REAX - CoStar: Deserves A Premium Multiple But Not This Premium

2023-07-07 08:24:58 ET

Summary

- CoStar owns the most popular commercial real estate database, research, and advertising platform, which earned $837m in revenue in 2022, the bulk of the company's total revenue.

- This platform allows CoStar to maintain higher margins when compared to others in the real estate tech industry.

- This sustainably higher margin and potential long-term growth due to the size of the real estate market lead me to believe it deserves to trade at a premium multiple.

- However, at 35 times my estimate of 2027 normalized earnings, I rate the stock a sell.

- In this article, I'll discuss how industry dynamics, CoStar's various business segments, the current valuation, and my forecast bring me to a sell rating for the stock.

One thing I've learned in my time covering businesses in the real estate technology industry is that competition is fierce. I covered Redfin Corporation ( RDFN ) last August , Anywhere Real Estate Inc. ( HOUS ) at nearly the same time , Zillow Group, Inc. ( Z ) about 18 months ago , and eXp World Holdings, Inc. ( EXPI ) in this recent article (among many others), and one thing they all have in common is that they operate in a space that is intensely competitive. This leads to reduced pricing power, higher maintenance expenditures to maintain market share and growth, which in turn leads to lower margins and cash flow.

I've also found that the most profitable companies in this space are the ones that own the most popular platforms. Owning these sites that command the most clicks and eyeballs is the most sure way in this industry to earn relatively higher margins.

CoStar Group, Inc. ( CSGP ) is a good example of both of these observations concerning competition and profitability. It owns what is by far the most popular commercial real estate database, research, and advertising platform. This segment earned $837m in revenue in 2022 which was the bulk of total revenue. They also own the apartments.com platform, which is smaller than Zillow's platform in terms of revenue, but it is slowly growing and gaining share.

The popularity of these platforms has allowed CoStar to consistently maintain higher margins when compared to others in the real estate tech industry. Their GAAP operating margin has been in the 16-20% range since 2017 while Zillow's has been negative in that time except in 2020 and 2021 when it was around 10%. Zillow does not operate in the commercial real estate space, but I would argue that it is the only other company that owns a platform of equal ubiquity, which makes it good for high-level comparisons.

In general, CoStar commands a high earnings multiple due to: 1) its sustainably profitable and popular platforms and 2) its long history of topline growth. The market expects that this profitability and growth will continue well into the future as it currently trades at a trailing 12-month GAAP EV/EBIT ratio of 80. It makes more sense to consider a normalized earnings multiple with CoStar, but I will discuss that in more detail below. For now, it is worth noting that this GAAP multiple does not paint the whole picture of the economics of the business.

CoStar may deserve this higher multiple, but in my opinion, it is currently too high to warrant an investment. I think this is the case due to the competitive pressures of the industry and the underappreciated capital intensity of the business.

Business Overview

CoStar owns and operates a portfolio of information, analytics, and online marketplaces related to commercial real estate, residential real estate, multifamily real estate, and real estate management. For purposes of financial reporting, CoStar breaks revenue down into the following segments: CoStar, Information services, Multifamily, LoopNet, Residential, and Other Marketplaces.

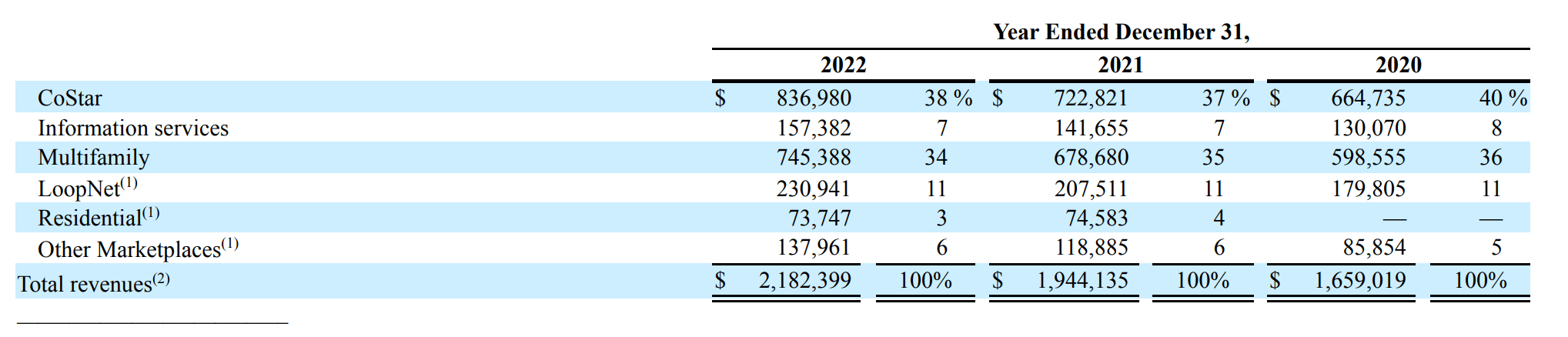

The CoStar and Multifamily segments accounted for a combined 72% of revenue in 2022. While CoStar does not break out segment earnings, I assume that these two segments are relatively profitable and make up the bulk of the business value. Information services make up another 7% of revenue, LoopNet is 11%, Residential is 3% and Other Marketplaces is 6%.

CoStar Business Segments (CoStar Group 2022 Annual Report)

{kind=link}

The CoStar segment generates revenue via a subscription model for its commercial real estate intelligence platform. Multifamily is an ad-based model where property managers and owners can pay to showcase their apartment communities. LoopNet provides a subscription-based model for commercial real estate managers and owners to advertise properties. Residential provides services through Homes.com, which is a subscription-based home listing site that provides real estate professionals tools to manage listings and workflows. Finally, Other Marketplaces consist of sites that provide services to auction commercial real estate, list rural land sites for sale, and list businesses that are for sale.

This is a diversified portfolio of operations and as such, no one client accounted for more than 5% of revenue in 2022, which is an indicator of the quality of CoStar's revenue.

Does it Deserve a Premium Multiple?

The real estate tech industry is so competitive due to the size of the addressable market. Investors and entrepreneurs are attracted to this because the real estate market comprises of trillions of dollars of assets and services, and no single real estate company has its hand in a majority of the total market.

This creates ample opportunities for businesses to try and take small portions of the market. Additionally, because it's an industry built on software, the start-up costs are low. These factors lead to constant new entrants into the market and intense competition over time.

I've covered eXp World Holdings in-depth, and this is a big issue for the real estate brokerage industry in which it operates. Keller Williams first started the agent profit-sharing model, and eXp modified that to a revenue share model. Now, The Real Brokerage Inc. ( REAX ) and Fathom Holdings Inc. ( FTHM ) are both newer brokerages that offer revenue share and are growing quickly because of it. Both the Real Brokerage and Fathom take away from eXp's agent pool and have subsequently reduced eXp's profitability by reducing the effects of leverage from higher scale, and by reducing pricing power.

Notice the consistently negative GAAP operating margins for the businesses mentioned above.

Similar to the brokerage industry, CoStar deals with intense competition from Zillow, Redfin, and new entrants on the multifamily segment of the business. However, CoStar differs in that it has what looks like a monopoly with its commercial real estate intelligence platform. With this, CoStar has maintained a ~20% operating margin over the past few years, far surpassing that of other real estate tech businesses.

This sustainable and structurally higher margin, along with the long runway for growth due to the sizes of the commercial and residential real estate markets, has led the market to assign CoStar a premium earnings multiple. I agree with the market; it deserves this premium, but at the moment I think the multiple is too high to warrant an investment.

Valuation

CoStar's trailing GAAP P/E ratio is currently about 96x. This is a very high multiple, but it doesn't tell the full story. Due to many acquisitions, CoStar generally books a large amortization expense, equal to around 5% of revenue over the past few years. Adding this back to 2022 net income, CoStar's trailing P/E ratio would be 76x. This is still quite high, but I would argue thinking about normalized earnings provides a better picture of CoStar's long-term economics.

To calculate normalized earnings, I estimate that 1% of total SG&A and R&D spend consists of what I would call growth capex. Removing this amount from 2022 net income and subtracting the tax effect from this adjustment leaves the stock trading at 74x times normalized 2022 net income.

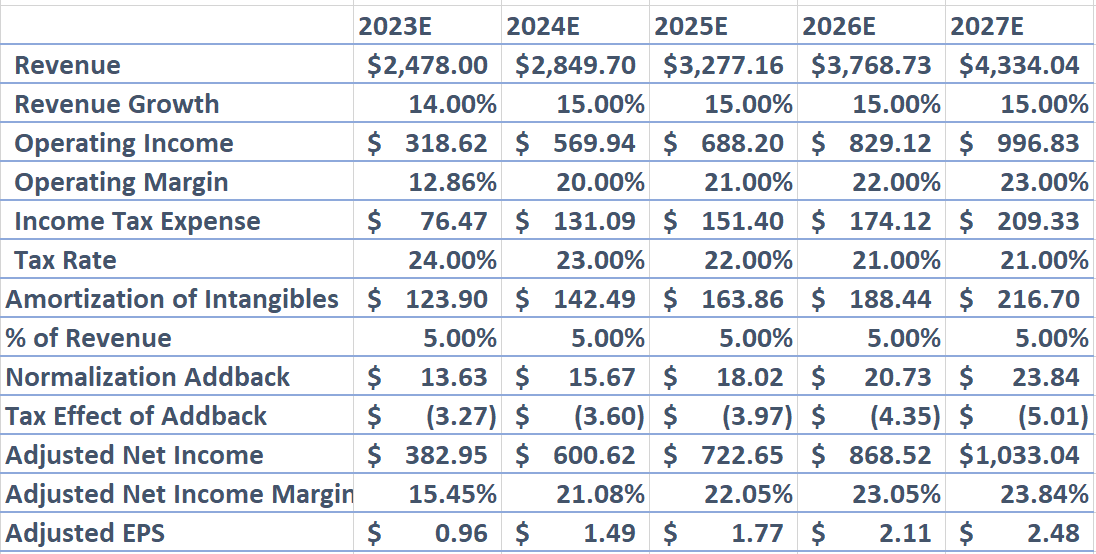

I estimate 2027 normalized adjusted EPS to be $2.48. My assumptions to get to this estimate are 14% revenue growth in 2023 followed by 15% through 2027, a 23% operating margin in 2027, a 21% tax rate in 2027, 416 million diluted shares outstanding in 2027, 5% of revenue as amortization and 1% of the total operating expense spend as a "normalization addback".

Financial Forecast (Created by Author)

{kind=link}

This estimate means the stock is currently trading at 35 times 2027 earnings. This could be reasonable depending on your views of competition, the runway for growth in the real estate tech industry, and the quality of my estimates.

I personally think this is too expensive given what I know about the competitive structure of this industry. While CoStar and other peers in the industry are light on physical capital, they require consistent spending on intangible capital. CoStar has a good history of smart capital allocation in this regard, but I prefer to pay a lower multiple for capital-intensive businesses. I will revisit the stock if it is closer to 25x my estimate of 2027 EPS as this seems more reasonable given the business context, the industry context, and the current overall market multiple.

Final Thoughts

CoStar deserves a premium earnings multiple due to its rare status as a consistently and highly profitable player in the real estate tech industry. This is rare because this industry is not kind to excess returns due to intense competition. New entrants that are attracted to the low start-up costs of a software business and the size of the residential, multifamily, and commercial real estate markets, constantly nibble away at profits and reduce pricing power for all industry peers.

Zillow operates in the residential real estate space as opposed to the commercial real estate space, but it is the business with the most ubiquitous real estate site. One would assume that this would lead to solid profits, but Zillow consistently operates with a negative operating margin, only reaching about 10% in 2020 and 2021. In comparison, CoStar consistently maintains a ~20% operating margin. This sustainably higher multiple and the potential long-term growth given the size of all real estate markets combined, leads CoStar's stock to trade with a premium earnings multiple.

My estimate puts the stock at a P/E of 74x based on 2022 normalized earnings and a forward P/E of 35x based on 2027 normalized earnings. Given the current market multiple and the competitiveness of the industry, which necessitates high capital intensity on intangible assets, I rate CoStar a sell. All else equal, I will more strongly consider an investment in the stock if it is closer to $65.

For further details see:

CoStar: Deserves A Premium Multiple, But Not This Premium