GLW - Corning: Glass Technologies Behind AI And Consumer Devices Will Drive Q3 2023

2023-09-27 09:37:41 ET

Summary

- Corning's Q2 2023 report showed diversified revenue streams and recent news suggests new opportunities for continued growth in Q3 2023.

- Optical communications and display technologies expected to drive changes in Q3 2023.

- Federal BEAD program for broadband access and data-intensive AI datacenter segment offer steady revenue and growth opportunities for Corning.

A month ahead of Corning's (GLW) Q3 2023 earnings report, what can we expect? At Citi's recent Global Technology conference on September 7th, 2023 Corning's chief strategy officer shared a brief outline of the long-term value creation model, as well as the short-term priorities. This provides some potential upside to look forward to, and should represent a trend away from the lower than expected results from the Q2 2023 earnings report .

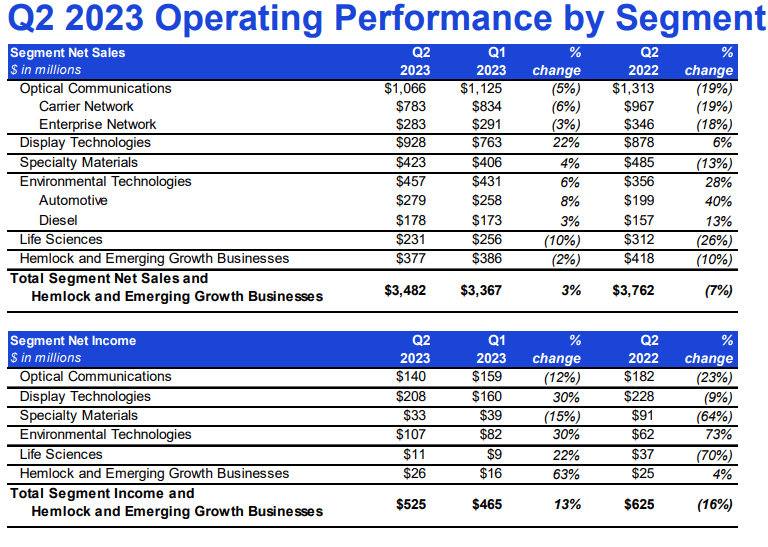

The main pain points from the Q2 2023 report were due to decreasing sales from fiber optic customers, despite the diversified revenue streams across consumer mobile devices, automotive, life sciences and solar. However, with a 36.2% gross margin and $0.45 core EPS, their profitability remains strong even in a weak quarter. Their forecast for Q3 2023 includes core sales remaining largely in line with Q2 at $3.5B, and I expect core EPS to slightly improve. My reasoning for this is based on continued growth across Corning's diverse profile, and a ramp up in optical communications revenue in late 2023 through 2024. I expect Q3 2023 to improve on the results from Q2 2023.

Figure 1: Q2 2023 Earnings Summary (Corning Q2 2023 Earnings Report)

{kind=link}

For Q3 2023, we should see the largest changes to come from optical communications and display technologies, the two largest segments of sales for Corning. While telecom networks may be slowing the pace of their 5G installations, I expect consumer and datacenter networking to continue to boom with the current government incentives and AI market. For datacenter revenues, I expect this to represent a growing segment as AI compute resources become ever more data-intensive.

Corning's consumer network sales are expected to increase in the near future with the BEAD program in the US funding $42.5B starting in late 2024 with the goal of greater broadband access across the US ( source ). The proposal phase is currently open for BEAD and BEAD-subsidized projects are projected to provide steady revenue through 2027. BEAD selection criteria target projects using end-to-end fiber optic connectivity wherever feasible to increase fiber coverage, even though subsidies are required to make them cost competitive. With their investment into building out a new facility in Arizona, Corning is well situated to supply broadband projects across the United States. Fiber optic infrastructure is split roughly 50-50 between labor and supplies, and the BEAD program will likely drive $10-20B of fiber optic purchases from late 2024 until at least 2026. I expect that Corning and its compatriot CommScope will likely see preferential selection over international competitors such as TE Connectivity and Sumitomo.

Additionally, while the core customer base of telecom operators have been weak, as seen in the Q2 2023 earnings report, the datacenter segment has continue to rally. The growth of AI in hyperscale datacenters with insatiable demand for data transfer rates has required 2-5x more connectivity than even the typical high-performance compute center requirements. With projections for continued growth of AI data centers and hyperscale technologies, Corning is well-positioned to continue to sustain profitable operations and maintain cashflow as long-term projects begin to ramp up. The data transfer speeds required for the latest LLM AI training processes can only be satisfied via fiber optic interconnects. Corning has been critical in assisting the hyperscaling of many network centers with large interconnects to provide low-latency, high-bandwidth throughput between different physical sites. The numerous investments into AI training and datacenter compute capabilities will continue to drive revenue in the high-margin datacenter segment over more traditional enterprise networking.

In the display market, the constant improvements to advanced glass technologies allows for cutting-edge consumer devices. However, the bulk of Corning’s sales in this segment are more mundane, but much higher volume - Corning’s Gorilla glass on the front and backs of newer smartphones is critical for enabling transmission of 5G mmWave signals. I expect consumer device sales to remain steady as inflation continues to impact consumer spending, but expect new high-margin smartphones and other devices using bendable glass platforms to continue to represent a growing segment of consumer sales. As a growing portion of Corning's revenue profile, supplying custom solutions for niche and flagship consumer products contributes significantly to the strong profit margin Corning is able to maintain.

Lastly, Corning has a long history of driving R&D innovations and specialty products. This drives growth and opens new markets, but also allows them to continue to capture new revenue streams. This includes their recent and growing business as a supplier of lenses for EUV lithography, as well as their AR/VR high-quality glass screens. The recent push from government incentive programs into solar energy will allow their capital investments in solar to reap dividends in the next 1-3 years as the IRA bill continues to stimulate demand for US-made solar panels. These sectors represent a small, but high-margin, outlet for Corning’s substantial R&D spending and we can expect to see this continue to grow.

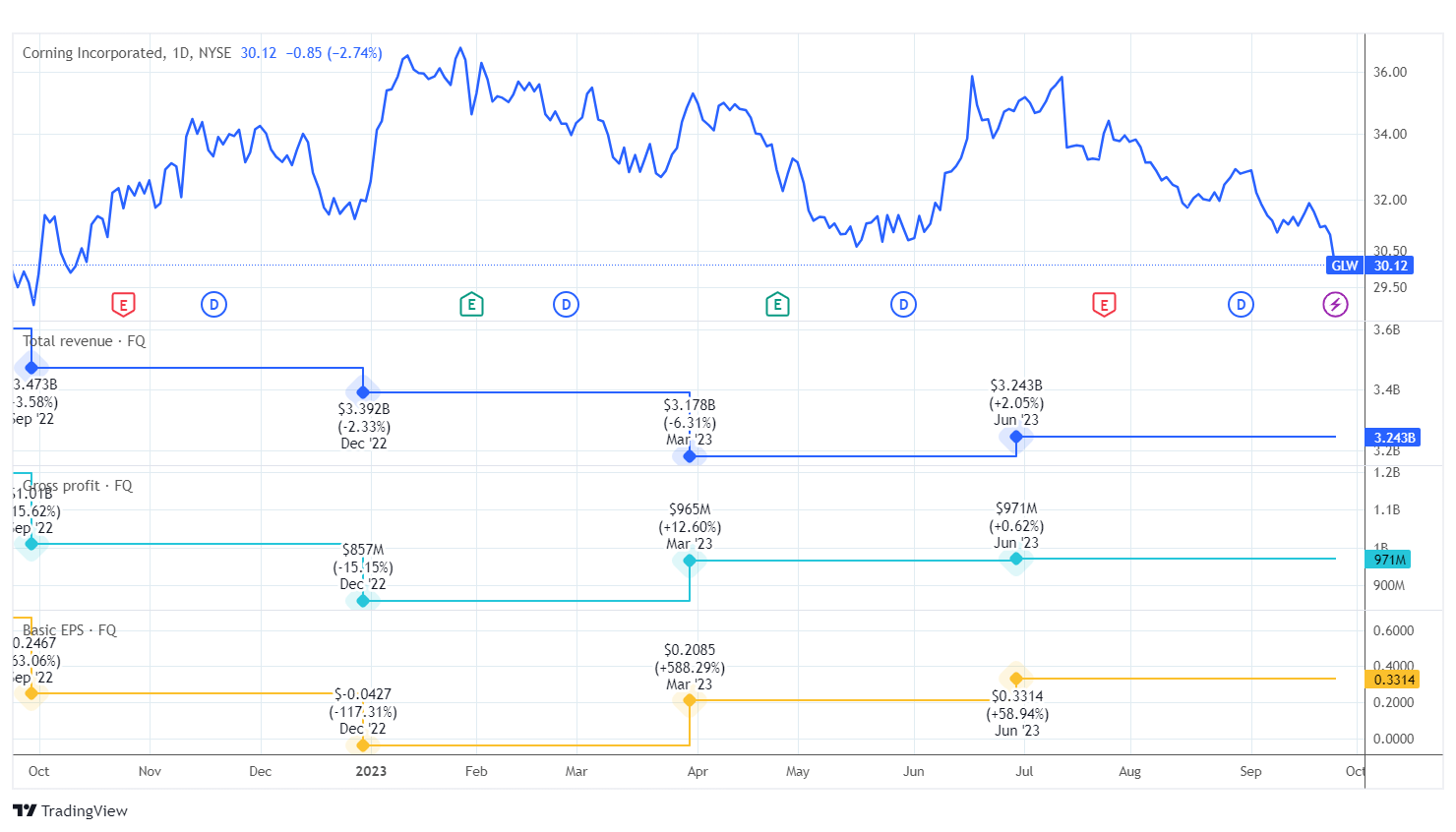

GLW: 1Y stock price history with quarter financials. Note the relatively stable revenue, profit and EPS despite the recent downward trend in price. (TradingView)

{kind=link}

I believe that Corning remains undervalued at the current price point around $30/share. Despite starting the year at over $36/share, the gross profit margin and EPS have remained steady. If Corning is able to continue to secure new revenue streams and build on existing partnerships, I expect their revenue growth to remain consistent around 4-5%. I predict a Q3 2023 EPS of $0.47, up 4.5% from their Q2 2023 report. Based on historical data, this would suggest a price target of $35-36 in the next 6-12 months. It bears noting that Corning is not without competition in this sector, but I think that their strong profit margins despite their prioritization of R&D spending is a winning combination in the long run.

In summary, Corning is well-positioned as an excellent choice for a low-risk stock pick with high exposure to the explosive AI growth that we have been seeing. Despite the recent doldrums in the price, with a 3.59% dividend yield and solid profit margins, I think that much of the turmoil of Covid-19 is behind the company and we can expect steady 3-5% revenue growth across Corning’s diversified portfolio. One can view the current pricing of stock around $30-31 as a discount ahead of improved Q3 2023 earnings, with a low-risk, high dividend yield for long-term growth.

For further details see:

Corning: Glass Technologies Behind AI And Consumer Devices Will Drive Q3 2023