CRVS - Corvus Pharmaceuticals: Targeting $1 Billion/Year U.S. T-Cell Lymphoma Market

2023-05-12 16:25:30 ET

Summary

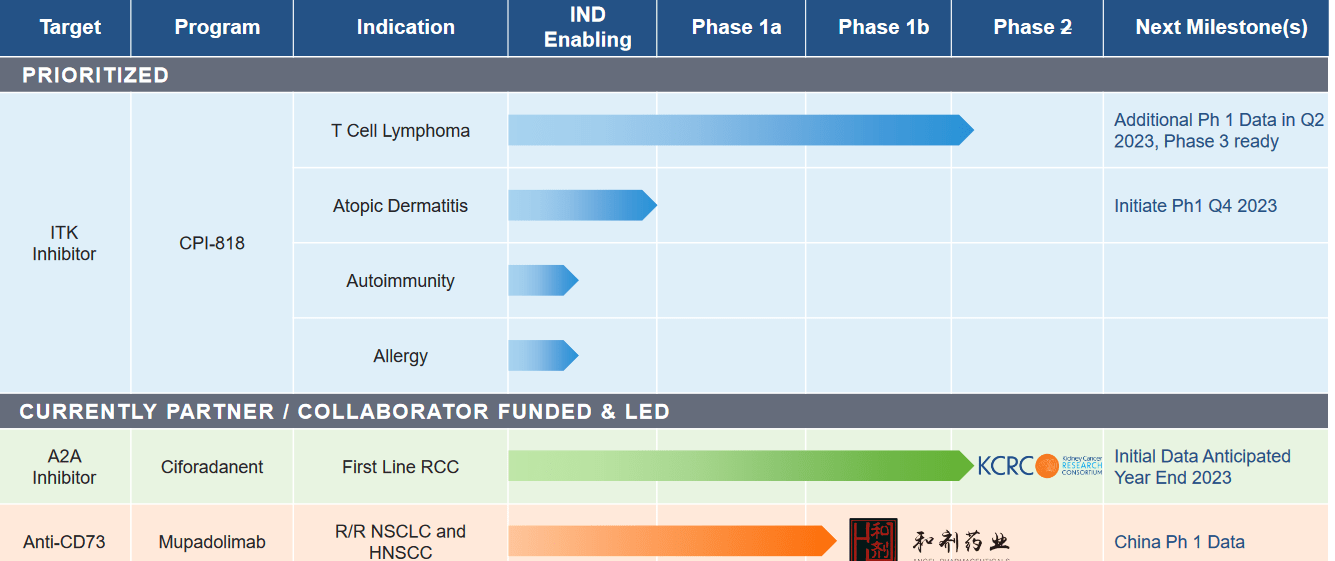

- Additional Phase 1b data for CPI-818 in T cell lymphoma is expected in this quarter.

- Phase 2 data for Ciforadenant is expected this year.

- The stock's upside momentum is expected to continue over the next 1 year due to above catalysts.

Corvus Pharmaceuticals ( CRVS ) is a clinical-stage biotech company, which was founded in 2014 and is based in Burlingame, California. The company is focused on ITK inhibition as a novel approach to cancer immunotherapy.

CPI-818 in T cell lymphoma

The company's flagship molecule CPI-818 causes ITK inhibition, which is comparable to the blockbuster drug ibrutinib. This product candidate is being developed in multiple indications like T cell lymphoma or TCL, atopic dermatitis, and autoimmune and allergic disorders.

The ITK Pathway is involved in multiple diseases. ITK inhibition causes an increase in Th1 and a reduction in Th2 cells. This causes an anti-cancer effect and also causes reduced immunity in autoimmune diseases. By causing T cell inhibition through the ITK pathway, CPI-818 causes an anti-cancer effect similar to ibrutinib, which had more than $2.5 billion in global annual sales.

The problem

The lead indication for CPI-818 is T-cell lymphoma, TCL which has a very poor prognosis. The median overall survival rate after the first relapse or progression of this cancer is only 6.5 months. FDA approved agents have shown an objective response rate, ORR of less than 30% and progression-free survival, PFS of about three months. Even with an allogeneic stem cell transplant, the three-year progression-free survival is only 30%.

The potential solution

In preclinical studies, CPI-818 inhibited tumor growth and increased CD8+ T cell infiltration. it also showed anti-cancer effects in a phase 1B trial in PTCL. In the study, absolute lymphocyte count, ALC was found as a prognostic marker. The ORR in patients with ALC >=900 was about 55% and median PFS was 19.9 months. A patient with a highly refractory disease showed partial response for up to 13+ months. Another patient with highly refractory disease had a complete response lasting 25 months. The clinical efficacy is terms of PFS (19.9 months) was much higher than just 3 months shown with the currently approved agents.

The company is enrolling additional patients in the phase 1b trial in patients with PTCL and three or fewer prior therapies and ALC biomarker count of more than 900. The primary endpoint of this trial is ORR. Data is expected in Q2 this year. The company is meeting with the FDA to discuss a pivotal phase 3 trial comparing the drug monotherapy with the standard of care. The primary endpoint of this Phase 3 trial will be PFS.

Additional products in the pipeline

The second molecule in the pipeline is Ciforadenant, an A2A inhibitor, which being developed in a phase 2 trial in frontline renal cell cancer. Data is expected this year.

{kind=link}

Investor presentation

Manage ment

The company is CEO Richard Miller who was the co-founder and CEO of Pharmacyclics, where he led the initial discovery and development of the blockbuster drug ibrutinib.

Financials and valuation

Cash reserves are expected as $24 million and are enough till the upcoming Q2 data. The operating cash burn rate was approx. $29M in Q1 2023. There is no long-term debt. The company is expected to raise cash after the Q2 data release in TCL.

T-cell lymphoma is 15% of all non-Hodgkin lymphomas in the US. The annual death rate due to this cancer is about 7000 patients in the US, which is the target market for CPI-818 since it represents highly refractory cancer. At an annual cost of $150,000/year, this represents a $1 billion US revenue opportunity. Biotech companies have an EV/peak sales ratio of 7. The current enterprise value of the company is negative because the investors are ignoring the pipeline. Even at just 20% market share, and using EV/peak sales of 7, and discounting at 15% cost of capital, the company's enterprise value is worth $457M.

The stock is held by prominent institutional investors like Orbimed advisers, BVF, and Millennium management. The average analyst price target is $3.83 or 113% upside from Seeking Alpha.

My timeframe for the investment is at least one year till the above two data releases. This is also a good long-term investment considering the large TCL market. FDA is expected to provide guidance on the pivotal Phase 3 study in TCL in Q3 and the data could be expected by 2025.

__________

Risks in the investment include underwhelming data from the ongoing trials, side effects, etc. The company has low capital reserves and is expected to raise cash after the Q2 data release. This may cause a dip in the stock price. The stock has a low daily average volume and can be very volatile. Investing in biotech/pharma/medical devices stocks is risky and may not be suitable for all investors. This note represents my own opinion and is not professional investment advice.

For further details see:

Corvus Pharmaceuticals: Targeting $1 Billion/Year U.S. T-Cell Lymphoma Market