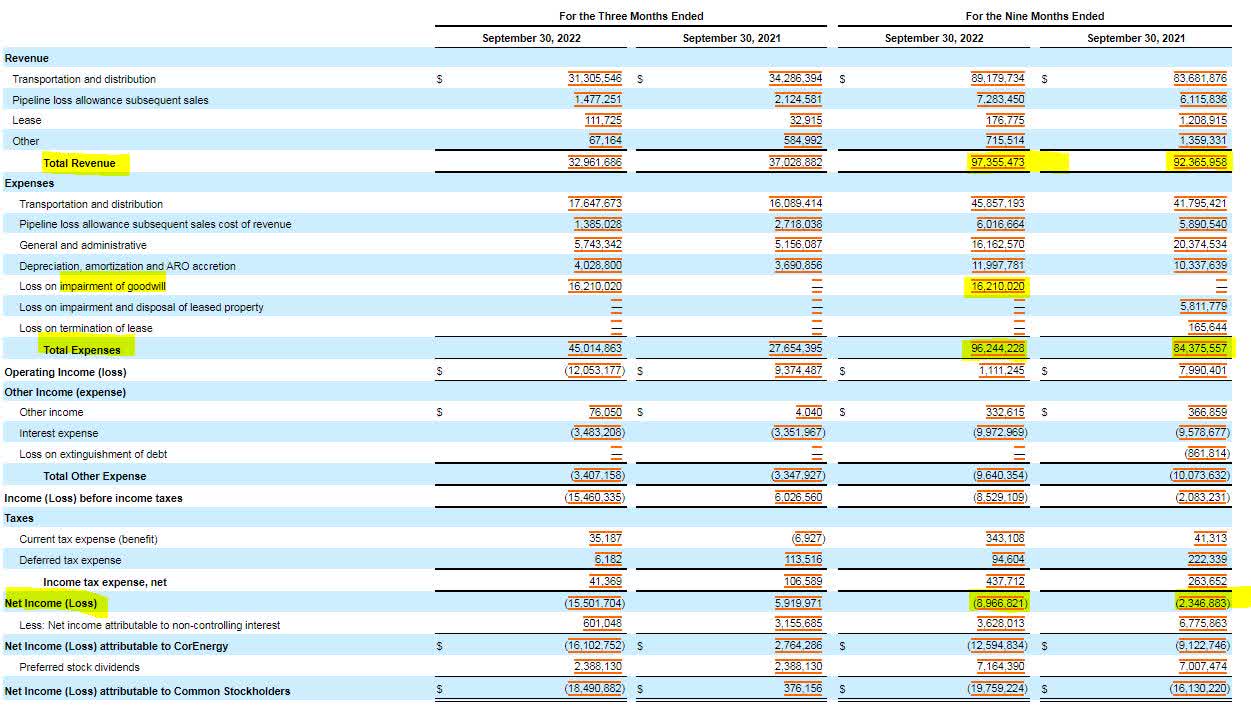

CorEnergy's income statement shows that the company has grown revenue in the first nine months of 2022 by $5 million compared to the same period in 2021. While expenses have grown by more than revenue, this increase, and subsequent net loss was caused by the impairment of goodwill (a noncash expense). If we remove the impairment charges (from both 2021 and 2022), we'll find that operating expenses grew by only $2 million and operating income in 2022 based on this adjustment would be $17 million, nearly double the company's interest expense.

{kind=link}

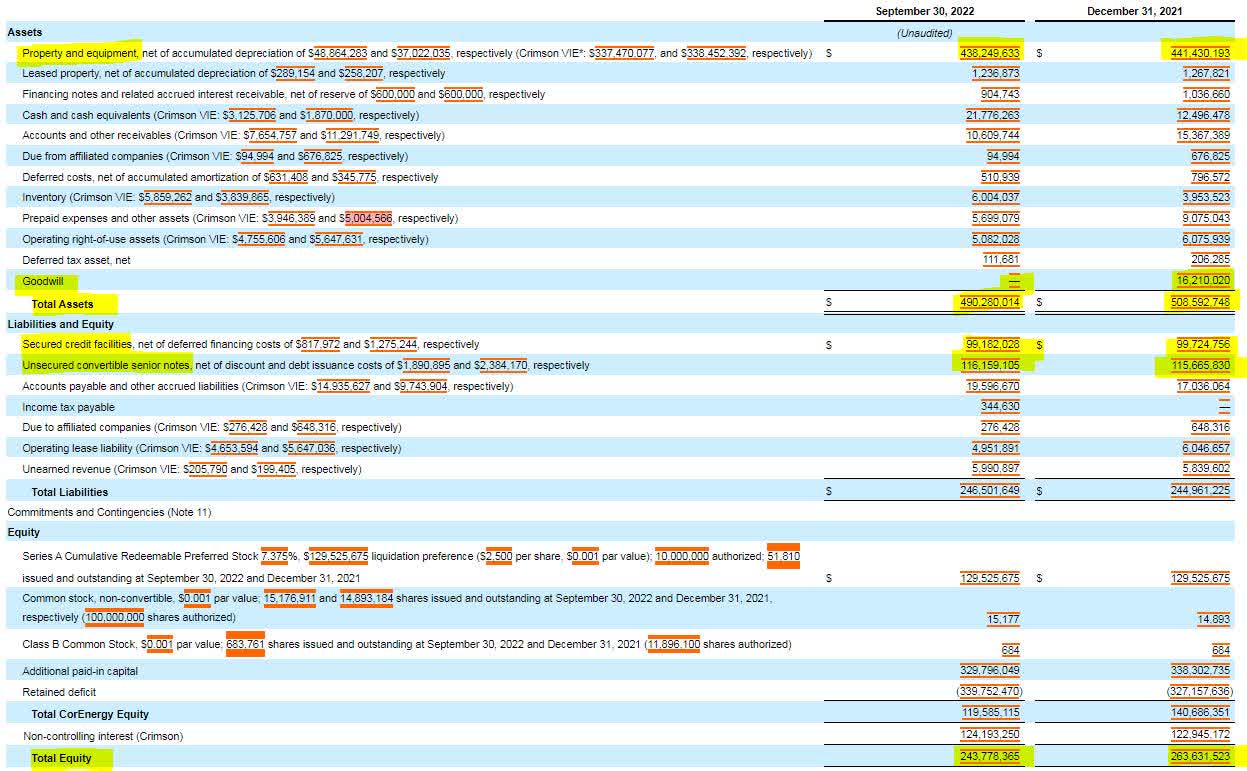

CorEnergy's balance sheet is a consolidated, cut and dry document. The company's assets are mainly comprised of the pipelines, listed as property and equipment. The liability side is comprised mostly of secured credit facilities and convertible senior notes. The only significant change to the balance sheet in 2022 has been the impairment of goodwill, which led to the decrease of the company's total equity. Overall, CorEnergy has maintained a stable capital position throughout the year.

{kind=link}

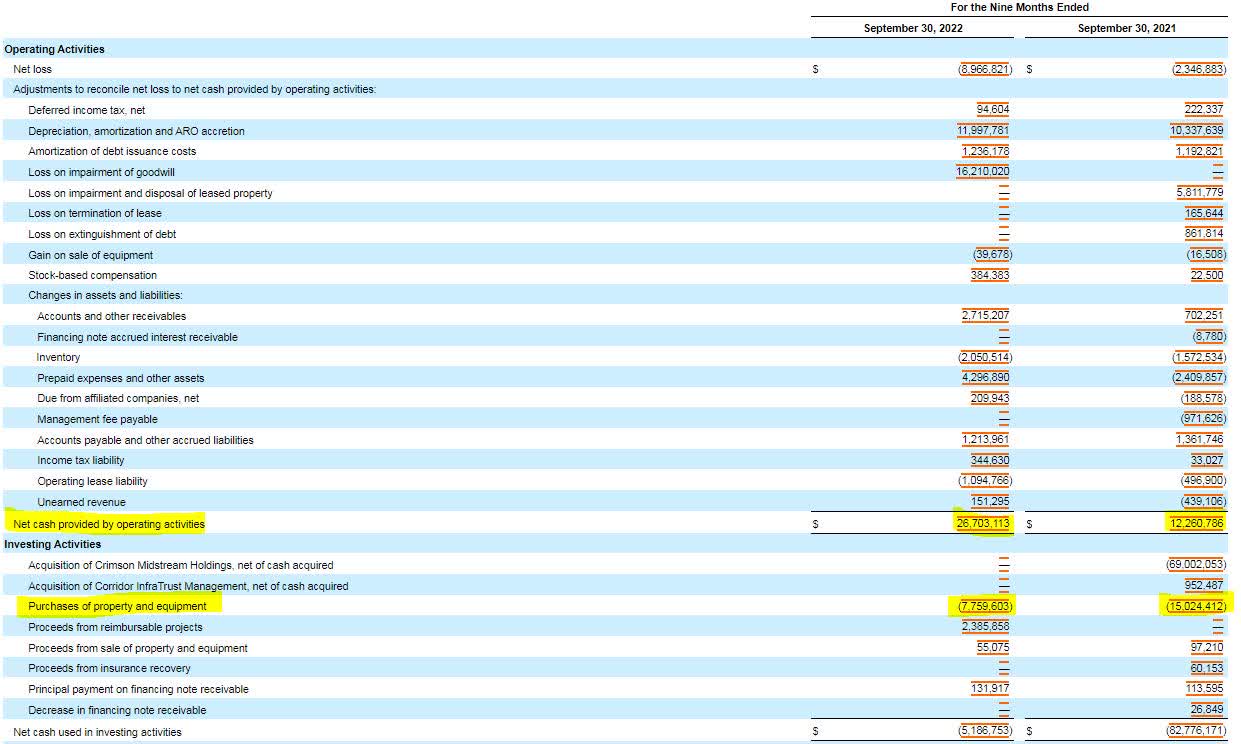

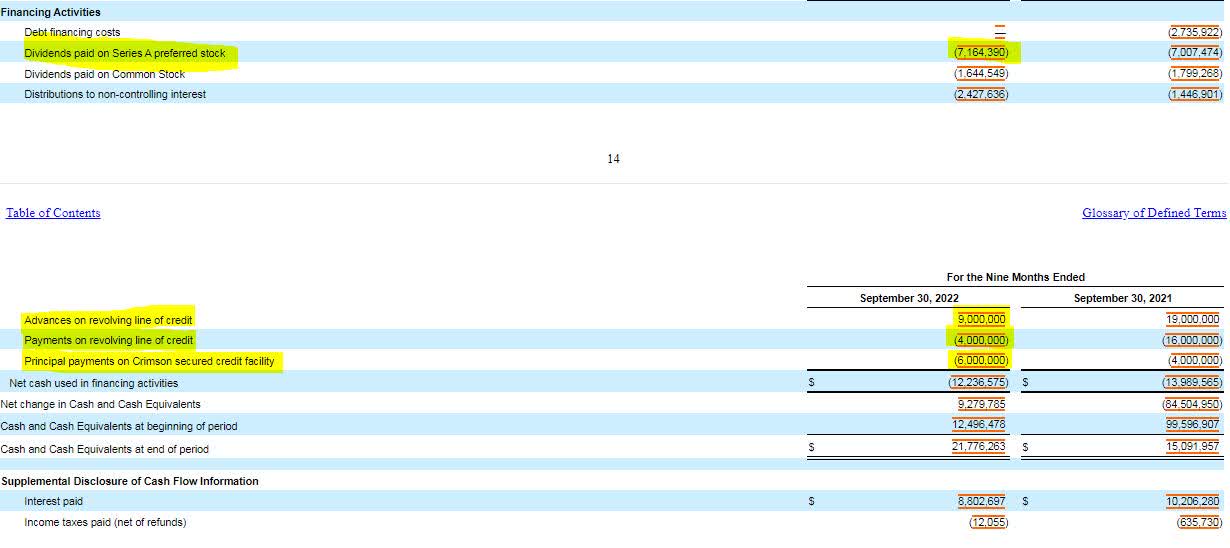

In terms of cash flow, CorEnergy has doubled its operating cash flow in the first nine months of 2022 compared to 2021. After capital expenditures, the company has free cash flow of $19 million, which is enough to cover its preferred dividend obligation of just over $7 million. It's also important to note that CorEnergy did not add debt in 2022 and was able to increase its cash position from $12 million to $21 million.

{kind=link}

{kind=link}

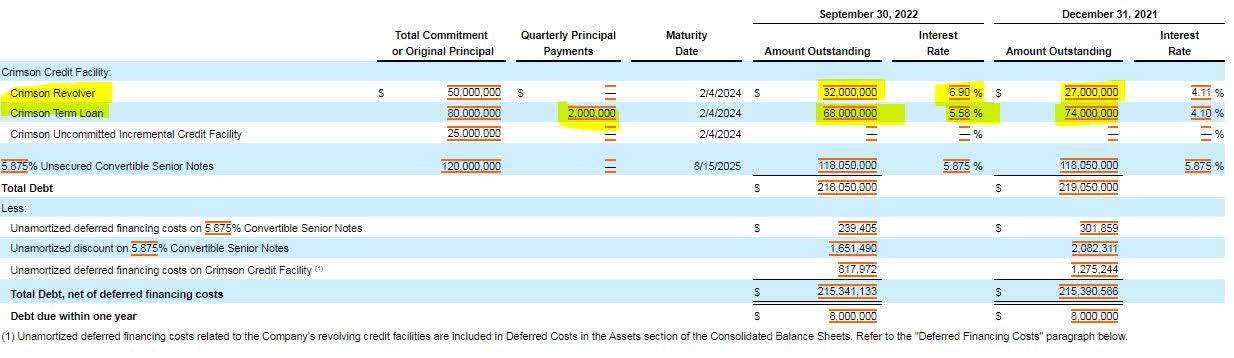

One concern regarding CorEnergy lies in all its debt maturing in 2024 and 2025. The company has $100 million in revolver and term loan debt that has already seen an increase in interest expense compared to last year. CorEnergy does seem to be preparing for a capital raise should the company need it. They have a shelf registration on file that allows it to raise up to $600 million in capital through either stock or debt offerings. The refinancing need combined with the shelf registration is why I am not advocating for investment in the company's common shares, because I believe they stand to be diluted by any capital raise.

{kind=link}

{kind=link}

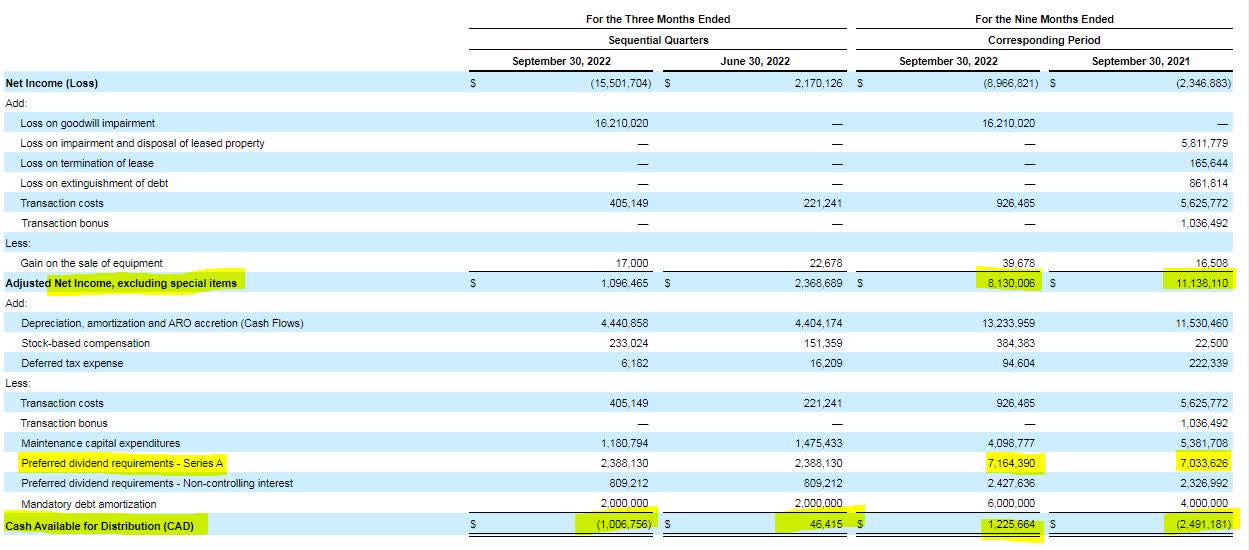

Another concern that investors need to weigh is the cash available for distribution analysis. This is an internal calculation used to determine the viability of the company's dividend. CorEnergy's third quarter performance did push the cash available for distribution downward, but the company still has cash available for distribution after taking the preferred dividends into account and the mandatory principal payments on the company's term loan. It's also important to note that the company maintained common and preferred dividends in 2021 despite a negative cash available for distribution.

{kind=link}

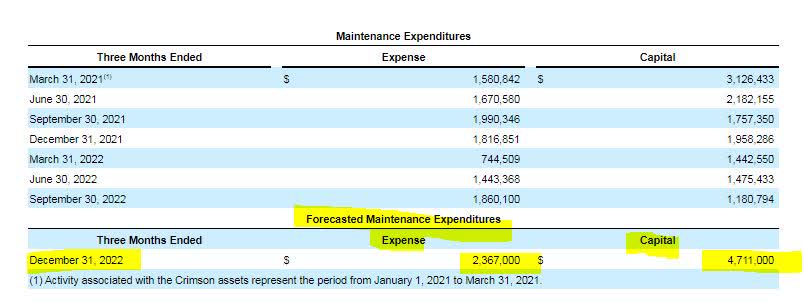

Possibly the most tangible threat to the company's cash flow capabilities lies in its capital expenditures forecast. In one section of its most recent 10-Q, CorEnergy disclosed a sizable expected increase to capex in the fourth quarter of 2022. When earnings are released, investors should expect cash available for distribution to be negative for the year. Looking further into the future, the company is expected to make additional investments to its assets in late 2023 and early 2024 related to legislation in California.

{kind=link}

{kind=link}

CorEnergy is implementing a surcharge that will be used its late 2023/early 2024 capital obligations, so investors should expect those not to be financed from current operating cash flows. Additionally, the shelf registration could easily fund these anticipated increases.

Should CorEnergy choose to eliminate its dividends, the execution of a capital raise would become more difficult and the types of offerings would become more limited. Overall, while the company is facing headwinds in the form of capital commitments and debt refinancing, I believe that CorEnergy has positioned itself to face these challenges without the sacrifice of its dividends.

For further details see:

CorEnergy Infrastructure Trust: 16% Yield On Preferred Shares