CRSXF - Corsa Coal: Pennsylvanian Coal Miner Set To Benefit From 2023 Contracts

2023-04-20 02:25:03 ET

Summary

- For the past two years, Corsa Coal has not been a profitable way to get exposure to the recovery in met coal.

- Corsa has disclosed a strong contract base for 2023, suggesting a light at the end of the tunnel.

- If Corsa can execute their 2023 contracts, free cash flow could exceed both their market capitalization and net debt amounts.

Corsa Coal ( OTCQX:CRSXF ) ( CSO:CA ) is located in my family's stomping grounds of Somerset County, PA and presents a fascinating investment opportunity in the Metallurgical Coal space. Corsa offers several of my favorite features in an investment - forced/indiscriminate selling, underfollowed, recent legal overhang removed, and approaching an earnings inflection point. As usual, these opportunities come with plenty of risk - let's dig in.

Note - all amounts in USD corresponding to company financials on SEDAR

History

Corsa has a storied history, despite its small size. Part of the business was previously known as PBS Coals, which was bought by a Russian steel company (OAO Severstal) in 2008 for $177m, and later sold to Corsa in 2015 for $60m cash and $60m assumed liabilities. Corsa merged PBS with their Wilson Creek Energy business to form the current Corsa Coal Corporation. PBS owned the land surrounding the site of the Flight 93 crash and memorial, and joined CONSOL Energy ( CEIX ) in the donation of lands and later sale of additional tracts for the memorial grounds.

Corsa returned to the news in 2017 with the launch of the new Acosta mine , heralding that "the war on coal was over." Met coal prices subsequently dropped from mid-2018 through the beginning of Covid, and the situation became dire at Corsa. The business took a Main Street Loan from the government and has benefited from the sharp recovery in Met prices, though FY22 contracts were hedged significantly below market pricing.

So why has the share price cratered while many Met producers are trading near highs? To start, look at the ownership chart in a prior Corsa presentation:

Former Corsa Ownership (Corsa 2022 Investor Presentation)

This aged poorly, as Sev.en started selling shares in Jun-21 and fell below 10% ownership in Jan-22. Quintana distributed their shares to limited partners in Dec-21. The combination of these two events means half the ownership of Corsa hit the open market last year. Meanwhile, Lukas Lundin stepped down as the Chairman of his own Lundin Mining Corporation and Lucara , due to a battle with cancer, and has sadly passed away . These drastic changes happened quickly, impacting key shareholders who used to own most of the company. The news was alarming enough for Corsa management to implement a rights plan .

The selling began to make sense as FY22 unfolded and Corsa became a company adrift. Coal production was contracted under $160/ton, well below market prices, and shares flooded the market.

FY23 Outlook

With the bleak past behind, let's consider the future. Per the Q4 press release :

Corsa committed over 900,000 tons at an FOB mine price of nearly $179/ton for the calendar year 2023. The price per ton is the equivalent of $287/mt FOBT for Australian premium low volatile metallurgical coal. The volumes and price/ton were impacted by nearly 153,000 carryover tons from 2022, which were priced at the 2022 fixed price contract rate.

Given FY22 tons have been selling at ~$160, it appears Corsa contracted actual FY23 tons around [(153k*160 + 747k*X)/900k = 179] which equates to [X = $183/ton] FOB, within $10 of larger peers, a much better outcome than their FY22 contracting season.

I expect Corsa can produce about 1m tons in FY23 given their stated Q1 production of 240k. Increased production will lead to better fixed cost coverage, while labor and rail issues have also eased. Therefore, I'm assuming $120/ton cost for FY23. Corporate cash expense should be $10m, including the minimal interest on their Main Street loan.

All in, I expect Corsa sells the non-contracted tons around $180 FOB, getting $60m of gross cash flow, less $10m corporate and $5m CapEx. The resulting $45m of FCF would be enough to pay off their outstanding debt and deal with some of the water and environmental liabilities, maybe even releasing some of their $41m of restricted cash .

{kind=link}

Valuation

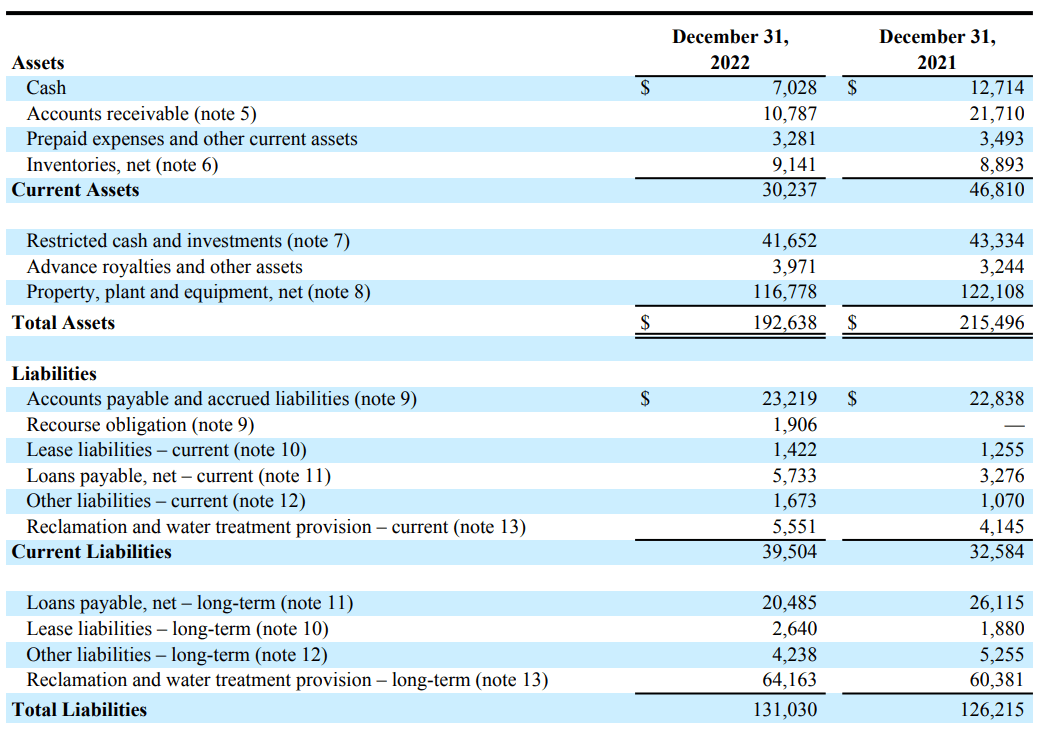

So, what is Corsa worth? Through Q4-22, Corsa has a $19m net debt position, not inclusive of outstanding site reclamation liabilities which are secured by restricted cash. Per my estimates above, Corsa could pay off their debt in FY23 via FCF and address reclamation, but if there are further operational headwinds, the business will continue to languish.

Corsa is NOT a low-cost producer and has historically shown lower margins than peers like Arch Resources ( ARCH ), Ramaco Resources ( METC ), Warrior Met Coal ( HCC ) and Alpha Metallurgical ( AMR ). The main advantage for each of these peers is their scale. AMR can produce around 15m tons and Arch 10m, versus the mere 1m tons for Corsa. Corsa's mines are not longwall mines (a lower-cost way to mine underground coal), impacting the company's cost efficiency.

If Corsa's long-term EBITDA power is around $10m, a 5x multiple might be the ceiling, suggesting a $50m USD market cap might be appropriate (~$0.50/share, 100% upside). They have some growth options that could expand their earnings power, but I would be nervous investing in a sub-scale operator for growth. Instead, I'd be a proponent of addressing liabilities with 2023 cash flow and returning future cash to shareholders via dividends and buybacks. If normalized EBITDA settles at $10M/year and 50% is returned to shareholders ($5M/year), it would provide a ~20% long-term yield from today's price, with the possibility of continued Met coal strength and the equity being de-risked if $45m FCF in 2023 becomes reality.

The torque for Corsa will become apparent if they execute in 2023. $45m of FCF would be enough to pay off all debt and cover the current equity value. The reclamation and water obligations could be addressed later, as these include 20+ year tail liabilities.

Risks

Corsa alleviated one major overhang stemming from an FCPA bribery case against two former employees . Corsa brought the case to law enforcement upon discovery, which appears to have led to the DOJ to decline prosecuting the company and settling for a $1.2m fine . This case could have been a death blow to Corsa but the overhang is gone.

Corsa presents other generic commodity producer risks: exposure to volatile prices, increasing raw material costs, and possible recessionary headwinds. Their lack of scale exacerbates these risks. Corsa trades over the counter in the US and fairly thinly on the TSX Venture Exchange, subjecting shareholders to significant volatility and illiquidity.

A Corsa employee passed away at their Acosta mine in October. Initial reports suggest the fatality was not mining-related, but if the employee's death was due to Corsa's negligence there may be further legal exposure. This was not addressed in Corsa's Q4 MD&A.

I am assuming Corsa executes well this year and fulfills their contracts at lower costs of production. If they fail to execute due to persistent production headwinds, they may not generate meaningful cash flow in 2023.

Conclusion

Corsa remains one of the few metallurgical coal producers that has not seen substantial appreciation in their share price - quite the opposite. Buoyed by 2023 contracted volumes, Corsa has provided a clear path to freeing themselves of the capital crunch they experienced the last few years. I've acquired shares expecting the stock to re-rate after earnings prove stable. I remain optimistic profitability will return to the confines of Somerset County.

For further details see:

Corsa Coal: Pennsylvanian Coal Miner Set To Benefit From 2023 Contracts