GLW - Corning: Recent Weakness Provides Good Buying Opportunities

2024-01-13 05:39:22 ET

Summary

- Corning's stock has underperformed the market, but the company is still well-positioned to benefit from secular trends and has 20% upside potential.

- The company's Q3 earnings were weak due to macroeconomic weakness, but the balance sheet remains healthy and the stock offers an attractive dividend yield.

- Challenges for the top line are expected to continue in Q4, but the worst is likely behind the company and it has strong prospects in the fiber optic, clean energy, and specialty materials segments.

Investment thesis

My initial bullish thesis about Corning (GLW) did not age well since the stock by far underperformed the broader U.S. market with a -4.7% total return since early June 2023. The main reason the previous thesis did not age well is the top-line underperformance in Q2 and Q3, together with the shrinkage of the respective profitability metrics, but I believe it was due to temporary and not secular factors. While the thesis did not work well over the short term, today, I want to update it by emphasizing the company's solid strategic positioning to prove that the current challenges are highly likely temporary. To say shortly, from the longer-term perspective, the company is still very innovative and well-positioned to benefit from multiple favorable secular trends. Furthermore, my valuation analysis suggests that the stock has more than 20% upside potential. All in all, I reiterate my "Strong Buy" rating for Corning.

Recent developments

The latest quarterly earnings were released on October 24, when the company missed consensus estimates. Revenue declined by 5.7% on a YoY basis, and the adjusted EPS followed the top line by shrinking from $0.51 to $0.45. The revenue decrease was primarily due to the still soft demand in the Optical Communications segment.

Seeking Alpha

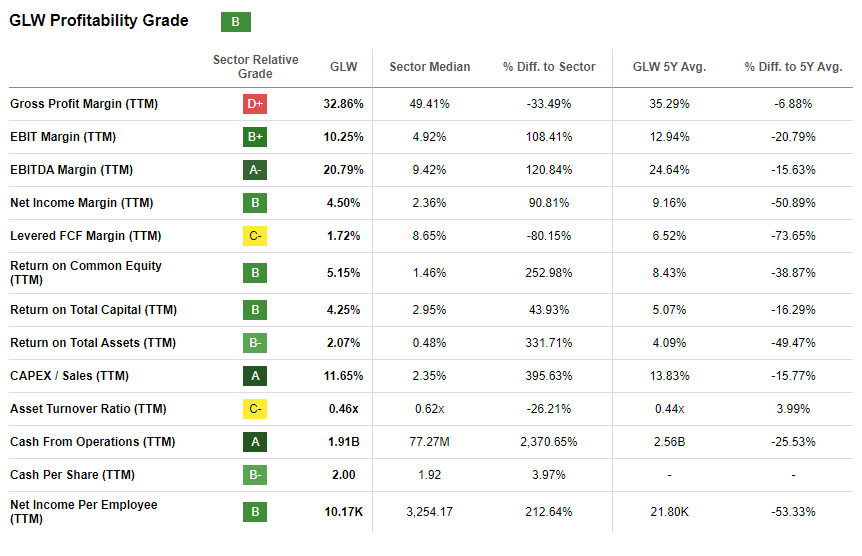

Looking at the financial performance in the first three quarters of 2023, all three quarters demonstrated YoY revenue declines with the EPS shrinking. This might look like a red flag for potential investors, but I would like to add a little bit of context here. First, the company demonstrated strong revenue growth in fiscal year 2022, which made comparatives much harder to bear. Second, The company's highly diversified revenue mix allowed GLW to minimize the revenue drawdown and to sustain profitability which is substantially higher than the sector median almost across the whole board.

{kind=link}

Despite facing temporary challenges in the macro environment, the company maintains a healthy balance sheet with solid liquidity and moderate debt levels. The $1.6 billion in cash as of the latest reporting date, together with the comfortably high covered ratio, gives me firm conviction that the company's solid dividend consistency grade is safe. The stock offers a 3.65% forward dividend yield; in the last five years, the CAGR was an impressive 9.2%. That said, GLW looks like an attractive option for dividend growth investors.

Seeking Alpha

Challenges for the top line are expected to remain the issue in Q4. The upcoming quarter's earnings release is scheduled for January 30, with consensus estimates projecting Q4 revenue at $3.25 billion. This will be about 11% lower compared to the same quarter 2022. The adjusted EPS is expected to continue declining with the projected YoY decrease from $0.47 to $0.41. I want to emphasize that there were eleven downgrade EPS revisions over the last 90 days which means that estimates are already very conservative. It is also crucial to know that the company historically has a strong track record of delivering positive surprises for the December quarter. That said, I expect Corning to deliver strong Q4 earnings.

Seeking Alpha

While current headwinds for the company are apparent and related to the weak end market demand due to substantial macroeconomic uncertainty, I believe the worst is in the rearview mirror. My optimism is based on several factors. Interest rates are expected to drop in 2024 as inflation is now finally not very far from historical averages. Amidst the disruptions caused by the pandemic and the Russia-Ukraine war, global supply chain routes have now regained stability. The fact that Corning's management maintains its substantial R&D investments despite the revenue decline also underscores that challenges are temporary. Another good sign is that profitability metrics and the free cash flow [FCF] keep up well despite an expected 8.4% full-year revenue decline.

Corning

It is apparent to me that the company's relatively weak financial performance over the last multiple quarters is due to temporary headwinds and not secular reasons. Unsurprisingly, end markets demonstrated softness in the high inflation environment where central banks of the developed world reacted with sharp interest rate hikes starting from summer to spring 2022. As a long-term investor, I prefer to ignore temporary headwinds because secular shifts are more important. From that point of view, Corning is an innovative market leader across several promising end markets. The company's well-balanced revenue mix allows it to avoid sharp fluctuations in revenue and profitability.

Corning's latest 10-Q report

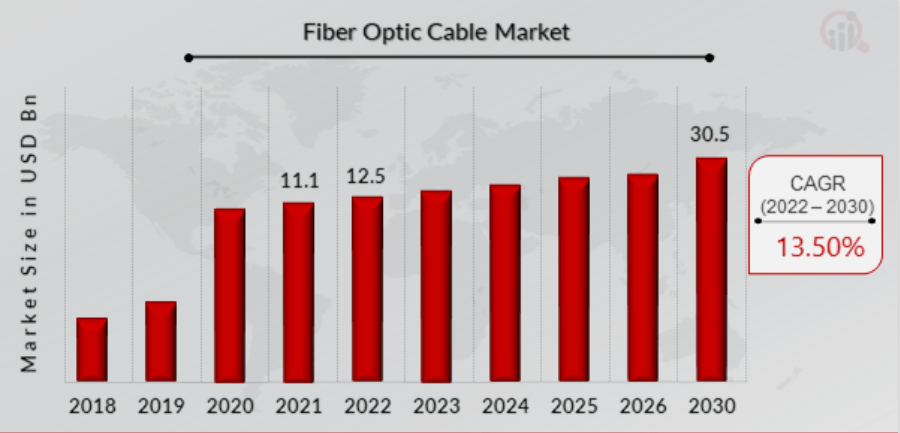

The fact that Corning's management sustains R&D investments at above $1 billion per annum underscores the company's bright prospects. The company's Optical Communications segment experienced a notable decline in 2023; however, secular trends look quite favorable for this business. Strong technological tailwinds will likely drive demand growth for multiple years for this segment: 5G, data centers, AI, and governmental initiatives to modernize infrastructure. This positive outlook is underscored by the expected 13.5% CAGR for the fiber optic cable market up to 2030. The fact that Corning surpassed one billion kilometers of optical fiber more than six years ago suggests the company has vast experience and reputation in this industry. Vibrant history, together with constant substantial investments in innovation, makes the company well-positioned to capitalize on the favorable trends in the fiber optic industry.

{kind=link}

Corning's exposure to clean energy should not be underestimated as well. Starting in 2027 , according to the new EPA's requirements, all new vehicles must implement particulate filters to reduce CO2 emissions. And Corning is the company that invented the gasoline particulate filter technology. The company has sold over 50 million filters throughout its history, meaning it has a vast presence in this niche. Corning is by far the largest player here, with a 27% market share. Apart from the exposure to legacy internal combustion engines [ICE], the company also aims to use electric vehicles [EV] with its auto glass for EV interiors and displays. That said, Corning will likely capitalize on the ICE and EV.

The company's Specialty Materials segment is probably the most well-known business to the broad audience since it is represented by the flagship Gorilla Glass, which dominates in the premium smartphones industry, accounting for a staggering 40% market share . Apart from its famous Gorilla Glass, the segment is also firmly exposed to the semiconductor industry , which is also experiencing a boom due to strong tailwinds behind its back.

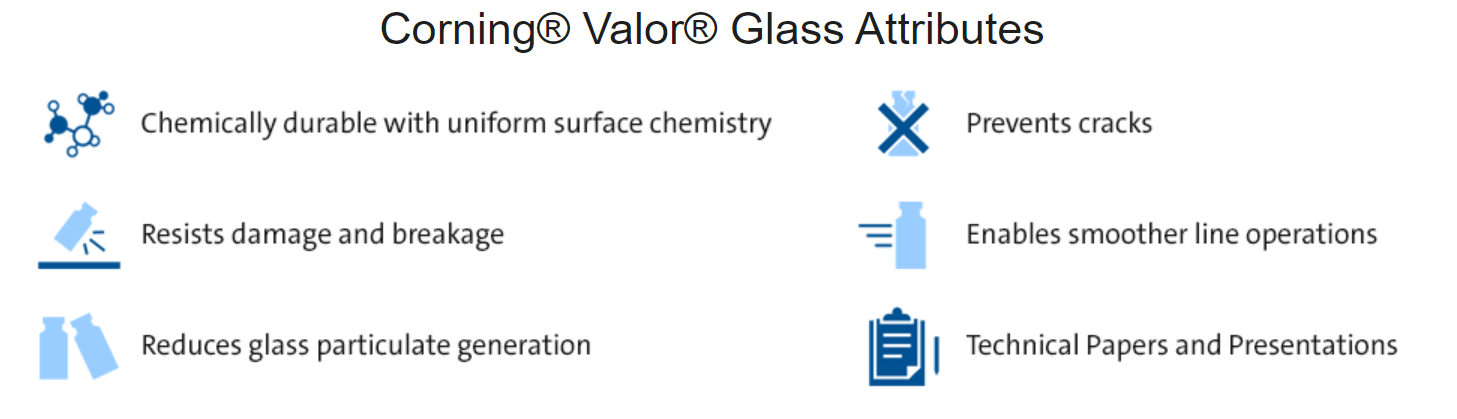

Lastly, the company's relatively new business is the Life Sciences. The segment is the smallest and experienced a massive YoY revenue drop in Q3, but I believe Corning also has an ace on its sleeve here. I am not an expert in pharmaceutical packaging, but after reading the product's description on the company's website, it looks like Valor Glass is an absolute disruptor. Valor Glass is a true disruptor because the pharmaceutical package industry has been very conservative for decades by using traditional borosilicate glass, the technology invented in the late 19th century . From our everyday lives, we all know that traditional borosilicate glass is very fragile, and Corning's Valor Glass provides superior resistance to damage . The fact that Corning has a long-term purchase and supply agreement for Valor Glass with Pfizer (PFE) looks like a strong quality sign to me. However, it is important to understand that supply contracts are usually long-term in the pharmaceutical industry, and it will take time for Valor Glass to expand its market presence. Overall, the pharmaceutical glass packaging market is expected to compound at an 8.5% CAGR over the next multiple years, which is another solid tailwind for Corning.

{kind=link}

All in all, I like the company's wide exposure to promising end markets and its long-term commitment to innovation, which is not sacrificed even in the current uncertain environment. Current headwinds are temporary, and the company is well-positioned to return to its revenue growth path once the macro environment strengthens, which is just a matter of time.

Valuation update

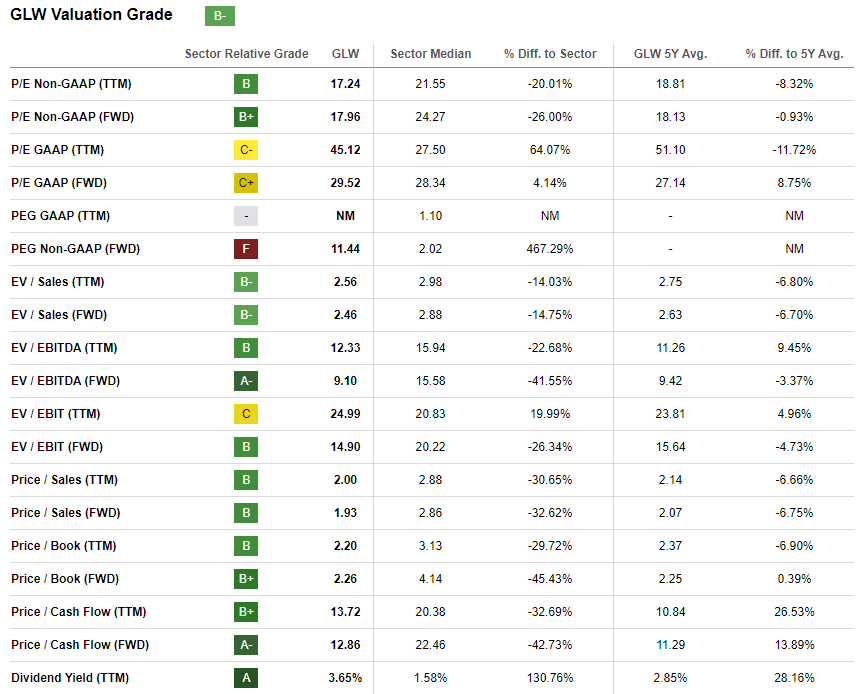

GLW significantly lagged the broader U.S. stock market over the last 12 months with a -16% price decline. On the other hand, the start of 2024 was quite positive, with the stock price appreciating by around 1%. Corning's current valuation ratios are very close to historical averages across the board, which suggests GLW is fairly valued.

{kind=link}

I think Corning is a mix of growth and value company, which is crucial to understand while selecting the valuation approach. Given the attractive dividend yield and growth, I want to implement the dividend discount model [DDM] approach. I use an 8.5% WACC recommended by Gurufocus. Consensus estimates project a $1.16 dividend for FY 2024, indicating a 2.6% growth compared to FY 2023. This looks conservative compared to the longer-term CAGR, which applies to my DDM. GLW's last decade's dividend CAGR is 11%, which will be too optimistic to use for valuation. Given the current headwinds and my risk-averse profile, I prefer to discount the last decade's CAGR by 50% and implement a 5.5% long-term dividend growth rate.

Author's calculations

According to my DDM simulation, the stock's fair price is $38.7. This is 26% higher than the current share price, representing a massive upside potential. Readers should also not forget the current attractive dividend yield and solid history of dividend growth.

If we add context from my previous valuation analysis perspective, the target price produced by the DDM simulation last time was slightly higher due to a more optimistic FY 2024 dividend estimate. However, I believe the $1 decrease in the target price is not dramatic. I would also like to underline that compared to my previous valuation analysis, I have dropped the discounted cash flow [DCF] approach because of the high level of uncertainty regarding the pace of the revenue and FCF margin recovery.

Risks update

The sentiment around the stock has been quite negative for a while, which we can see in the relatively weak momentum grade. It is highly likely that to break this trend, Corning will need a couple of quarters of strong earnings beats or solid guidance upgrades. That said, investors who are interested in opting in should be ready to accept that it might take several quarters to restore the market's confidence in GLW's prospects.

The pace of the company's top-line recovery will depend on macroeconomic factors to a great extent. Despite inflation cooling down in the U.S., the Fed is expected to be much less hawkish in 2024, but the level of uncertainty is still extremely high. There are still two large military conflicts in Europe and the Middle East, which add massive unpredictability for commodities. The presidential election scheduled in late 2024 adds an additional layer of uncertainty. Last but not least, even after three rate cuts expected in 2024, interest rates will still be relatively high.

Bottom line

To conclude, Corning is still a "Strong Buy" for long-term investors seeking a high-quality business delivering solid dividend growth. The revenue dip this year is temporary, and the company is well-positioned to capitalize on multiple favorable secular shifts thanks to its strong commitment to innovation. Lastly, my valuation analysis suggests the stock is substantially undervalued.

For further details see:

Corning: Recent Weakness Provides Good Buying Opportunities