CAAP - Corporacion America Airports - A Lot To Like But Not Yet A Buy

2023-11-13 16:40:13 ET

Summary

- Corporación America Airports is a leading private operator of 53 airports across 6 countries.

- We cover some attractive narratives surrounding CAAP.

- We pick out the important talking points ahead of CAAP's Q3 results due to be announced on November 15.

- The charts suggest that a long position wouldn't be ideal at this stage.

Company Snapshot

Corporación América Airports S.A. ( CAAP ) is a Luxembourg-based entity that specializes in the acquisition, development, and operation of airport concessions. CAAP has been in this business for 25 years now, and as things stand, it operates 53 airports across six countries (Argentina, Brazil, Ecuador, Uruguay, Armenia, and Italy).

A Lot To Like

For a business of this sort to flourish, solid operating leverage is vital, and it's fair to say that CAAP has yet to hit its ceiling on this front.

{kind=link}

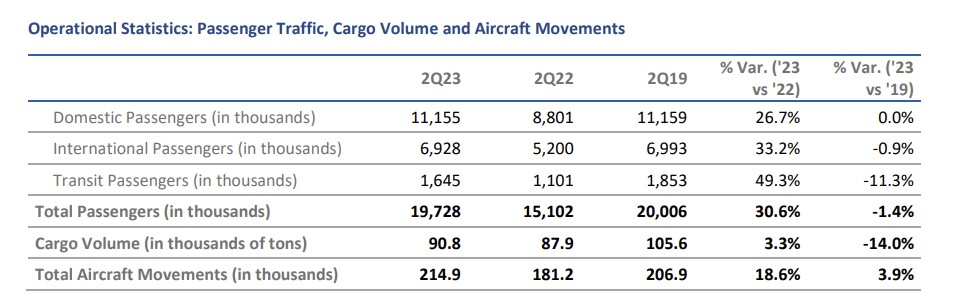

In Q2, passenger volumes across all its airports were still short by -1.4% relative to the pre-pandemic era, whilst cargo volumes were down by an even greater margin of -14%. Under ordinary circumstances, one would have expected this to translate to a weaker revenue cadence relative to 2019, but such has been management's prowess in extracting higher revenue per passenger, that the overall revenue growth is already up by 3% vs. the 2019 period.

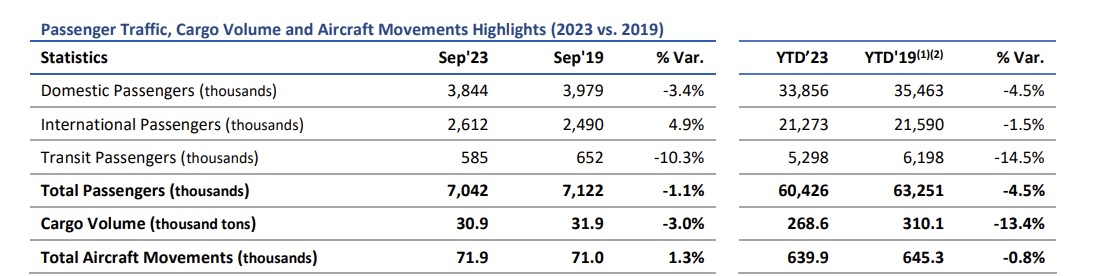

There's potential for this to still improve as the latest September data shows that passenger volumes across all its airports are still around -5% short of what was seen in the pre-pandemic years, whilst cargo volumes are short by an even greater margin of -13%.

{kind=link}

All in all, to get a sense of the stellar operating leverage in store, investors ought to look at consensus estimates through the next three years. Whilst CAAP may only likely witness mid-to-high-single digit topline growth, the earnings growth, particularly in FY24 and FY25, could come in at 2-4x the pace of the topline growth!

Seeking Alpha

Now that's what they could do with the existing capacity, but as part of its concessions, CAAP can also help drive increased air traffic and additional revenue growth by building out new infrastructure; we're talking about things like enhancing and re-working terminals, platforms, runways, adding more duty-free shops, retail stores, eateries, etc. All of this entails significant CAPEX and the question to ask is does CAAP have the necessary financial profile to fund its capital needs? The answer is a resounding yes.

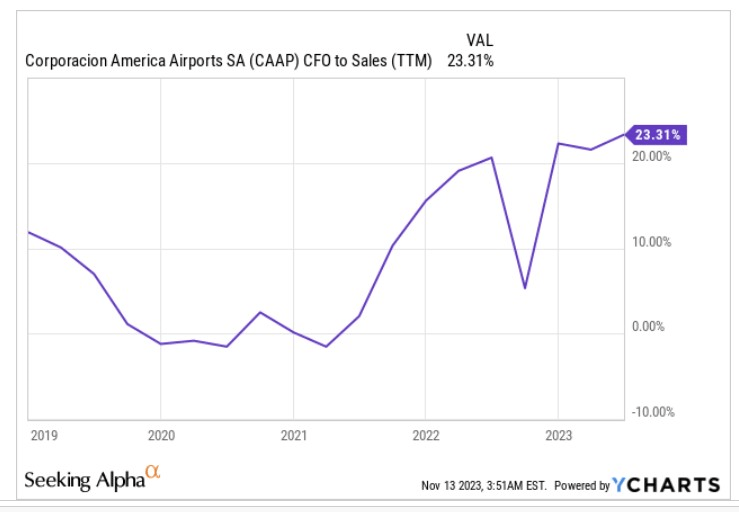

First of all, note that the level of sales that gets converted to operating cash flow is at almost 25%, which also represents 5-year highs.

{kind=link}

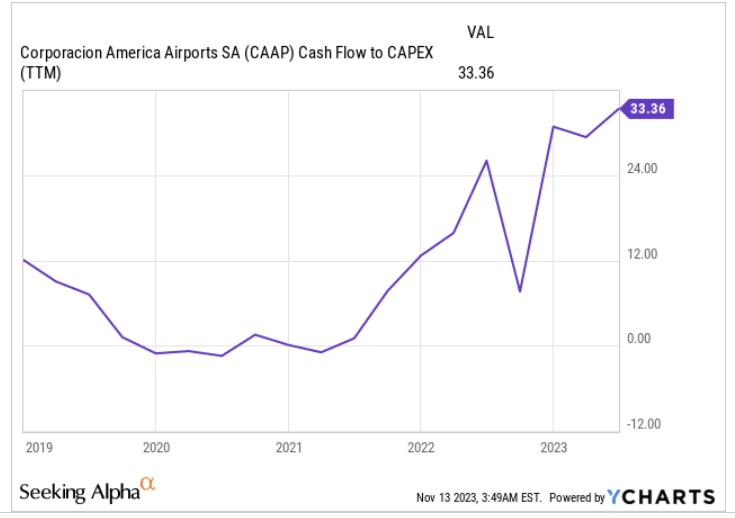

Now with a higher chunk of operating cash flow (OCF) brought to the table, CAAP's investment ambitions too are getting comfortably covered by 33x (once again 5-year highs)

{kind=link}

Separately, also note that management has done very well to bring down the degree of financial leverage in the capital structure, which puts CAAP in a solid position to bid for future concessions. CAAP's net debt level is currently at its lowest point in 11 quarters whilst the net debt to EBITDA ratio has dropped to record lows of 1.8x.

CAAP is also on the cusp of adding another arrow to the quiver - the untapped African market. Around a year ago, the consortium formed by CAAP won preferred bidder status for the operation of the Nnamdi Azikiwe International Airport ((NAIA)) Abuja, and the Mallam Aminu Kano International Airport ((MAKIA)) Kano two of Nigeria's leading airports, and they are currently in the process of finalizing that agreement.

At around N40bn , the domestic air cargo market may not yet be the biggest opportunity, but we'd like to think that this could be the start of a broader thrust within Nigeria and even Africa as a whole, as the government there is now a lot more open and forthcoming about ramping up Nigeria's air cargo value-chain.

Q3 Event - Key Discussion Points

In a couple of days from now, we could potentially have a catalyst as CAAP will publish its Q3 results on November 15, after market hours, followed by an earnings call the very next day at 9:00 AM ET.

Given CAAP's recent track record in trouncing EPS estimates (over the past five quarters, the earnings beat over consensus estimates has typically come in at over 4.5x), investors may likely be feeling emboldened ahead of the event. CAAP may well beat estimates yet again, but in the context of the performance seen in recent quarters, we think it would be prudent not to expect the company to hit those elevated standards yet again.

On the bottom line front, CAAP's EPS has been trending up sequentially since Q4 last year, but as per consensus estimates, this trend will reverse in Q3, with an expected EPS GAAP estimate of $0.34; that would constitute a -6% sequential decline, and an even greater percentage decline of -21% on a YoY basis.

Then, after witnessing a 37% spike in passenger traffic in Q1, followed by 31% growth in Q2, note that the pace of YoY growth has continued to slow sequentially in every month of Q3.

Monthly passenger traffic reports and Q2 report

In contrast to the picture of passenger traffic, you have cargo volumes that are poised to be a lot stronger in Q3, although one would be curious to hear from management if one of the biggest assets in CAAP's portfolio - the Ezeiza airport in Argentina has come through employee strike challenges seen in late Q3. Air cargo employees there went on strike, causing significant delays to ground transportation. Do consider that after two solid months of air cargo volume growth, growth came off significantly towards the single-digit levels in September.

Monthly passenger traffic reports and Q2 report

Closing Thoughts - Technical Considerations

Based on what the charts tell us, we're not overly optimistic about opening a long position at this juncture.

{kind=link}

The chart above measures how CAAP is positioned relative to other global infrastructure stocks including transportation infrastructure. In H2 last year, one would have eyed CAAP as a potential rotation option in this space as its relative strength ratio was only half as much as the mid-point of its long-term range. That narrative is no longer in play with the ratio now trading above the mid-point of its range.

{kind=link}

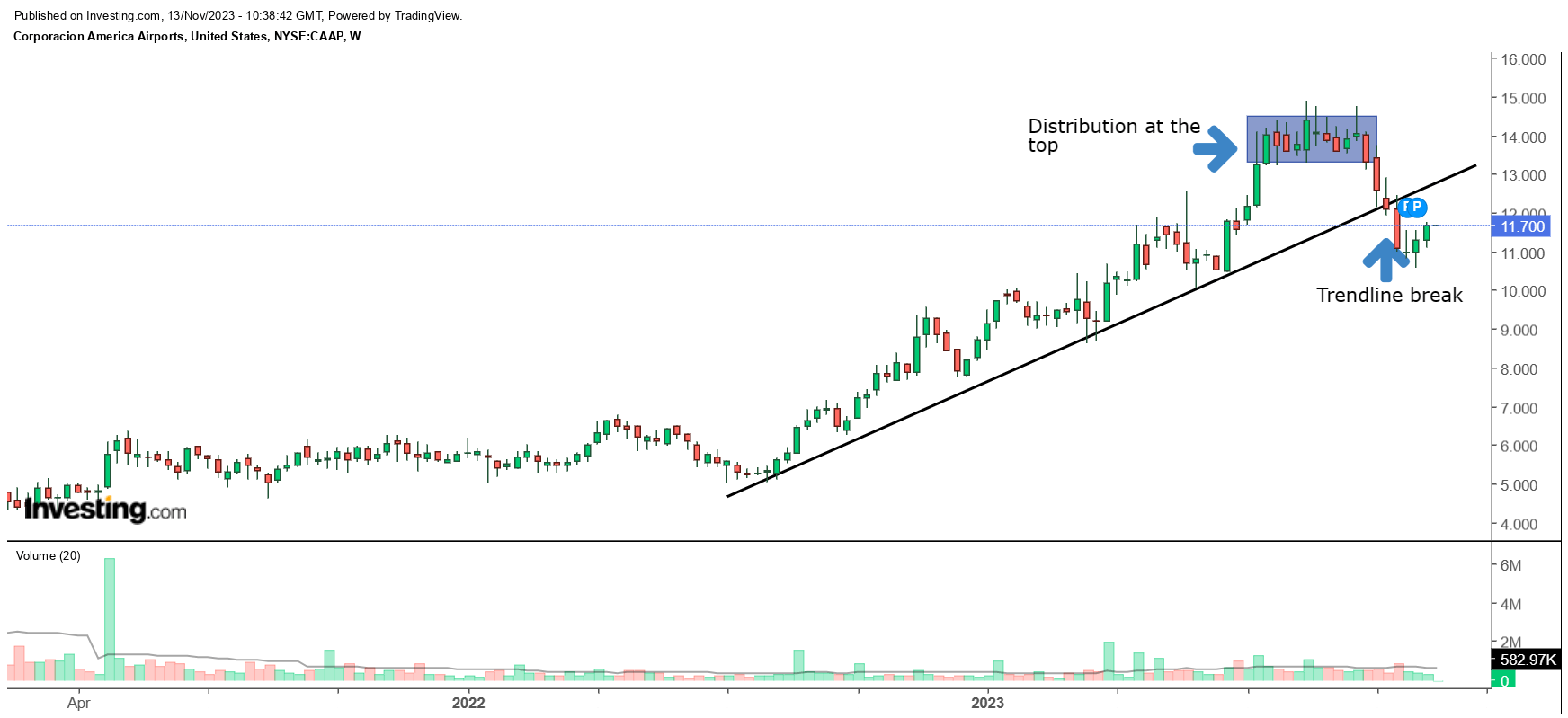

Meanwhile, on CAAP's weekly chart, note that from July last year until this year we had a rather strong uptrend, but then the price action began to flatten out at the top, reiterating the classic distribution phase. This terrain would've represented an opportune time to book profits. Then last month we also saw a breach of the upward-sloping trendline, reiterating the growing strength of the bears. Basically, what we have since September is a bearish flag pattern .

Given the onset of bearish conditions, we would prefer to wait on the sidelines and see if CAAP can defend the $10.59 levels during a potential sell-off. If it can demonstrate that, it would represent a defense of its previous pivot lows and would point to some underlying bullish support.

For further details see:

Corporacion America Airports - A Lot To Like, But Not Yet A Buy