GLW - Corning: Stock Price Decline Is Justified

2023-11-28 07:34:13 ET

Summary

- Corning stock does not meet the criteria for a rational stock investment due to slow earnings growth and inability to keep up with inflation.

- Historical earnings growth for Corning has been below the minimum required level of 4%, making the stock unattractive.

- Corning is considered a "no-growth business" with limited potential for future growth, making it unappealing for investors.

Introduction

It's always important that investors understand the reasons stocks can be attractive investments relative to other alternatives. In the case of a stock like Corning (GLW), understanding this is even more important because I don't think Corning stock meets the basic criteria that underpin a rational stock investment. One of the most important reasons, if not the most important reason to invest in stocks is that, unlike bonds and cash, the stocks of quality businesses have the ability to grow their earnings at a rate equal to, or greater than, inflation -- even if we don't know what the future inflation rate will be. That's because the key feature of a quality business is durable pricing power. In fact, I literally define the term "quality business" by its ability to grow earnings faster than inflation over a complete business cycle. If the businesses can't do that, then it's not a high enough quality business for me to own, and alternative investments become more attractive than the stock.

It is only after this basic quality metric is achieved, that I move on to determine a valuation for the stock based on future earnings expectations. I have found that historical earnings trends are one of the best predictors of future earnings trends. So let's start by examining Corning's historical earnings growth.

Corning's Earnings Growth

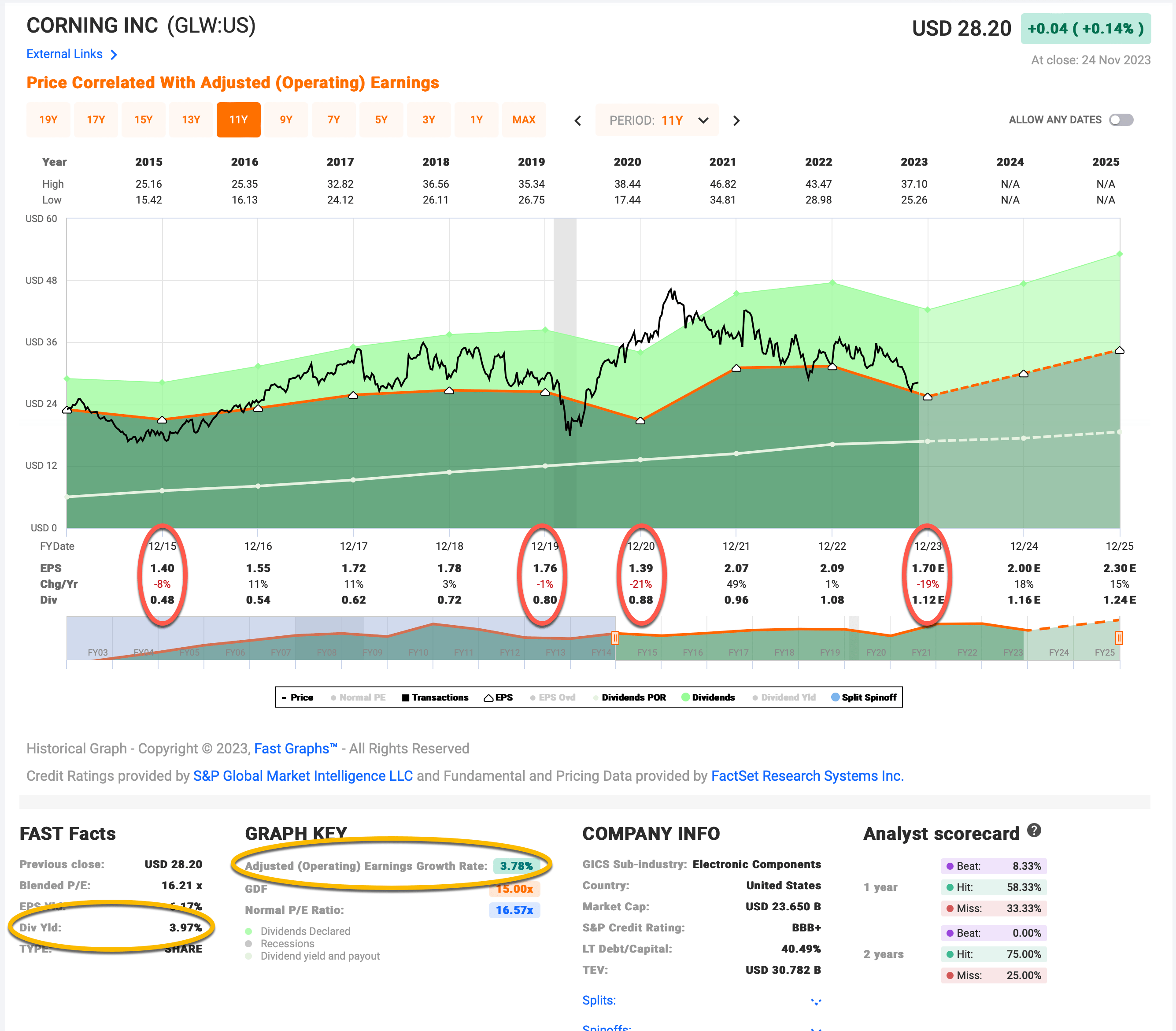

Below is a FAST Graph of GLW since 2015.

{kind=link}

In the FAST Graph, I want to first highlight the most optimistic earnings growth expectation, which is the one measured from 2015 through the expected EPS in 2025, and is circled in gold in the FAST Graph at +3.76%. I call this rate "optimistic" for three reasons. The first is analysts currently expect mid-teens earnings growth in 2024 and 2025, and that growth hasn't actually happened, yet. If we measured just from 2015 through 2023, the earnings growth rate would be +1.18%. The second reason it's optimistic is that FAST Graphs measures earnings growth from point to point so it does not take into account the negative earnings growth years in 2015, 2019, and 2020, which, if accounted for would lower the average earnings growth this period. The third reason it is optimistic is that EPS growth has been distorted by significant stock buybacks during this period, which serve to inflate the earnings per share because the number of shares is being reduced.

Before I move on to my more pessimistic assumptions, I want to point out that even the more optimistic assumption based on historical performance is only +3.76% earnings growth. That rate is below my minimum required earnings growth level of 4%. So, even optimistically, this stock is not attractive unless one thinks the future will be significantly different than the past 9 years (or 15 years, because if we go back to 2007 the earnings growth rate is still very slow). I use 4% as an approximate cut-off for earnings growth because historically inflation in the US has been between 3% and 4%, so a quality business, by my definition, should be able to grow earnings faster than that. Additionally, businesses with slow earnings growth often eventually have earnings growth turn negative, and when that happens, the stock price almost always falls fairly rapidly and in many cases never recovers. So, experience has taught me it's best to avoid any stock that is in danger of secular earnings decline.

More Pessimistic (Realistic) Numbers

When I run my basic historical earnings growth numbers and take into account the years in which earnings growth declined from 2015 to 2023 I get an even more humbling +0.49% earnings growth CAGR over these years. Earnings growth is still nominally positive, at least, but did not keep up with inflation.

But the bigger issue is the amount of shares GLW has bought back during this time period.

GLW reduced the number of shares outstanding by 1/3rd. Reducing the number of shares inflates the earnings per share because the number of shares is decreased, making earnings growth look higher than it really is. When I control roughly for what earnings growth would be without the buyback I get -2.76% CAGR over this period. So earnings are actually shrinking over time.

Sometimes revenues can tell a story that earnings do not. So they are worth checking.

Over the past 5 years, GLW's revenue growth has not kept pace with inflation.

Moving back to 9 years ago, revenue growth is just barely keeping up with inflation.

When we put all these pieces of data together I think it's fair to call Corning a "no-growth business".

Capital Allocation Preferences

I am not primarily a dividend investor, so I'll just put that out at the beginning here. And I don't think there is necessarily anything fundamentally "wrong" with a business that is only growing around the rate of inflation. Every business has an addressable market and when it's filled we shouldn't expect a business to keep growing as though it weren't. However, when it is the case that a business doesn't have any real growth, my preference is they give back their earnings to shareholders in the form of a dividend so shareholders can then invest that money into a business that does have more growth potential (or, spend it as the shareholder sees fit). That returned money can also act as a sort of insurance policy if the business slowly declines over time. At least the investor has a good chance to get their money back.

Currently GLW's dividend yields about 4%. It's obviously up to each investor what sort of return hurdle they require before investing in something. In theory, a retiree who needs a 4% yield from their portfolio plus inflation, could buy GLW here and have a decent chance of achieving that, though they would have no margin of safety, and it would take about 17 years for them to earn their initial investment back via the dividend. It might take a little less time, around 15 years if the dividend grows a little faster, and, in theory, with a current 65% payout ratio, that could happen. But my personal dividend yield threshold for a no-growth business is about 8%. If we assume no dividend growth above inflation, then that would require about a -50% price decline for GLW to get close to being attractive. With some dividend growth, perhaps a -35% decline would do it.

It does look as though the past couple of years the GLW has shifted more toward my preferred capital allocation. The buybacks have mostly stopped and the dividend has been raised about 10% per year. I think it's a good sign management has decided to take the approach of increasing dividends rather than buybacks.

Given this trend, if the stock price declines enough, at least in theory, it could become a decent buy for a dividend investor at some point in the future, but not yet, and not for me because I require certain levels of earnings growth.

Conclusion

Over the past 3 years, there have been about 30 articles on Seeking Alpha with a "Buy" or "Strong Buy" rating on this stock, and 0 "Sell" articles written. And in the past 9 years, there has only been 1 "Sell" article written. After noticing that, I thought I would at least offer to readers the reasons I would sell the stock if I owned it. Part of the reason is that I think history usually offers the best guide to the future, and another part has to do with the fundamental nature of why I invest in stocks in the first place. Other investors may have different fundamental reasons for buying stocks. But everyone who bought this stock in the past 3 years is underwater at this point. I thought this article might help explain why.

For further details see:

Corning: Stock Price Decline Is Justified