CMRE - Costamare E-Series Preferred Bolstered By Long-Term Charter Arrangements

2023-04-28 11:13:30 ET

Summary

- Charter rates are normalizing, but they're still reasonably high relative to COVID-19 lows, so profitability can be expected.

- They are in the process of disposing some ships in arrangements penned during the tightest of markets in early 2022.

- On top of that, they have pretty long-term average charters right now. The Preferred Series E dividend is defensible for the foreseeable future, also thanks to favorable refinancing.

- They are doing an asset-lite approach in expanding their dry bulk business by chartering in on an index basis for now, but this could also be a speculative platform.

- Still, implied credit rating on the preferred cash flow looks a little low. The Costamare preferreds are attractive, but we think that the company picture is getting blurred by bulk.

The Costamare Inc. (CMRE) 8.87% CUM PFD E (CMRE.PE) are the E-series preferred shares in the CMRE capital structure, sitting at the lowest wrung of seniority just above equity. The business performance signals that the preferred dividend should be pretty safe, and we don't think the implied credit rating for that fixed income-esque cash flow is appropriate.

The company is doing good work, although we aren't so convinced by what's happening with the dry bulk segment, where they are chartering in for now on a pretty low risk basis, but look to be gearing up for more speculative activities around freight derivative contracts. While this is a reasonable thing to explore, especially to insulate from asset value risks by not having to invest directly in new capacity, they are scaling this business fast and the profile is changing from being strictly predictable on the basis of demand and supply dynamics for capacity as shipowners.

Q4 Review

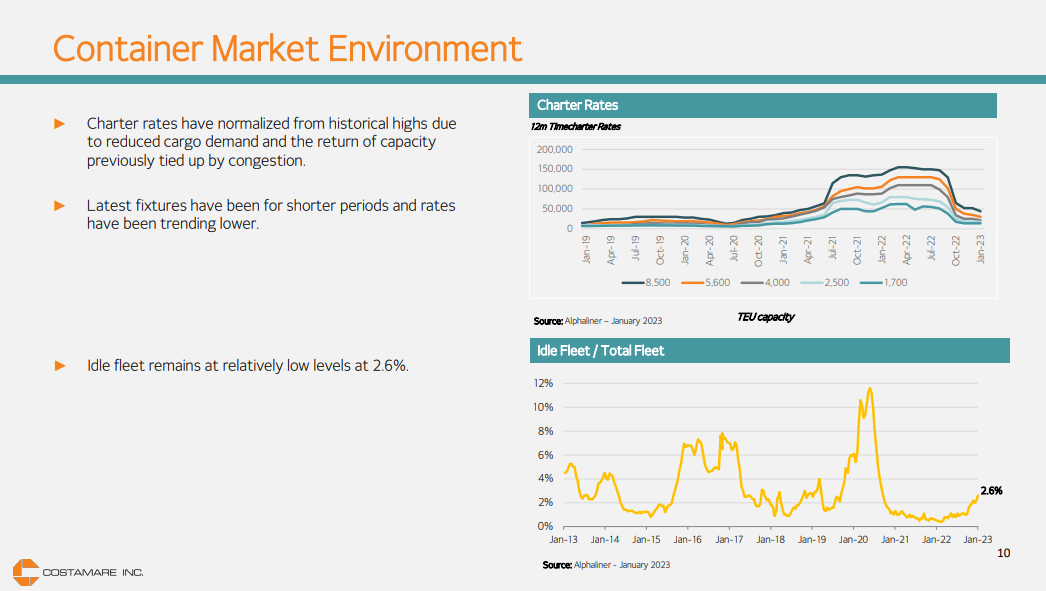

The FY figures were very good, but it is owed entirely to the beginning half of the year. Charter rates have normalized meaningfully, and while above pre-COVID levels, they are not so high anymore. This is consistent with the softening macro, and declines in demand for things like electronics.

{kind=link}

The company was apparently in the process of some dispositions penned at prices in the tight environment, and this should see some nice capital realizations in the next quarter or the one after that. In general, the demand on the markets for ships has fallen, both for containerships and dry bulk, with dry bulk at rather depressed levels still on a historical basis. However, while containership markets are seeing incremental pressure that is unlikely to let up as we come off a goods boom, there is indication of some pickup in the dry bulk market through the forward contracts, possibly from a China turnaround after an awful 2022.

{kind=link}

Dry bulk is broadly speaking a more volatile situation, but they use the dry bulk platform for growing their dry bulk fleet without actually investing, but which can still be volatile in the future since they might start chartering in and selling contracts forward on a basis that aim for speculative gains on hedges. For now they are chartering in on an indexed basis and selling on an indexed basis for a pretty low volatility spread. They are also hedging fuel costs. But this could change in the future. Containerships have been chartered out at quite high rates for the current year and the next year, providing a good deal of earnings visibility for the majority of CMRE's business, ensuring sufficient profitability for the next couple of years to cover the preferred dividends almost certainly. 4.2 years is the average charter duration as of the Q4.

Dry Bulk

The dry bulk platform is worth commenting on. While CMRE would have been viewed by investors as a relatively pure-play ship owner, they are now committing lots of capital into a subsidiary in order to finance the chartering-in of dry-bulk vessels to try to charter them out and create spreads, currently in a pretty safe way. This is supposed to be an asset lite approach, and it is in principle, but it is changing the economics of the business quite meaningfully to becoming more like a liner. There are advantages in that the dry bulk market is a little more uncertain, and CMRE is able to not expand its assets in a period where shipping assets may be too expensive, and indeed management is clear that they are not making moves for new acquisitions right now. However, the changing picture and the need to play the markets on the hedge construction side aren't what all investors want to see CMRE management play at, especially where the company is opening the door to more routinely be trading in shipping derivatives. This is not so wild, it's much like a utility company trading on power hedges, but it's not what all investors want.

So strictly speaking when you have a ship charter on index, there is no real exposure, because it is an index you pay what the market is paying [charter in]. And you get the COA based on market terms [charter out].

However, having said that in the future we may have ships with a fixed rate, again for period.

Greg Zikos, CEO of CMRE

They are definitely looking at the possibility of growing this operations, currently at 23 chartered-in vessels but able to go up to operating 50 or even 100 or 250, which may be an exaggeration in order to point out that scaling this business isn't so difficult. But we do think that this is getting a little too speculative, where earnings volatility is already very high in the industry.

Conclusions

If you use the credit premium model utilized in our last article , the implied credit rating definitely appears a little too low, unchanged since then given the static price and the error range that includes the latest rate hikes.

Valuation (VTS)

With charter rates normalizing, but not cratering, and with a recovery that was better than expected in China, profitability is sustainable considering the fixed arrangements. The dividend appears safe for now over the worrisome part of the coming cycle.

We like that the company isn't aggressively buying ships at highs in the market, but we also want to watch for too much speculation by the company as it expands the dry bulk platform and changes its profile.

Overall, preferred plays like this Costamare Inc. Series E don't look bad, especially with the fact that preferreds offer that duration in a market where we may be seeing peaking rates somewhat soon. However, shipping is still earnings-volatile, and E-series are very low in the capital structure with other preferreds increasing the effective leverage for that tranche (closer to 55% Net Debt/TA). With Costamare Inc. phasing laterally into being a liner and not just an owner, while not inherently alarming, one has to see where all this will go first.

For further details see:

Costamare E-Series Preferred Bolstered By Long-Term Charter Arrangements