ANYYY - Corporacion America Airports: Vertical Takeoff With Growing Market Trend

Summary

- Corporación América Airports manage and develop airport concessions in 6 countries.

- Passenger traffic is fast catching up to 2019 pre-pandemic data.

- The company is growing in revenue and margins and is planning new concessions.

- Even if the investment is very risky, the share price seems to be very attractive.

The aviation industry has probably experienced one of the worst periods in history during the pandemic and, with a recent fast recovery, one of the largest airport service providers in terms of airports served is benefitting from the trend and is betting on new expansions in new continents and on a new innovative electric air transport vehicle.

Corporación América Airports S.A. ( CAAP ) is part of Corporacion America International (a holding with various businesses in the energy, infrastructures, agriculture, and technology) founded by billionaire Eduardo Eurnekian who is the uncle of the company’s CEO Martin Eurnekian.

The company has a high-risk profile not only due to the high debt rate or most of the revenue derived from a country (Argentina) with a currency that could lose value by triple digits but also and above all due to the propensity to grow by acquiring airports concessions in very difficult contexts (Nigeria) or to invest in highly innovative projects such as eVTOLs.

On the other hand, the company was also able to emerge almost unscathed from 2 extremely difficult years and to enter the market with a very attractive share price. Passenger volume recovery is almost completed and the trend seems to be positive for 2023. My rate is Buy.

General Overview

Corporación América Airports, a Luxembourg-incorporated company manage and develop airport concessions. The company operates 53 airports in 6 countries on three continents from Latin America to Asia passing through Europe. It begins operations in 1998 through the acquisitions of the AA2000 Concession in Argentina which represent the core business country. Today the company is present also in Armenia, Uruguay, Ecuador, Brazil, and Italy.

Corporación América Airports acquire airport concession through a public tender and is involved in heavy investments in the airport’s infrastructure. These investments are mainly based on terminals, platforms, and runaway remodeling with also the target to increase revenue with new areas for stores.

The business revenue is based on passenger traffic that can generate aeronautical and commercial revenue through the services offered by the company. The airport agreements are mainly based on fees charged to departing passengers and to aircraft operators (for the uses of premises and other aeronautical services). Other sources of revenue are the commercial fees for food and beverage and duty-free stores but also for advertising and parking services.

The company was listed in 2018 on NYSE but operates globally for more than 20 years.

Financial and commercial development

Revenue and Profitability

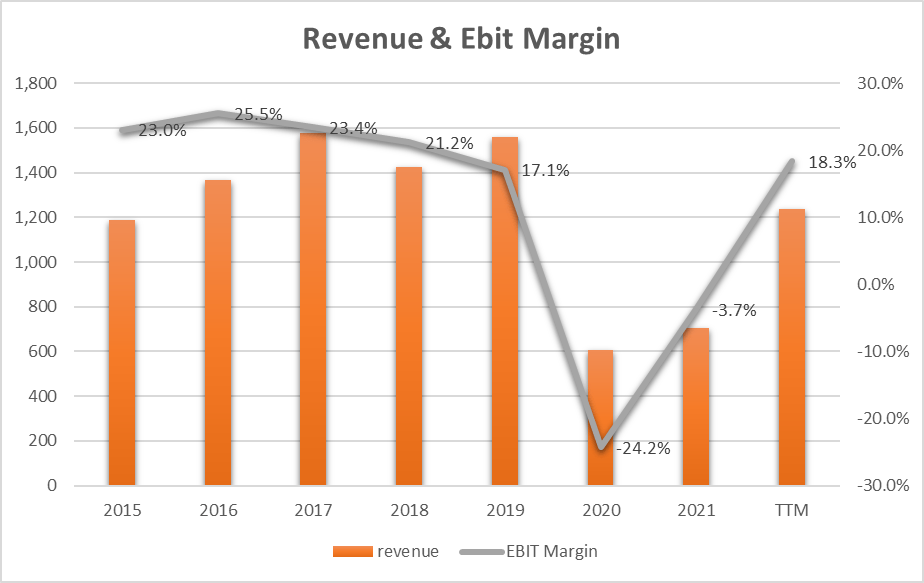

{kind=link}

Together with COVID-19, 2020 and 2021 marked the worst years for air traffic and should therefore be excluded from the comparison. From the graph, we can see how from 2015 to 2019 the company grew in terms of revenue while it had a decline in EBIT Margin which went from 23% to 17.1%. This is mainly due to an increase in direct costs or a decrease in gross profit. Going deeper into the topic of direct costs, we can analyze from Form 20-F of 2019 how construction services costs have increased by 77% and this can be linked to the increase in inflation in Argentina of 53.8% in 2019. In other words, it seems that active contracts do not protect the company in the event of rising inflation as much as direct costs grow.

2022 saw a recovery in air passenger traffic and this brought revenue back to the levels of 2015 while margins grew to 18.3% and which is a positive figure.

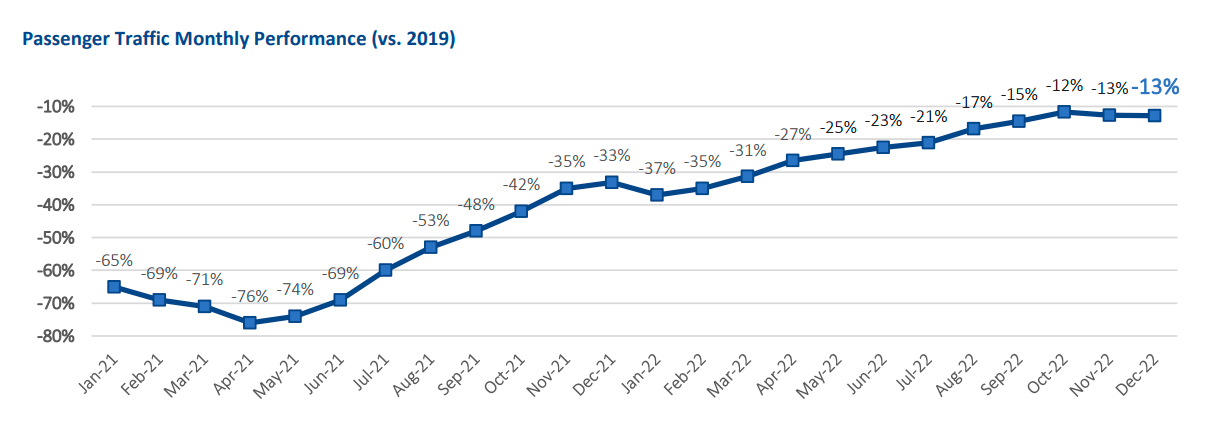

The most important key point parameter is passenger traffic

{kind=link}

If we want to take 2019 (pre-pandemic year) as a reference, we can note the monthly deviation from the targeted traffic which marks the full recovery of the business.

The figure stands at -13% on Dec 22 and we can see that starting from the beginning of 2021 there has been a rapid recovery in the total number of passengers which on Jan 21 was -65%. In the last 3 months (since October 2022) the growth trend seems to have momentarily stopped, which also happened a year ago.

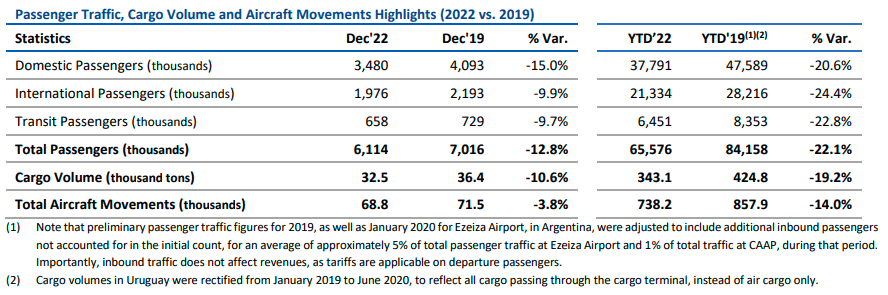

Going into detail on the type of passengers, we can see how international passengers have grown more (-9.9%) than domestic ones (-15%) and this could imply an effect linked to the macroeconomic trend of the countries where the company has the greatest revenue impact (Brazil and Argentina). The total movement of aircraft, on the other hand, was almost in line (-3.8%) with the 2019 figure. This could indicate that the airlines have made their entire fleet available and that greater aircraft saturation is expected.

The commercial part relating to cargo is growing more (-10.6%) than passengers (-12.8%) and this could indicate anticipation of the future growth of passengers as well.

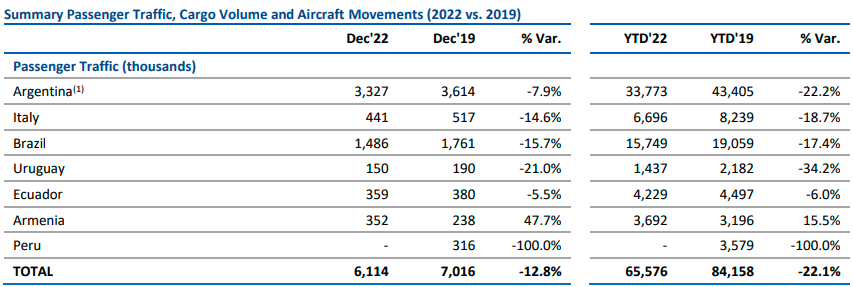

{kind=link}

If we analyze the passenger data at a country level we can see how Argentina in terms of YTD (-22.2%) determines the global trend (-22.1%). We can also note how the month of December saw an acceleration precisely in Argentina (-7.9%) and this is a very important element for the projections of the next quarters. Brazil and Italy, on the other hand, are growing at a slower pace.

{kind=link}

In conclusion, we can see that the passenger trend is approaching the peak of 2019 and that Argentina has been driving growth since December 2022.

Business Development

Corporación América Airports extended concessions in Uruguay until 2053 and in Argentina until 2038 and handed over the management of 5 airports in Peru to a local partner leaving the direct management in the country.

Abuja and Kano (Nigeria) represent the new opportunity as the Company is designed as a ‘preferred bidder’ for the concession of the two airports. So the new airport pipeline could be designed in the African continent! The Company is now waiting for the final decision by the Nigeria Government and it could be the first step for building a new African business. Speaking about Nigeria we can see that rampant terrorism, economic crisis, and turmoil over the presidential elections are the three major issues that dominate the country. The development plan in the new African country will therefore be full of challenges and difficulties precisely at the level of political and social stability.

Vertiports

Corporación América Airports is investing resources in the potential electric aircraft market. In December 2022 the company signed an agreement with Skysports Infrastructure for electric vertical take-off and landing [eVTOL] operations in Latin America. In June 2022 the Company signed a similar agreement with Eve Holding, Inc. ( EVEX ) for developing the same infrastructure in European airports. In 2026 the Winter Olympic Games will take place in Italy and the use of electric aircraft will be an absolute novelty in terms of air taxis. This could be an excellent stepping stone for the company to implement technical expertise in airport infrastructure management.

Martin Eurnekian (Corporación América Airports CEO) said :

“We already have a design for vertiports and we’re working with the whole ecosystem so it can actually work…If things continue as they are, we may see the first eVTOLs around the world in 2025 and 2026, and in Latin America between 2026 and 2027.”

Again Martin Eurnekian in terms of business strategy for the year 2023 underlined in the last earnings call :

First, we remain focused on building new routes to serve our passengers across our airport network. Second, this month, we received economic compensation for our concession in Brazil and remain focused on advancing with economic re-equilibrium process for our concession in Armenia. Finally, I reiterate that the key element of our growth strategy is to selectively expand our airport concessions, and we remain focused on pursuing attractive value-creation opportunities for our company.

The company is therefore defining the growth of revenue through new concessions as strategic even if these may be accompanied by a high risk (Nigeria for example)

Share price valuation

CAAP and Earnings Power Value

Assuming that the cash profit remains constant over the long term, I use the EPV (earnings power value) method to calculate the intrinsic share price value.

The method starts with EBIT. The second step is to add depreciation and amortization and then subtract stay-in-business CAPEX.

The result is the Cash Trading Profit

I then subtract the taxes by calculating the amount using the actual tax rate that the company pays.

The result is the After-Tax Cash Trading Profit

At least to calculate the total company enterprise value I divide the After-Tax Cash Profit by the interest Rate I define as fine for this kind of Company (CAAP is a high-risk company so I decided to use 15%)

The result is the Total Company Earnings Power Value. Dividing the result by the total number of shares we find the value per single share.

The table below shows the calculation for CAAP:

| EBIT |

| 227.30 |

| Dep & amort |

| 170.50 |

| CAPEX |

| -7.40 |

| Cash Trading Profit |

| 390.40 |

| TAX |

| 21.40% |

| TAX |

| -83.55 |

| After TAX cash profit |

| 306.85 |

| Interest Rate |

| 15% |

| EPV |

| 2045.7 |

| Share in issue |

| 160.8 |

| EPV per share |

| 12.7 |

$12.7 represents the share price valuation using the EPV method. If we compare the data with the current market price ($9.9) we see that the current price could be seen as cheap.

EPS Growth Model

The EPV approach may be a little bit conservative as there is no growth in earnings. Therefore I need to implement an alternative comparison method based on the estimated EPS growth in the next few years. Since the company is growing in terms of revenue and EPS, I decided to use the EPS growth parameter from 2015 which is 20.7% [CAGR], and halve it to maintain a safety margin. So 10% is the estimated growth rate [CAGR] of EPS.

The Formula is (by popular investor Benjamin Graham):

Intrinsic value per share = EPS x (8.5 + 2 g)

Where

EPS = earnings per share

g = EPS growth rate = 10%

{kind=link}

Example of calculation for 2023:

Intrinsic value per share = EPS x (8.5 + 2 g) = 0.56x(8.5+2x10) = $15.96

The last intrinsic value of $28.27 for 2029 underlines an annualized return of 18,9% as the current share price is $10.

18.9% is a great figure and is the annualized expected return for my investment in CAAP.

Peer Comparison

To compare CAAP with similar companies in the same Airport Services industry I have defined the following peers:

- Grupo Aeroportuario del Centro Norte, S.A.B. de C.V. ( OMAB )

- Grupo Aeroportuario del Sureste, S. A. B. de C. V. ( ASR )

- Grupo Aeroportuario del Pacífico, S.A.B. de C.V. ( PAC )

- Aena S.M.E., S.A. ( OTCPK:ANYYY )

Using Seeking Alpha's Quant Ratings we have a ‘Strong Buy’ rate related to the ‘Buy’ or ‘Strong Buy’ rating of the other company. These assessments highlight a very favorable moment for the airport services sector.

{kind=link}

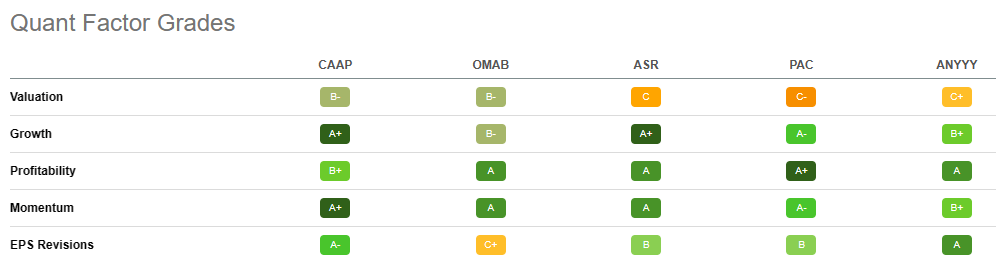

From the Quant Factor Grades point of view, we can see how CAAP is outstanding in Growth and Momentum. Only in Valuation, the grade is ‘B-‘ and only OMAB reaches the same grade, all the others are less preferable. Profitability is ‘B+‘ but if compared with peers CAAP represents the worst choice. Globally CAAP has the best mix factor grades and, at the moment, represents one of the best investment opportunities.

{kind=link}

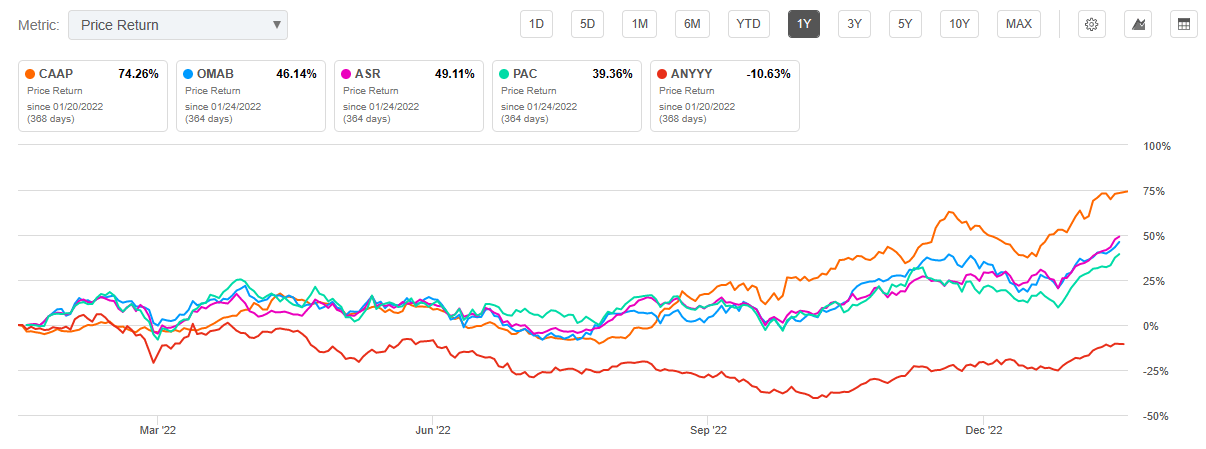

Looking at the share price trend we can see how CAAP has been the best performer in the last year with a 74% return and despite this result, it continues to have a very attractive share price valuation. The second performer is ASR but it has a ‘C’ in valuation and this could represent a second choice in terms of investment.

{kind=link}

A high debt level and high inflationary environment could represent high Risks

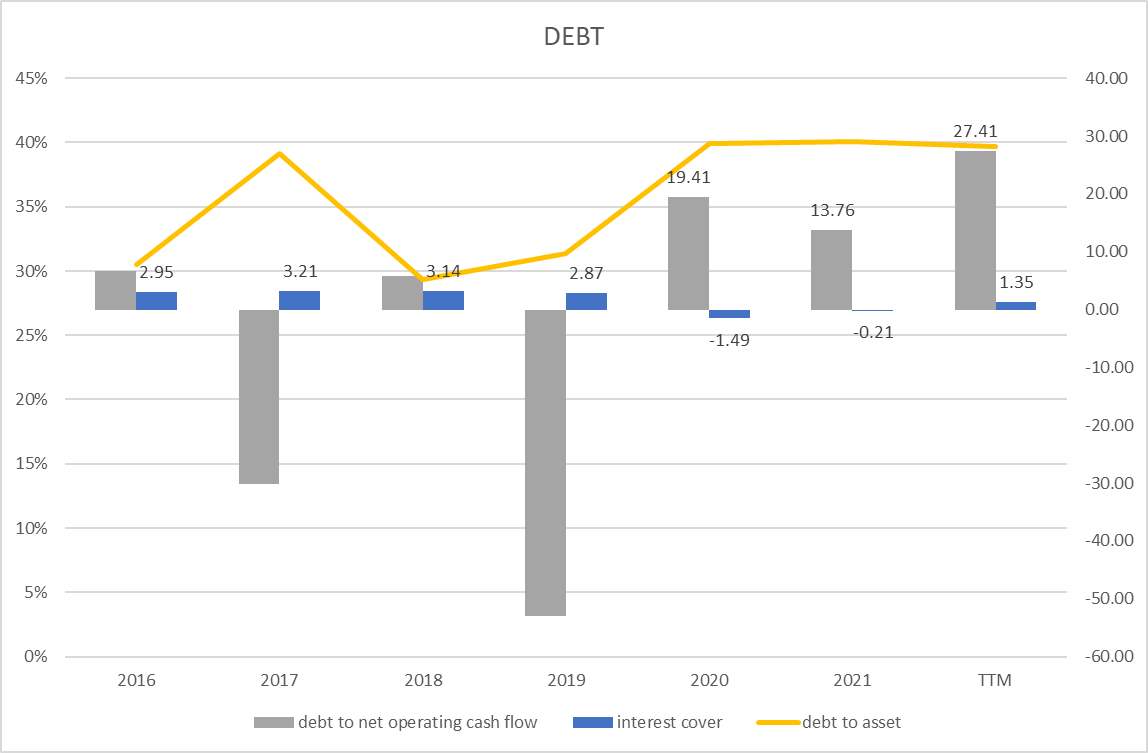

{kind=link}

The debt-to-asset ratio (yellow line) is between 30% (2016) and 40% (2022), and in the last three years, the company was not able to reduce total debt if compared to assets. Anyway, the ratio is about 40% and this underlines that the total debt level is high and represents a critical parameter to allow the company to go through the next periods with the peace of mind of being able to meet the financial commitments to pay the interest on the debt.

The blue bars represent interest cover which is not a measure of debt but a measure of how many times the company's corporate profits can pay interest on the debt. The higher the parameter, the more secure the company can be considered.

In the last 7 years, the company ratio was above 3.0 on only two occasions (in 2017 and 2018). In fact, from the graph, we can see that in the last three years, company profits have not even been able to repay the interest on the debt (parameter negative or close to 1) and this is an element of high risk. Even the figure of 1.35 of the last quarter’s release is low in absolute value and does not represent an element of financial safety.

Corporación América Airports get revenue in Argentina in hard currency from foreign passengers and in pesos for domestic passengers. The company is also waiting for the government for a new date review in 2023 for discussing peso-denominated fees.

The loss of value of the current currency and the high rate of inflation in the country (which could reach three digits) represents a further element of risk. We have seen in the previous paragraphs how, for example, the construction costs, because of the infringement led to heavy erosion of the gross margin in 2019, and this scenario could recur, causing a high risk to company profitability.

Conclusion

After the COVID-19 debacle, the airport services market is going through a period of strong growth and expansion. The pre-pandemic volumes have not yet been fully recovered but the data and the trend indicate that soon we could see the passenger figure reach a new high and exceed the 2019 figure. CAAP represents a consolidated reality with more than 20 years of presence on the market and an interesting investment opportunity in terms of the share price. The risk is very high and is mainly due to the high corporate debt as well as the triple-digit inflationary environment of the Argentine peso. With a strong risk appetite, my rate is Buy.

For further details see:

Corporacion America Airports: Vertical Takeoff With Growing Market Trend