GLW - Corning Incorporated: Decent Entry Point For The Long-Term Oriented Investor

2023-07-12 12:12:06 ET

Summary

- Corning Incorporated is predicted to continue generating revenue from its Optical Communications segment due to the US government's commitment to expanding rural broadband.

- The company's Display Technologies segment also holds potential for revenue growth, particularly in the mobile phone and automotive industries.

- Despite a healthy working capital ratio and interest coverage ratio, Corning's financials are considered underwhelming, with improvements desired in the upcoming quarters. The company's intrinsic value is estimated at $34.64 a share.

Investment Thesis

With the earnings just around the corner, I wanted to take a look at one of the companies that I use something made by them daily, Corning Incorporated ( GLW ) to see what kind of potential it has in the future and what I would be willing to pay for its prospects. If the rebounds in Optical and Display segments return, and the company manages to improve margins over the next decade, Corning is valued fairly right now and is a good buy for the long-term-oriented investor.

Outlook

Optical Communications

This segment has been the top revenue generator for a while now, and I see that it will continue to be that way for a while. More and more of the world is getting connected now, and it is very important to have a stable, fast, and reliable internet connection, especially after COVID. Corning manufactures fiber optic wire for many carriers and there is still a lot of work to be done.

Potential revenue growth in this sector I think will come from the US government's commitment to connecting rural America to the Internet. It will take some time, but the work is already on the way. Since 2015, the federal government has provided over $22B in investments to support the expansion of rural broadband. I would say that the number is much higher now since it’s been another 3 years since that article was published. As of 2020, around 22m of Americans in rural areas still lack an internet connection . I believe the initiatives from the government will work out and as recently as July 2022, $401m was provided to rural areas broadband expansion by the Biden-Harris administration, so the government is not sitting still because to be more advanced, the US will have to get connected, especially in the post-pandemic world.

Corning will capture a good chunk of these initiatives and will enjoy a steady revenue stream for many years to come.

Display Technologies

There is so much revenue potential in this segment. The most obvious one for me is the updated glass for mobile phones and tablets. There are so many phones out there in the world and screens break a lot. The company is constantly coming up with innovations in how to improve mobile screens, as phones get larger and heavier. Phone manufacturers in the future will opt to use the latest Gorilla glass iterations like the Glass Victus 2 .

I also see a lot of potential in the automotive industry, although the management does not share the same sentiment, as they believe the automotive segment will not recover yet in the 2 nd quarter . That is understandable, however, over the long run, cars will have more and more dashboards that are fully screen displays and Corning will see a lot of revenue coming from this segment in the long run.

I’m a little more skeptical on the AR/VR side of things as I know that there is a market for these products, however, I don’t think it’s going to be groundbreaking like I think the car or handset displays in my opinion.

Financials

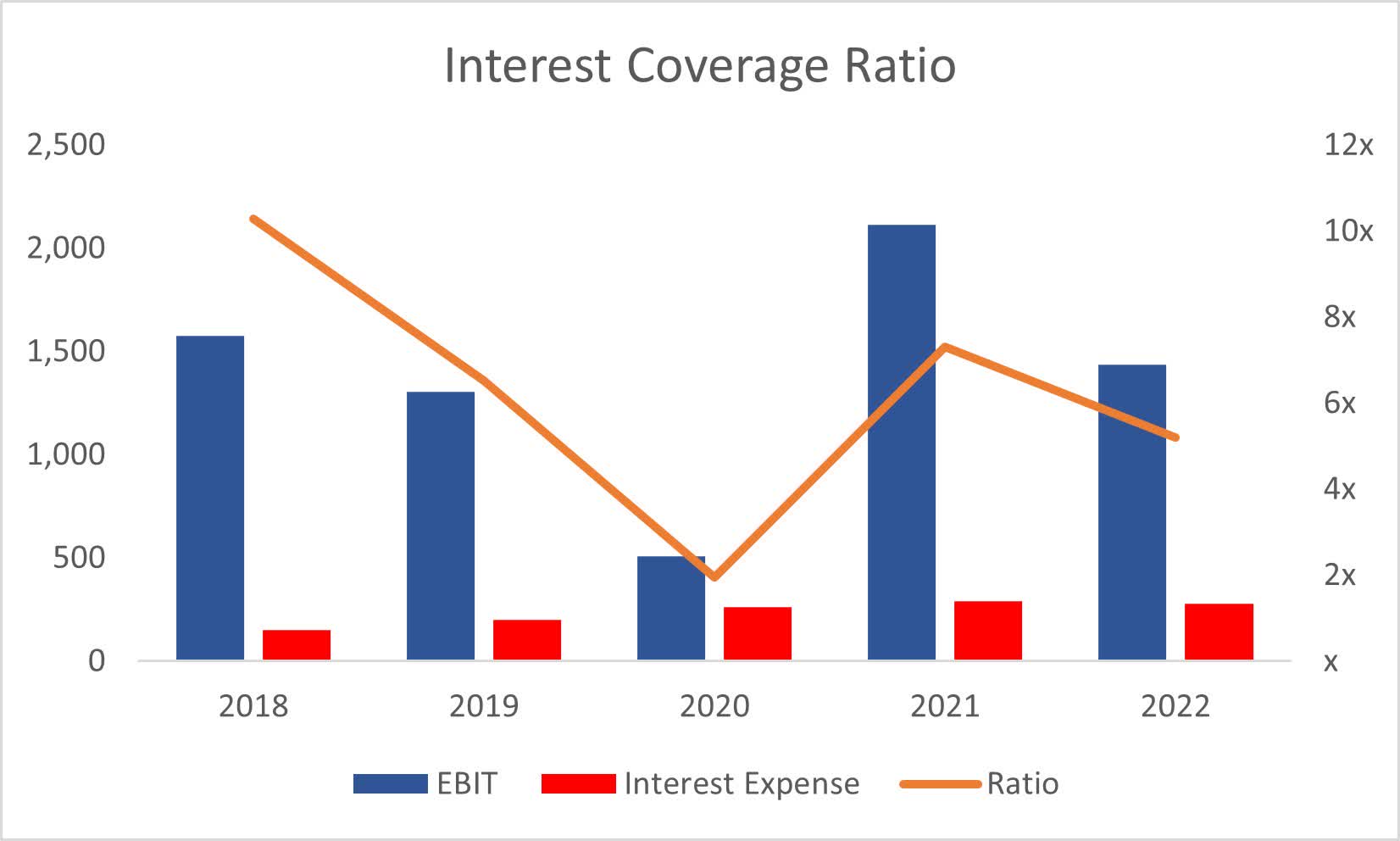

As of Q1 ‘23 , the company had $1.14B in cash against $6.6B in long-term debt. To me, that does not seem like an issue at all. After looking at the company's financial health, the interest coverage ratio stood at around 5x as of FY22, which means that EBIT covers annual interest expense 5 times over. That is well above the healthy ratio of 2x as considered by many analysts.

{kind=link}

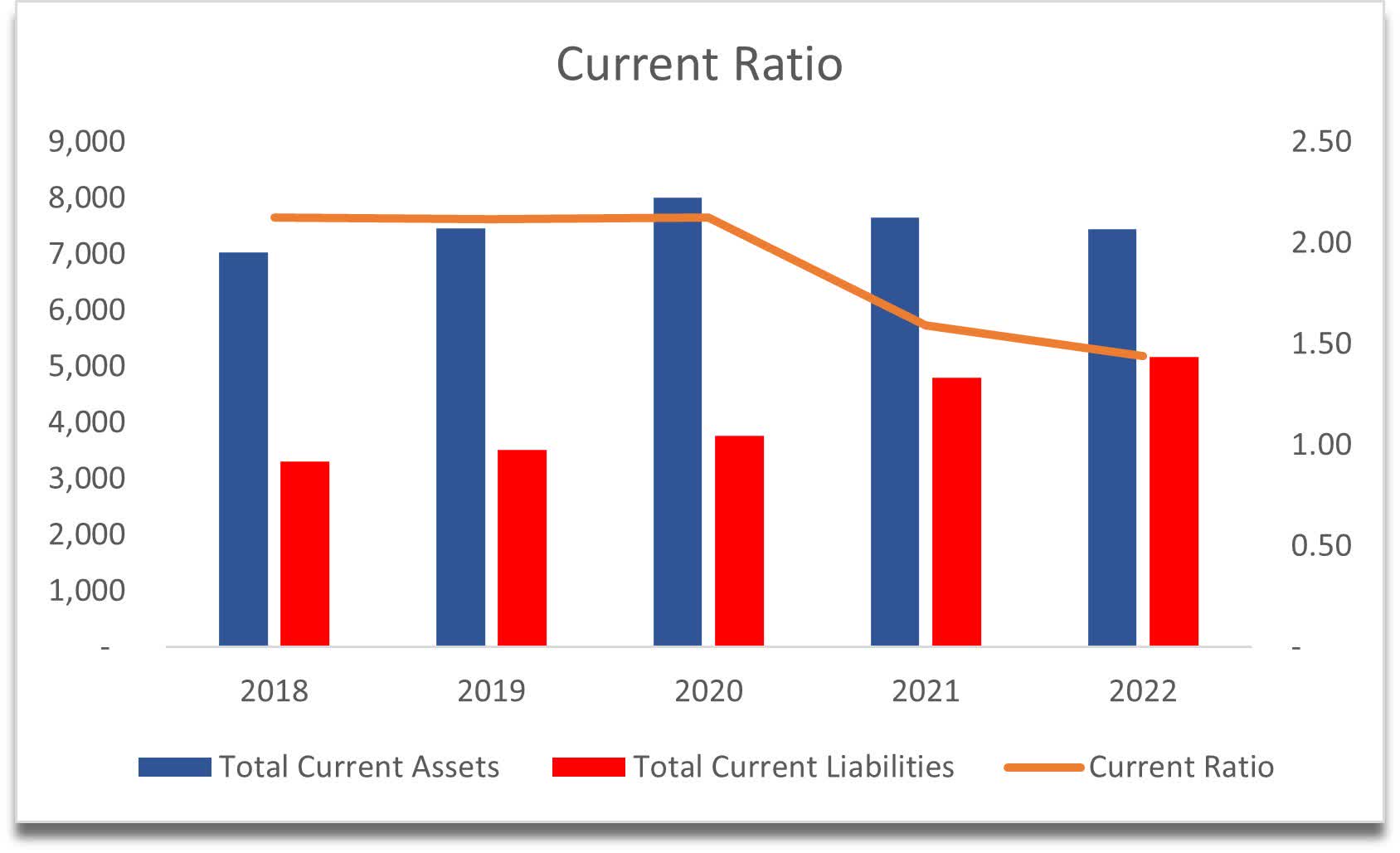

The company’s working capital ratio has been very healthy over the last 5 years at least, which stood at around 1.4 at the end of FY22, meaning if all of their short-term obligations had to be paid off at the same time, which is very unlikely, the company would be able to pay off everything and still have liquidity left over. I don’t see any liquidity or insolvency issues at the company.

{kind=link}

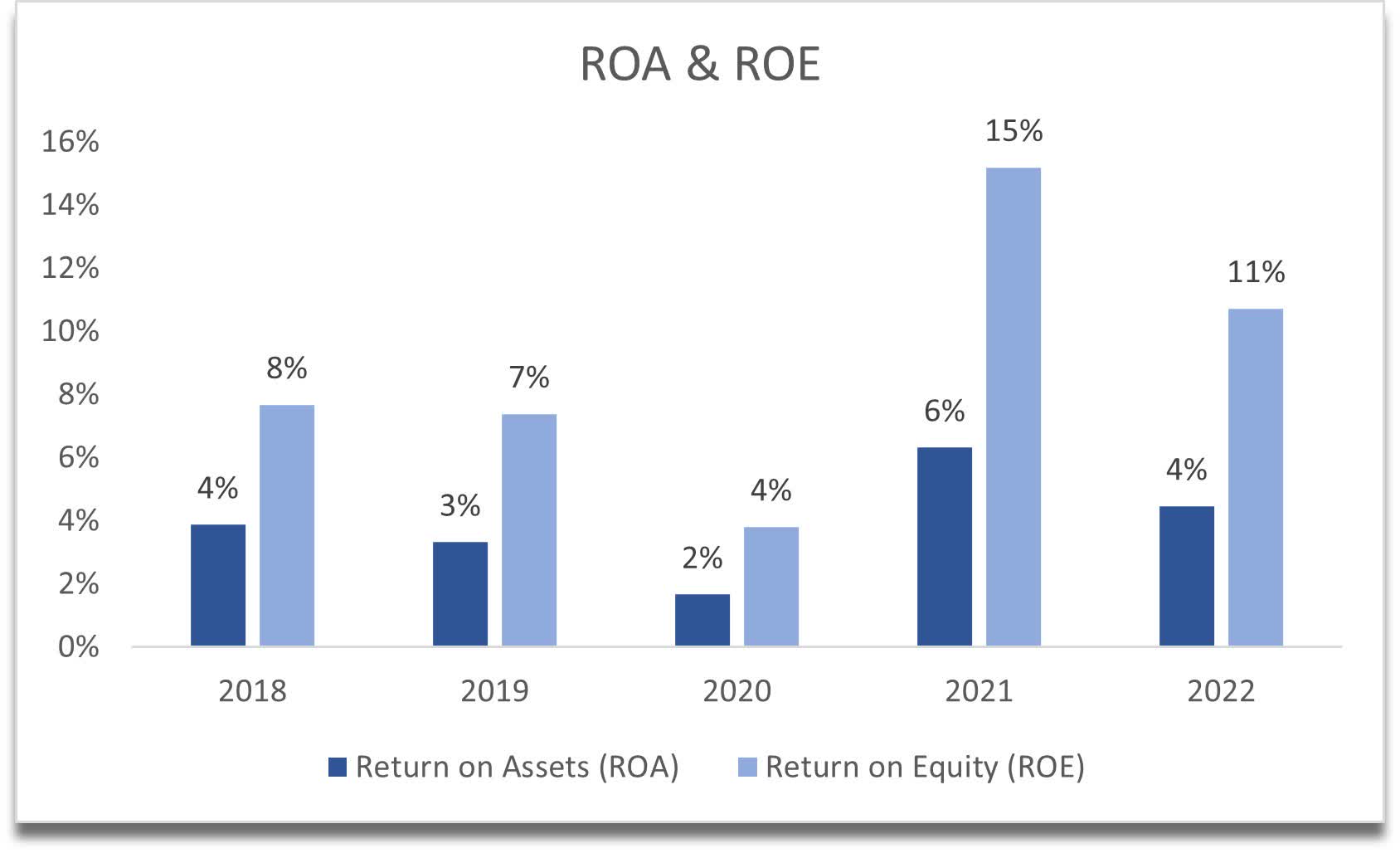

Looking into efficiency and profitability, the company’s ROA and ROE aren’t very impressive. They are just about what I think is acceptable, meaning the company can utilize its assets and shareholder capital better, however, these are acceptable. I would like to see these improve over time.

{kind=link}

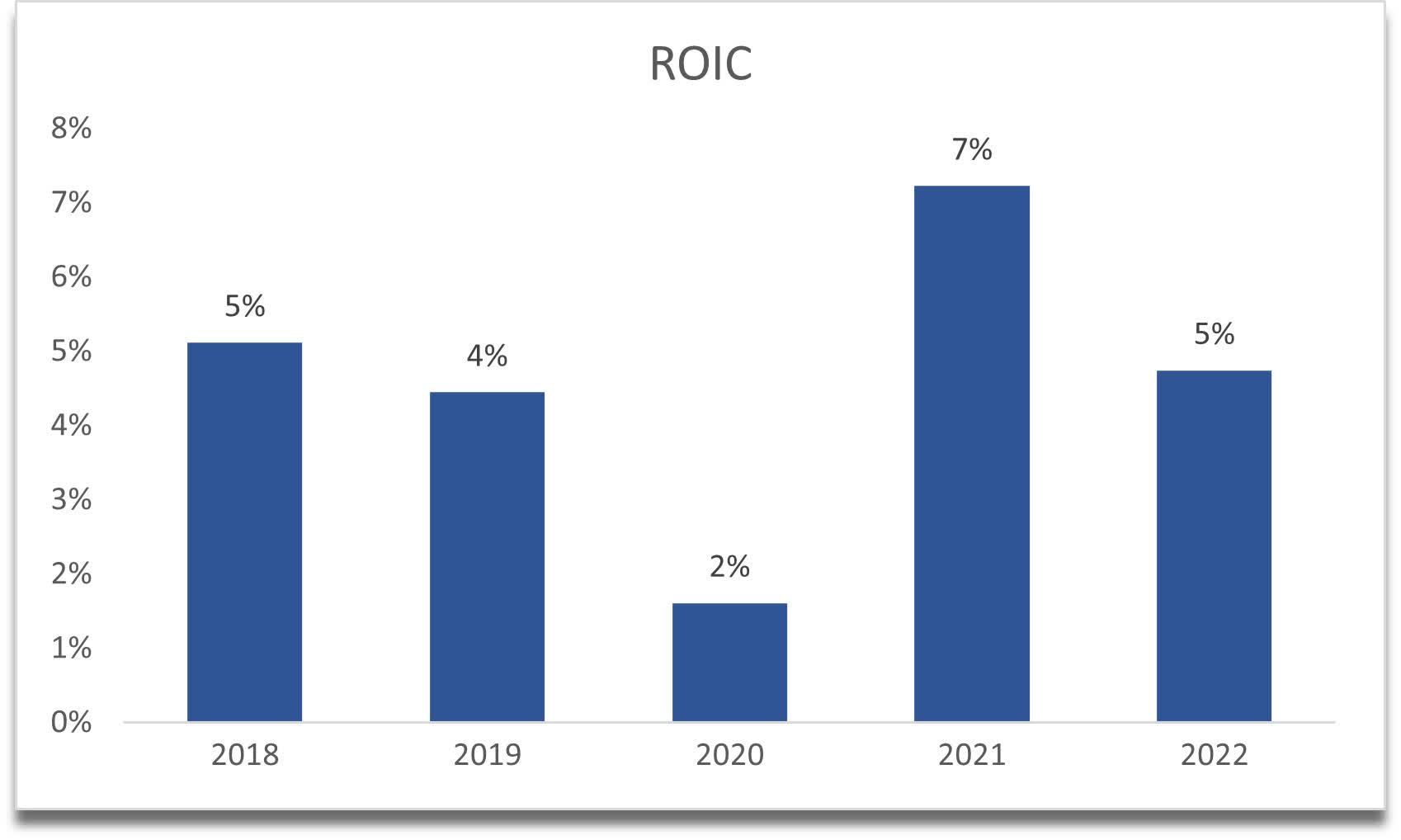

In terms of return on invested capital or ROIC, I was expecting to see a much higher number, especially since the CFO in the latest transcript said that the investment opportunities they target “generate 20% ROIC or greater”. Maybe these opportunities are still in their infancy because historical ROIC has been below 10% for at least 5 years now and fluctuating without a clear direction. I would like to see at least 10% in the future, which will tell me that the company is enjoying a competitive advantage and a strong moat.

{kind=link}

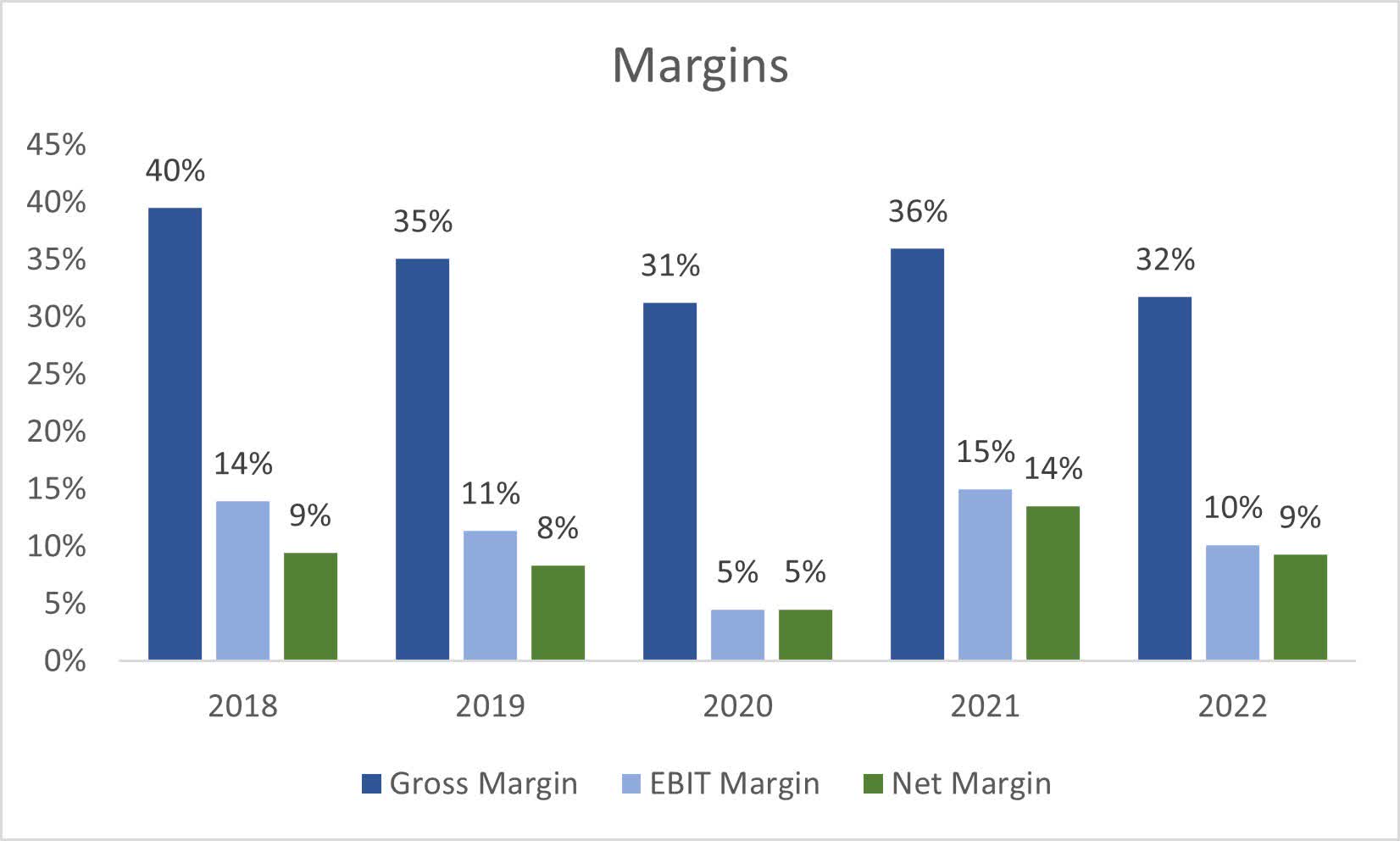

In terms of margins, these have recovered from the pandemic lows, however, also saw a slight decline from FY21 which is not good. So far in Q1 '23, gross margins returned to 35% and operating margins to 15% which is in line with FY21. We would have to wait for the full year’s results to see if they managed to maintain these margins or even improve them.

{kind=link}

Overall, the financials are quite underwhelming. They’re not the worst but also there is a lot to be desired. I would like to see improvements in the upcoming quarters to see which direction these metrics are going.

Valuation

In terms of revenues, I decided to go with around 4% CAGR for the base case, which includes around 3% decline in FY23. The company managed to grow at around 7% in the last decade, so I am being slightly more conservative to give myself more room for error.

For the optimistic case, I went with 8% CAGR, while for the conservative case, I went with 2.2% CAGR for the next decade. All scenarios seem to be possible in my opinion.

In terms of margins, I decided to go with improvements of around 800bps on gross margins over the next decade and around 100bps on operating margins. My reason is, just five years ago gross margins were 800bps or 8% better, so a linear improvement to those margins in a decade is very possible in my opinion. I don’t think there is much room for improvement in operating margins.

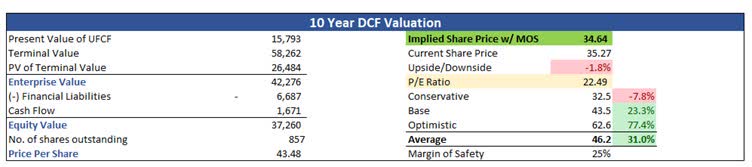

On top of these estimates, I will add a 25% margin of safety to be on the safer side even more. It looks like the company is priced fairly right now for a decent return for long-term-oriented investors in my opinion. The intrinsic value of Corning Incorporated is $34.64 a share.

{kind=link}

Closing Comments

The company has been around for a very long time. I don’t see it going away anytime soon. I believe it will keep a steady revenue stream for a long time, and to keep on top of it, it will keep innovating and adapting to the consumer market. It will keep providing the world with valuable fiber optic cables and connect everyone and provide protection for their screens and displays for future cars.

I would like to see some improvements in the mentioned metrics above in the future. Not to say that they are bad, just that they could be better in my opinion. The company has been buying back its shares aggressively and has pretty much halved in the last decade meaning the value of a single share doubled. If it continues to opportunistically buy back its shares, the long-term investor will be rewarded also.

For further details see:

Corning Incorporated: Decent Entry Point For The Long-Term Oriented Investor