SB - Costamare: Sell The Preferreds Buy The Common At 3.2X EPS

2023-07-03 10:30:00 ET

Summary

- Costamare's preferred stocks have performed as expected, maintaining their value while paying high-single-digit dividends. However, the common stock has underperformed despite the company's financial progress.

- Costamare's dry bulk segment may be grappling with industry weakness; however, its containership fixtures should continue to generate substantial profits.

- Costamare's capital returns have been inferior to industry peers, while its investment in Neptune remains speculative.

- Still, Costamare's enormous liquidity, noteworthy future catalysts, and discounted valuation make the common stock quite an attractive pick.

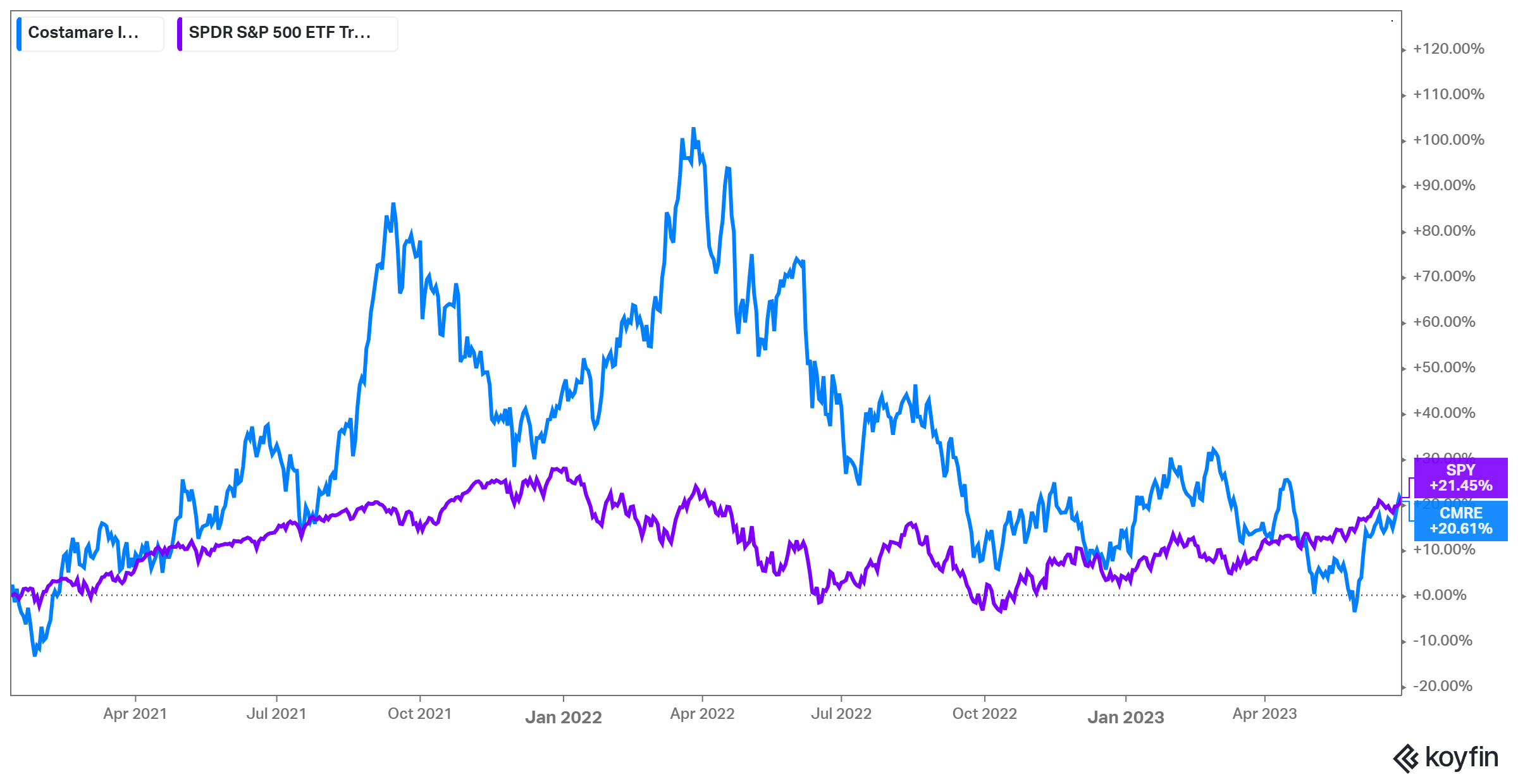

Back in January 2021, I wrote an article explaining how one could combine Costamare's ( CMRE ) preferreds ( CMRE.PB ), ( CMRE.PC ), ( CMRE.PD ), ( CMRE.PE ), along with the common stock to merge the stable dividends provided by the former with the upside potential of the latter.

Since then, Costamare's preferreds have performed as expected, hovering close to par while paying their hefty, high-single-digit dividends. The common stock, on the other hand, has achieved a total return of around 20.6%. While this is a decent return, mostly matching the S&P500's total return of 21.5% over the same period, I believe that Costamare's financial progress during this time is not reflected in the stock's performance.

{kind=link}

Specifically, while the common stock could have been indeed overvalued at its April 2022 peak, it has since given away much of its past gains unjustifiably considering its financial advancements.

In the meantime, with interest rates having swiftly risen by a significant rate since early 2021, I find the 8%-9% yield offered by the preferreds much less attractive. In fact, given that Costamare's preferreds trade above their par values (with dividends accrued, but still...), I believe that selling the preferreds and buying more of the common stock position makes for a smart move.

{kind=link}

Costamare's Recent Financial Progress

Costamare's common stock presents a compelling opportunity due to the mismatch between its performance and the remarkable strides made by the company in terms of its underlying financial progress.

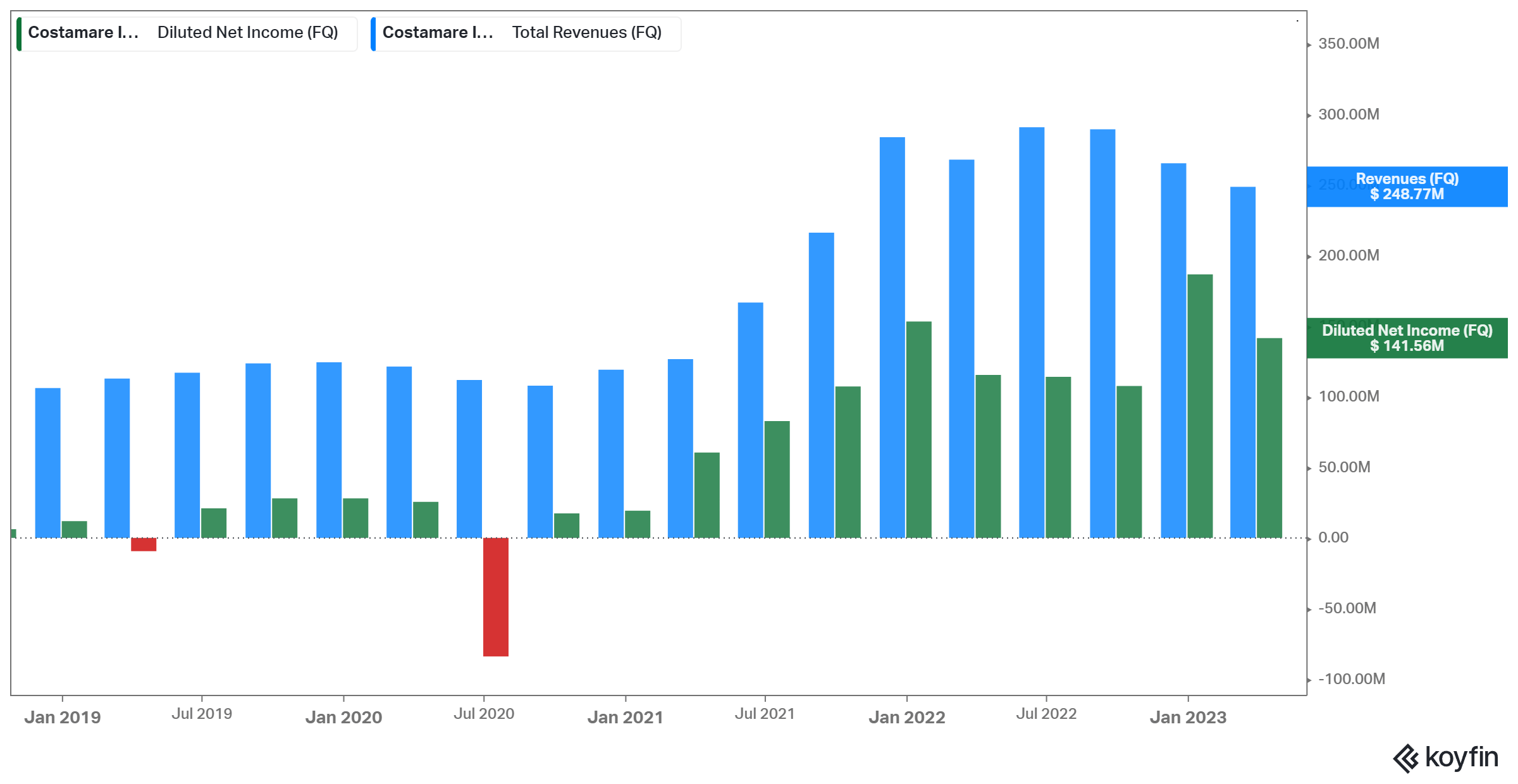

As the underlying chart shows, Costamare has managed to produce exceptional revenues over the past couple of years, extracting massive profits from its high-margin fixtures.

Costamare's Revenues & Net Income in Recent Quarters (Koyfin)

{kind=link}

Revenues have recently lagged compared to their 2022 levels. This can be attributed to the fact that while Costamare's containerships continue to be secured under long-term charters, many of which were negotiated at advantageous rates during the containership boom a couple of years ago, the company's dry bulk fleet, primarily engaged in the spot market, has been adversely affected by the recent downturn in rates.

The Containership Segment

To throw in some color, the image below shows all of Costamare's containerships along with their respective coverage. Their total contracted revenues are roughly $3.1 billion, with a TEU-weighted remaining duration of 4.1 years. In fact, a decent amount of Costamare's containerships feature coverage that extends post-2030. Hence the company's performance is more or less insulated from its containership segment through the medium term, despite the recent weakness in containership rates.

Costamare's May Factsheet (Costamare)

The Dry Bulk Segment

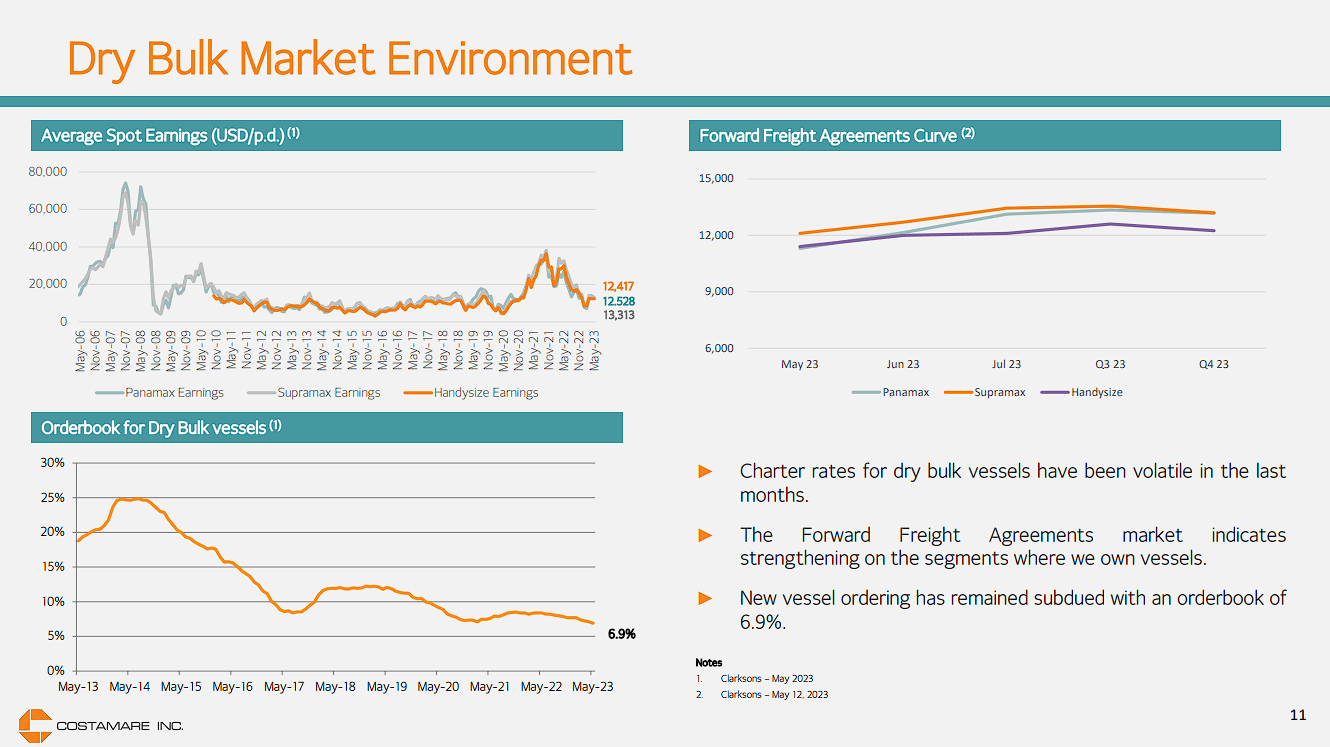

Costamare's dry bulk vessels contributed nicely to profits during the boom in dry bulk rates around 2021. However, rates have plummeted since, which explains the lag in Costamare's revenues in recent quarters. The bullish case for the dry bulk industry is reinforced by the global order book representing a mere 6.9% of the total fleet. This suggests that in addition to the significant number of vessels projected to be scrapped in the coming years, the scarcity of available vessels has the potential to propel dry bulk rates upward.

Nevertheless, it is important to note that the demand for dry bulk remains insufficient, likely due to China's construction industry (which predominantly drives dry bulk rates) remaining soft. Until there is a substantial increase in demand that coincides with the constrained vessel supply, it is likely that dry bulk rates will continue to remain at lower levels.

{kind=link}

Management intends to continue expanding Costamare's dry bulk platform, which could position the company ideally if dry bulk rates do indeed rebound in the medium term. Otherwise, this segment could admittedly keep offsetting some of the tremendous cash flows coming in from containerships.

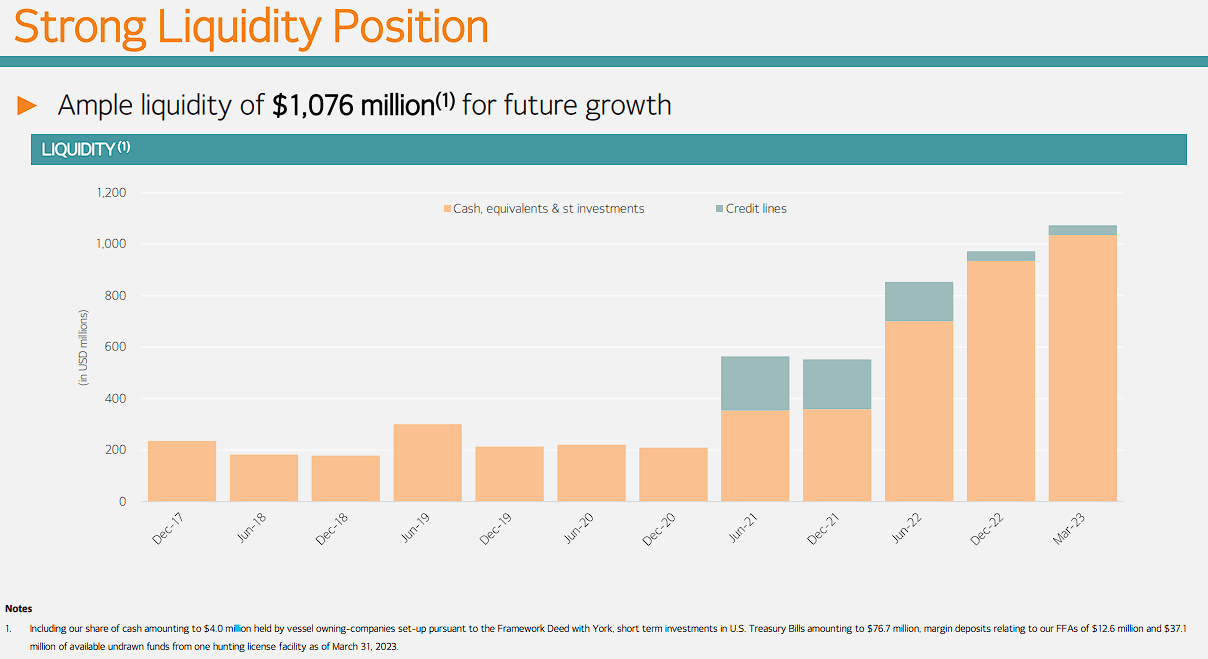

Enormous Profits Has Boosted Liquidity Massively...

Despite the recent weakness in dry bulk, Costamare has managed to post enormous profits in recent quarters, as previously mentioned. At the end of Q1, Costamare's liquidity was close to $1.1 billion, including cash equivalents of $945.6 million, $76.7 million invested in short-dated US Treasury Bills, and $12.6 million margin deposits in relation to its FFAs. To illustrate why Costamare is drowning in cash, the company's market cap currently stands at $1.2 billion, just $0.1 billion over its very own liquidity.

{kind=link}

...But Capital Allocation Has Disappointed Investors

Despite Costamare's massive liquidity, investors have increasingly raised concerns regarding management's capital allocation practices, which I firmly believe to be the primary driver behind the stock's underperformance in recent quarters. Specifically...

Inferior capital returns:

Costamare's inferior capital returns have likely been the most significant contributor to the stock's underperformance. The company has maintained its quarterly dividend to $0.115/share since mid-2021, hoarding massive amounts of cash that could have instead been (partially) shared with investors.

The company did pay a special dividend of $0.50/share in fiscal 2022 but given that more than a year has passed since and that no talk of another special payout has taken, it's somewhat frustrating to see all this cash piling up without us getting paid a more substantial amount. In the meantime, the 5% yield is not enough to spike investor interest, as many shipping companies offer significant yields these days. Even Safe Bulkers ( SB ), whose sole exposure is in the weak, dry bulk space, is currently yielding a heftier 6.1%.

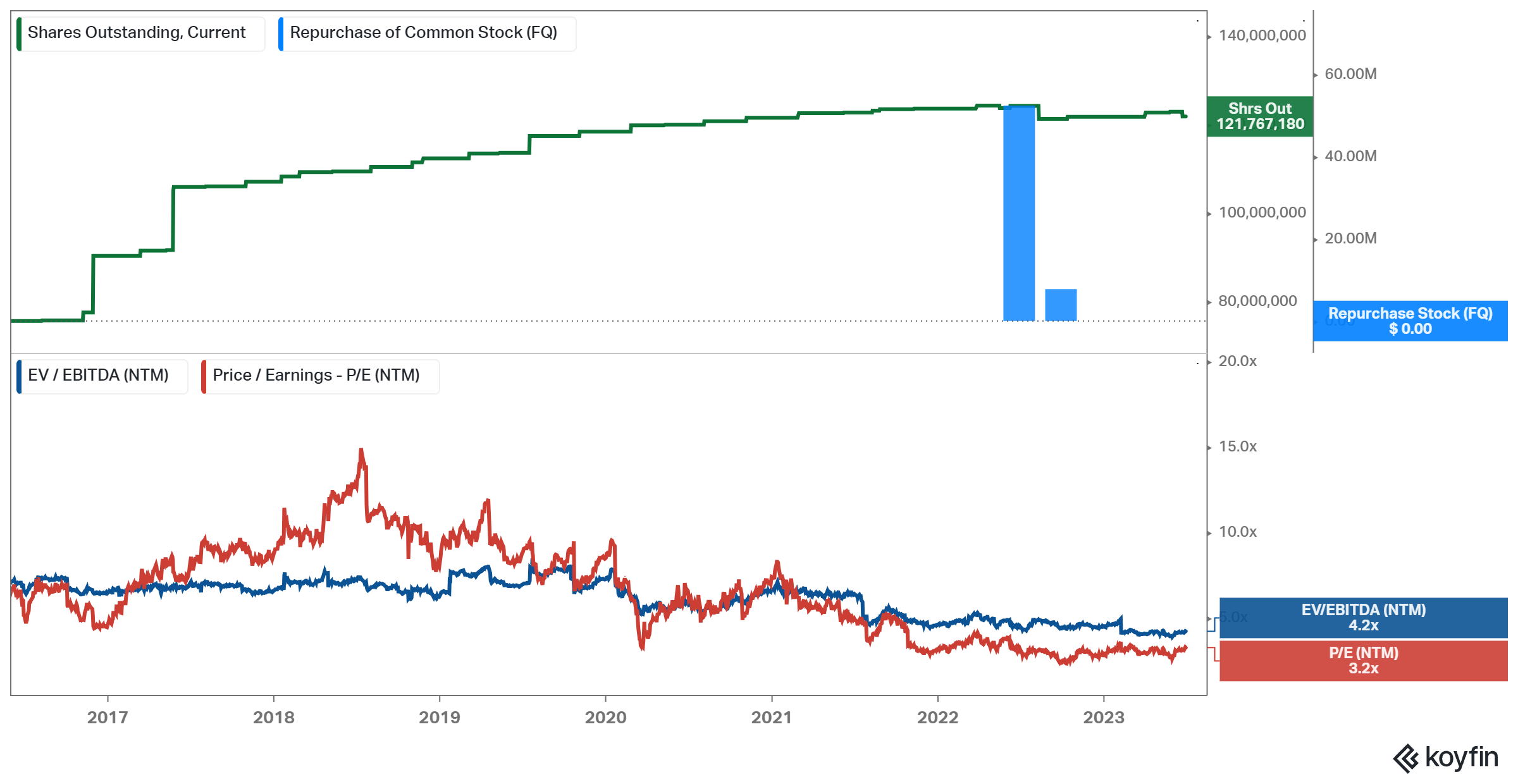

Share repurchases have also been almost absent despite, again, the stock's discount and overall liquidity. In fact, management didn't buy any stock in Q1, despite the decline in share price driving Costamare's valuation multiples lower. At a forward EV/EBITDA of 4.2X and a forward P/E of 3.2X, it's a mystery why this is the case with so much cash sitting on the sidelines.

Costamare's Share Repurchases, Share Count, and Valuation Multiples (Koyfin)

{kind=link}

Investment in Neptune Maritime:

In March, Costamare announced it had agreed to invest up to $200 million in Neptune Maritime Leasing, a growth-oriented marine leasing platform. In the press release, we can read the following:

Considering current asset values, the Company believes that the Neptune Leasing investment is a favourable employment of the Company’s increased liquidity and is expected to provide healthy returns at acceptable risk levels. The new venture is synergetic to the existing ship owning platform and is expected to further enhance the strong relationships built over the last decades with shipowners and commercial lenders in the ship financing sector.

Okay, this all sounds good, but the press release contained no specifics regarding what management expects in terms of ROI and/or other useful metrics. This is important because, with Costamare stock trading at such a massive discount (see below), they should be able to justify that alternative uses of capital (i.e., buying back their own stock) would make for a less accretive option.

Analysts made some efforts to reveal additional insights regarding this investment during Costamare's Q1 earnings call. Regrettably, the available information of practical value was rather limited. So as far as many investors are concerned, $200 million just walked out the door with questionable ROI prospects, while a clear opportunity to enhance shareholder value (buybacks) was disregarded. This also explains the stock's underperformance.

Nevertheless, Switching The Preferreds For The Common Is An Attractive Option

There are definitely solid reasons to be upset about management's capital allocation practices lately. While the stock has performed alright since my initial article, I believe we would have made so much more money had a larger portion of capital been allocated to shareholders.

That said, I do believe that the common stock continues to present a compelling opportunity for several reasons. Firstly, don't forget that despite the recent capital allocation "missteps", Costamare's management remains heavily aligned with common shareholders. Around $145 million has been reinvested by the sponsor family through the Dividend Reinvestment Plan to date. The company's latest 20-F shows that:

- Konstantinos Konstantakopoulos, Costamare's chairman and CEO, owns around 26.3% of the company,

- Achilles Konstantakopoulos, his brother, owns about 17.8% of the company and,

- Christos Konstantakopoulos, his other brother, owns about 16.8% of the company.

From that perspective, it can be argued that management must have filtered actions like the $200 million investment in Neptune in line with their intent to maximize the value of the family's shares.

Further, shares appear to be trading at a ridiculous discount. This is reflected both in the forward EV/EBITDA and forward P/E ratios, as previously shown, but also in the stock's discount to NAV. In Jeffries' April update on asset values, Costamare's NAV/share was estimates to be close to $13.80 , implying shares are currently trading at a 30% discount to NAV.

That's not as massive of a discount as we've seen in other companies in the space (e.g., EuroDry ( EDRY )). Still, given that Costamare is a high-quality company with a proven track record of creating value, I believe that this discount is hardly justifiable - especially given the $3.1 billion in contracted revenues from containerships and the massive liquidity.

Hence, I have decided to sell my Costamare preferreds and allocate the proceeds to the common stock, whose risk/reward ratio now feels significantly more fruitful. I am going to miss their 8%-9% yields, but the common stock's 5% yield + upside potential from multiple catalysts (dividend increase, potential buybacks, special dividend, Neptune actually delivering results, dry bulk rates recovering) seems compelling enough for this switch.

For further details see:

Costamare: Sell The Preferreds, Buy The Common At 3.2X EPS