GSL - Costamare: Diversified And Growing Shipper Strong Buy

2023-04-11 05:16:20 ET

Summary

- Container leasing companies are unloved by Mr. Market.

- Costamare is a hybrid of containers & dry-bulk ships.

- CMRE has a healthy balance sheet & significant growth prospects: CMRE stock is a strong buy.

Introduction

Costamare (CMRE) is a medium (to large) sized container leasing company, that has recently expanded into the dry-bulk shipping space. It has a very strong container-ship backlog; it owns a dry-bulk fleet; and is now expanding rapidly.

I think Costamare is significantly underpriced, as it is slightly difficult to understand. And I rate them as a strong buy.

Who are Costamare?

CMRE is a medium/large shipping company. They currently own 117 ships, 72 container ships and 45 dry bulk ships. That makes them one of the largest listed shipping companies out there.

They've been active for 49 years, so far. For most of their life they were a container-ship company, and in recent years they've expanded into dry-bulk. CMRE pays a reasonable dividend yield, and management owns a considerably large share of the company.

I think most investors would be initially sceptical of CMRE: a Greek shipping company, with management heavily invested in the company. However CMRE doesn't have a history of mismanagement, and the stock looks to offer considerable value today.

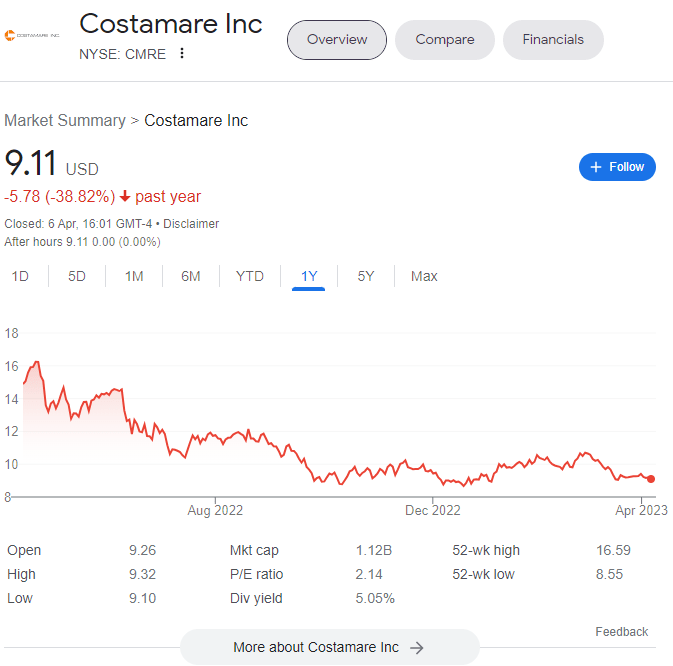

The share price

I think it's important to always start at the share price, and how the stock has performed. This graph shows us the share price of CMRE over the past 12 months. -40% tells its own story!

{kind=link}

Yahoo finance

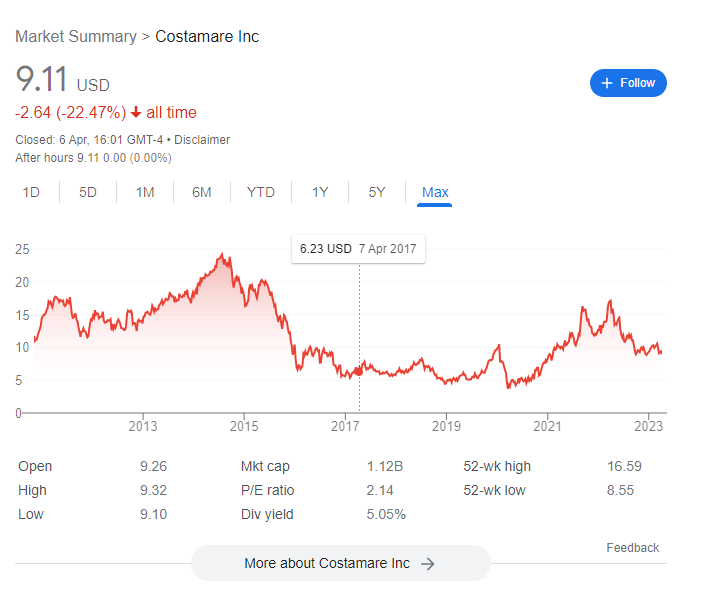

And this shows the performance since 2010:

{kind=link}

Yahoo finance

Obviously neither graph paints a particularly pretty picture. So I do wonder - is now a reasonable time to enter the stock?

What is the company worth?

CMRE is - in shipping terms - a large company.

The current stock price, at just over $9 per share, gives a market capitalisation of $1.12bn

The below is a snip of their balance sheet, as at 31/12/2022. Sourced from their Q4 earnings release.

CMRE Q4 earnings release

CMRE has current assets of nearly $1.1bn. Compared with a market cap of $1.1bn! This clearly looks like a tremendous amount of ready cash for a company of this size.

On the liability side, they have $2.75bn of current + non-current liabilities.

We need to consider their preferred equity as well. They have around 15mn total preferred shares issued. Assuming it is called at $25, that represents another $375m.

Assuming preferred stock represents a liability, they had $3.125bn of liabilities. Netting off their cash, that comes down to effectively $2bn.

So for $1.12 bn in market price, you get to take ownership of a mixed-fleet of 117 ships, plus some ancillary investments. Taking on $2bn of debt.

So...is CMRE a bargain?

CMRE is big in containers, and growing in the dry bulk area. For a shipping company it is reasonably complicated, so we should go through it relatively slowly. I feel it is unloved for a number of reasons, including:

- it is in the capital intensive industry of shipping

- it is somewhat more complicated than many shippers.

P/E metric

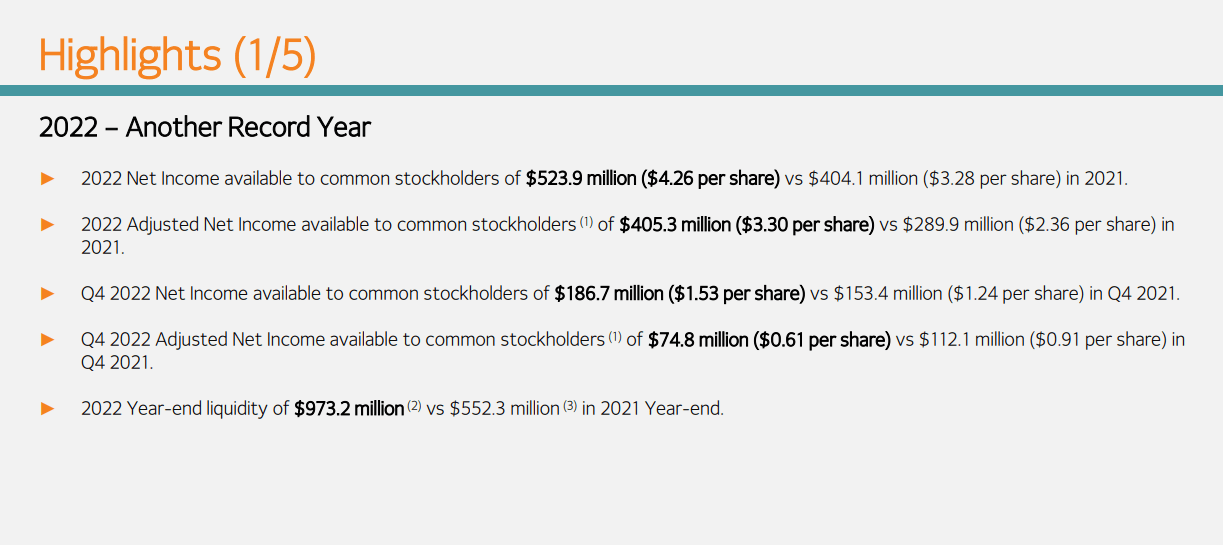

From their Q4 earnings, CMRE earned $0.61 (adjusted) in Q4. And $3.30 (adjusted) for full year 2022.

{kind=link}

CMRE investor presentation

Let's consider that for a moment. Based on 2022 CMRE trades at under 3x earnings.

It must be noted that 2022 was strong for their dry-bulk segment, so that is (somewhat) overstated. However this still implies that CMRE is still exceptionally good value here.

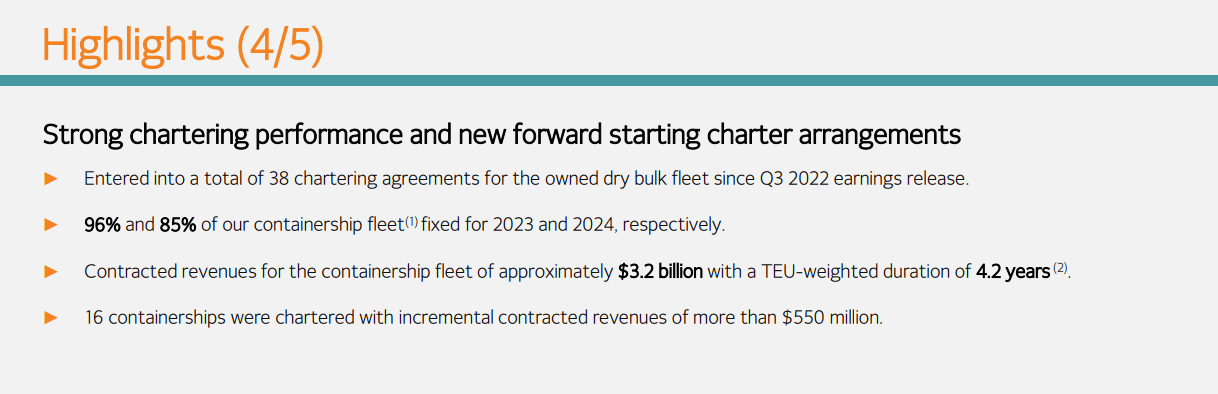

Fleet backlog

{kind=link}

CMRE investor presentation

CMRE has contracted revenues for their container ships of $3.2bn. With employment for around the next 4 years. That's an incredible amount of backlog.

So let's look at what CMRE tells us this will translate into.

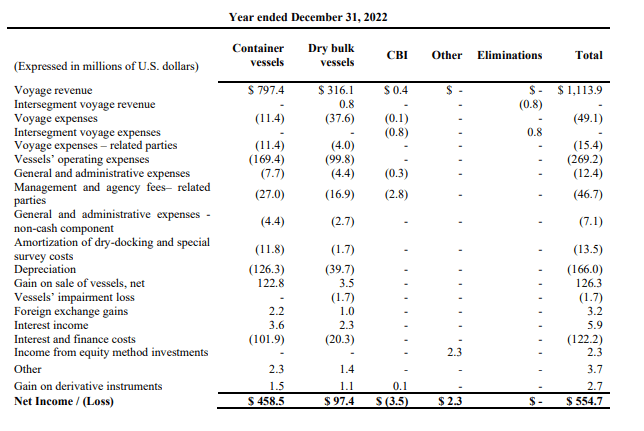

The below is from their 2022 annual report:

{kind=link}

For full year 2022 $797m of revenue in the container space translated into $458m net income. But we need to back out the gain on sales of $122m, leaving us with $336m.

They have 4 years of backlog in place...so in terms of earnings alone, they have $336m x 4 = $1.34bn of revenue. Before we even consider the dry bulk segment, they have contracted earnings of $1.34bn for a company with a market cap of $1.2bn.

Now, let's consider the cashflows. If we add back in depreciation, interest, and preferred dividends for that period:

$126m + $102m +$20m (approx. preferred) = $248mn.

So allowing for 4 years of backlog, they have about $1.34bn + $992m in cashflow due to come in. A total of $2.33bn

Remember, their market cap is $1.12bn, and their net debt is about $2bn. Just considering the containers, you could purchase the entire company of $1.12bn. In 4 years, there would be no debt, and you would own a fleet of 117 ships.

So let's consider their dry bulk investments now:

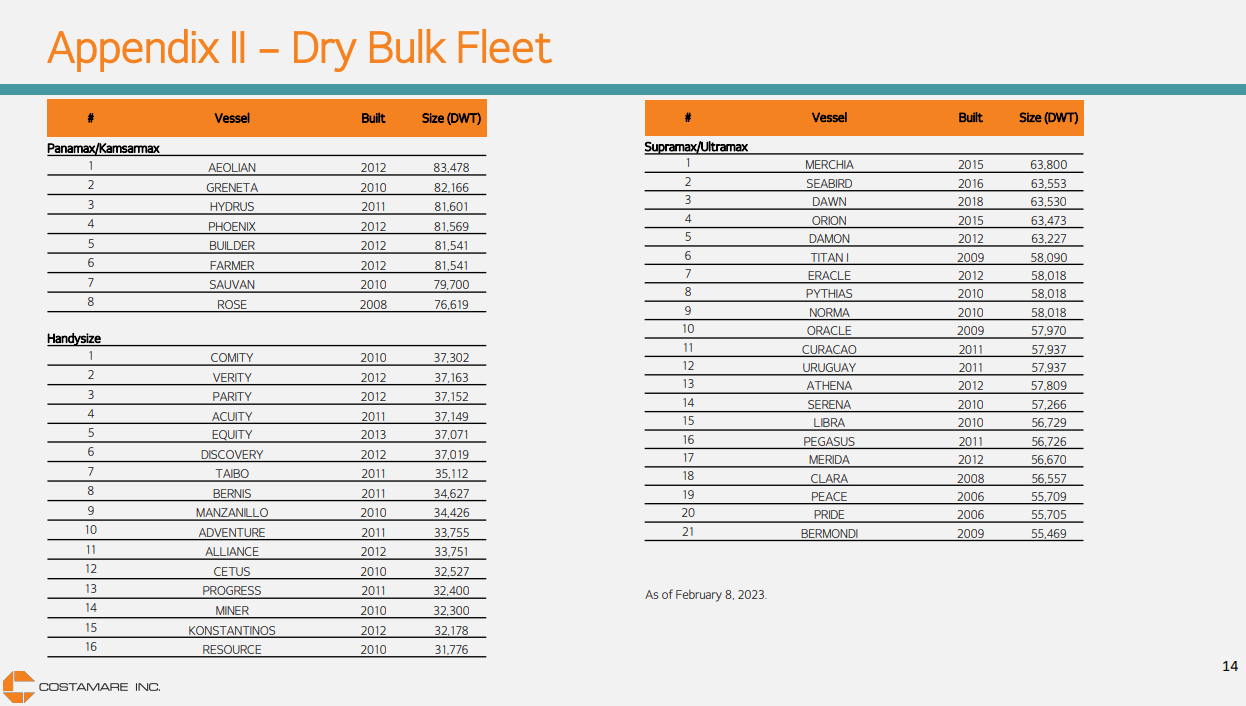

Their owned fleet is below:

{kind=link}

CMRE investor presentation

I don't have an estimate of NAV for these ships.

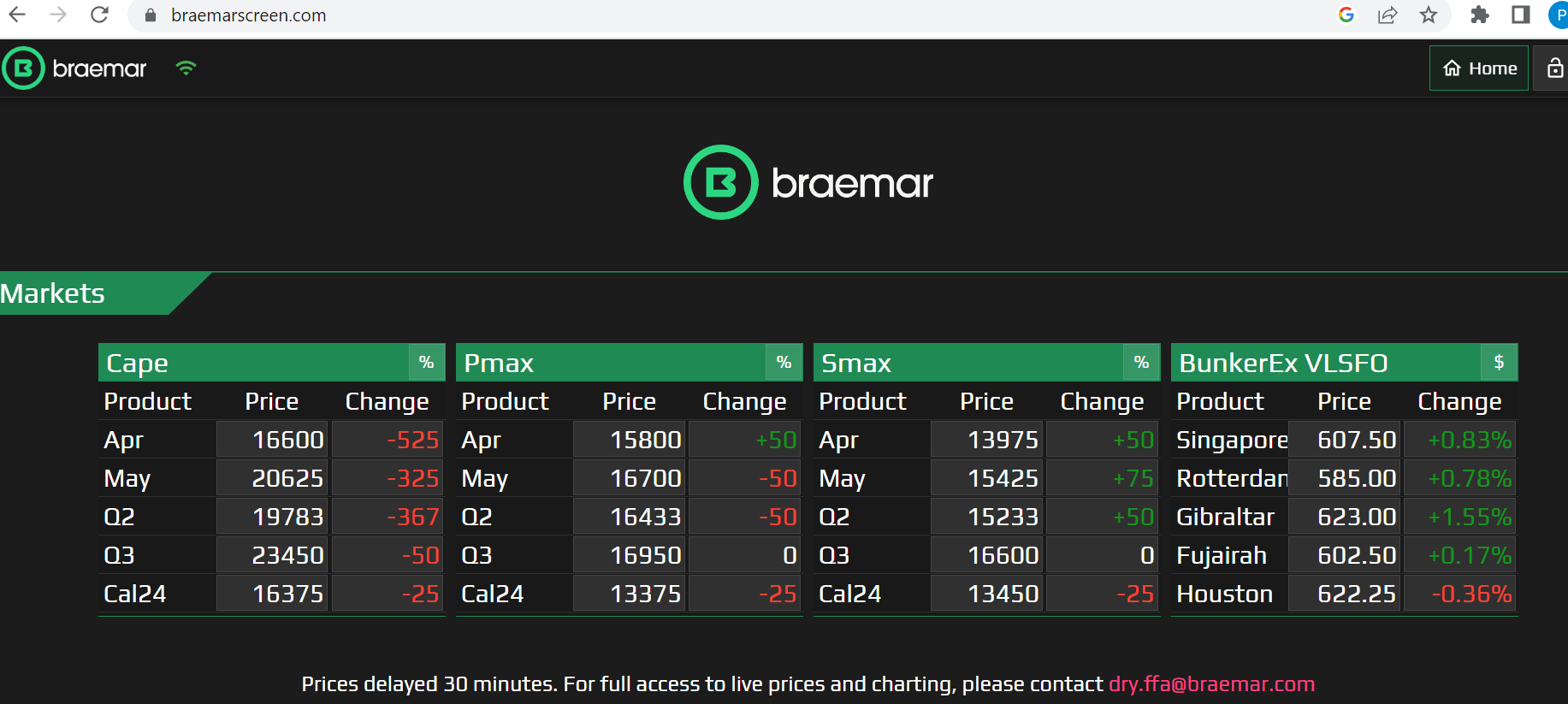

8 Panamax, 16 handysize, and 21 Supra/Ultramax vessels. We can look at Braemar to see the Forward Freight market:

{kind=link}

Braemar

So the Panamax vessels could earn around $15/16k for the rest of the year. And the Supramax could expect to earn similarly. The handymax vessels should earn less.

I would note that Q1 2023 was worse for all vessel sizes. So Q1 will have lower earnings than Q4 2022.

In the absence of a NAV estimate, we should look back at earnings. From the CMRE annual report we can see how much money they are - or aren't - earning on these dry-bulk vessels:

{kind=link}

CMRE annual report

The dry bulk segment certainly was profitable last year. Market conditions have been reasonably positive of late, so I'd certainly expect some significant contribution from this segment towards earnings/cashflows.

Exceptional items after Q4

From their Q4 investor presentation:

{kind=link}

CMRE investor presentation

The carrying value was $31m. So this is bringing in an immediate $79m. That's 7% of the "price" of the company, from just 1 of their 117 ships. Although it is just one ship, I think it goes to highlight that their existing fleet is very valuable indeed.

Other business

Costamare has been very busy of late. Towards the end of 2022 they announced that they would invest more into a new dry-bulk platform. They have not really given a huge amount of details on this except they plan to invest up to $200m into this business. What are they going to do? It appears they'll lease more dry bulk vessels, and subsequently re-let them. They'll then attempt to earn revenue by:

- using FFAs to hedge their costs

- entering into Contracts of Affreightment (rather than more typical leases)

At the end of Q4 they indicated they could expand this platform significantly. From the Seeking Alpha conference call transcript:

Seeking Alpha

And in their annual report, they've indicated they are already up to 42 ships!

CMRE annual report

I don't have much insight here. To be honest, at this point, I don't think there's much we can do but wait to see how they have fared on this front. I don't think we'll see much white smoke until Q2 or Q3 or 2023.

Last...and maybe least...

In addition to their own bulk platform, they've also indicated - in March 2023 - an investment in Neptune Maritime Leasing. Again, Neptune will lease ships and subsequently re-let them. The total investment will be "up to $200 million", but is significantly below that at present:

{kind=link}

CMRE annual report

For the time being, we can simply ignore any impact Neptune would have on CMRE's bottom line.

CMRE - is this a worthwhile investment?

Most shipping companies are simple and easy to explain. Costamare is somewhat more complicated, given that they are now:

- a significant container lessor. With considerable backlog.

- a reasonable owner of dry bulk ships

- a large "trader" of dry bulk ships

- with a very, very healthy balance sheet.

In aggregate, for $1.12bn you get:

1. the container fleet, after the contracted revenue is accrued

2. the dry bulk fleet, from now. This fleet earned $97m last year.

3. the sale in Q1 2023 of just one container-ship, netting cash of almost $80m

4. 2 new, growing, leasing businesses

Strictly speaking, it looks quite apparent that CMRE is very good value, and a reasonably good value investment. They have a healthy balance sheet, and are paying you a well-covered dividend yield of 4.5%

That said, it is unclear whether or not the leasing investments will pay off. And this represents both risk...and opportunity. I think there is sufficient value in the various parts of the business to more than justify the current share price.

Summary

CMRE has some risks. However, it is also clearly significantly underpriced. It has a lower yield than some of its peers like (GSL). And it's also slightly more complicated. But it is growing quickly, has a great balance sheet, and overall offers significant upside. I rate CMRE stock as a strong buy - it could reward a reasonably patient investor handsomely.

For further details see:

Costamare: Diversified And Growing Shipper, Strong Buy