OFC - Corporate Office Properties: An Evolving Property Portfolio And Promising Future Outlook

2023-05-31 01:54:40 ET

Summary

- OFC divested from some of its non-core assets in non-primary markets, most notably selling off seven properties that were considered tangential to its core mission.

- Occupancy rates remained solid at 94.8%, slightly down from 95.3% in Q4 2022, reflecting an excellent ability to maintain high occupancy despite the portfolio transition.

- In my opinion, the current potential rewards out weight the risks.

Corporate Office Properties Trust ( OFC ) has started 2023 strong, restructuring its property portfolio to align with future growth. Despite minor declines in Q4 2022 metrics, the strategic shift resulted in increased Q1 operating income. OFC's management foresees a prosperous 2023, with dividends already increased by 3.6%, offering an attractive target for investors. However, potential political changes in defense budgets and upcoming elections signal a need for investor vigilance.

OFC's Property Portfolio Q1 2023

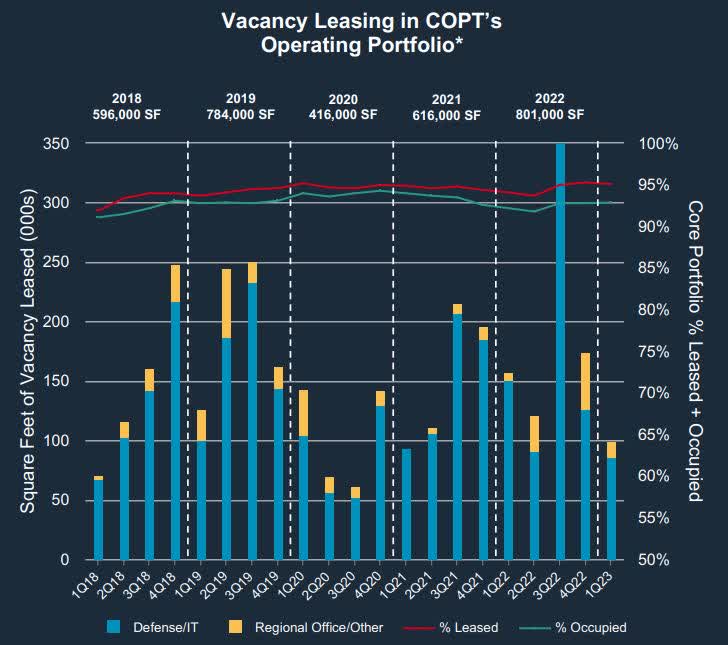

As 2023 unfolds, Corporate Office Properties is proving that it's more than capable of riding the tides of change. Throughout Q1 2023, the company significantly altered its property portfolio to align with market demands and future growth prospects. OFC divested from some of its non-core assets in non-primary markets, most notably selling off seven properties that were considered tangential to its core mission. The money raised from these sales was immediately re-invested into properties located in thriving markets, further strengthening OFC’s presence in regions showing remarkable growth potential . A significant highlight was the acquisition of a premier office complex in Virginia, reinforcing its strong footing in the defense and government-related office spaces. Since 2012 , COPT has significantly focused its capital investments on Defense/IT locations that are integral to high-priority U.S. defense missions.

{kind=link}

Robust Q1 2023 Results and A Progressive Trend From Q4 2022

When comparing the fiscal report from Q1 2023 to Q4 2022, there's a clear testament to the effective strategies being employed by OFC. The company reported a noticeable increase in operating income, underpinned by the divestment of non-core assets and the strategic acquisition of new properties. Even though this transition required considerable financial outlays, it led to a net increase in income. This shows OFC's adeptness at financial management, even in the face of major strategic shifts. Occupancy rates remained solid at 94.8%, slightly down from 95.3% in Q4 2022, reflecting an excellent ability to maintain high occupancy despite the portfolio transition . FFO per share stood at $0.79, a slight decrease from the $0.82 of Q4 2022, primarily due to the transactional costs associated with the portfolio transition. I believe that due to the tenant base the company serves, its long-term stability is virtually guaranteed. Even with back-and-forth party arguments and harsh debt ceiling talks, the defense budget was raised with almost no questions asked as the China-U.S. tensions will very likely increase in the upcoming decades.

Management's Expectations For the Remainder of 2023

OFC's management remains extremely bullish about the company's prospects for the rest of 2023. With the major changes in Q1 behind them, the company expects to leverage its reinvigorated property portfolio to deliver even stronger results. The management anticipates that the shift towards high-growth markets and sectors, particularly defense and government-related properties, will drive increased rental income which I agree with. When a company focuses on its core business it is usually more profitable than doing something that they do not have the proper resources and talents. They also predict that the newly acquired properties will reach full occupancy by the end of the year, further boosting revenue. Along with this, OFC aims to continue its disciplined capital recycling strategy, looking to further divest from any non-core assets and invest in promising opportunities.

OFC's Dividend is Steady

Shareholders can continue to have faith in OFC's dividend policy. Despite the significant changes in its portfolio and slight variations in the financial metrics, the company maintained a steady dividend payout in 2023. OFC has been paying dividends for decades but the management has not increased it for more than 10 years until now. In 2023 they announced a 3.6% dividend increase to $0.285 per share. This decision reflects the company's confidence in its strategic shift and its future profitability. The dividend yield remained competitive, providing a compelling reason for income-focused investors to consider OFC stock as a viable option. Going forward, the company intends to uphold this policy, driven by the belief that its new investments and portfolio adjustments will sustain, if not improve the trust's financial performance. The CFO made the following comments about the company’s new increased dividend in its earnings call:

“The dividend increase illustrates our confidence in strong FFO and AFFO growth. With this increase, we expect our full year AFFO dividend payout ratio will still be roughly 70%.” - Anthony Mifsud - Executive Vice President & CFO

Valuation and Risks

OFC is trading at attractive valuation levels. Its forward price to FFO is down from around 10.7x in Q1 to 9.4x in Q2 2023. It might seem a bit high compared to the office REIT sector but investors should keep in mind that OFC is operating in the defense market. Its price-to-book value further emphasizes the undervalued stock theory. It is trading at 1.45x its book value the lowest level in 10 years. Investors could get a bargain deal with the current valuations in my opinion. OFC’s 5% dividend yield provides an attractive target for office REIT investors looking for safe office portfolios with high occupancy rates.

Investors should be aware of the risks as well. OFC's financial stability is notably resilient to macroeconomic fluctuations, making it an effective safeguard in the face of potential economic downturns. However, political decisions over the defense budget and military spending can heavily affect its portfolio and its bottom line. The upcoming 2024 election might also be a small risk factor and could cause some volatility.

Summary

OFC's Q1 2023 performance marks a period of significant change and progressive transformation. As the year progresses, all eyes will be on how well the company manages to leverage its reshaped portfolio and whether its promising predictions translate into enhanced profitability. In my opinion, the current potential rewards out weight the risks, and the niche market makes the company immune to hybrid work trends that most office REITs could suffer from in the future.

For further details see:

Corporate Office Properties: An Evolving Property Portfolio And Promising Future Outlook