OFC - Corporate Office Properties: Further Room To Rise Following Strong Monthly Gains

2023-08-01 07:47:55 ET

Summary

- Corporate Office Properties is reaching new milestones in its Defense/IT segment.

- This is driven by favorable demand drivers, particularly in the area of cyber defense.

- Of those that lease properties to the U.S. Government, I believe OFC's portfolio faces the least risk relating to non-renewal.

- Though shares have gained over the past month, the stock appears to have more room to run.

Of those that have the benefit of leasing properties to the U.S. Government, I view Corporate Office Properties ( OFC ) as one of the best investment choices for investors seeking exposure. While the company doesn't have as strong of a dividend track record as Postal Realty ( PSTL ), they make up for this with the quality of their portfolio, which is centered around highly specialized defense/IT operations. Compared to both PSTL and another peer, Easterly Properties ( DEA ), OFC's properties are at significantly lower degree of nonrenewal risk. Their Q2 results provide support to this. And at current trading values, I believe the stock has further room to gain, despite the recent run-up.

OFC Q2 Results

Reported Q2 results came in slightly better than expected , driven in part by 8% YOY growth in total lease revenues. The growth resulted from occupancy gains, positive cash rental rate growth, and annual rent bumps.

At period end, the overall core portfolio was 93.6% occupied and 95% leased. This followed total leasing activity of 891K SF, 803K SF of which was attributable to renewals. Retention also held at a strong 89%; 93% for their Defense/IT locations.

In the same-property population, cash net operating income ("NOI") grew 5.8% YOY due to lower-than-expected net operating expenses. This in turn contributed to Q2 funds from operations ("FFO") of $0.60/share or $0.02/share greater than the midpoint of their guidance.

The strength through the first half of the year enabled positive revisions to guidance. The midpoint of same-property cash NOI was increased 100 basis points ("bps"). This follows a 100bps increase in Q1. And the midpoint of full year FFO was revised to $2.40/share, which represents a $0.02/share increase in guidance. The new midpoint also represents a 2% increase over 2022's results.

Key Takeaways From OFC Q2 Results

Milestone Leased Rate In Defense/IT Segment

OFC's Defense/IT segment is clearly benefiting from favorable demand tailwinds. The 2024 budget for the Department of Defense is 3.2% greater than fiscal 2023 and 13.4% greater than fiscal 2022. Despite gridlock elsewhere, support for defense remains largely bipartisan. In recent periods, too, there has been growing recognition of the threats posed from a cyber standpoint. This has led to increased cyber-related investments.

The Defense/IT portfolio is leased accordingly. At June 30, the segment was 96.8% leased. This is 190bps improved from last year. It also represents the highest leased rate since OFC began separately disclosing the metric in 2015.

OFC Q2FY23 Investor Supplement - Occupancy Summary Of Core Portfolio

And looking at their three largest defense locations, representing approximately 45% of annualized revenues and consisting of the National Business Park, Redstone Gateway, and The Lackland Air Force Base, the aggregate leased rate at these three properties was 98.8% at period end. It should also be noted that about half of their annualized revenues were generated from properties that were 99.3% leased.

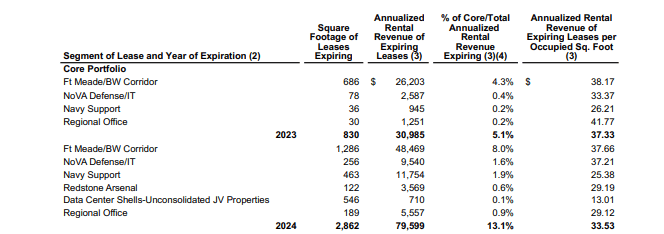

High Confidence In Renewing Upcoming Expirations

OFC does have 7.1 MSF of leases expiring over the next ten quarters. While some may see that as a risk, retention rates have been high. And I expect retention to remain high. Since the properties are highly specialized for mission-critical work, tenants have limited options at the time of renewal. They could certainly opt to build-to-suit, but that has proven cost prohibitive in the past. This is unlikely to change, in my view.

OFC Q2FY23 Investor Supplement - Partial Summary Of Lease Expiration Schedule

{kind=link}

CEO, Steve Budorick, mentioned that of the total set to expire, about 4.0 MSF was attributable to large leases, which is defined as those over 50K SF. On these leases, they are expecting a retention rate of 95%, with 100% renewal expected for the large leases set to expire over the balance of 2023.

Positive Progress In Active Developments

OFC currently has active developments totaling 1.5 MSF. These are across nine projects with a total estimated cost of +$480M. At present, they are 92% leased. But looking ahead to the remainder of the year, OFC expects to place over 50% of the square footage into service with a leased rate of 99% upon delivery.

The successful lease-up of these projects gives confidence that they will continue to have success in their future pipeline, which currently stands at 1.0 MSF, up from 700K SF last quarter. Furthermore, OFC is also assessing another 1.2 MSF of potential future opportunities. This should provide the company with a strong runway for future growth.

Is OFC Stock A Buy, Sell, Or Hold?

Shares in Corporate Office Properties have outperformed the broader S&P ( SPY ) by about 450bps since my prior update following Q1 results. The stock, however, still trades approximately 7% below my target price of $28/share. Consensus Wall Street targets are even higher at $28.70/share.

I believe the stock can capture the target pricing. Since Q1, the company has expanded the leased rate in their Defense/IT segment, the primary driver of NOI, to a new milestone. Bipartisan support for continued defense funding should ensure tenant resiliency. Emerging threats in cybersecurity should be especially favorable to their IT-focused properties.

At the new midpoint of full-year FFO expectations, the stock trades at a forward multiple of just 10.8x. Related peers who also have exposure to the U.S. Government, Easterly Properties and Postal Realty Trust, trade at 12.9x and 17.4x, respectively. I continue to believe OFC is overly discounted, especially to Easterly, given their portfolio metrics.

Following a rise of 7.8% this past month, I believe shares can rise further to $28/share. I, therefore, maintain OFC as a "buy."

For further details see:

Corporate Office Properties: Further Room To Rise Following Strong Monthly Gains