DSX - Costamare: There Will Be Pain But Much More Gain

Summary

- Baltic Dry Index is down 75% for the year due to monetary policy tightening and global tensions.

- Costamare is diversified across dry bulk and container segments.

- In dry bulk, the company has exposure mostly to smaller vessels, which are associated with a lower degree of rate volatility.

- In container shipping, Costamare has signed longer time charters, thus shielding itself from further rate decreases.

- All of the above, together with a strong cash position and an ongoing share repurchase plan, make Costamare a long opportunity, although there will be ups and downs along the way.

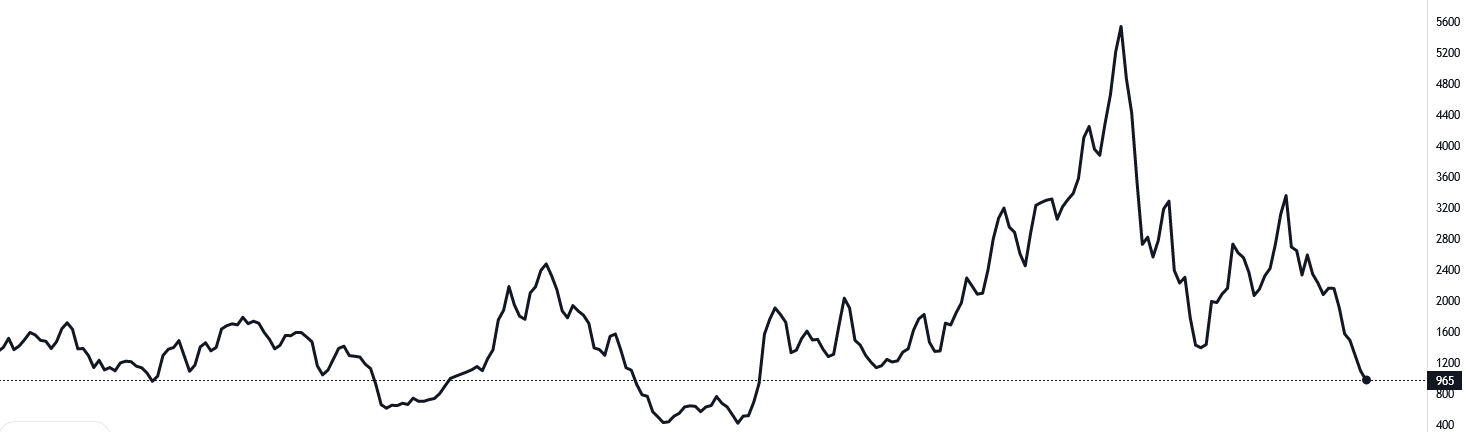

During the last weeks, the Baltic Dry Index has been in a downward trend, which has accelerated in the last few days. As I'm writing this article, Baltic Dry Index has slumped to 965 points, following another 5% decline on Wednesday. As we can see in the graph listed below, these levels were previously seen in early 2020 and late 2019, when the global pandemic was emerging. During these periods, Costamare Inc. ( CMRE ) was trading in the areas of $4.50 and $9, respectively. These figures represent a significant downside from today's price levels.

{kind=link}

So, the question that arises is this: should one sell their interest in Costamare? In the following paragraphs, I will outline several reasons why believe that long-term investors shouldn't.

Exposure in smaller dry bulk vessels

As with every other index, the Baltic Dry Index ("BDI") is comprised of different constituents, tracking the performance of individual vessel types. As one would reasonably expect, larger vessels are assigned a larger weight in the overall index. The recent acceleration of BDI's decline was largely attributed to the very high decrease of the Capesize index. For instance, a couple of days ago, BACI fell by 18% in one day, dragging the whole BDI down significantly. As I've written in some of my other articles here in SA, larger vessels mean higher volatility. We saw this notion being confirmed after Powell's recent statements regarding the continuation of the FED's hawkish policy in a desperate attempt to tame inflation.

Luckily, Costamare's dry bulk segment is comprised of smaller to medium vessels. More specifically, the company owns a total of 45 dry bulk vessels, 16 of which are Handysizes and 21 of which are Supramaxes / Ultramaxes. In other words, 37 out of a total of 45 vessels are small ones. This means that the company's dry bulk segment is somewhat more insulated from the volatility of freight rates and the fluctuations of demand. In addition, such vessels have the ability to dock in smaller ports without loading / unloading infrastructure. This adds to the overall less volatility associated with the rates of these types of vessels.

Long term container time charter contracts in lucrative rates

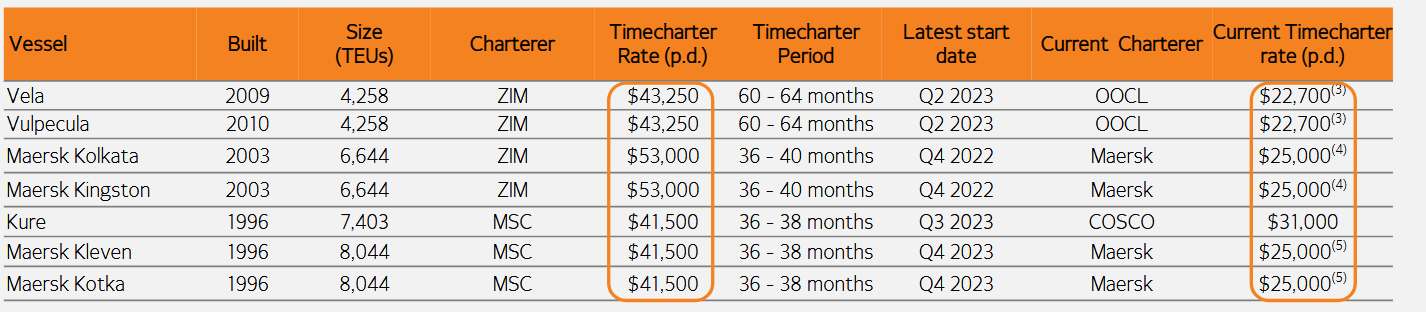

The comparison of the BDI levels and Costamare's share price that I mentioned in the introduction of this article has the limitation that the company also has exposure in the container market. As of July 28th 2022, the company owns a total of 76 container vessels, with an average age of 13 years. The company did a nice job by securing longer time charters when container rates soared some months ago, which resulted in their TEU - based weighted average time charter duration being around 4 years. The key thing to remember here is that they have leased their larger container vessels in contracts expiring anywhere between the next 4 to 8 years.

In addition, the company concluded the renewal of two of their 6.500 TEU vessels, the Aries and Argus, at a rate of $58.5k per day with a duration of 36 to 40 months. Although this figure is higher than the previous one, it is still 50% less than the current 6.500 TEU charter rates . However, the fact that the contract is set to begin in early 2023 and it is a three-year duration are factors that soften the final rate. However, in such troubled times, I am very fond of longer-term time charter contracts, as I've already written before in the case of Diana Shipping ( DSX ). When the market is in a downturn, there's nothing better than having a clear picture of your future returns, even if you have to accept lower rates.

Forward - fixed container ship time charter rates (Costamare's June 2022 Investor Presentation)

{kind=link}

The above are amplified by the potential time charter renewals that are coming in the following months. Taking a look in the company's time charter table, we can see that some vessels are approaching the end of their contracts. For instance, the 4.9k TEU "Oakland," currently chartered to Maersk for $24.5k per day, will be rechartered in March 2023. We're looking at almost 100% potential increase in the real time charter rate here. Or the 4.5k TEU "Androusa" vessel, made in 2010 and currently also leased to Maersk for $22.75k per day, has a lease that expires in May 2023. Combine that with a very low idle container fleet availability and you have some nice freight rates, able to sustain profitability for Costamare. This is why the company took the decision to forward-fix some time charter rates in some of their older vessels, which is something that I totally agree with.

Nice and strong balance sheet

The company has done a nice job in protecting their liquidity, which, in my opinion, is of crucial importance for companies operating in a cyclical and seasonal industry, such as shipping. At the end of Q2 2022, the company had a total of $688 million of cash in hand, together with another $152 million available from other sources. The company's financial position is to be enhanced further, with the sale of 5 of their container ships in the following months, with anticipated proceeds of $333 million. Moreover, Costamare recently secured a $500 million syndicated loan facility and refinanced existing debt on 17 of their vessels. Finally, the company has an ongoing share repurchase plan with $90 and $150 million remaining for common and preferred shares, respectively. The average common share repurchase price is $12.67.

Conclusions

Despite the recent turmoil in the Baltic Dry Index, I believe that Costamare represents a buying opportunity at these levels. Volatility will be high, but lower than peers which have exposure in larger vessels. In addition, the company offers a nice degree of diversification between dry bulk and container shipping. While there are some older vessels in their fleet, management has shown a tendency to divest from older vessels and invest in newbuilds.

While there will be definitely some volatility along the way, especially in the beginning of 2023, all these factors, together with a strong cash position and an ongoing share repurchase plan, make this company a nice, long opportunity for the medium to long-term investor.

For further details see:

Costamare: There Will Be Pain, But Much More Gain