GASS - Cosan: Undervalued And Potential Upside In The Near Term

2023-07-14 14:41:40 ET

Summary

- Cosan presents a strong buying opportunity due to attractive valuation multiples, potential macroeconomic tailwinds, and an upside potential according to Wall Street analysts.

- Cosan is undervalued compared to peers, trading at low EV/Sales and Price/Sales ratios, indicating potential growth.

- Potential risks include commodity cycles and high indebtedness, but the company's diversification and cash flows mitigate these risks.

Investment thesis

Cosan ( CSAN ) is showing a strong buy opportunity due to its attractive valuation multiples, potential macroeconomic tailwinds, plans for subsidiary listings, and the ability to reduce its debt level. Despite some risks associated with commodity cycles and high indebtedness , the company's business diversification and steady cash flows from one of its subsidiaries provide a solid foundation for managing leverage.

Cosan is currently trading at remarkably low EV/Sales ((FWD)) and Price/Sales ((FWD)) ratios, indicating a potential undervaluation relative to its peers. These low multiples, coupled with the market forecasting robust growth in the medium term and the expected cut in interest rates, surely offer a great moment for acquiring Cosan shares.

Seeking Alpha

Getting to know Cosan and its potential

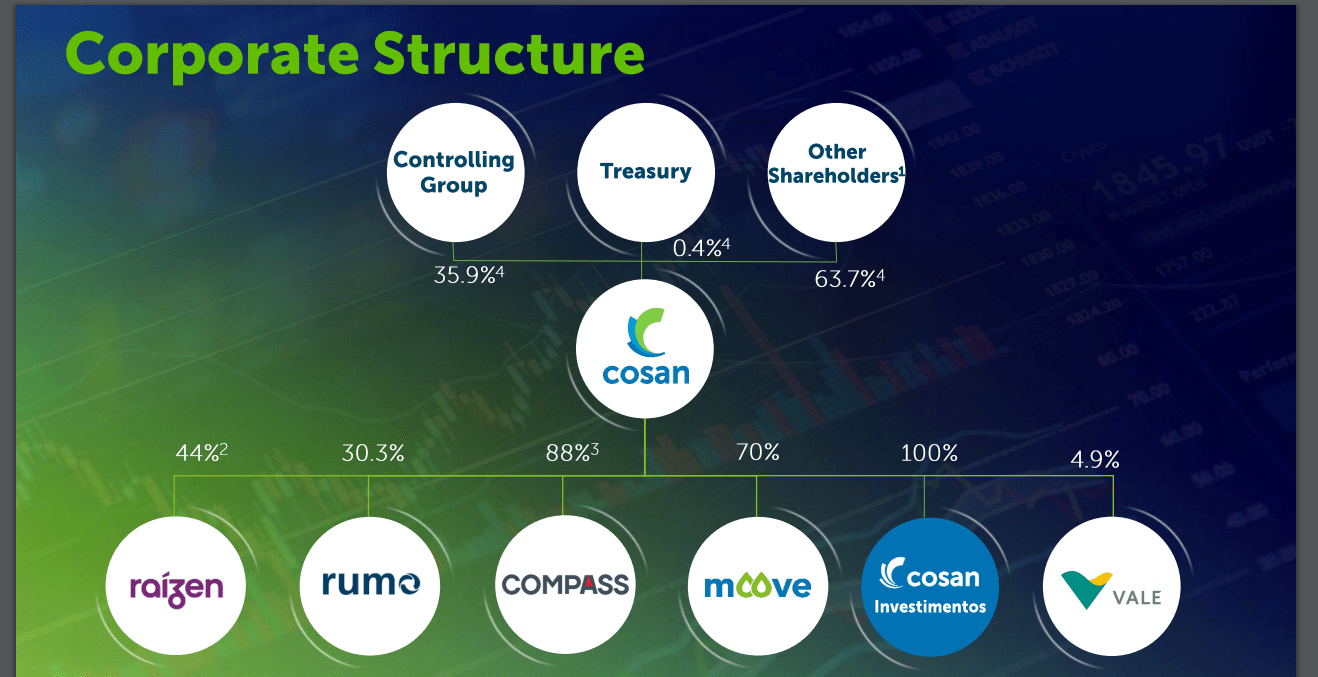

Cosan S.A. is a Brazilian holding company that controls businesses related to Brazil's agribusiness, such as ethanol, fuel distribution, natural gas, lubricants, and logistics. It holds approximately 6.5% of the shares and options of Vale S.A. ( VALE ), an investment company operating in the mining sector. Currently, the holding's portfolio consists of five major companies: Raízen, Moove, Compass, Rumo ( RUMOF ), and Vale.

With over 80 years of history, the company has diversified its portfolio over time. After its Initial Public Offering in 2005, raising US$ 400 million at the time, the company began investing in new businesses. Controlled by the Ometto family, which owns 36% of the organization's shares, its business started in the sugar and alcohol sector.

{kind=link}

Cosan's corporate structure (Investor Relations)

-

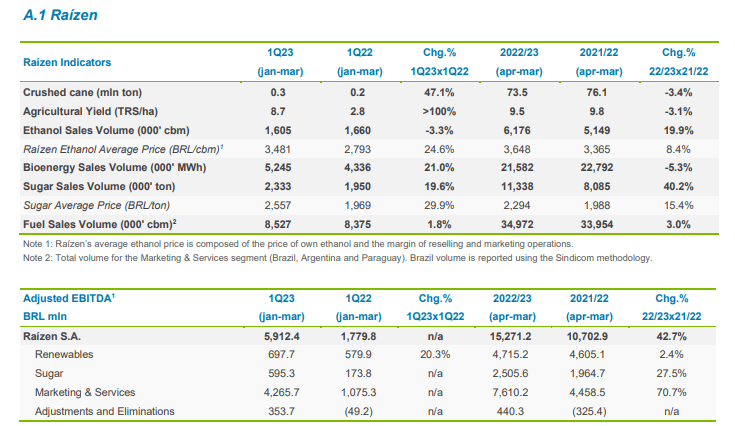

Raízen

Many years later, in partnership with Shell ( SHEL ) in 2011, the companies combined their businesses, creating Raízen (Root + Energy). After the merger, the company operates in the production of sugar and sugarcane ethanol and also operates in the fuel distribution segment under the Shell brand.

Cosan is a giant in the sugarcane market and has recently expanded its leadership through the acquisition of companies. For example, the purchase of Biosev in 2021 increased Raízen's number of mills from 26 to 35, raising its sugarcane grinding capacity by 40% and its annual production to 105 million tons. The company is jointly owned by Cosan and Shell, each holding 44% of the total shares of Raízen.

The synergy created by its controllers provides Raízen with a business model that encompasses different products derived from sugarcane, leading in their respective markets, including ethanol, biomass, and sugar. Its business line is divided into three segments: Renewables, Sugar, and Marketing & Services. The renewable products line has significant growth potential, as debates on decarbonization and greenhouse gas emissions become increasingly frequent, leading the world to seek renewable energy sources.

The company is expected to benefit from the global energy transition and has an ESG aspect. It has expansion projects for its second-generation ethanol, known as E26. In the last year, its revenue was R$ 244 billion, and the operating cash flow (EBITDA) amounted to R$ 5.5 billion in the same period. Thus, Raízen is the largest operation controlled by Cosan.

{kind=link}

Breakdown of Raízen indicators (Investor Relations)

-

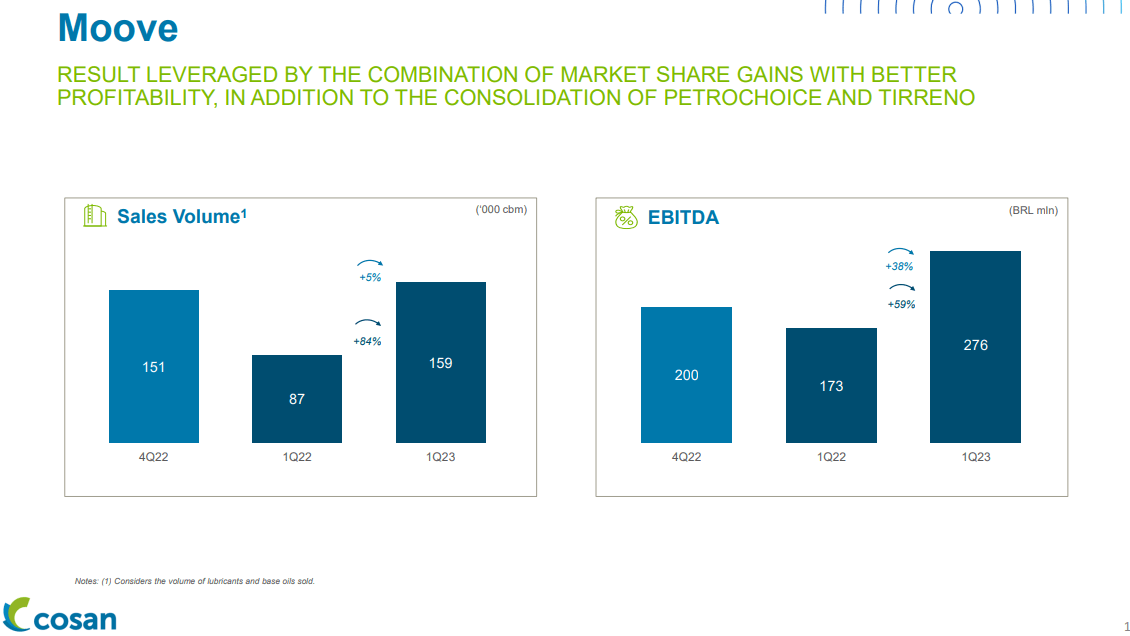

Moove

Moove is the company responsible for Cosan's lubricant line in partnership with Mobil. It operates in Brazil, Europe, and the United States, and its current operations generate lower revenue and results compared to other operations of the company. However, it contributed R$ 850 million to Cosan's EBITDA in 2022, a 41% growth compared to 2021. Cosan holds 70% of the equity rights of the lubricant company, and this business is closely linked to Raízen's operations in Brazil.

{kind=link}

Moove's highlights (Investor Relations)

-

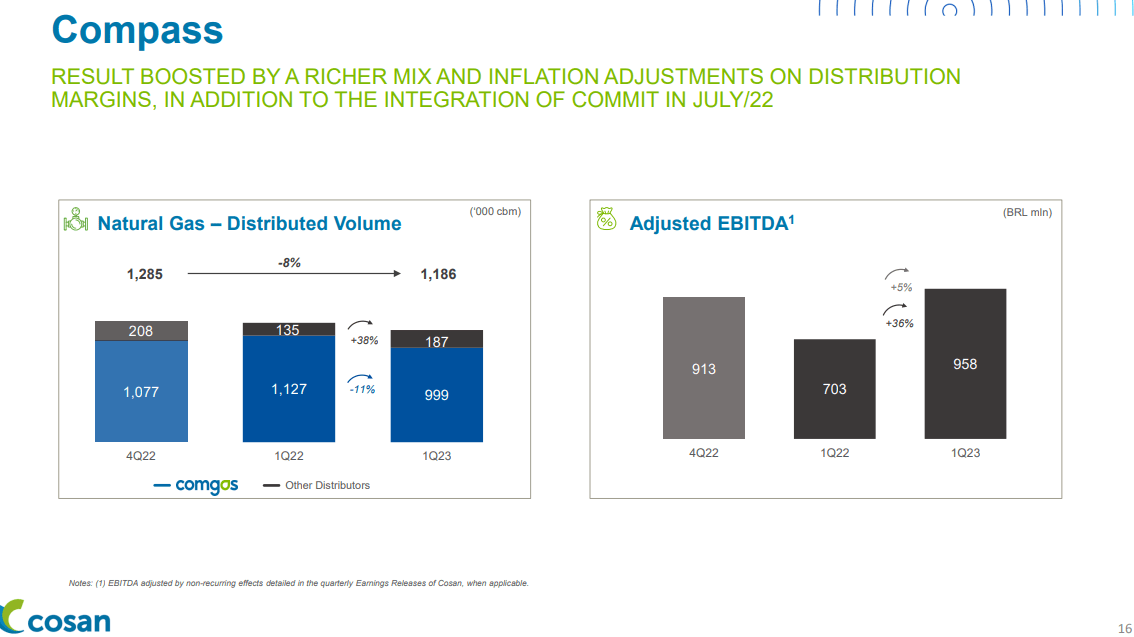

Compass

Compass is the company in the gas segment that controls Comgás, a company that operates natural gas in the state of São Paulo. In addition to this operation, the organization has been investing in distribution, commercialization, and thermal generation, aiming for expansion within the sector.

Cosan owns 88% of the total shares and, therefore, controls Compass. In 2022, the company's net revenue was R$ 20 billion, a growth of 63% compared to the same period of the previous year. The net profit for the analyzed period was R$ 1.8 billion, compared to R$ 1.4 billion in the previous year, representing a 22% increase. Since Compass's business is quite predictable and has a high return on equity, the company is a good dividend payer, greatly contributing to Cosan’s cash generation.

{kind=link}

Compass' highlights (Investor Relations)

-

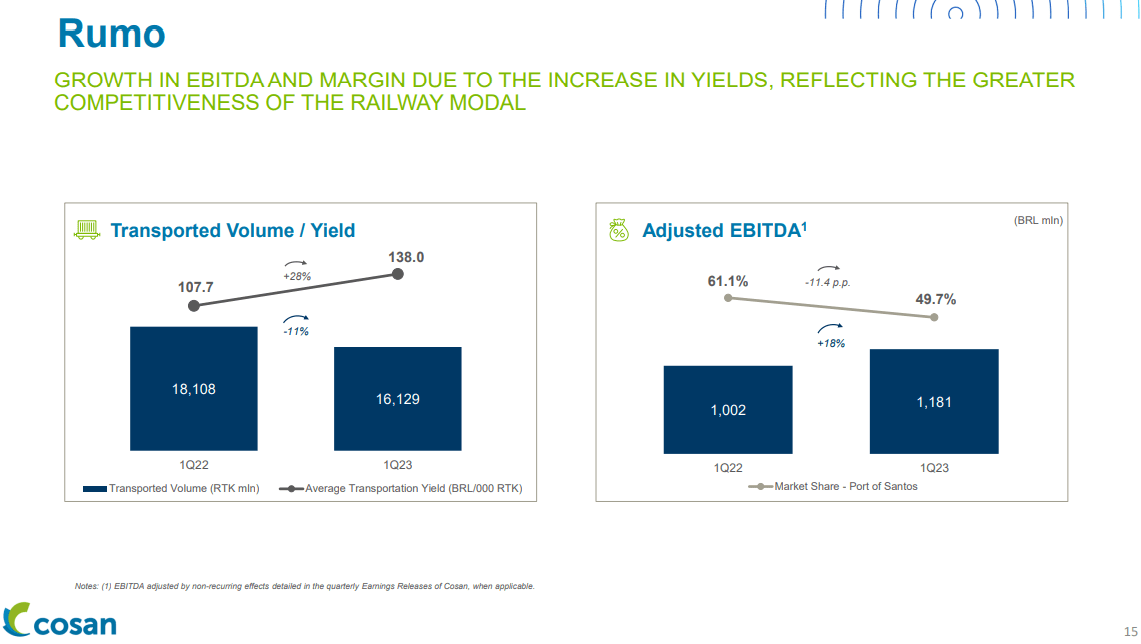

Rumo

Rumo is the railway transportation company of the Cosan group, which originated from the former ALL - América Latina Logística. The company, led by Rubens Ometto, acquired control of it in 2016, making it the largest railway operator in Brazil in terms of rail line extension. The organization provides services in road transport logistics, port handling, and storage.

The company's main clients are agricultural commodities companies, making it directly exposed to the expansion of Brazilian agribusiness. Currently, the company is responsible for transporting approximately 30% of grain exports in the country.

Rumo is controlled by Cosan, which holds 30% of the shares. In the last twelve months, the net revenue was R$ 9.8 billion, representing a 32% growth compared to 2021. This reflects primarily the increased volume of transported products, with industrial goods and containers making the greatest contributions. The net profit for the period was R$ 540 million, compared to R$ 156 million in 2021, representing a growth of over 100%. This increase in net profit reflects the improvement in the company's margins.

{kind=link}

Rumo's highlights (Investor Relations)

-

Vale

Vale is one of the largest mining companies in the world and currently produces 315 million tons of iron ore. It is worth noting that the company's product is of high purity, generating an additional premium over the price of its main product. The main destination for Vale's products is China, which is still in a reopening phase and uses the ore in both the construction industry and the industrial sector. Thus, exposure to Vale leaves Cosan exposed to the growth of the Asian giant.

Another interesting factor that comes with the Vale investment is the dividend payments, which are expected to assist Cosan in its deleveraging. Unlike the other companies, Vale is not controlled by Cosan. With a 6.5% stake, the mining company falls under financial investments in the holding's balance sheet. This position was acquired at the end of 2021, and the market is still digesting how the dynamics of this new asset will have a role in Cosan's portfolio.

{kind=link}

Cosan's highlights considering all holding positions (Investor Relations)

Assessing Cosan's financials and past returns

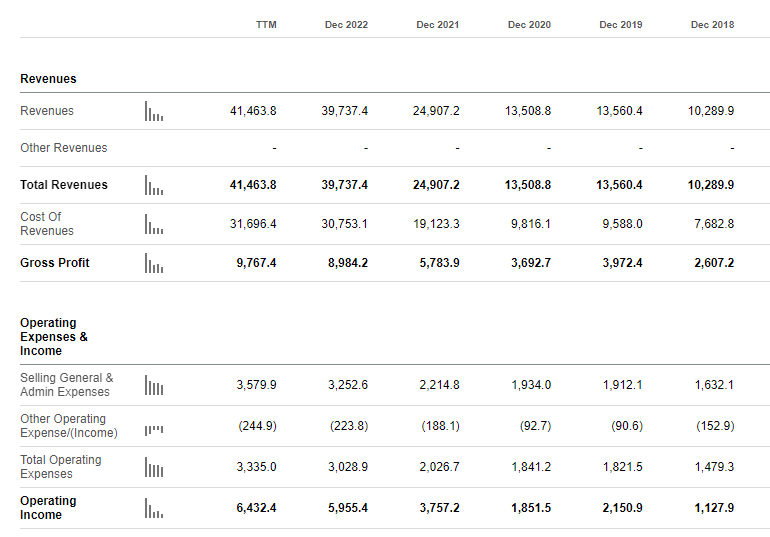

First, let's analyze the company's inflow over the past 5 years. We can see from the image below (all figures in R$) that Cosan is the perfect example of steady revenue growth, jumping from a "mild" R$ 10.3 billion in 2018 to over R$ 41 billion in the last twelve months. This historical income statement displays the effectiveness of Cosan's portfolio building over the years and how it became a Brazilian giant. These great inflow results and steadiness go up to the EBITDA and Operating Income lines of the income statement, showing that the company's operational segment has been indeed well-managed and executed over the years, indicating responsible corporate governance all around.

{kind=link}

{kind=link}

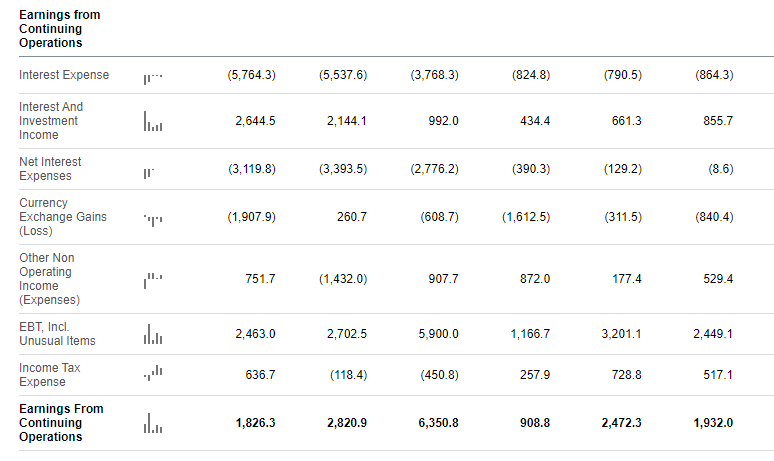

Now, all this growth didn't come organically through the generation of cash flows only. Cosan's management has its merit for all the past results, but we have to deeply take into account the company's indebtedness within the period to get where it is now. When we take a closer look at the Interest Expense line, we see that it wipes out most of the company's Operating Income, getting to a level where the Net Income doesn't have the same steadiness as the revenues or EBITDA, and even reporting loss in the trailing twelve months.

{kind=link}

{kind=link}

Cosan's leverage level, despite being high, is manageable, as you'll see later in this article. So, even though it's still considered a potential risk, investors shouldn't be that worried. Once again, the company seems to know pretty well what to do with the incoming cash flows, and the debt can be approached as just a means to a fruitful end, just like it's been happening until now.

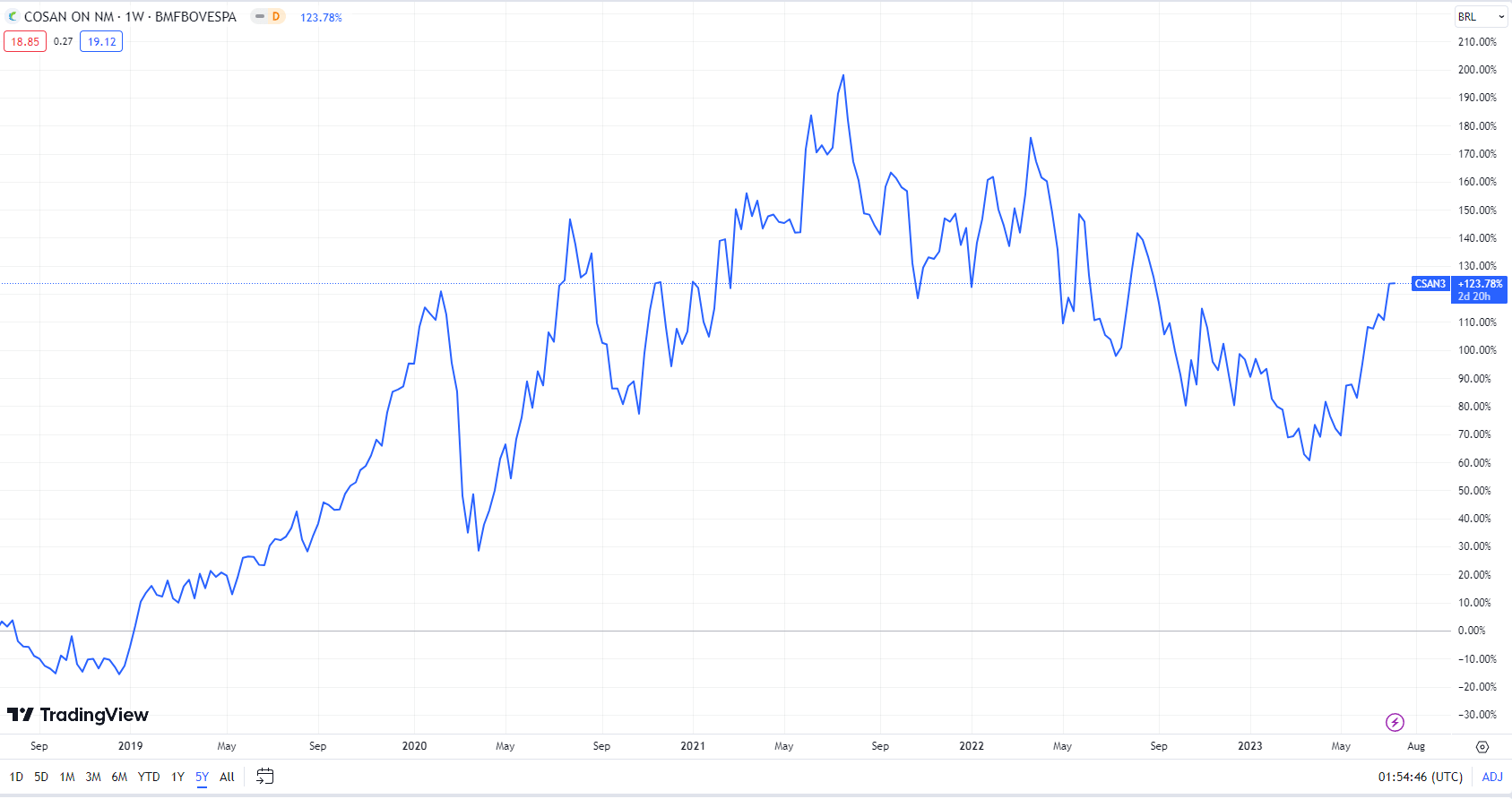

As a matter of fact, Cosan's managed to deliver +123% in BRL and +88.37% in USD over the past 5 years. These returns are not fantastic but they are far from poor, especially for Brazilians that use BRL on a daily basis. But, the key point to pay attention to here is that Cosan is trading at the same price as 2020, as you can see from the chart, only that its revenue and EBITDA now are 3x and 4x higher than that year, respectively. This, combined with the price multiple comparisons I'll be performing in the next section, surely strengthen the buy case that this investment thesis is trying to display.

{kind=link}

PS: I'm using the ticker CSAN3 in the TradingView chart above because Cosan's ADR was only listed in NYSE in 2021, so I couldn't use the usual ticker CSAN to fetch data before that year.

Valuation and why Cosan is a great option now

Before we move on to the fundamentals of why I believe Cosan is a great buy opportunity now, let’s analyze some of the company’s price and growth multiples . According to last quarter’s result , Cosan had a non-recurring event that ended up affecting the company’s net income in the books, but had no impact on cash. Here is a fragment from the last earnings call transcript so you can comprehend the situation in detail:

“Net income for the quarter decreased due to the negative impact of mark-to-market update of Vale and also Cosan’s shares due to the total return swap in the financial result and also due to the impact of the provision related [exclusion] of the tax on circulation of goods and services, [SME] asset, benefit in the corporate income tax and social contribution on net income calculation basis recorded until then at Comgás and Moove. It's important to highlight that these are non-cash effects.”

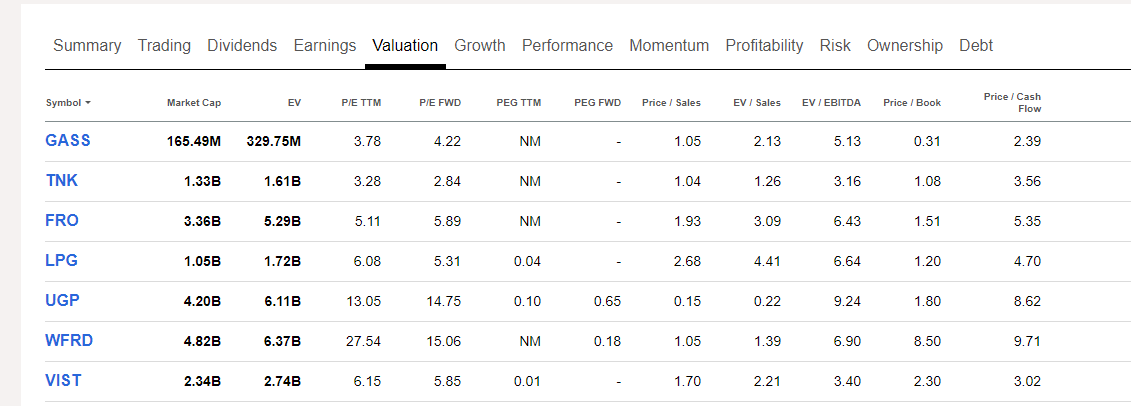

With that in mind, all multiples that consider the trailing twelve months will be greatly distorted, therefore the FWD variations will be the best options for now. As I write this article, Cosan is trading at remarkably low EV/Sales and Price/Sales ratios, sitting around 0.52x and 0.20x, respectively. These figures are quite low on their own already, which tells me that the market is already forecasting robust growth in the medium term. And they can get even lower when compared to the sector median (see first image below), indicating that Cosan might be undervalued against its peers, like StealthGas Inc. ( GASS ), Teekay Tankers Ltd. ( TNK ), Frontline plc ( FRO ), and others (second image below).

Cosan's price multiples (Seeking Alpha)

{kind=link}

Valuation metrics of stocks in the Energy sector (Seeking Alpha)

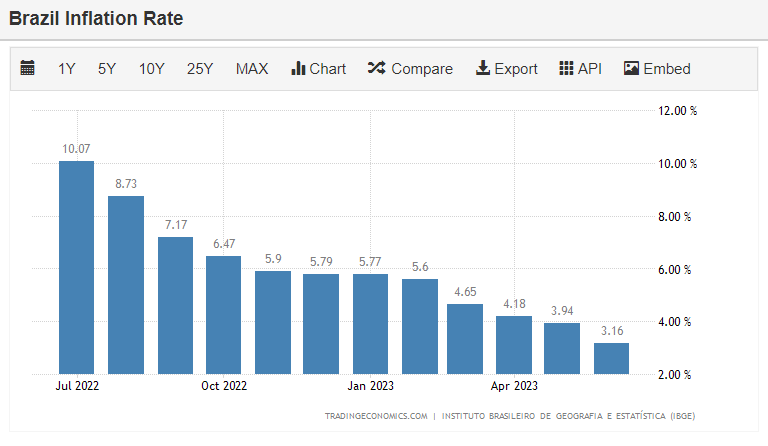

In my opinion, these considerably low forward price multiples are the market pricing in the probable dovish scenario in the Brazilian economy. As of now, the national's interest rate, the Selic rate , is at 13.75%, which is historically high for the country and incredibly high when compared to any developed economy. Since the national CPI seems to be managed to a certain degree, I feel that the market is predicting cuts in the Selic rate by September this year already, which would probably be the first of multiple cuts ahead. These cuts would definitely provide a dovish environment for businesses in the next years and probably drive the entire economy and stock market up, including all companies in Cosan's holding portfolio.

{kind=link}

In addition to that, this decline in interest rates will probably lead to Cosan’s deleveraging, thus reducing the company's debt burden. Also, the company’s underlying assets will naturally get more valuable, reflecting on the share price. The lower interest expenses might also free up cash that can be used to invest in new ventures or opportunities.

It’s also important to note that Cosan plans to have all its subsidiaries publicly listed, and that Compass and Moove still remain privately held. Similar to what happened with Raízen in 2021, in my view, a potential listing of companies could bring value to Cosan. When it comes to liquidity, I also believe that Cosan would not need to let go of any of its assets to meet its debt obligations.

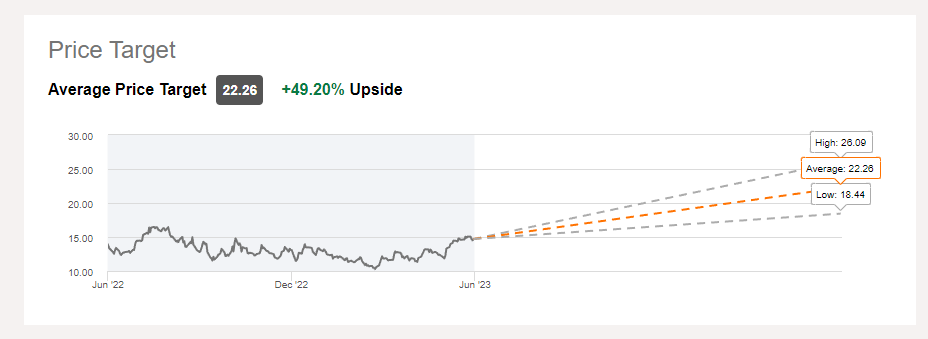

Now, to wrap up my stance and to show that it's in line with the market, Wall Street analysts set the average price target at US$ 22.26, providing a +49.20% upside. And the best part is, even in the pessimist scenario of US$ 18.44 per share, it still poses an upside of around +25%. Seeking Alpha's Quant Rating mechanism might not be as optimistic as me and Wall Street, but it still marked Cosan as a hold case for now, showing that, even in the worst-case scenario, holding CSAN shares is a viable option.

{kind=link}

Cosan's price target according to Wall Street analysts (Seeking Alpha)

Potential risks not that risky

One of Cosan’s potential risks is definitely its large exposure to commodities cycles, especially with the new stake acquisition of Vale. The good thing is, Vale is the largest and most dominant mining company in Brazil, and most of its revenue is generated internationally, so a natural currency hedge surely adds a layer of safety to the holding.

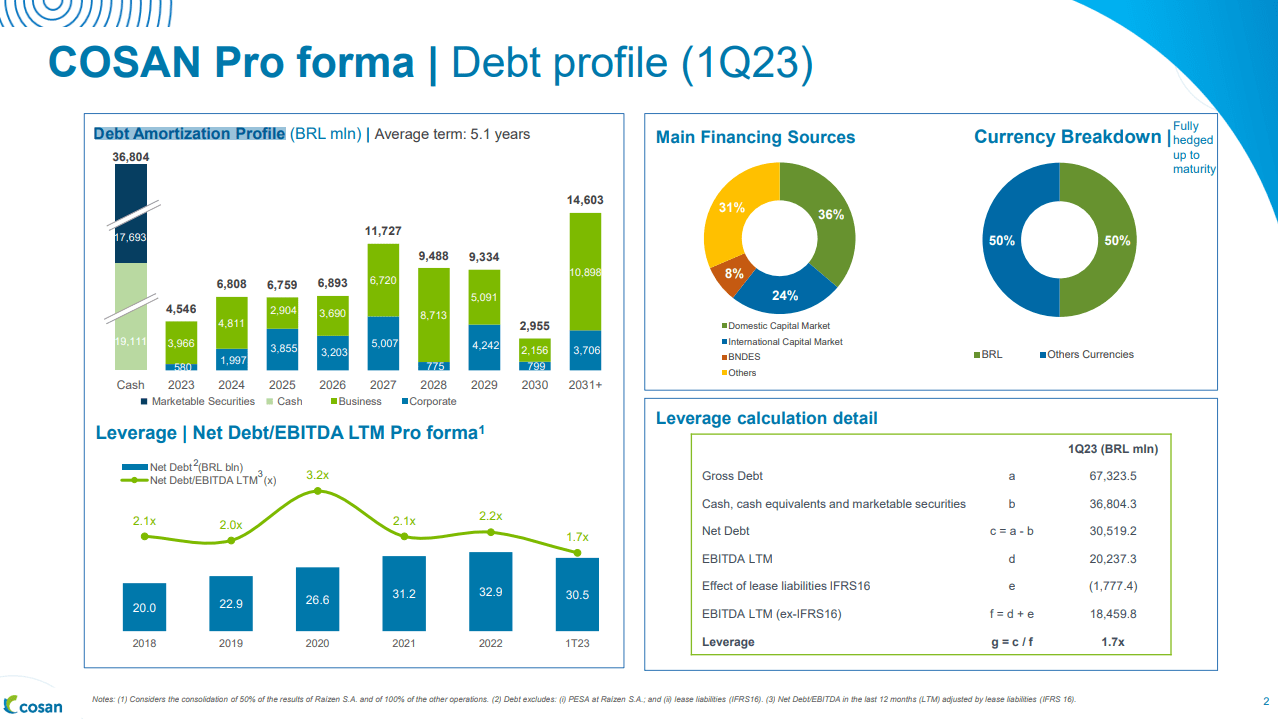

But, in my opinion, the most relevant factor investors should be paying attention to is Cosan’s indebtedness level , which, as I write this article, is considerably high at US$ 11 billion. But even so, the business diversification Cosan has, the “steady” cash flows generated from Compass, and the marketable securities available make the company more than capable of handling this leverage. This can be easily seen in the image below, which shows the company's debt amortization profile.

{kind=link}

Investor Relations

Those factors were definitely accounted for by Fitch Ratings, who just recently assigned an AAA National Long Term Rating for Cosan’s corporate bond issuing. In summary, the potential risks Cosan offers fall short of the potential upside it has in store, and the debt reduction is currently the main value-unlocking trigger for the company’s shares. As the company's debt reaches lower levels, it is likely that equity will have more room for appreciation.

Conclusion

Cosan's portfolio offers a very interesting diversification of businesses and sectors within the Brazilian economy. Furthermore, the companies within the Cosan group have growth opportunities in different markets and are linked to segments where Brazil has clear competitive advantages, which can be observed in both Vale and Raízen. Regarding Rumo and Compass, not only do they have profitable businesses, but they are also well-positioned to capture avenues of growth and benefit from deleveraging processes.

From a valuation perspective, Cosan's current Price/Sales and EV/Sales ratios are notably low, suggesting potential undervaluation compared to its peers. The market's probably expecting considerable growth in the medium term, and the macroeconomic scenario, including potential interest rate cuts, may further benefit the company's deleveraging and increase the value of its underlying assets.

One of the potential risks for Cosan is its exposure to commodity cycles, particularly with its stake in Vale. However, Vale's dominant position in the mining industry and its international revenue generation provide a natural currency hedge and add a layer of safety to the holding. Although Cosan's indebtedness level is currently high, the company's business diversification and steady cash flows from Compass contribute to its ability to manage the leverage.

Overall, the potential risks associated with Cosan are outweighed by the upside potential it offers. As the company continues to reduce its debt, there is room for equity appreciation and significant shareholder returns.

For further details see:

Cosan: Undervalued And Potential Upside In The Near Term