FMC - Corteva: Better Inventory Management For Better Profits

2023-11-30 00:03:59 ET

Summary

- Corteva's Pioneer Agency Model allows for better inventory management and has helped the company outperform competitors like FMC Corporation.

- Corteva's financial data shows effective inventory management and higher growth prospects compared to FMC.

- Corteva's market valuation underestimates the strength of its distribution model, making it an attractive investment opportunity.

Investment Thesis

Since the outbreak of the war in Ukraine in February 2022, agricultural supply chains have been out of sync. While this created a boon for more agricultural companies at the start of the war, many are now feeling the overhang of mismatched inventory levels and elevated costs.

While Corteva ( CTVA ) has not been immune to the ups and downs of the industry over the last 2 years, their Pioneer Agency Model distribution channel allows unprecedented foresight into farmers’ future product demand trends allowing Corteva to better manage inventory, alleviating some inventory imbalances seen throughout agricultural companies. This has allowed the firm to maintain a more efficient inventory and outperform competitors like FMC Corporation (FMC). In my opinion, as supply chains normalize, Corteva will be able to continue to excel. The stock is a buy.

Company Overview

Products & Geography

Corteva Agriscience ((CTVA)) innovates and provides agricultural products in the form of crop/seed species, crop protection innovations, and digital solutions. Pioneer Hi-Bred International, Inc. (different from their Pioneer agency model) is a subsidiary of Corteva, specializing in crop genetics and biotechnology innovation. They offer genetically modified crop species and herbicide and insecticide solutions, with their largest revenue fractions consolidated on soybean and corn.

Corteva’s revenue breakdown YTD includes crop protection solutions segmenting at 42% and seeds at 58% ( 2023 Q3 Earnings presentation ). Geographically, the United States is the largest revenue consolidation at 43.3% of sales, with Brazil following at 18% (FactSet). Management's outlook is also optimistic, claiming FY24 to see sizable growth in soybean seed demand as the US market backdrop slowly shifts from corn.

Corteva’s Distribution Model

Corteva’s Pioneer Agency Models allow for high-touch, personalized insight into consumer (farmer) demand needs and trends. These Pioneer stations are smaller distribution centers, placed near farm fields. Through independent, local dealers, Corteva can sell products while leveraging grassroots relationships and personalized, locality-based insights for various geographies. These independent local dealers are nestled in farming communities worldwide.

This contrasts traditional agriculture distribution methods of designating product sales sites located in municipalities to service various surrounding regional communities, who are less able to provide deep insight into local needs and capable of fostering relationships within tight-knit, ultra-interdependent farming communities.

As supply chains have become more saturated with grain and farming supplies as the war in Ukraine has gone on, this has become key. Effective supply chains are the key to more stable profits in this space.

One of Corteva’s competitors exhibiting a more traditional distribution channel, FMC Corporation, (FMC), has been suffering due to a more inefficient supply chain and worse inventory management.

Deep Dive: Financial & Product Inventory Position

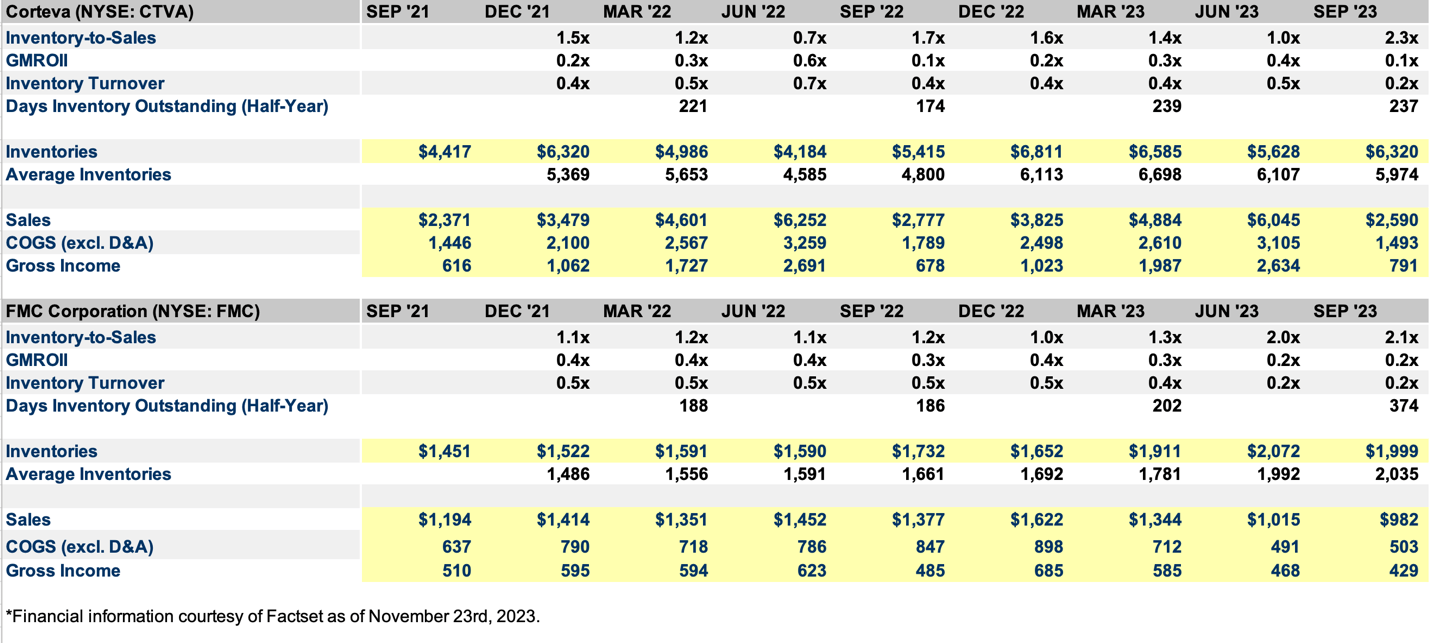

To help better understand why this Pioneer supply chain makes a key difference, below is some data from FactSet covering inventory for Corteva vs. FMC Corporation ((FMC)).

CTVA vs. FMC Inventory Analysis (FactSet)

{kind=link}

To get a better Corteva’s finances, the last 8 quarters of inventory and sales data were analyzed to account for and mitigate seasonality in the agriculture industry as well as non-recurring global macroeconomic phenomena. These included CTVA’s aggregate balance sheets and CTVA’s aggregate income statements. We’ll go over the key terms here as well to help analyze the implications for each. This will help us better understand why their inventory system is key.

Inventory-to-Sales (I/S)

I/S ratio measures the value of a company’s inventory to its sales. Generally, for Corteva, as the growing seasons progress (northern hemisphere), I/S decreases throughout the successive quarters signaling sales exceeding production. During the typical Q2 CTVA has a ratio historically lower than FMC, before replenishing inventory (inventory jumps) in Q3 for the growing cycles of the southern hemisphere and the global cycle continues. As Corteva’s I/S decreases from Q3 to the following year’s Q2, their sales also increase at a significant rate inverse to I/S. This signals effective inventory management as sales grow at a rate faster than replenishing stock.

Compared with FMC, for their last 8 quarters, decreasing I/S trends are scarce. However, in the case of increasing I/S, FMC experienced the longest stint of growth from Q4 22 to Q3 23 from 1.0x to 2.1x, as sales decreased and management did not manage inventory as efficiently.

Going into the winter of 2022, FMC appears to have overstocked inventory. When demand from Europe waned this year, FMC experienced immense channel destocking as their sales distribution model could not provide adequate insight into changing farmer demand trends with 2023’s Europe backdrop shift. Corteva’s ability to manage I/S with their Pioneer Agency Model reigns vital in the current climate of shifting global trends.

Gross Margin Return on Invested Inventory ((GMROII))

GMROII measures how effectively a company’s inventory is generating gross profit. GMROII increase trends also match with Corteva's sales cycle from Q3 to FYQ2, as seen from 22Q3 to 23Q2 and the latter 3 quarters of 2021-22 from 21Q4 to 22Q2. These direct trend relationships indicate effective inventory management to meet sales demand. Meanwhile, FMC’s GMROII had stints of consistency despite shifts in sales. But FMC is mostly faced with decreasing GMROII alongside decreasing sales, signaling decreasing sales volume and inaccurate demand forecasting.

For Corteva, their more accurate demand forecasts carry them into the forward years as crop prices saw a slowdown in 2023, with Corteva, FMC, and other ag companies like John Deere projecting a slowdown in demand for growing complement products like machines and chemicals.

Inventory Turnover: Inventory turnover measures the rate at which a company sells and replenishes its inventory within a certain period. Corteva’s is cyclical, while FMC’s was consistent but has been experiencing decline within the past few quarters.

Days Inventory Outstanding ((DIO))

As lower global seed volumes have hurt Corteva’s farm revenues, DIO is considered to analyze inventory turnover, mitigate yearly seasonality, and ensure a more transparent weighting. In Q3 2023 DIO increased significantly for FMC, while DIO saw a small decrease for Corteva, on par with historical seasonality changes. Channel destocking has hurt FMC at a higher level that has not impacted Corteva’s as much.

Valuation

Corteva’s high-touch, personalized product distribution models through independent sales representatives (through the Pioneer Model) allow them to manage their inventory to a higher degree compared to competitor FMC or even John Deere, who’s been experiencing a slowdown of tractor sales as farmers suffer from declining crop prices.

Both FMC and Corteva’s share price has been decreasing significantly over the last 12 months, facing diminished volumes from product destocking. CTVA’s share price has dropped from a high of $67.55 on December 2nd, 2022 to $45.57 as of November 29th 2023, a 32.5% decrease. FMC’s share price plummeted from $134.38 to $52.88 the same period, a 60.6% drop.

FMC’s FWD EV/EBITDA sits at 10.54x while Corteva’s is at 10.90x . This sits close to farming and agricultural company EV/EBITDA benchmarks that typically range from 9.48x to 10.55x. However, Corteva’s slightly higher forward EBITDA metric implies higher growth prospects than FMC given their better inventory management.

In my opinion, CTVA should see a significantly higher EV/EBITDA forward multiple than FMC or the industry. Their EPS 3-5 year forward CAGR stands at 15.43% , almost 50% higher than the industry average of 8.27% and over 20% higher than the growth rate at FMC of 12% .

Given this, I believe that Corteva should have an EV/EBITDA multiple between 20-50% higher than industry averages. This should allow shareholders to benefit from a 20-50% upside in share price from here if the market appreciates their more nimble business model as well, and management’s optimism about 2024 comes to fruition.

Risks

Some members of the farming community have expressed concerns regarding Corteva's management of the Pioneer Agency Model, specifically about the company's shift from local seed dealers to larger, designated sales sites. This change has led to dissatisfaction among some farmers who feel that long-standing relationships with local dealers are being undermined by Corteva. However, in a lot of cases, farmers are stuck with Corteva as one of their suppliers given that this market is largely an oligopoly .

In Brazil, agriculture has been influenced by the fallout from the Ukraine-Russia war, which has disrupted European supply chains and led to decreased demand for Brazilian products. This created a jump in the prices of commodities like soybean oils, and farmers here could be seen as winners as a result of the conflict . Brazil’s farmers are planning to adjust their purchasing behaviors in the upcoming year. With this, Corteva's independent sales representatives (through Pioneer) are positioned to effectively monitor and respond to these shifts in demand trends, potentially more accurately than their competitors. Management is optimistic about next year.

Conclusion

Corteva stands out in the agricultural sector as a solid investment choice, primarily due to its innovative Pioneer Agency Model. This distribution strategy has helped partially shield the company from the inventory imbalances plaguing many competitors, demonstrating exceptional foresight and operational efficiency. This has helped Corteva maintain a competitive edge over rivals like FMC Corporation. This resilience can be a launch pad, allowing the company to be more nimble going forward and more competitive in the ever-changing agriculture market.

In my opinion, Corteva's market valuation seems to underestimate its intrinsic strength of this model, presenting an attractive entry point for investors. While, with any thesis, there are risks, Corteva's track record of effective management and adaptability offers a reassuring outlook. I think the stock is a buy.

For further details see:

Corteva: Better Inventory Management For Better Profits